Over the past few years, we’ve written about the growing discord between the United States and the People’s Republic of China as dueling narratives. These newsletters have, for the most part, positioned the two global juggernauts as empires teetering on the brink of a “new cold war” over trade, technology, defense, and ideological differences. This week, we are presenting a view that recognizes the drastic disparities – and inherent conflicts – between the two countries but offers up a compelling proposition for investors. Chiefly, that investors can benefit from diverging sets of policies by allocating capital across separate asset classes in both countries.

Without stealing too much of Evergreen ally Vincent Deluard’s thunder, this week’s guest author makes the case that allocating capital between US equity markets and Chinese government bonds should be “the new 60/40.” For anyone who needs a primer on what that term “60/40” means, it is an investing guideline that recommends investors keep 60% of their assets in equities and the other 40% in bonds. For a long time, the basic principle was essentially the “gold standard” for portfolio construction. However, in recent years, analysts from major firms like Bank of America, Morgan Stanley and JPMorgan have proclaimed the “old” 60/40 rule DOA. (Regular EVA readers may note Vincent’s favorable comparisons of Chinese government bonds today to the remarkable past performance of German “bunds”—as their federal debt is popularly known--is very much in synch with various prior essays by Charles Gave.)

Despite Vincent’s compelling case for “the new 60/40”, and our own belief that Chinese government bonds are a good long-term investment, we believe the weighting belongs in the camp of “hyperbole” rather than recommendation. Instead, we believe a more modest, but still noteworthy, target allocation range of between 4%-8% to Chinese government debt on the bond side is advisable for most balanced portfolios. There are a number of other countries, mostly in Asia, that also offer attractive fundamentals for fixed-income investors seeking refuge from the Modern Monetary Theory (MMT) being practiced in most Western countries. Per earlier EVAs, we believe it’s critical for those holding US dollar-based bonds to begin diversifying off-shore—before the greenback backs down 15%...or even more.

If you or a loved one need help constructing a portfolio with international bond and equity exposure, please reach out to us at info@evergreengavekal.com.

“Arx tarpeia capitoli proxima”: the Tarpeian Rock – where the Roman Republic executed traitors – is close to the Capitol. Russia’s most powerful oligarch, Mikhail Khodorkovsky, may have meditated on this Latin adage when the disgraced oil tycoon was thrown behind bars by FSB agents in 2003.

He surely wished he had been an American billionaire, whom politicians cajole and almost never jail. So would Jack Ma, who “disappeared” for three months after criticizing China’s financial regulators. This report will draw a broader lesson for asset allocators in the 21st century: buy the bonds of (stable) dictatorships and buy the equities of (powerful) democracies. In other words, China is for bonds and the U.S. is for stocks. Call it the new 60/40.

The first part will show that China’s coming demographic collapse will be a massive headwind for stocks and a huge boost for its government bonds, which already pay the highest real yield in the world. In addition, the recent crackdown against Chinese tech platforms could do to Chinese stocks what the Khodorkovsky trial did to Russian equities: a permanent de-rating of multiples.

The second part will go against my bearish view of overvalued U.S. stocks. I have repeatedly argued that secular inflation should devastate stocks’ multiples. But what if the Fed never hikes rates? Could rising nominal cash flows translate into higher stock prices, especially if they are discounted at deeply negative real rates? Also, my case that big tech stocks cannot grow into their valuations could be based on a false premise: big tech stocks’ valuations may never normalize if they retain their monopolistic margins.

The conclusion will argue that people (or countries for that matter) usually get what they really want and lose the things they care less about.

In the U.S., rising stock prices have become an economic goal which probably supersedes the Fed’s dual mandate. The S&P 500 index is a political object, celebrated by POTUS 45. On the other hand, inflation, financial repression, and a weak dollar are necessary to restore the U.S. manufacturing base, solve its debt crisis, and reduce wealth inequalities.

In China, politicians can force billionaires to play for the national team and do not care about stock prices. The prize for China is to turn the Yuan into a reserve currency, which can only happen if Chinese Government bonds remain a great store of value over the next decade.

A Bullish Economic Slowdown For Chinese Bonds

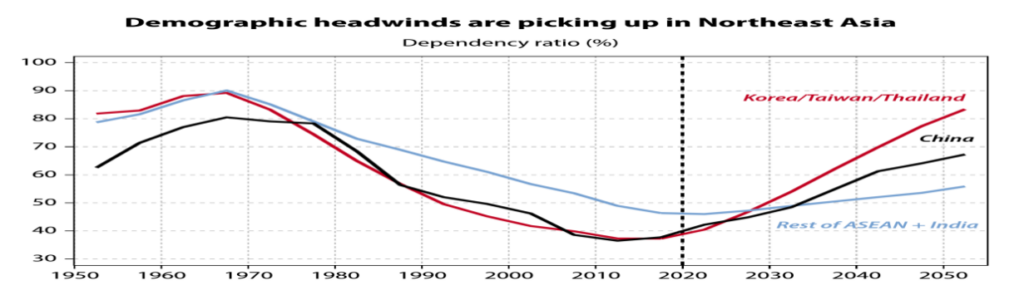

If I had to pick one macro chart for the coming decades, it would be the insanely rapid increase in East Asian dependency ratios, as reported by my esteemed friends of Gavekal. The huge Asian youth bulges, which were born in the ‘70s and entered the workforce in the ‘90s, forgot to make babies. Chinese households had the excuse of the one-child policy, but Koreans households performed even more poorly in the bedroom. The average Korean woman is expected to have less than one child in her life. In a country with little tolerance or experience of immigration, this means that the population should halve every 25 years. With the exception of the destruction of the pre-Columbian civilizations, mankind has never experienced the kind of demographic collapse which East Asia will face in the next 20 years.

The slowdown in growth will be massive. Growth is the result of labor, capital, and an unexplained residual called productivity. Robotization, heavy R&D investment, and large savings pool will not be able to offset the collapse of Asia’s labor force.

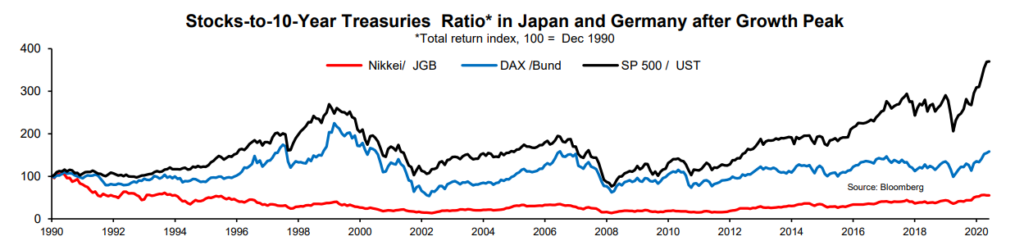

This slower growth rate will have important consequences for asset allocators. Japan and Germany are interesting precedents which experienced large growth shocks in the 1990s (albeit smaller than what China will experience in the next decades). Japan’s high-growth era ended with the bursting of its real estate bubble in 1989 and Germany’s post-reunification boom petered out in the ‘90s. Japanese government bonds overperformed the Nikkei-225 index by 100% in the following three decades. German equities eventually recouped their loss relative to 10-year bunds, but at the cost of enormous volatility. For German insurers, pension funds, and banks, which do not need to put capital against their holdings of sovereign bonds, holding long-term bunds, which returned 600% since 1990, was a no-brainer.

Equities are quintessentially a growth asset. This is especially true in China, where investors must ignore serious issues of corporate governance, government interference, and IP theft to access its large and rapidly growing market.

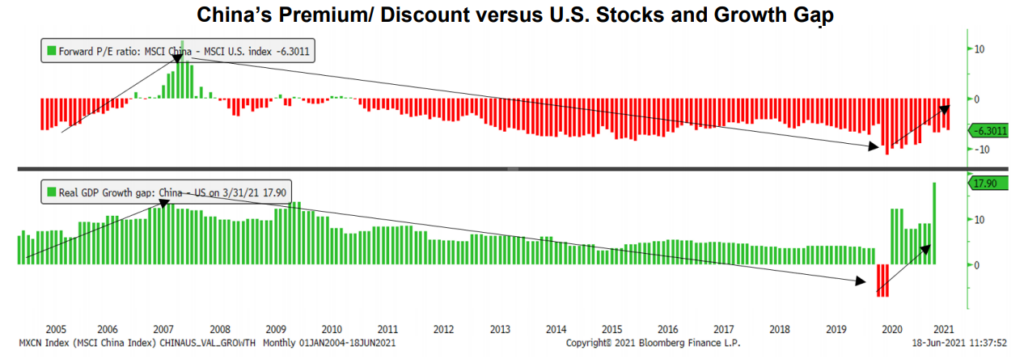

As shown in the chart below, the relative valuation of Chinese stocks followed the growth gap between China and the U.S. From 2004 to 2008, the Chinese discount closed and turned into a premium as China’s GDP growth outpaced the U.S. by more than 10 percentage points annually. This gap shrank in the ensuing 13 years when China’s forward P/E ratio hovered around 15, against 25 in the U.S. The pandemic partially closed the gap as the U.S. brutal 2020 recession temporarily restored the Chinese growth premium.

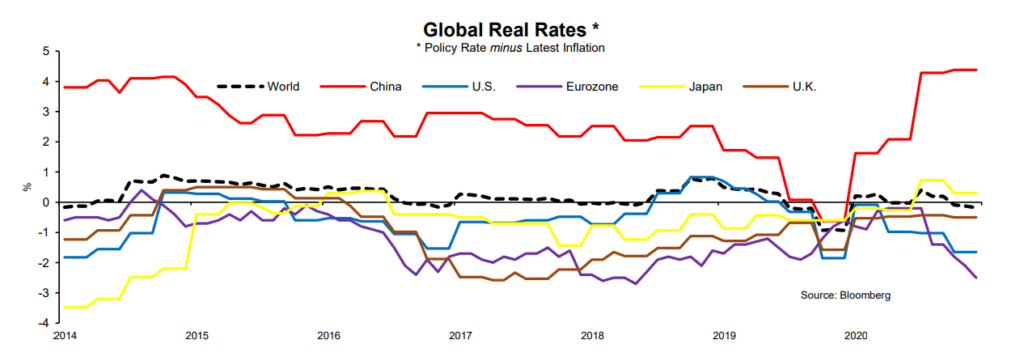

As investors experienced in the past 20 years, what is good for stocks is bad for Treasuries, and vice versa. The coming collapse of China’s nominal growth will boost the returns of its government bonds, which are already offering exceptionally positive real rates.

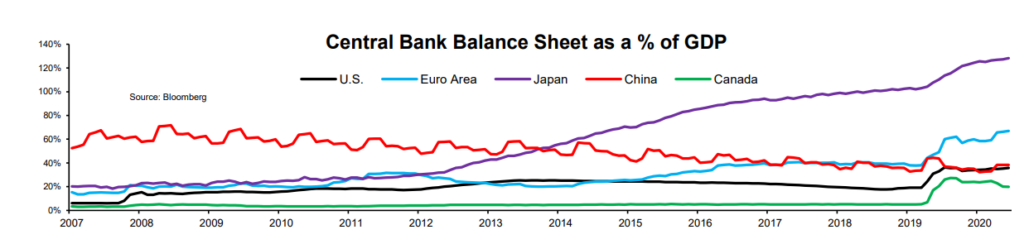

As I observed in “Just Buy the Yuan”, the PBOC has been exceptionally hawkish in its response to Covid. While the balance sheets of most Western central banks doubled or tripled in the past year, the PBOC’s balance sheet has fallen to 38% of GDP, from 71.2% in 2009. In the U.S., the fiscal and monetary authorities decided to risk inflation and the erosion of the Dollar to protect stock prices, while China prioritized price stability and its long-term objective to elevate of the Yuan as a reserve currency. The West is euthanizing its rentiers, while China cajoles them.

Shareholders do not get the same love from Chinese policymakers, especially if their wealth casts a shadow over the glory of Xi Jinping or if they criticize the system which allowed their rise. In such instances, a good old shakedown reminds forgetful tycoons of who the top dog is.

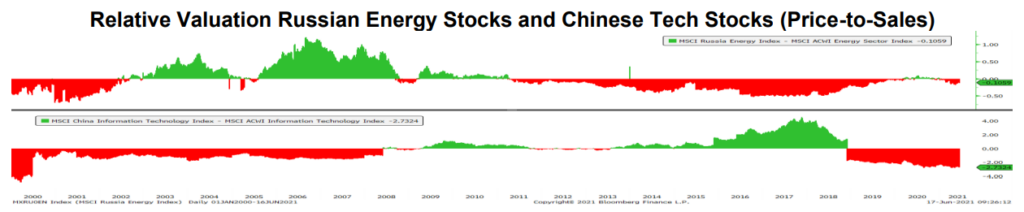

The abrupt cancellation of Ant Financial $37 billion IPO last year and the ensuing “disappearance” of Jack Ma was China’s Yukos’ moment.

After the botched privatization program and the chaos of the ‘90s, a class of fantastically rich oligarchs emerged from the ruins of the Soviet economy. Oligarchs initially engineered the rise of a little-known KGB agent named Vladimir Putin to protect their interests and the Kremlin initially viewed them as a modernizing force for the economy, which was necessary to the restoration of Russian power.

This symbiotic relation between Putin and Yukos’ chairman, Mikhail Khodorkovsky, ended in 2003 when Russia’s richest man started to make electoral moves and criticized Russia’s “managed democracy”. The oligarch was jailed, his company was broken up, and Russian energy stocks, which traded at a premium to their global peers during the reform era, were punished by a permanent discount. Chinese tech stocks have suffered from a similar de-rating after the crackdown on Jack Ma’s empire.

The whims of autocrats are not the only Damocles sword hanging over hanging over Chinese shareholders.

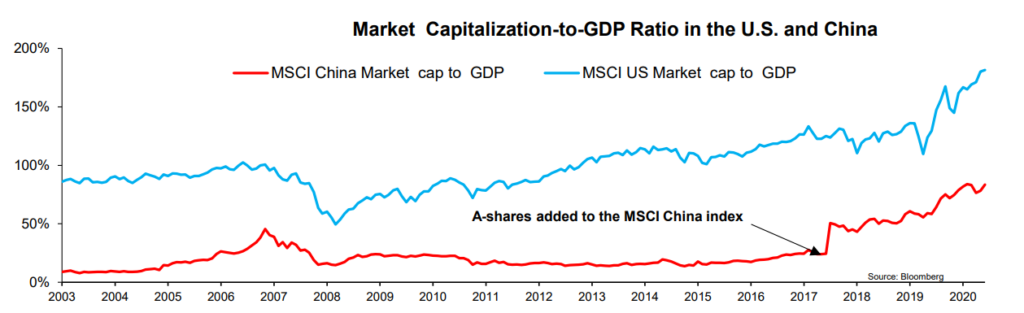

The chart below is usually shown as bullish for Chinese shares: China’s equity market capitalization accounts for just 83% of GDP, versus 181% in the U.S. Rather than the naïve extrapolation (“look, China’s stocks need to double to catch up with the U.S.!”), I view the relatively small size of China’s equity market as a vulnerability. The stock market is not that important, especially for politicians who derive most of their wealth from real estate and their power from guanxi (personal connections).

On the other hand, the stock market is systemically important to the U.S.: Trump tweeted about daily highs in the Dow Jones as if they were a greater achievement than the 1969 moon landing. It only took two months in the fall of 2018 for the stock market to remind J. Powell that the Fed’s dual mandate is conditional upon the impassable horizon of permanently rising stock prices.

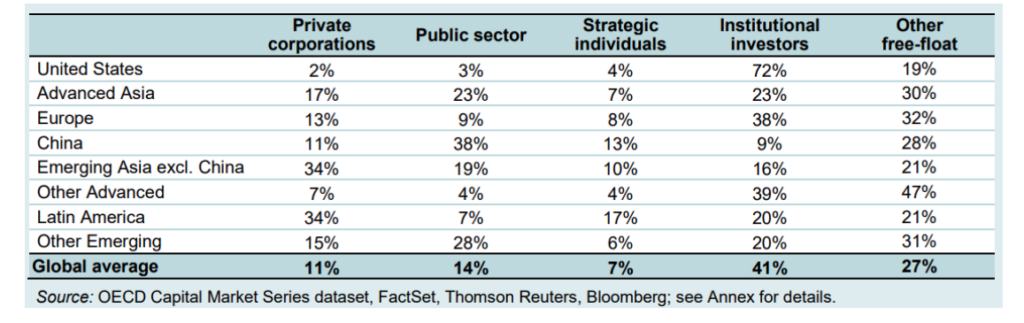

The OECD’s data on stock ownership explains this difference in philosophies. Institutional investors own 72% of the U.S. stock market. A bear market becomes a political problem when it devastates banks, insurers, and pension funds, and prevents voters from achieving their retirement goals. Conversely, China’s stock market is dominated by gambling-prone retail investors. Asking the government for bailouts is seen as absurd as asking the house for a refund after a bad night in Macao.

Could the Inflation Shock Be Bullish for US Stocks?

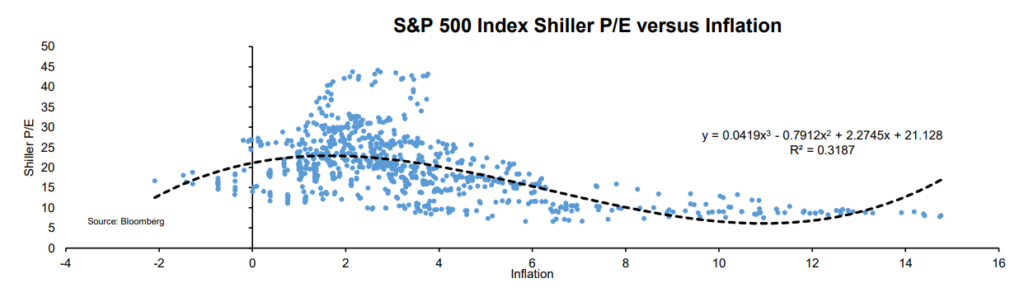

My case for inflation has now become consensus. There is also little debate that inflation is devastating for bonds and currencies. Stocks are a harder call because moderate inflation is good for stocks. As shown in the chart below, the Shiller P/E of the S&P 500 index has tended to peak when inflation was around 3-4%.

In “the inflation-proof portfolio”, I argued that multiples should start compressing as inflation rises above 5%, as predicted by the quadratic regression line below.

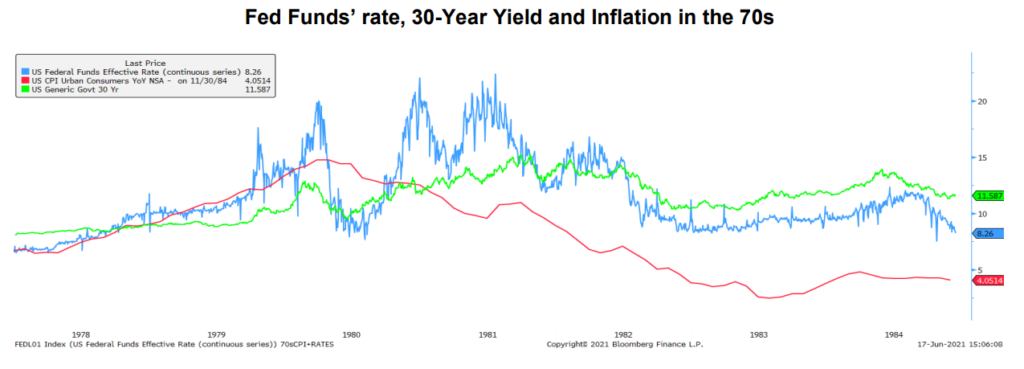

However, this relation is mostly driven by the late ‘70s, when the market expected the Fed to hike rates in response to rising prices (which it did - short-term real rates were positive throughout the ‘70s).

Would multiples have compressed if the Fed had let go of inflation? My guess is “yes” as I believe that investors would have eventually created a “shadow, inflation-adjusted cost of capital” but I also agree that the Federal Reserve was the immediate cause for the bear markets of the ‘70s.

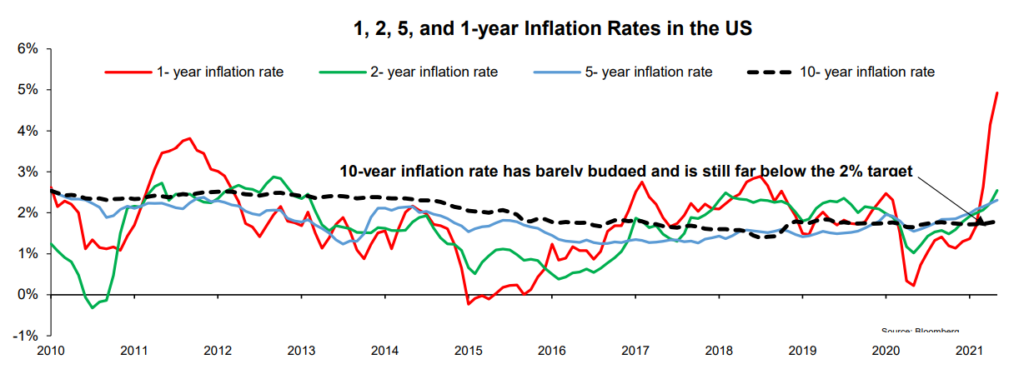

As a follow-up question to this historical debate, investors should realize that the Fed is more likely to ignore inflationary pressures than in the ‘70s. Despite the supposedly hawkish tone of last week’s meeting, the Fed’s tolerance for inflation will surprise markets. As shown in the chart below, the 10-year inflation rate is a still well below target at 1.79%. I expect these charts to become increasingly popular as the Fed’s economists repeat the mantra that “long-term prices remain anchored despite strong base effects in year-over-year inflation data”.

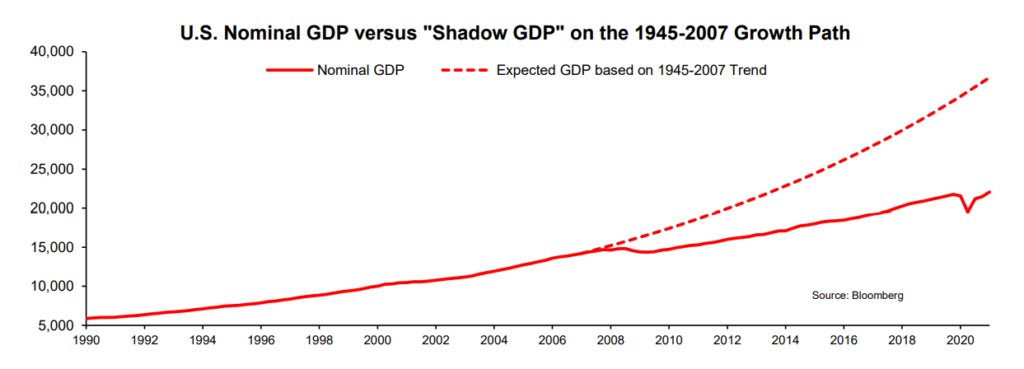

“Nominal GDP targeting”, which the Fed has embraced for all practical purposes, could justify even more tolerance for above-target inflation. If we accept the premise that something was broken in 2007 and that the U.S. economy needs to return to its pre-GFC growth trajectory, the Federal Reserves must manifest 40% of GDP or $14 trillion. Since the Fed prints banknotes rather than goods and services, the normalization of nominal GDP would require about a decade of 6% inflation. Nominal profits would soar under such a scenario, and so would stock prices if these cash flows are discounted at a Fed Funds rate of 0%.

Surely, the dollar would plummet under such a scenario, but that would actually be a blessing for S&P 500 companies which derive 50% of their profits from abroad. What about margins? Would soaring commodity prices and labor costs eventually destroy corporate profits?

Not immediately: as I argued in “Three Unconventional Arguments for Secular Inflation”, unchecked merger waves have led to unprecedented levels of concentration in most industries. Big tech oligopolies, too-big-to-fail banks, cable monopolies, and acquisitive consumer staple companies enjoy a lot of pricing power. When Google controls 92% of the global search market, price is an executive decision set in Mountain View, rather than the outcome of market forces.

What about consumers? Would they not get squeezed as American monopolies and oligopolies pass down price increases? Eventually yes, but not right away. For foreigners, the weak dollar would offset the effect of higher prices. Domestic buyers are flush with cash and eager to consume so they would stoically accept higher prices as the cost of returning to normal life – or at least that is what I tell myself when I see the prices of Hawaiian hotels for my upcoming vacation.

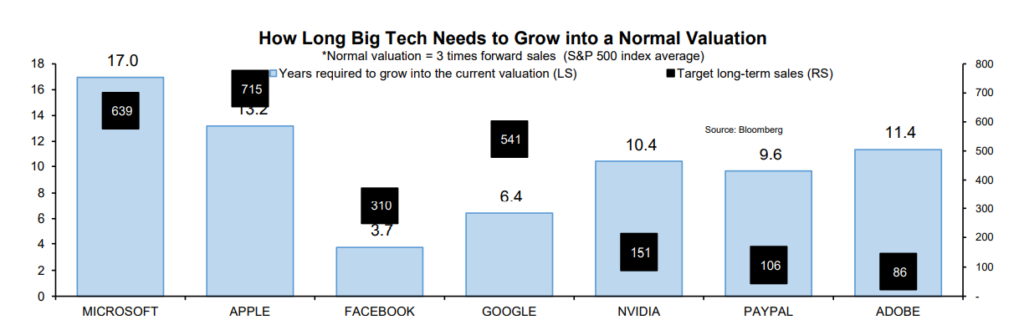

The resilience of margins due to monopolies’ pricing power is a big flaw of my “mathematical case” against big tech. The chart below, from “the Nuclear Winter of the 60/40 Portfolio” shows that big tech stocks, as a whole, cannot grow into their valuations. Smart clients have made two wise objections:

In this chart, I implicitly assumed that big tech’s abnormal margins would be eroded by competition, regulation, and antitrust enforcement. This may be wishful thinking: what if big tech companies are already more powerful than the government which is supposed to regulate them? To which we shall turn...

Conclusion: What Do We Really Want and What Can We Let Go of?

The experience of loss has led me towards a journey of introspection. My conviction is that real change starts with only two questions: what do you really want? And conversely, what can you afford to let go to achieve this objective?

If one answers these questions with honesty and realism and commits to path of steady improvements, chances are that, over time, he will get what he set to achieve and he will let go of the things he can afford to lose.

Applying this self-help philosophy at the national level, I would say the U.S. really wants higher stock prices and can let go of its currency and bond market. If anything, a decade of financial repression, inflation, and a weaker U.S. Dollar may be secretly desired by smart populists who understand that these are the necessary conditions to rebuild the manufacturing heartland of the country, reduce wealth inequalities, and default on the unsustainable entitlements that the boomer generation granted itself.

Conversely, rising stock prices have become a political priority. D. Trump celebrated every new market high as a confirmation of his personal glory. Establishment Democrats such as J. Yellen or N. Pelosi may be less blunt, but they also have significant stock portfolios - which Nancy Pelosi actively trades (see her latest and likely well-informed transactions here). They also have donors to please and lobbies to cajole. For those who do not share my cynical view of the origin of N. Pelosi’s $120 million fortune, there are legitimate reasons for Democrats to engineer perpetually rising stock prices: their electoral base – college-educated suburbanites – relies on 401-K plans for retirement.

On the other hand, Chinese leaders really want a world reserve currency. In order to convince foreigners to accept pieces of paper decorated with Mao Zedong’s picture in exchange for their commodities, China needs a strong and rising currency. China needs the world to trust that Chinese Government Bonds will be the best store of value in the next decades.

On the other hand, CCP members view tycoons with a mix of envy and scorn. Too much private wealth is seen as a threat to the primacy of the party. To caricature, I would say that in the U.S., politicians work for the billionaires, while in China, politicians force the billionaires to work for the party.

I will let the reader decide which system is better, as I am personally torn. On the one hand, a society where B. Gates, J. Bezos, and E. Musk call the shots should be innovative and very respectful of property rights – which usually generates long-term wealth. On the other hand, the Chinese system is much better at rapidly mobilizing resources towards a common goal, such as reversing two centuries of humiliation by Western Powers, rapidly stopping the spread of a pandemic, and projecting power across the Eurasian world island. Fortunately, investors do not need to choose: they can have the best of both world by owning U.S stocks and Chinese government bonds.

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.