“Monetary policy has run its course.”

–Financial Times economics columnist MARTIN WOLF

“The Federal Reserve now believes its monetary policy is normal. That should worry you: If this is normal then the Fed has precious little ammunition for when economic conditions again turn abnormal.”

–The Wall Street Journal’s Greg Ip

“An act of desperation born out of despair over the inability of quantitative easing and inflation targeting to produce the desired results.”

–Richard Koo, Nomura Securities chief economist, referring to increasingly widespread negative yields

“To me, capitalism is irredeemable.”

–Alexandria Ocasio-Cortez, popularly known as AOC

At the beginning of 2018, we initiated a new EVA series titled “Bubble 3.0” with excerpts from David Hay’s upcoming book titled “Bubble 3.0: How Central Banks Created the Next Financial Crisis”.

If you are just joining us in the middle of this ongoing series, which will eventually culminate in a full-length publication, please read the prior installments in the series here:

In this month’s Bubble 3.0 missive, David outlines his concerns with one of today’s hottest – and most controversial – economic theories, which is quickly becoming known by its abbreviation: MMT. Bubble 3.0: Can an Acronym Save the World? will run in two parts, with Part II of the edition running next week on April 12th.

BUBBLE 3.0: CAN AN ACRONYM SAVE THE WORLD?

The speed of light in a vacuum. That’s how quickly a once-obscure economic theory has moved from the dusty wings to center-stage, with all spot-lights trained on it. Ironically, this is the very “exit strategy” that I referred to at the end of the previous chapter of “Bubble 3.0”, “No Way Out”.

For those one or two of you who missed it (ok, maybe add three zeroes to those numbers since we now have about 10,000 readers), when I closed out that chapter, I made an enigmatic reference to a solution many have called secular stagnation. To be clear, much of “No Way Out” focused on the failure of 10 years of radical central bank policies to force higher growth on what has become a slow-growth world—hence, the secular, or long-term, stagnation.

The radical aspect relates to the over $13 trillion that spewed out of the world’s monetary gods’ digital printing presses. It also is a function of forcing interest rates down to zero and then below; as noted in the February 22nd, EVA, there are now $11 trillion of negative-yielding bonds (where the lender pays the borrower, as incredible as that seems) inhabiting the planet. By the way, that number has been growing on almost a daily basis lately, as more and more bonds fall into the negative yield category.

Yet, one of my key points in “No Way Out”, was that it was becoming increasingly obvious these unprecedented attempts at pump-priming efforts had whiffed—big-time. The most salient argument along those lines was that the world looked to be on the verge of another recession. Since then, the evidence of a downturn has only multiplied.

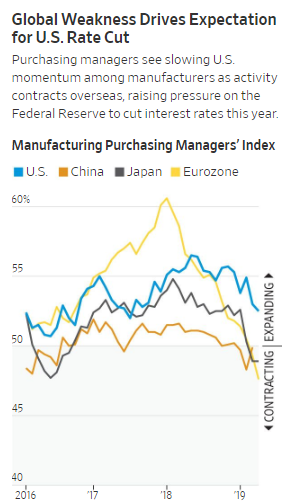

If you’ve been paying attention to the drumbeat of economic data over the last month—and clearly the stock market hasn’t—it’s hard to escape the reality that the trend is not our friend. A proliferation of forward-looking economic indicators—like surveys of global manufacturing purchasing managers and futures market views of Fed rate policy (hint: that would be lower)—continue to tell a consistent story: things ain’t great and they’re getting less great.

In fact, Evergreen has seen enough along these lines to make the reckless bold statement that even the Energizer bunny US economy is likely to be in recession soon. But, how soon, you ask? To quote the esteemed macro-economic thinker, Forrest Gump: “stupid is as stupid does.” Heeding that advice, I’m not going to do anything as foolish as attempting to conjure up an exact date.

With that as a lead-in, let’s refer back to my cryptic closing from “No Way Out”:

“Fascinatingly, though, the main topic for the next chapter of Bubble 3.0 may provide a way out, after all. It’s already beginning to garner significant media coverage with much more likely to follow. To many, it is the only viable exit strategy from this quagmire our dear central banks have created with their fealty to the faulty logic that punishing savers for years and years is a good thing. If you can’t wait a month or so to learn what I’m rambling about…well…sorry. There’s an old show biz saying that you should always leave your audience yearning for more. Just this once, I’m going to follow that advice.”

It’s now time to dispense with the suspense. What I was referring to is the acronym that is taking the political world by storm these days, MMT, officially known as Modern Monetary Theory. (In a nod to the NCAA basketball tournament that is still underway, perhaps MMT should be MMM, as in Modern Monetary Madness. But more on the “madness” line of reasoning to follow.)

Frankly, when I obliquely referred to it in February, I had no idea it was poised to go viral. Equally frankly, I hadn’t heard of it as recently as the start of the year. And, as most of you are aware, I spend rather a lot of time on macro-economic research.

It has also been interesting that in doing an informal poll of Evergreen’s brightest clients, not a woman nor man among them had heard of it—or at least they hadn’t stored it in their memories (which maybe was a sub-conscious form of sanity protection). Therefore, don’t feel bad if you have totally missed the media frenzy MMT has suddenly spawned. But I will assure you most confidently that you will be hearing and reading much more about it in the months ahead.

It’s clearly time for a definition and my best effort at a plain English explanation. One of the most succinct overviews I’ve seen was from Investor’s Business Daily (IBD) in early March. Intriguingly, though, it was buried on page A11. Let me dare to say, this theory will be page 1 news before long. In fact, I believe it is the most electrifying financial thesis to emerge since supply-side economics way back in the 1970s. As this IBD article notes, the basic idea is that since the US can issue debt in its own currency, which also happens to be the world’s reserve currency, it can deficit spend to its heart’s despair delight. Per the IBD, “it can simply print more money when it needs it to pay off its debts”.

If this falls under the too-good-to-be-true category in your mind, please bear with me. MMT advocates assert that, no worries, as long as the Fed keeps interest rates low, like below the increase in GDP (it seems to excel at that these days), AND lower than the growth of government debt (that one’s not so easy in this era of deficits gone nuts), then it’s all good—and not too good to be true.

Perhaps you detect a hint of cynicism in my tone. If so, you are definitely not tone-deaf. But I need to give the in-favor argument a fair hearing. Actually, in an upcoming Guest EVA I am going to present the pro-case from someone whom I truly respect—though, in this instance, with whom I vehemently disagree. But I’m getting ahead of myself…which isn’t that hard to do given the deliberate pace I move as I approach the iconic Beatles’ age of 64 (“Will you still need me, will you still feed me, when I’m 64?”*).

It’s no exaggeration to say that MMT has both strident defenders and attackers. The former point out that the government should only employ MMT as long as it doesn’t create inflation. Considering that inflation is presently melting right along with interest rates around the world, this doesn’t seem like an unreasonable assurance. But more on that later because, to this author, inflation is this theory’s ultimate Achilles heel.

Let’s back up a bit to understand the genesis of MMT. As one critic opined in the aforementioned IBD article, it’s “sort of turbocharged Keynesianism”. If you missed the excellent essay my partner Charles Gave wrote on this topic in our March 14th EVA, you can access it here.

For those, who would like the Twitter version, Keynesian economics dates back to the Great Depression. It was the creation of Lord John Maynard Keynes and its essence was (and still is) that during periods of a collapse in private demand due to a crisis – like the stock market crash of 1929 and subsequent bank failures – the government needs to spend far more than it takes in from taxes. In other words, deficit-spend as much as necessary to revive the economy. Alright, I know, that was a lot more than the max 160-character Tweet but it’s still pretty concise.

As many old enough, like me, to remember watching the Beatles live on the Ed Sullivan show back in ’64 (there’s that number again), we also are at least vaguely aware Keynes’ brainchild was the dominant economic policy in the US, and most of the developed world from after WWII until the late 1970s. (At that point it was superseded by the previously mentioned supply-side theory).

Interestingly, and quite likely most relevantly, its quasi-demise was triggered by inflation. Further, the rampant CPI rises of the mid-‘70s happened at a time when unemployment was soaring. According to the many disciples of Keynes, that was nigh on impossible. (In 1946, the Lord himself went to be with the Lord of lords—maybe—well before his doxology became viewed as the bible of economics). Keynesian theory held that a high jobless rate virtually guaranteed low inflation. But as Charles Gave wrote in the March 14th EVA, another great macro-econ thinker, Yogi Berra, once said: “In theory, there’s no difference between theory and practice. In practice, there is.” (The growing legion of MMT fans out there might do well to remember those sage words.)

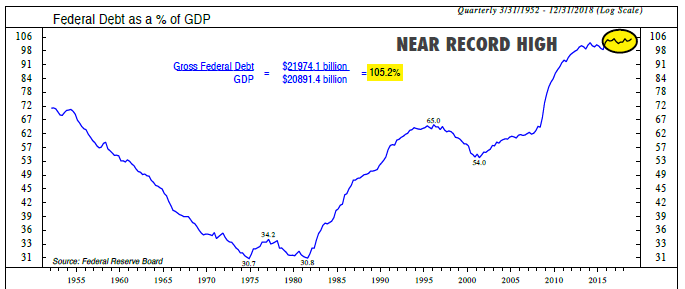

However, a key difference between Keynesian economics and MMT is that the former assumed deficits generated during downturns would be financed by bonds. In turn, that debt would be repaid by surpluses during expansions. For a number of years, governments more or less adhered to that approach. For example, in the US, the massive debt incurred to win WWII was gradually paid down over the next three decades, at least as a percentage of GDP.

Again, being old enough to remember the extreme angst of the 1970s, when it seemed like nearly all the economic news was bleak, it’s hard not to wistfully yearn for a time when the US was so lightly indebted. This was especially true compared to the swelling size of the economy during the polyester and bell-bottoms decade. Basically, as bad as things were in the ‘70s, at least the economy grew faster than government IOUs did in those days.

Ironically, it was the supply-side policies of Ronald Reagan that began the great debt lift-off. And, equally ironically, inflation and interest rates went down, pretty much the exact opposite of what was expected to happen as deficits under “The Gipper” blew out to unprecedented levels, at least in peacetime.

Basically, for many years Keynesian theory looked like a winner until it met its inflation Waterloo. That’s actually a relevant lead-in to the first dramatic example of MMT (which perhaps should stand for Modern Monetary Terror) in action. One of the main causes of Napoleon’s rise to power in the late 1700s was the French Revolution and its revolting Reign of Terror excesses.

But many historians believe the downfall of the French aristocracy was a function of the hyper-inflation that broke out decades earlier. This was, in turn, caused by the economic theories of an on-the-run Brit by the name of John Law (who apparently ran afoul of his last name back home).

A future Gavekal EVA, again authored by Charles Gave (who is a French citizen), will go over this fascinating episode in more detail. But suffice to say that John Law’s plan, which he sold to the heavily indebted French monarchy, involved the idea that France could effectively borrow enormous sums by issuing shares in a company backed by its vast holdings in North America (what would eventually become the Louisiana Purchase).

Cutting to the chase—or crash—after a brief initial boom, Law’s scheme collapsed. Tellingly, it was runaway inflation that brought it down. The social malaise and cynicism toward the government that followed was believed to contribute to the eventual overthrow of the French monarchy. One could say that France’s aristocracy really lost their heads over this early version of MMT.

Undoubtedly, the many eloquent defenders of this “new and improved” economic theory (after all, it has “modern” in its name) will quickly point out the differences between what became known as the Mississippi Bubble and what they are proposing. Stephanie Kelton, the former economic adviser to Bernie Sanders, is among the most articulate. You can view one of her presentations on it here.

But there are haunting similarities, particularly the belief that creating enormous sums of new money, or money equivalents, can produce real wealth and lasting prosperity. As my good friend Will Denyer, one of Gavekal’s keenest analysts, recently wrote in a treatise on MMT: “At its core, (it) is a recognition that government spending is not constrained by how much the government can tax or borrow—not if the government has independent control of its own printing press and no obligation to maintain a fixed exchange rate (such as against gold or another fiat currency).” Because the US qualifies under those terms, it is the perfect candidate to adopt MMT—at least based on this logic.

You may be wondering why now? With the economy supposedly doing fine—notwithstanding the number of economic straws swirling in the wind these days—why would something this extreme be gaining such sudden notoriety? In my view, there are multiple answers, a few of which I will offer up, but among the most likely is the main theme of “No Way Out”. Essentially, elected officials around the world are waking up to the abject failure of monetary mayhem like negative interest rates and relentless quantitative easings to produce consistent growth versus a constant stream of stop-starts. (For Charles Gave’s incisive take in this regard, please click here.)

On this score, there is a growing awareness of how harmful it is to the banking systems in those countries that have exterminated interest rates. And when banks are under siege, they tend to be reluctant financiers of enterprises, especially of the smaller variety. They tend to prefer lending to big business where the risks are lower or simply to hold government bonds which have essentially zero reserve requirements. As these pages have long predicted, it’s very dangerous to force interest rates down to levels that impair the planet’s lending apparatus and serve mostly to inflate asset prices. That view is becoming more accepted on almost a daily basis. Thus, there is a growing chorus, particularly on the progressive end of the political spectrum, that fiscal stimulus needs to step up to the plate.

One of the main arguments of those proposing MMT is that most of the planet’s developed economies have been hamstrung by fiscal austerity. In other words, governments have been too worried about their debt levels and have not been bold enough in spending to revive growth.

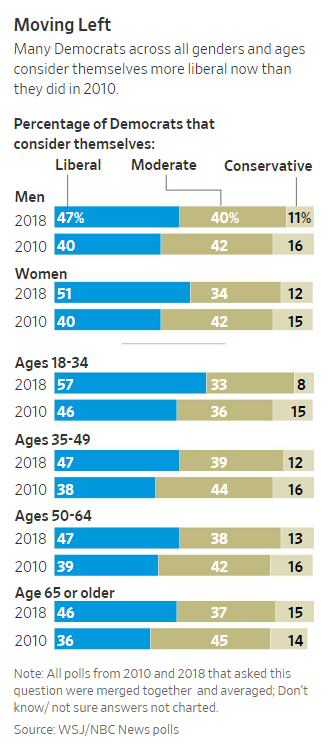

This has been argued for years by those who feel if governments would only really cut loose with deficit spending the world’s growth problems could be solved. But the rise of MMT has taken this debate to an entirely new level and it’s coinciding with another mega-trend Evergreen has been chronicling for several years: America’s “Leftward Lurch”.

We’ve previously noted that millennial Americans have, on balance, more affinity for socialism than capitalism. Moreover, the following words by Bernie Sanders, who is now tied with Joe Biden in online betting to win the Democratic presidential nomination, are not just a campaign boast: “The ideas that we talked about when we came to New Hampshire four years ago, ideas that seemed so radical at the time—well, today virtually all of those ideas are supported by a majority of the American people.”

In this regard, it’s been startling to see that almost half of all Republicans support the onerous tax proposals by those once considered to be on the fringe left, such as Elizabeth Warren. You may have noticed that she’s no longer the most firebrand woman in Congress. That designation has now passed to Alexandria Ocasio Cortez, also popularly known by an abbreviation, AOC. If you didn’t know this, AOC is a proud and self-avowed socialist (as is Mr. Sanders). One of her top advisors went so far as to say that every billionaire is a policy mistake (apparently, these boo-boos include prominent Democrats such as Bill Gates and Jeff Bezos). AOC is also a proponent of the New Green Deal that is estimated by some to cost as much as $90 trillion.

Unfortunately, even a tab half that high would be most inconvenient given that the US budget is already around $1.5 trillion (based on what the Treasury is borrowing not the so-called official deficit figure). The math problem becomes far worse when you look out at the next 10 years and consider the tsunami of entitlement spending the aging Baby Boomer generation represents. To raise taxes high enough to pay for that would almost certainly crash the economy. Thus, when AOC and others try to pay for the New Green Deal it creates a situation that is utterly impossible. And that’s another key reason MMT looks so irresistible to those who feel like a blitz of government spending is the answer to “no way out”. In their minds, it is not just the way, it is the only way.

Luke Gromen writes a niche newsletter called The Forest for the Trees that is popular with a number of professional investors and fellow financial authors, including my partner Louis Gave. Louis routed me some comments Luke made on MMT earlier this month that I feel are spot-on. To wit: “If we didn’t want to do MMT, we either need 75 million baby boomers to vanish by the end of next week or we need to get in an ’83 DeLorean with a flux capacitor and go back to 1937 and stop FDR from passing social security and then make a stop in 1968 and get LBJ not to pass Medicare and Medicaid…the bottom line is there are 75 million people who overspent and under-saved for 80 years because they were told the government would take care of them in the end. And the bill is due…The bottom line is if we didn’t want to get to MMT or something like it, that was a decision that should have been made 80 years ago, 50 years ago, 20 years ago with Medicare Part D. But it’s human nature. Politicians like to spend and people like free stuff that’s not going to show up until ‘someday’. It sort of stinks for the people who are there when ‘someday’ arrives.” (Emphasis mine)

Based on the policy decisions we’ve made in the US (and, for that matter, most of the rich world), it’s hard to argue with the part about politicians liking to spend and people (voters) liking to get free stuff. As Luke wryly writes, it’s no worries…until “someday” arrives.

In my view, MMT is the ultimate “someday” deferral technique. It not only kicks the can down the road, it launches it at escape velocity nearly into the exosphere…but not quite out of gravity’s reach. Eventually, that can will start falling back to Earth as fast as it went up. But, just like in 1700s France, MMT will likely work for a while.

It’s certainly possible that MMT won’t be implemented. There have been vehement objections raised since this theory has entered the political discourse, with most of those challenges, predictably, emanating from the political right. But, surprisingly, there have been numerous critiques from the left, perhaps because some of its older folks have now been far eclipsed by a Democratic party that is fast heading toward a warm embrace of socialism.

One not so surprising left-of-center voice that has come out forcefully against MMT is former Treasury Secretary under the Clinton administration, Larry Summers. He wrote in a recent Op-Ed: “Modern monetary theory…is the supply-side economics of our time. A valid idea…has been stretched by fringe economists into ludicrous claims that massive spending on job guarantees can be financed by central banks without any burden on the economy…(MMT) is fallacious on multiple levels.”

The real shocker, though, are the dire warnings from someone who, in my experience, has never previously seen a “progressive” program he doesn’t like, The NY Times columnist and Nobel Prize-winner in Economics, Paul Krugman. Mr. Krugman aptly notes the ultra-inflationary implications of MMT: “When people expect inflation, they become reluctant to hold cash, which drives up prices and means that the government has to print more money…which means higher inflation, etc. Do the math and it becomes clear that any attempt to extract too much seigniorage (i.e., printing money)—more than a few percent of GDP, probably—leads to an infinite upward spiral in inflation. In effect, the currency is destroyed.” (Emphasis mine)

This may be the first time in our lives that Mr. Krugman and I see eye-to-eye on economic policy (ok, maybe the second: He has also called the current social security system a Ponzi scheme, a scathing assessment I share). But let’s store his inflation point for now and allow me to return to it next week.

Apolitical types like Jeff Gundlach, the reigning King of Bonds, have summed up their MMT views in much briefer terms by simply stating: “It can’t work. You can’t drink yourself sober.” That’s one of those pithy sound-bites he’s famous for but I’m afraid there are many, especially of the elected official variety, who don’t believe—or won’t accept—its veracity.

It’s safe to say that MMT has already become one acrimonious acronym – and the controversy surrounding it is almost certain to become more intense. Next week’s second installment of “Bubble 3.0’s” chapter 11 will include more views from some of the world’s most influential financial thought-leaders on MMT, as well as what could cause it to go down in infamy. You won’t want to miss it.

*A silly bit of minutia is that Paul McCartney wrote this for his own father when Paul was 16 and his dad was—yikes—64. And I thought my dad was old when he had me at 40!

David Hay

Chief Investment Officer

To contact Dave, email:

dhay@evergreengavekal.com

OUR CURRENT LIKES AND DISLIKES

Changes highlighted in bold.

LIKE

NEUTRAL

DISLIKE

* Credit spreads are the difference between non-government bond interest rates and treasury yields.

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.