“Bonds are not the place to be these days. Can you believe that the income recently from a 10-year Treasury bond - the yield was 0.93% at yearend - had fallen 94% from the 15.8% yield available in September 1981?”

-Warren Buffet, CEO Berkshire Hathaway (Annual Letter to Shareholders 2021)

“Fixed-income investors worldwide - whether pension funds, insurance companies or retirees - face a bleak future,”

"I think Treasurys at these rates, I wouldn't touch them with a 10-foot pole."

-Jamie Dimon, CEO JP Morgan

Any long-time fan of the NFL (National Football League) is keenly aware of just how much the game has changed. Gone are the days of leather helmets and a herd of players pushing their way down the field, in offenses largely geared toward running versus passing. Why the change? The reason is likely tied to the almighty “buck.” Fans do not want to watch defensive grudge matches with a final score of 9-6; fans like scoring. (I’ll add that a popular and lucrative sub-culture also has emerged in the form of fantasy football, where fans select players and succeed when their players produce offensive statistics.) The overarching theme is the NFL wants action and it comes in the form of high-scoring games, driven by lots of passing.

In order to protect the golden goose, the league has instituted a seemingly endless amount of rules meant to shield the offensive players who score these points. The game has evolved in response to these changes in the rules. Defense is less important and players that score points are more valuable and better protected by the rules. Teams have adapted to this new norm by structuring their rosters and style of play to ensure maximum results under the current rule regime.

This, however, is not a letter about sports, it’s about investing. If you haven’t figured out where I’m going yet, I’ll cut to the chase: The rules in the investment world have changed. The league officials are the world central banks (here in the U.S., the Federal Reserve). The Federal Reserve following the financial crisis has forcefully suppressed interest rates hoping to encourage borrowing and punish savers. The efficacy of this policy move is a contested debate among market observers, with many warning that the end result may lead to a surge in inflation, another outcome that could be very painful for savers.

What I am describing will be a difficult environment for investors. On the one hand, the “officials” are attempting to keep rates very low, and on the other hand, these actions could trigger inflation. All of this leaving investors between a rock and a hard place. As a firm, we have been anticipating these widely divergent outcomes and have been taking steps within client portfolios to hedge against both.

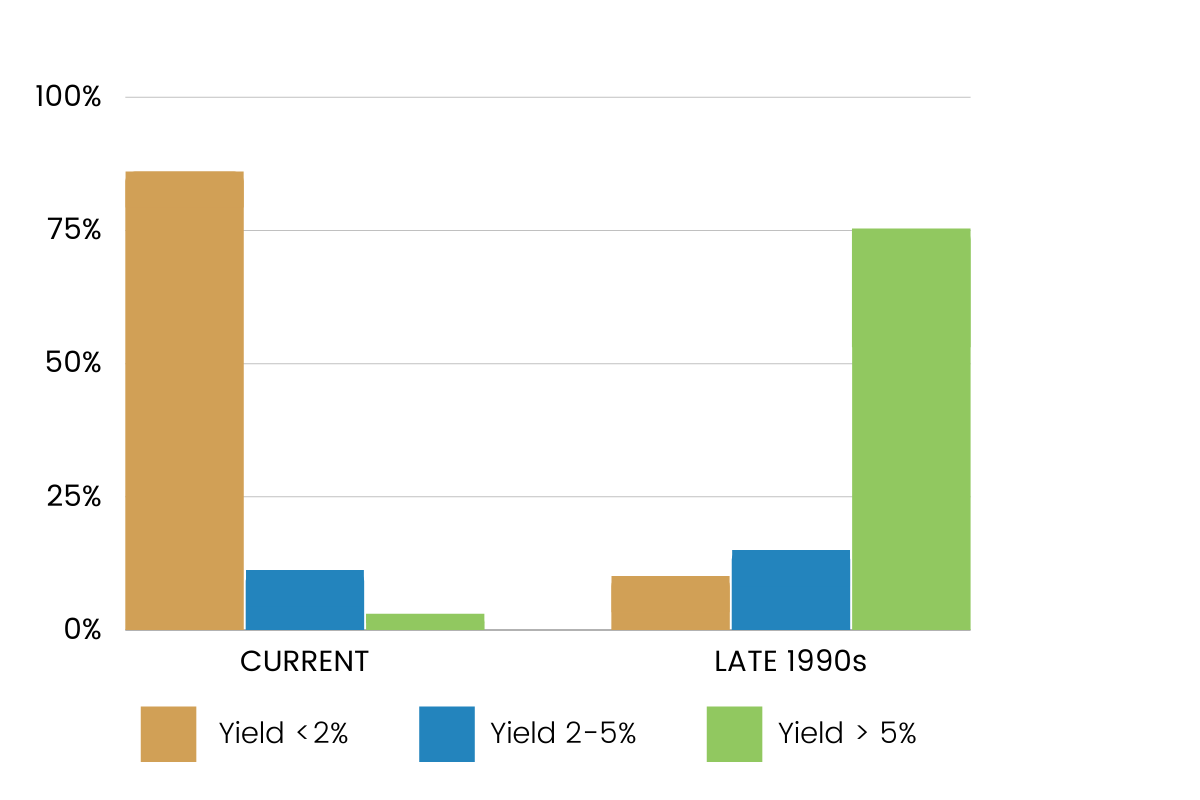

To illustrate my point more succinctly on how effective the Fed has been at forcing rates down, consider the following... As I write this, 86% of the globe's $60 trillion bond market yields less than 2%. Just 3% of the global bonds market yields more than 5%. In the late 1990s, less than 10% of bonds yielded under 2% and 75% of all bonds had yields of 5% or higher. These statistics are jarring for investors, but how we got to this point is a topic for another day and isn’t relevant to surviving in today’s low-rate paradigm.

Bonds have long served a critical role in portfolio management by providing stabilization in stock downturns and offering cash-flow to their owners. With interest rates at all-time lows, there is little to no income to be made. This is a nightmare for investors who rely on portfolio income to provide a portion (or in some cases all) of their cash-flow. It’s an equally challenging situation for many financial advisors who’ve relied on very basic principles for investing in bonds. Think back to the point I made above about the late 1990s where 75% of all bonds yielded more than 5%. Advisors could simply “run the football” and pick from a wide variety of investments that would generate the necessary income for their clients. Today, advisors who have not committed resources to revise their investment process and hoped that the old “normal” would continue are ill-equipped to face the challenges of the current investment landscape.

One of my pet peeves at work is when someone comes to me and lays out a problem yet offers no solution. So, to our readers, I will not simply tell you that investors are facing significant challenges; I will go ahead and outline what can be done to deal with the “new normal”. Here is an overview of what investors can do:

I will dismiss option 1 as I don’t consider hope a strategy, nor do I find the argument that rates are going "back to normal” very coherent. Option 2 is also out for me, as I doubt most investors are eager to meaningfully scale back their lifestyles. This leaves us with option 3: a new game-plan for a new environment.

Fortunately for Evergreen clients, we have been finding creative approaches to income for years and have options to address the current situation. But as one of my favorite sayings goes: “nothing in life comes without a cost.” When it comes to investing, this rings truer than ever. In this case, investing in different asset classes will come with a cost which every individual must carefully consider. Before I begin discussing our prescriptive steps for generating income, let me first outline one thing I hear other advisors suggesting that I do not agree with, and is frankly outright dangerous. The easiest path to ratchet up one’s yield on income securities is to simply take on more risk. So instead of buying a blue chip company bond, an advisor might suggest buying lower-quality bonds that are paying far higher yields. While this should strike anyone as a reckless acceptance of risk, it is what many will suggest. For one, because it’s the easiest way to increase income and secondly because many people simply don’t have the skill set required to do expand their “playbook.” This leads me to the ways we think we can help clients most effectively modify their portfolios to still provide income without adding excessive risk.

Evergreen launched a portfolio we call “Dividend Appreciation” roughly two years ago. It’s comprised of dividend-paying stocks that have sound financials with sound businesses. Dividends, unlike bonds, are generally not taxed at ordinary income rates, offering significant tax savings on the cash-flow they provide. Reallocating a portion of one’s assets to dividend-paying stocks, yielding in the neighborhood of 4%, seems like a sensible way to generate income in today’s world. In fairness, one must accept that stocks are more volatile than bonds and the prices of the stocks can decline (but, as we’ve seen lately, so can bonds). Our philosophy remains focused on high-quality household names that we believe can stand the test of time and have a history of rising dividends. I’d also highlight that dividend stocks could be a beneficiary of a growth to value rotation. Growth stocks have had an incredible run and like most things in markets, trends ebb and flow. If, in fact, the pendulum has begun to swing the other direction, dividend-paying stocks, usually found in the value style, should perform quite well.

After the global financial crisis, banks have stepped back their lending programs. Loans to businesses bring significant regulatory burdens for banks and often aren’t the profit centers they use to be for financial institutions. This has given way to the emergence of the private credit space. This can either be done through investing in a fund that provides credit to companies or by investing directly into a business that is seeking capital. What’s interesting about this space is that it doesn’t necessarily bring with it “more risk.” By risk, I mean the underlying companies which are receiving the money are not too unsound for traditional banks to provide financing but, instead, have opted to source money from outside the public markets. A common misconception in the private credit space is that “if it was a good investment, a bank would have lent this company money.” While this can be the case it often is not. For example, think of a regional electric company that’s been in business for 50 years. This company does $10 million of profit and has a strong financial track record. They decide they want to acquire their competitor whose founder is retiring. The company must borrow $30 million to finance the acquisition. This could be a perfectly legitimate loan that many larger banks may pass on because it’s too small for them. On the flipside, smaller local banks may view the loan as too big for them to stomach despite finding it to be fundamentally a sound loan. This is just one among countless examples as to why “Non-bank” funds are emerging as alternative providers of capital. The type of lending I’ve described is what’s known as “middle market” lending but there are many others such as mezzanine lending, real estate lending, distressed lending, and the list goes on... The key is that one must have an understanding of this space to make sure that risk is being managed appropriately. That being said, there’s tremendous opportunity for those who are equipped to navigate and participate in the private credit space.

Again, there is a cost. In this case, the clearest cost is liquidity. When participating in these types of funds, capital is generally locked up for a longer period of time. Unlike owning traditional public market securities, you cannot exit at your discretion. For many of our clients who do not need to draw on their portfolio immediately, sacrificing some liquidity to earn higher returns is a palatable trade-off.

Given the massive amount of stimulus spending by the U.S. government, investors are closely watching the value of the dollar relative to other currencies. If the dollar continues to weaken, it may be prudent to allocate a portion of one’s bond portfolio into foreign-denominated bonds as a way to hedge currency risk in the U.S. In addition, many foreign countries offer bond yields that are markedly higher than what is available here in the U.S. Identifying the securities in which to invest, as well as the underlying countries, is not easily done. As many readers know, one of the reasons for our partnership with the global research provider Gavekal was to strengthen our resources, particularly when investing outside the U.S. If one can successfully identify a country with a currency that appreciates versus the dollar while also getting higher yields than are domestically available, that is a true win-win. Some Asian countries that run large trade surpluses--versus the chronic and massive deficits the US experiences--also have much lower debt levels. Additionally, they typically offer positive real rates (i.e., after-inflation).

And again, there is a cost. First, this is not easily done. Many investors don’t have the sophistication to perform this type of analysis. Also, if you get it wrong you can lose money on the currency as well as the underlying company’s bond, should it struggle. Further, many investors simply aren’t comfortable deploying capital outside their country of residence. In our view, this creates an opportunity since some people lack the skill to invest abroad and others refuse to do so as a result of home-country (i.e., US-centric) bias.

There are other ways to generate income and to protect against rising inflation aside from the three methods I’ve detailed above. This could be investing in REITs, floating-rate bonds, variable-rate preferred stocks, or master limited partnerships, just to name a few. These are not ‘vanilla’ securities novice investors should attempt on their own; they require specialized knowledge and skill. Fortunately for our clients, these are all categories we have built firm expertise around.

I started this piece with the football analogy of a world in which the rules have changed. Our clients should not fear the rule changes but embrace them. It seems hard to believe that this is just a cyclical event that will soon pass and that the Federal Reserve will step back from its interest rate suppression approach. Shrewd investors will adapt and find other ways to make money. For the past decade, the talk has been, “how are your stocks doing?” In fact, some people may use this current situation as the final straw to abandon bonds altogether, which is no doubt a mistake. Instead, my message is that investors who wish to maintain their lifestyle must adjust and find other investments to supplement the yield they once earned without taking reckless risks. Therefore, the question each client should be discussing is which investments are acceptable compliments to their portfolios and how much they should allocate to them. As a firm, we have been integrating many of these income vehicles on behalf of clients already and will continue to search for opportunities to help our clients protect their cash flows and lifestyles.

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.