“You pay a very high price in the stock market for a cheery consensus.”

- Warren Buffett

SUMMARY

- Evergreen’s 2016 forecast letter focuses on the potential surprises that could happen over the course of the next year but are far off the radar of most investors. Such events can impact our clients’ portfolios in a dramatic fashion, so it makes sense to think ahead.

- US Stock Market: Most commentators currently expect the S&P 500 to remain within a +10% to -10% range for 2016, so we consider the probability of a bigger move in either direction. While we believe an upside surprise is unlikely, we feel the stock market could fall by 25% to a support level of 1600. If that support level is breached, a 50% crash is possible. SUMM

- Credit Spreads: While credit spreads (which indicate the cost of capital for US corporations above the “risk free” rate paid by the US government) have widened considerably over the past 18 months, this trend could continue in the event of an economic downturn in 2016.

- US Economy: We believe there is more of a recession risk than the consensus currently thinks. The US manufacturing sector may already be contracting. While unemployment remains low and wages are showing some signs of escalating, these indicators often appear the most robust right before the economy rolls over.

- Master Limited Partnerships (MLPs): While optimists believe MLPs are poised for a “V-shaped” 2009-style rebound, we are skeptical (though we’d love to be wrong!). However, even flat performance (supported by their high yields & low valuations) could make this sector one of the best performers in what we think could be a difficult year for risk assets, like stocks. It will likely take a sustained rally in energy prices to produce the next MLP bull market.

- Oil: Oil prices (currently trading in the low $30s) can certainly fall further in 2016, but the big surprise could be a faster-than-expected recovery over the next few years. In fact, we believe widespread capital expenditure (CAPEX) cuts may be setting the stage for an oil shortage in the not-so-distant future.

- Federal Reserve: After last month’s Fed rate hike, most market participants expect one or two additional rate hikes in 2016. In contrast, the Fed is signaling as many as four hikes over the next twelve months. Instead, we believe the Fed may be forced to make an about face from rising interest rates to negative interest rates.

- Emerging Market Stocks, Bonds, & Currencies: While further sell-offs seem probable, we believe emerging market assets could bottom and rally explosively later in 2016.

- China: The People’s Republic of China is shaking the world as its economy slows under the weight of a massive debt burden and is struggling to transition toward a more consumption and services-based system. This is a long-term story with profound (good and bad) implications for the global economy and it’s been the source (or at least the scapegoat) of the last two global market panic attacks. While investors worry that China could drag the US into recession and usher in a bear market for US equities, the deterioration in US credit conditions suggests the next crisis could be homegrown in the USA rather than imported from the Middle Kingdom.

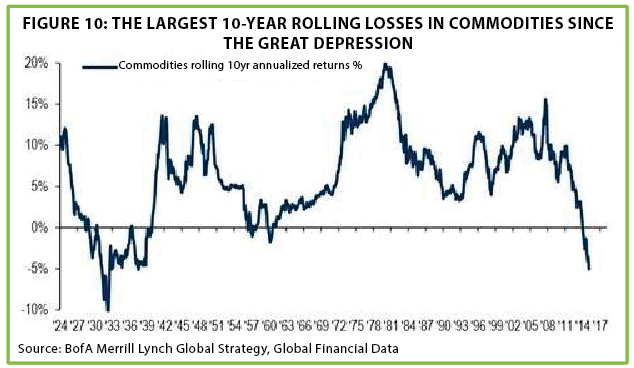

- Commodities: Should central banks decide to employ even more extreme monetary responses in a 2016 crisis, commodities could surprise to the upside.

The following commentary is from the Evergreen Investment Team:

Auld Lang Syne or Old Anxiety? It’s been the tradition of the Evergreen Virtual Adviser (EVA) to do a forecast issue at this time of year. Of course, that’s about as unique as wearing a red sweater over the Holidays. Consequently, to be a bit more differentiated and perhaps increase our readers’ interest level, we are emulating the venerable Byron Wien and shifting to a potential surprise format. Byron is one of the few strategists who attempts to visualize events that could happen but are far off the radar of most investors. And, as we all know, it’s those possibilities—should they become realities—that can have such a resounding impact on financial markets.

But before we get into what the Evergreen Investment Team believes might be the surprises of 2016, we want to invite those readers who would like to see the results of our 2015 predictions to click on this link.

The stock market: Ok, let’s get right to that ultimate hot button for most investors. Let’s also think about what would constitute a truly shocking turn of events for stocks. In our opinion, a 10% or 15% increase or decrease wouldn’t cut it; most commentators would say that any move within that band would be highly probable (though millions of lulled-to-sleep market participants would be seriously pained by a 15% drop).

That leaves us considering the odds of a bigger up or down move. Anatole Kaletsky, co-founder of our partner firm GaveKal, and one of the most esteemed financial thinkers in Europe, has believed for the last couple of years that stocks have broken out on the upside. As a result, he feels we are in the midst of a long-term bull market similar to the 1990s. Considering how flaccid stocks have been for the last 1 ½ years (the NYSE composite, an even broader measure of stocks than the S&P 500, is actually down 7% since the summer of 2014), they better surge soon to qualify for being in an on-going bull market. Something like a 25% or greater spike would clearly make the grade as a true upside surprise.

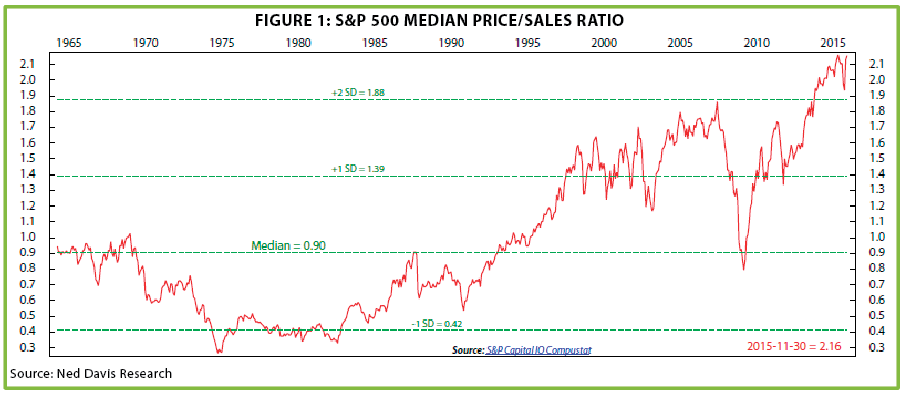

In order for the S&P to replicate its remarkable 30% gain in 2012, it would need to soar to around 2650. Since that type of leap happened in 2012—and numerous other times in the past—this is certainly possible. However, it would mean that the market would be trading at roughly 2.7 times sales per share, versus the long-term average of just under 1. The median stock in the S&P 500 (i.e., exactly at the mid-point between the largest and smallest member of that index) is already trading at its highest price-to-sales ratio ever. In fact, on this basis, the S&P 500 is 30% above the bubble peak in early 2000!

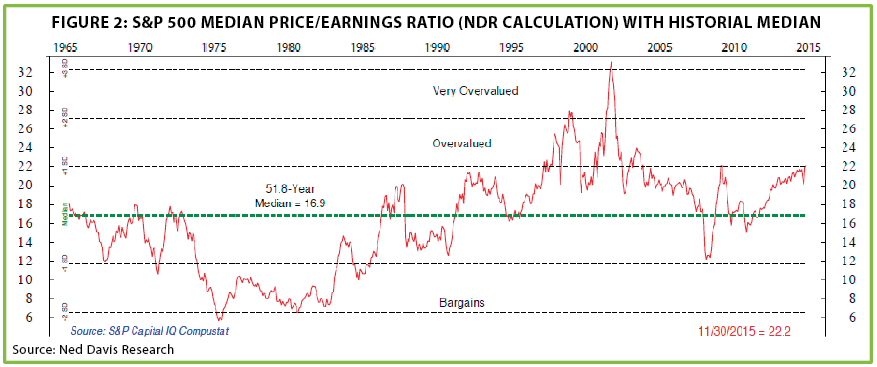

For those who prefer to use price-to-earnings—even though we believe revenues are a more reliable measure (especially when gargantuan share buy-backs and fuzzy accounting are inflating profits)—the news is better…but not much. Per Ned Davis Research, the median P/E ratio is 22. The highest ever was 32 in early 2000. To assume a 30% higher market would require either an extraordinary earnings thrust or the P/E ratio rising back close to what was the most insane valuation in stock market history. Unquestionably, this would qualify as a surprise but a rational investor needs to question the likelihood—not to mention the desirability—of that occurring.

For those who prefer to use price-to-earnings—even though we believe revenues are a more reliable measure (especially when gargantuan share buy-backs and fuzzy accounting are inflating profits)—the news is better…but not much. Per Ned Davis Research, the median P/E ratio is 22. The highest ever was 32 in early 2000. To assume a 30% higher market would require either an extraordinary earnings thrust or the P/E ratio rising back close to what was the most insane valuation in stock market history. Unquestionably, this would qualify as a surprise but a rational investor needs to question the likelihood—not to mention the desirability—of that occurring.

Now, let’s consider the odds of a 25% to 30% decline from the S&P 500’s peak of 2130. A quarter off of that level would bring it down to almost precisely 1600. Interestingly, that would be right at its hugely significant break-out point from back in 2013. The reason this threshold is so meaningful is that slightly below 1600 is where the market hit the wall (or ceiling) back in both 2000 and 2007. When it shattered this resistance in April of 2013, the S&P made an all-time record high. That breakthrough set the stage for the sprint to the 2130 zenith and we expect the 1600 level to represent serious support in the future.

Now, let’s consider the odds of a 25% to 30% decline from the S&P 500’s peak of 2130. A quarter off of that level would bring it down to almost precisely 1600. Interestingly, that would be right at its hugely significant break-out point from back in 2013. The reason this threshold is so meaningful is that slightly below 1600 is where the market hit the wall (or ceiling) back in both 2000 and 2007. When it shattered this resistance in April of 2013, the S&P made an all-time record high. That breakthrough set the stage for the sprint to the 2130 zenith and we expect the 1600 level to represent serious support in the future.

Beyond that crucial technical analysis consideration, 1600 on the S&P would also bring the median P/E back to its long-term average of around 17. This would also lower the median price-to-sales ratio to the mid-point of the last 20 years (however, it would still be quite pricey in comparison to the pre-1995 history.) As indicated above, we believe the price-to-sales measure is providing a more accurate picture of how expensive the US stock market is currently.

Should 1600 be meaningfully breached on the downside, that would be an exceedingly ominous development. This would raise the ugly scenario of a repeat of the 50% declines seen the last two times valuations got this high in 2000 and 2007.

Regardless, either a 25% or 50% decline would qualify as a true surprise—the kind few investors are prepared to endure. Yet, the former would just return valuations to so-so while the latter would still leave P/Es and price-to-sales ratios well above prior market troughs (excluding 2009 when stocks bottomed at far higher valuations than prior bear markets).

We will let our readers assess the odds of which surprise outcome is more likely to occur. But based on the next couple of sections, it will be quite obvious which we way lean (realizing this is anything but a surprise to longtime EVA readers.)

Credit spreads. Before you freeze up at this term, it is actually a simple concept, one we’ve frequently defined in prior EVAs. Credit spreads are the excess interest rate corporations have to pay to borrow money compared to what the US government pays. It is essentially a cost of capital—or cost of money—reading for Corporate America. And, as such, it is critically important.

When credit spreads are narrowing, it signifies a couple of significant things. First, it means companies can borrow more affordably, always a positive situation. Second, it means that investors are optimistic and willing to take on more risk (by holding corporate bonds with lower returns). When spreads are narrowing on high-yield (junk) bonds, this is especially reflective of a more relaxed attitude toward risk.

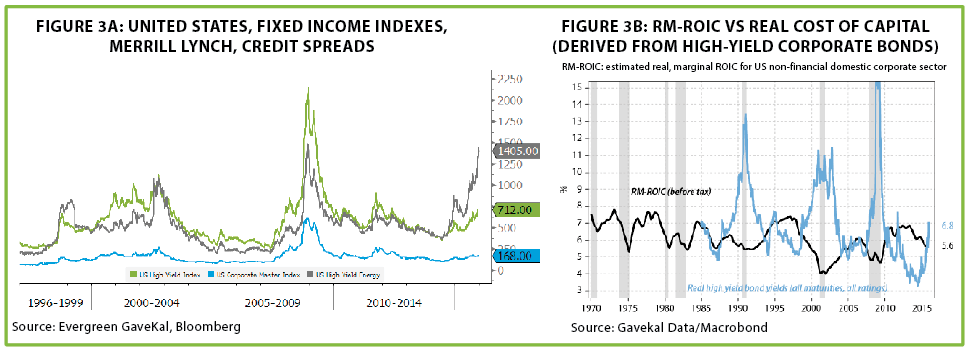

These days, the exact opposite is happening. Spreads have widened considerably, as you can see below.

In fact, as the right hand chart indicates, for those companies with below-investment-grade credit ratings, the cost of borrowing is now exceeding their return on investment. This is never a healthy situation. For investment grade companies, the difference is still positive but narrowing quickly.

In fact, as the right hand chart indicates, for those companies with below-investment-grade credit ratings, the cost of borrowing is now exceeding their return on investment. This is never a healthy situation. For investment grade companies, the difference is still positive but narrowing quickly.

Considering credit spreads are already in the danger zone—and recognizing how much of a drag this has been historically for stocks--the fact that every major Wall Street strategist in the recent Barron’s poll sees a higher market in 2016 means the consensus view must be that spreads will narrow. Thus, the wicked curveball for the majority outlook would be if spreads continue expanding.

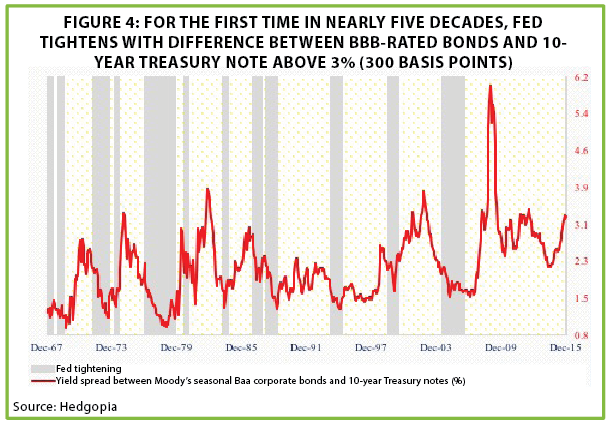

It is already extremely unusual that the Fed is now tightening at a time when spreads have widened as much as they have. In reality, this hasn’t happened in almost 50 years.

Spread widening doesn’t happen in a vacuum. It usually takes problems in the economy for this to happen. Consequently, a further blow-out in credit spreads will likely be caused by an economic downturn. And that’s an event that almost no one is expecting.

Spread widening doesn’t happen in a vacuum. It usually takes problems in the economy for this to happen. Consequently, a further blow-out in credit spreads will likely be caused by an economic downturn. And that’s an event that almost no one is expecting.

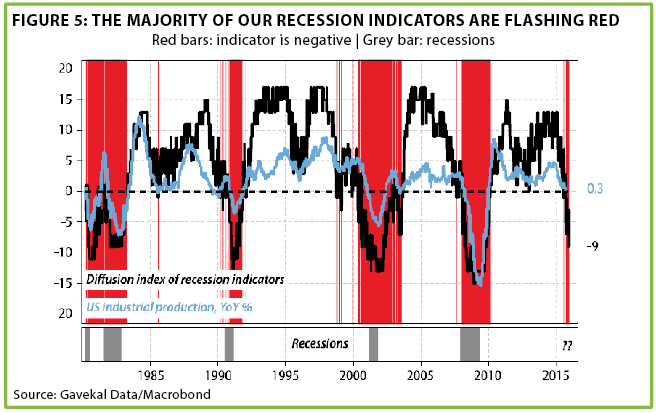

The economy. The key word in that last sentence is “almost”. There are a few renegade economists/strategists who are running up the red flags. Among that small group is Gavekal’s Charles Gave. His recession indicator has recently hit the -9 level, a point that has consistently warned of prior contractions.

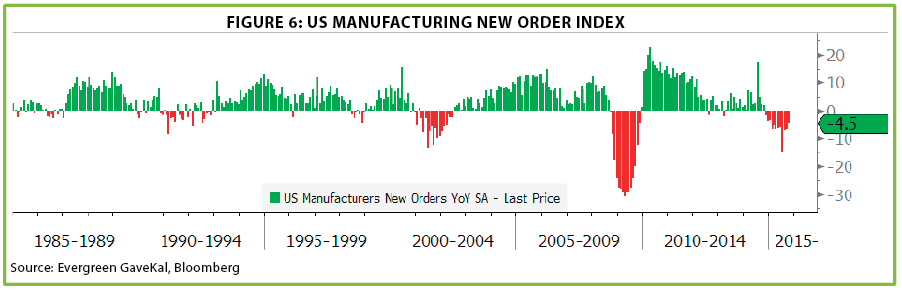

Frankly, there isn’t much doubt that the US manufacturing sector is already in a recession. Also, Corporate America has just experienced two quarters of declining profits, which qualifies as an earnings recession. It also appears that overall corporate profits will be reported to have fallen last year. But since the US economy is 70% services, the popular view is that America will not suffer an actual downturn in 2016.

Frankly, there isn’t much doubt that the US manufacturing sector is already in a recession. Also, Corporate America has just experienced two quarters of declining profits, which qualifies as an earnings recession. It also appears that overall corporate profits will be reported to have fallen last year. But since the US economy is 70% services, the popular view is that America will not suffer an actual downturn in 2016.

Evergreen has also been of the belief that the US was not on the cusp of negative growth—until recently. However, lost in the usual Holiday activities and euphoria was a decidedly un-euphoric Chicago Purchasing Manager Index (PMI). It was released on December 30th and it came in at a shockingly weak 42.9, the lowest reading since June, 2009, when the Great Recession was still raging (anything below 50 implies contraction). Moreover, the various sub-components were extremely disappointing, particularly New Orders and Order Backlogs (the latter dove to the lowest reading since 1951!). Nationally, New Orders for the US manufacturing sector are looking a lot like they did during the recession of 15 years ago.

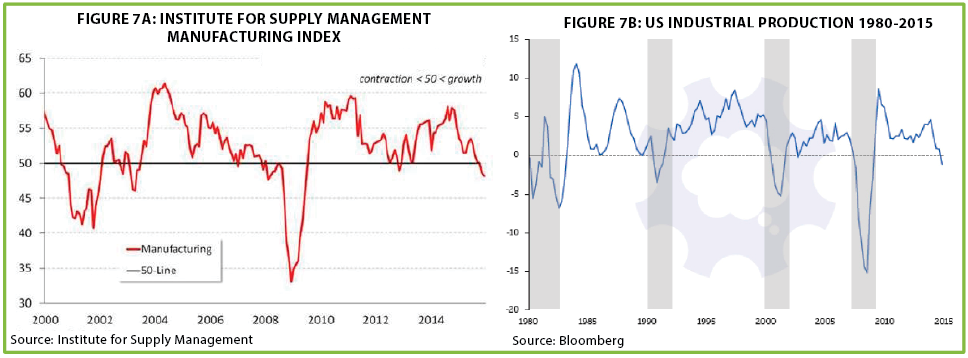

This continues a string of weak economic releases, particularly those related to industrial activity. Last Monday, kicking off economic releases for the year, the national Institute of Supply Management (ISM) Index dipped into negative territory. Meanwhile, US industrial production has also slumped to a level that has coincided with past recessions.

This continues a string of weak economic releases, particularly those related to industrial activity. Last Monday, kicking off economic releases for the year, the national Institute of Supply Management (ISM) Index dipped into negative territory. Meanwhile, US industrial production has also slumped to a level that has coincided with past recessions.

As mentioned above, the prevailing mind-set is not to worry about the production side of the US since our economy is mostly service-based. However, even the most recent Markit Service Sector PMI fell sharply. Encouragingly, though, at 53.5, it remains above the danger level of 50 (anything below indicates contracting activity).

As mentioned above, the prevailing mind-set is not to worry about the production side of the US since our economy is mostly service-based. However, even the most recent Markit Service Sector PMI fell sharply. Encouragingly, though, at 53.5, it remains above the danger level of 50 (anything below indicates contracting activity).

It’s also positive that unemployment remains low and wages are showing increasing signs of escalating. The problem is that these are classic lagging indicators. They often look robust right before the economy rolls over.

We are now at a point where we have to be mindful of positive feedback loops—though of a decidedly negative nature. Specifically, should the economy weaken further, this will mean more corporate defaults (and these have been on an upward path for the last year). This, in turn, pushes up credit spreads further yet. Should spreads rise beyond their already elevated levels, this puts additional downward pressure on the economy…which then pushes spreads higher yet. If we see an actual panic, such as in 2008—and, to a lesser degree, 2011—spreads might truly go postal.

As Worth Wray noted last week, with the Fed now tightening, however timidly, the usual remedies to halting this self-perpetuating chain reaction are limited. The Fed’s response, should a financial crisis erupt, could constitute another major surprise—but more on that in our interest rates section.

Suffice to say that with the majority so confident that a recession has about the same odds of happening as Donald Trump getting a buzz-cut, it won’t take many more recessionary economic reports, such as we’ve seen lately, to constitute a huge—and hugely uncomfortable—surprise.

Master Limited Partnerships (MLPs). In our section on energy, we make the case for why natural gas and crude oil prices might surprise on the upside at some point in 2016. This would likely be a catalyst for much better performance by MLPs in the coming year.

That wouldn’t be saying much, however, considering that they were down 36% in 2015. This utter collapse has divided the financial commentating world essentially into two camps: MLPs are poised to have a rebound rivaling 2009 when they exploded up almost 77% (after losing 55% in 2008) or their basic business model is broken and they will remain comatose indefinitely.

Accordingly, what could catch both camps off-guard is something in-between. Rather than the exhilarating “V” bottom we saw in 2009, MLPs might turn out to be in more of an elongated “U”, fluctuating in a fairly tight range with a few spirited rallies that excite their fans before fizzling out. Given our substantial MLP holdings, we’d love to be wrong about the “U” versus “V” scenario. Yet, we have to concede this is a much more challenging environment for many MLPs than even the double-whammy of the Great Recession and the Global Financial Crisis.

We didn’t think this was the case through much of last year. After all, what could be worse than 2008? Well, for MLPs, we just found out that a glut of supply is far tougher to cope with than a collapse in demand (which is what happened in 2008/2009).

Again, we wouldn’t have thought so but, as Einstein once mused, even though reality is merely an illusion, it’s a very persistent one. And the persistent reality of the MLP debacle is that there are no quick fixes. It’s highly likely we’ll see more distribution cuts and other once unthinkable measures taken to deal with the malaise.

This is not to say MLPs aren’t ridiculously over-sold and due for a snazzy rally. In fact, they popped 22% from mid-Dec through January 4th, before succumbing to another bout of selling due to oil prices cracking further. We believe that before we can get to the right-hand side of the “U” there needs to be a thorough sorting out of the winners and losers, some dramatic changes to the way many MLPs are structured, clarity on financing plans, and a definite sense that energy prices have troughed. And all of that doesn’t happen overnight.

Yet, for those who are grave dancing on this asset class, we also believe a rude surprise is in store. Owning and building out our nation’s energy infrastructure remains a growth industry. Giving MLPs the last rites now, is likely to turn out to be a classic case of believing exaggerated rumors of their demise.

One of the most surprising developments of 2016 might be that even though MLPs essentially go sideways they become one of the best performers of the year. They may even generate decent positive total returns due to their high yields (most of which we believe will be sustained). Lending that thesis some credence, what is arguably the premier MLP announced on Monday that it will raise its distribution by 5% this year. This led it to rise on the first trading day of the New Year even as the overall market had its worst start to the year since 2001. Whether this is an aberration or an indication of more to come, remains to be seen. But we like the odds for energy in general—and MLPs in specific.

The following commentary is from our CEO, Tyler Hay:

Oil: The case of the mistaken identity. Everyone has oil figured out. It will go nowhere for years, right? Wrong. Let’s go back in time to January 1, 2008 the Graduate Business School at Stanford published an article on the outlook for oil. The report was clear. It said the current supply of oil would, by their calculation, last the world for about 41 years. For those who don’t regularly exercise their mental math muscles, it means that today we only have 33 years until the global oil tank runs dry. I wonder how many people reading this still believe that—likely, very few.

Instead, it’s quite the opposite. The notion that we are running out of oil is laughable. Look at light vehicle sales in 2014. They set an all-time record with gas guzzling SUVs leading the way. The days of penciling out the economic feasibility of buying a hybrid are a distant memory. The new slogan being thrown around by experts is “lower for longer.” These are probably the same experts who were rambling on about “peak oil” not long ago. Turn on the news and it’s filled with folks guessing where oil may bottom. Most are predicting it will go lower and in the short run they are probably right. But making short-term predictions is the kind of game economists like to play. It’s fun, full of mistakes, hard to track, and played by people who can explain why they are never wrong. Good investing is the opposite. It’s longer-term in nature, it’s frustrating at times, and comprised of people who must be willing to be wrong near-term in order to be right eventually.

With oil prices in the low $30s, companies are being forced to dramatically tighten their belts. Companies all over the world are slashing capital expenditures (cap ex). Most estimates have overall cap ex cuts in 2015 at about 20% and expect them to be around 25% in 2016. It has been 30 years since there were consecutive years of cap ex cuts for these companies according to the IEA (International Energy Agency.) What all this means is that we are setting up for another shortage. Will oil price shoot up in the next few months? Probably not—unless there is some sort of geopolitical shock (like a collapse of the current regime in Saudi Arabia). So it could be awhile before prices recover. Consequently, it makes sense to gravitate toward companies with the strongest balance sheets and proven staying power.

As is always the case late in a wicked bear market, a lot of people are telling us that we haven’t seen the bottom in oil. However, we’ve yet to find one who thinks oil prices will be in the $30s two to three years from now. To an economist or a trader, three years is an eternity. To a good investor, it’s just a realistic timeline.

Barring a severe global recession, it’s hard to imagine oil prices can stay this low—or even lower—much longer. For now, the big surprise could be that we get the lower but not the longer.

Federal Reserve……… the Right to Change our Minds. That should be the new mission statement of the committee in charge of setting monetary policy in the United States. As everyone knows, last month the Fed decided to begin a campaign of raising interest rates. They believed—and still do—that the U.S. economy can handle higher rates. On January 6th, Stanley Fischer, the number two in command at the Fed, re-affirmed his stance on increasing rates. Despite the rocky first few trading days to start this year, he even provided some clarity by stating that a series of four hikes in 2016 was “in the ballpark.”

The recent comments by Fischer highlight two potential surprises for investors. First, Fischer basically said that he believed that markets expectations for the number of rate increases was “too low.” After years of watching the Fed maintain rates at deep-recession type levels—despite a slowly expanding economy—the market’s skepticism about serial hikes is understandable. Fischer went on to say that the Fed “watches what the market thinks, but can’t be led by what the market thinks.” I don’t believe too many people are really expecting them to complete four hikes in 2016. If they “succeed” I expect it will be a surprise to the markets and if there is one thing markets hate it’s unpleasant surprises.

Speaking of surprises I think the Fed is in for one. The Fed is in unchartered waters after keeping rates this low for this long. They are, as we have written before, in a race against time. They desperately need economic turmoil to remain at bay long enough for them to restore rates to more normal levels. The potential risks seem to be mounting. Europe’s problems remain unresolved, as Germany seems to be the sole winner of the single currency concept. The Middle East has gone from bad to worse with the recent escalation between Iran and Saudi Arabia. China looks to be facing challenges stabilizing both their currency and stock market.

Ironically, Fischer also admitted that global uncertainties could cause the Fed to veer off path. What exactly does veer off path mean? During a recent speech in San Francisco, he offered a glimpse into what the Fed’s options may be if the economy can no longer be stimulated by interest rates at zero. I will attempt to paraphrase and simplify his responses (full article here).

1) Create inflation

2) Implement negative interest rates

3) Attempt to boost GDP through asset purchases and government spending

4) Eliminate the availability of a physical currency to prevent saving

While some of the above may make you queasy, the one that’s most likely is negative interest rates, largely because other

countries have tested this approach. One thing central bankers don’t like being is the guinea pig…unless you’re the Bank of Japan and you have no choice (due to 25 years of stagnation).

So while it would be a huge surprise if the Fed is forced to do an about-face from rate hikes to negative rates in 2016, we don’t think it’s as unlikely as many investors believe. For those willing to imagine the unexpected, consider this irony: Fischer’s speech came on January 3rd, just three days into 2016 which he’s depicted as the year of hike. Yet, the first topic two topics he addressed were whether the economy was facing structurally slower growth and what new tools they might come up with to combat it. Hardly, the first words you’d expect to hear from the man leading the charge to higher rates!

It should come as no surprise that the Evergreen Investment Team would like to wish all readers of the Evergreen Virtual Adviser a happy and healthy New Year!

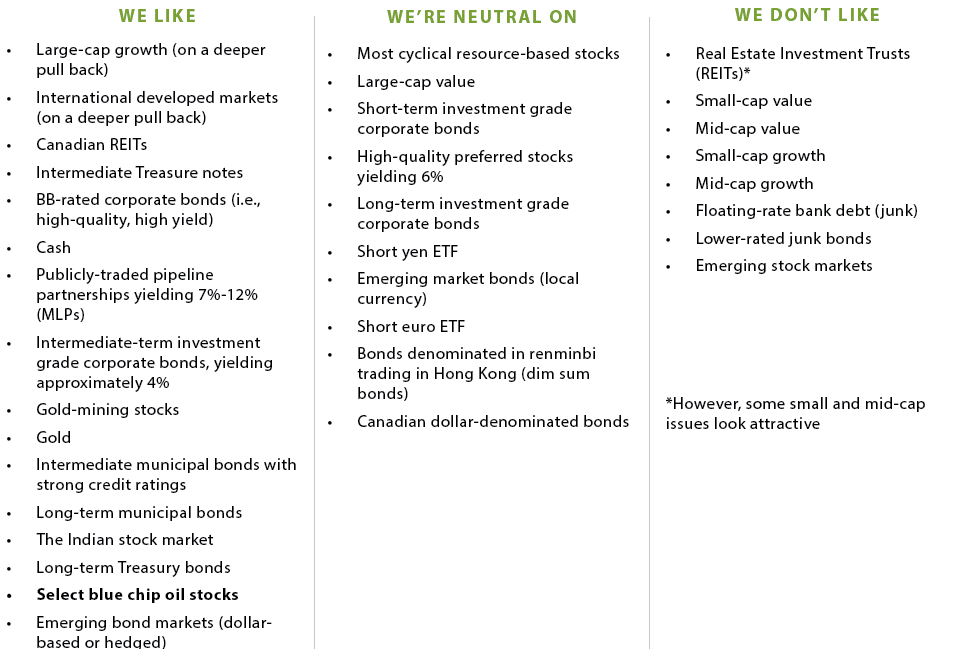

OUR LIKES AND DISLIKES.

Changes are bolded below.

DISCLOSURE: This report is for informational purposes only and does not constitute a solicitation or an offer to buy or sell any securities mentioned herein. This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. All of the recommendations and assumptions included in this presentation are based upon current market conditions as of the date of this presentation and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. Information contained in this report has been obtained from sources believed to be reliable, Evergreen Capital Management LLC makes no representation as to its accuracy or completeness, except with respect to the Disclosure Section of the report. Any opinions expressed herein reflect our judgment as of the date of the materials and are subject to change without notice. The securities discussed in this report may not be suitable for all investors and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. Investors must make their own investment decisions based on their financial situations and investment objectives.