“For those properly prepared, the bear market is not a calamity but an opportunity.”

- Sir John Templeton

SUMMARY

- Stocks have rallied over the past couple weeks as (1) China drew down its foreign exchange reserves to stabilize its currency, (2) the Fed decided to delay its second rate hike, and (3) the Bank of Japan surprised the world with a negative interest rate policy.

- Some investors see these events as cause for celebration, but we see them as reason to be worried about global economic and financial stability. From that perspective, we believe the latest up-move in stocks is nothing more than a bear market bounce.

- We believe the US dollar will ultimately weaken if fears of a US recession continue to rise and the Fed is forced to reverse course. However, history suggests the dollar can run a bit longer if foreign central banks ease aggressively, China’s currency free floats, and/or global risk aversion takes over in a powerful way. In that event, we would expect financial markets around the world to sell off significantly.

- With Japan’s unexpected move to negative interest rates last week, 23% of global GDP is now governed by central banks charging sub-zero rates on bank reserves. While it will undoubtedly lead to more misallocation and more financial system instability over the coming years, it also increases the risk of a Chinese currency shock, widespread competitive devaluation, and another surge in the US dollar in the short-term.

- Financial markets are likely to remain under pressure barring a sharp reversal in the US dollar. While it could be a head-fake, the greenback has softened considerably in recent days.

BEAR MARKET BOUNCE?

The following commentary is from the Evergreen Investment Team:

After falling roughly 10% in the first few weeks of 2016, US stocks melted up starting on January 20. Among the drivers of this rally were: (1) China deploying its limited foreign exchange reserves to temporarily stabilize its currency, (2) the Federal Reserve’s deciding to delay its second rate hike on fears of global stability, and (3) the Bank of Japan unexpectedly following Europe, Denmark, and Sweden into a negative interest rate policy.

Some Wall Street commentators interpreted this news and the subsequent bounce in global asset prices as a sign that the worst was over. They said that global growth jitters were somehow calming and that the US equity bull market would bounce back to new highs.

However, the Evergreen investment committee just looked on with skepticism. Yes, the stock market was clearly oversold, but we are not day traders. We are fundamental investors with a longer term outlook. Our view is that a bear market is already underway for most US stocks and recent events are more a cause for concern than for celebration.

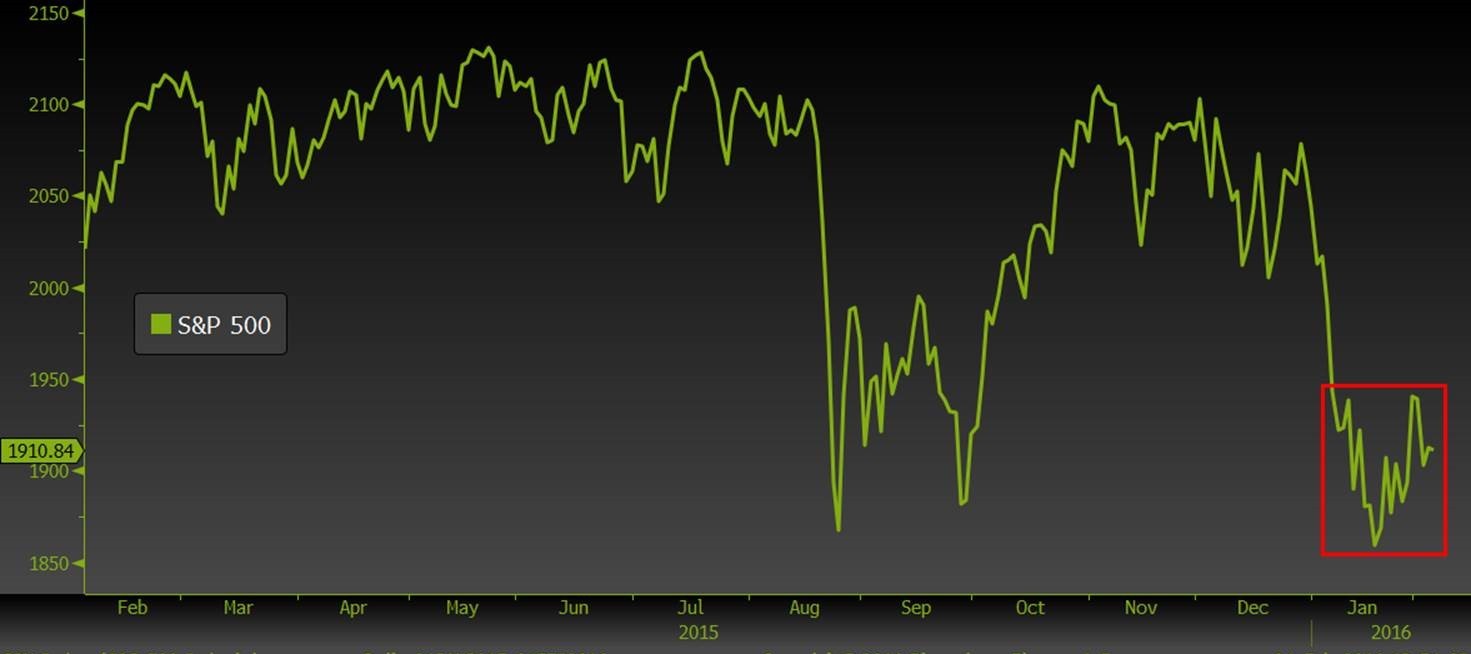

As you can see in the chart on the next page, it didn’t take long for the excitement to fade. This kind of volatility is a classic symptom of bear market sell-offs in which stocks tend to put in lower highs and lower lows all the way to the bottom.

S&P 500 SINCE 2015 Source: Evergreen Gavekal, Bloomberg

Source: Evergreen Gavekal, Bloomberg

The question is: what happens next?

As we’ve outlined in recent EVAs, Evergreen believes the Fed has been tightening for far longer than most people realize and that the resulting rise in the US dollar, fall in commodity prices, and tightening in credit conditions is pushing global markets to a breaking point.

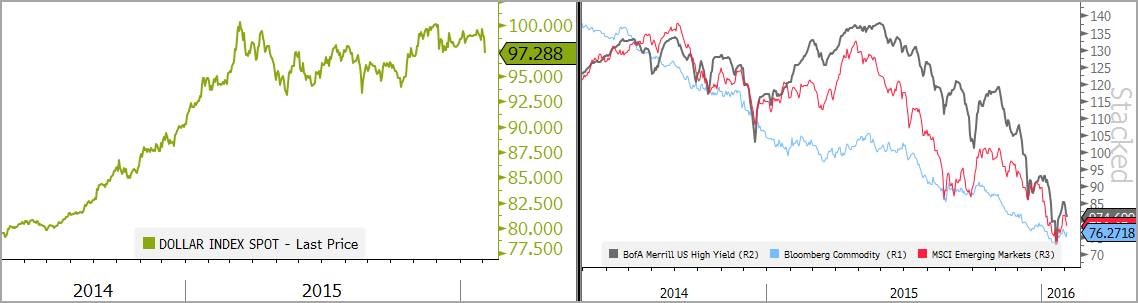

If that’s true, it also means that the trade-weighted US dollar could continue its volatile rally even as US economic growth softens and the stock market crashes… just like 2001.

TRADE-WEIGHTED US DOLLAR INDEX AND S&P 500 Source: Evergreen Gavekal, Bloomberg

Source: Evergreen Gavekal, Bloomberg

We’re not saying the dollar can run forever. US recession risks are clearly rising and we believe an eventual turn from Fed tightening to Fed easing will ultimately lead to a reversal in this powerful trend. But it’s important to note that—just like the stock market—dollar bull markets can dramatically outstrip their underlying fundamentals as we saw in the mid-1980s and in the early 2000s.

Over the last week, though, the US dollar has fallen sharply, a bit over 3%. That may not seem like much compared to the wild gyrations of the stock market this year but in currency terms, it’s quite significant. Our partners at Gavekal Research are wondering if this might mark the top of the buck’s incredible run since the summer of 2014. As they concede, it’s a huge “if” but the futures market is now implying a mere 10% chance of Fed rate hike in March.

In fact, a growing number of pundits are shifting to our view that Fed easing is more likely later this year than additional tightening. Should this perception become main stream, it undercuts the primary reason for the dollar to rise. Aside from the up-lift due to potential rate hikes—and the related, but now fading belief, the US economy is an island of economic strength—the dollar is extremely expensive against almost every other currency. In other words, it is over-priced and vulnerable to a deeper correction. You don’t need to look any further than Mexico and Canada to see how cheap their products and services have become compared to those in the US.

As you can see below, the dollar started to go postal in the summer of 2014. This is almost precisely when nearly every asset class on the planet began to crack.

US DOLLAR VS. JUNK BONDS, COMMODITIES, AND EMERGING MARKET STOCKS Source: Evergreen Gavekal, Bloomberg

Source: Evergreen Gavekal, Bloomberg

We believe mid-2014 will go down in the history books as the pivot point for this up-cycle in financial markets. Yes, the S&P rose a bit higher after that, strictly as a function of a handful of stocks like the infamous FANGs—Facebook, Amazon, Netflix, and Google (you may have noticed the FANGs* have been biting their holders so far this year). But most stocks essentially topped out during that fateful summer. And for asset classes like commodities, emerging market stocks, and the junkiest junk bonds, it’s been nightmare conditions ever since.

Consequently, if the dollar is truly in break-down mode, that should be very good news for the biggest victims of its spike. The fact that the yen is now higher than it was before Japan announced its negative interest rate policy gives some credence to the theory the dollar is topping. Also, the euro is higher versus the buck despite the European Central Bank’s head, Mario Draghi, promising to do whatever it takes to elevate inflation (central banker-speak for trashing its currency). The totally nuked energy sector would be among the most obvious beneficiaries if the dollar is actually reversing course.

Despite the hopeful scenario outlined above, we need to be realistic. And the reality is there is a lengthy list of negative developments occurring simultaneously around the world. One we don’t feel is getting the attention it deserves is the escalating banking crisis in Europe, especially Italy.

Then there is that Asian country—with “only” about 1.4 billion people—which may be facing a financial disaster of its own…

*The specific securities identified and described do not represent all of the securities purchased, held, or sold for advisory clients, and you should not assume that investments in the securities were or will be profitable. Facebook, Amazon, Netflix and Google, frequently used in market commentary using the FANG acronym, are used for illustrative purposes. ECM currently holds Google (aka Alphabet) and recommends it for client accounts if ECM believes it is suitable investments for the clients, considering various factors such as investment objective and risk tolerance. It may not be suitable for all investors. Certain clients may hold Facebook, Amazon or Netflix in their accounts, at their discretion; these securities have not been recommended by Evergreen. Please see important disclosures included following this letter.

RMB Wreck?

That’s the BIG shock we see dancing on the horizon as the world’s second largest economy—and largest trading nation—faces slowing economic growth and a high stakes policy conundrum. While the People’s Bank of China (PBoC) is working feverishly to prevent a credit crisis in its massive $34 trillion financial system with daily cash injections, the resulting rise in China’s money supply is leading to accelerated capital flight out of assets denominated in its currency, the renminbi (RMB, for short).

Depending on who you ask, between $700 billion and $1 trillion has left the Middle Kingdom in the past year. China’s central bank is spending its foreign exchange reserves at the fastest rate in history and, as a result, the PBoC may now have only $3.1 trillion left (assuming roughly $200B in January 2016 outflows) to defend against a domestic money supply of roughly $21 trillion. That’s beyond inadequate and may not last the year if Chinese savers vote with their feet. (China also looks to have roughly $5

trillion in dud loans. This amounts to a shocking 50% of GDP and makes the US mortgage disaster of 2008 look like a hiccup by comparison.)

CHINA'S FOREIGN EXCHANGE RESERVES Source: Evergreen Gavekal, Bloomberg

Source: Evergreen Gavekal, Bloomberg

As the old song goes, “something’s gotta give”. If that something is Beijing deciding to free float its currency – which could easily fall 15% or more – it would likely mean (1) a competitiveness shock to its export rivals, (2) a deflationary shock to its customers, (3) further declines in global commodity prices, and (4) a sharp spike in the US dollar (despite its flaws mentioned above). If you doubt the plausibility of this negative chain reaction, just remember the turmoil that hit financial markets during the two previous times China let its currency slide by 3% and 4%, respectively. This is far less than some estimates of how far it may slide if China actually allows the market to set its value.

To be clear, we’re not saying that a big drop in China’s currency is guaranteed. We’re saying that Beijing is running out of options every day the capital flight continues and anything that feeds these pressures—like another Fed hike or another round of competitive easing in Europe or Asia—raises the odds of a major shock. In other words, the RMB is a knife dangling over the markets’ heads from a fraying string.

Japan Goes Sub-Zero

With that in mind, why, oh why, would the Bank of Japan (BoJ) knowingly put the squeeze on China by surprising the markets with a move to negative interest rates? Because we’re living in a world where it’s every central bank for itself. Haven’t you heard?

Bank of Japan Governor Haruhiko Kuroda wasn’t messing around at last month’s World Economic Forum when he admonished Chinese officials to abandon reform and impose tighter capital controls. He knew exactly what he was doing and he did it anyway.

After years of ultra-low interest rates and more asset purchases (relative to GDP) than any other central bank on the planet, the Bank of Japan (BOJ) has failed miserably to boost inflation for any meaningful period of time or support a real recovery in economic growth. Yet it keeps upping the ante on a losing hand.

By taxing Japanese banks who hoard excess reserves on deposit at the central bank, the BoJ is trying to force new lending and reinvigorate an inflationary mindset. It’s the latest “new” attempt to address a debt problem with policies designed to fuel even more debt growth.

According to the Wall Street Journal, Japan’s decision to go sub-zero now means 23% of global GDP is now governed by central banks charging negative interest rates on bank reserves… with more on the way.

In case you are wondering why anyone would accept negative interest rates, there are several reasons. First, they may have no choice. A big bank with excess funds may not have another repository in which to place them. Also, if a country is experiencing zero inflation or deflation, a small negative rate is less penalizing than receiving ¼% when inflation is running close to 2% (basically, the current situation in the US). Then there is the convenience factor. For many large corporations, it’s impractical to hold large quantities of currencies or to conduct transactions in cash. Accordingly, central banks around the world are finding they can stick it to savers—even more than they already have!

Markets may temporarily see creative central banking tricks like negative rates and quantitative easing as a reason for celebration, but we believe the enthusiasm for these policies is dangerously misplaced.

Not only will negative rates lead to more broad-based capital misallocation in major economies and emerging markets alike, they’ll lead to more distortions in the already shaky European and Japanese financial sectors. It’s no coincidence that centuries-old Italian banks--having survived famines, plagues, and world wars—are now melting down. (Zero and sub-zero interest rates have allowed banks and companies that should have failed—the so-called zombies—to hang around, negatively impacting their healthier rivals; in other words, capitalism’s essential creative destruction is being subverted.)

You can see where this is all going over time, but let’s call a spade a spade. Central bankers are short-term focused and what the BoJ really wants—regardless of what it will publicly admit—is to weaken the yen at the expense of its export competitors.

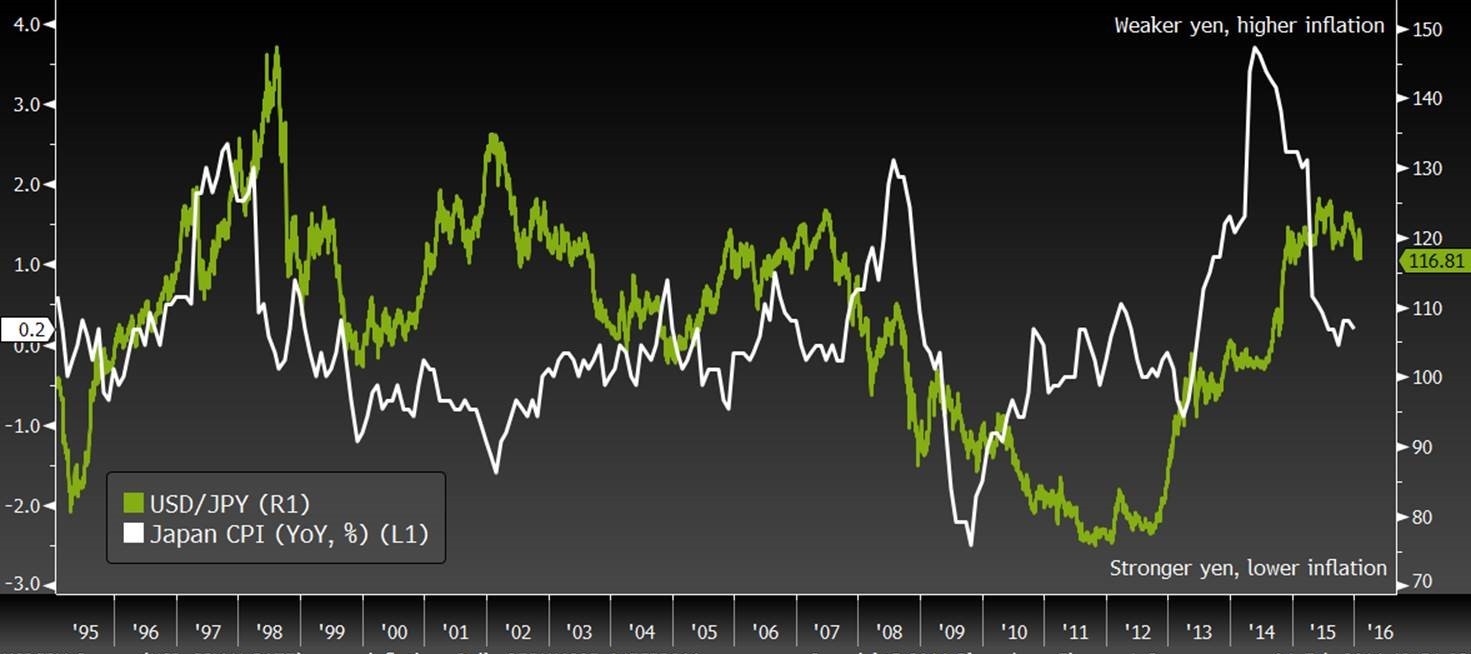

As you can see in the chart below, Japan’s currency tends to strengthen in periods of global risk aversion (like the late 1990s or 2008) as money comes back from emerging markets to repay short-term debts funded in yen. But because the rapid unwind of such “carry trades” typically results in a fall in exports and a tightening in Japanese financial conditions, it also drags significantly on inflation.

US DOLLAR/JAPANESE YEN EXCHANGE RATE AND JAPANESE INFLATION Source: Evergreen Gavekal, Bloomberg

Source: Evergreen Gavekal, Bloomberg

If Japan were to experience a carry trade unwind like it did in 1998 or 2008 (which would almost certainly happen in the event of an RMB shock), the blow back could be enough to throw the world’s most indebted government back into outright deflation.

So when Kuroda says the Bank of Japan is only halfway to his inflation target and that there is “no limit” to Japan’s ability to ease, he’s not just expressing an intent to resist further yen strength. He’s saying the BoJ is prepared to do “whatever it takes” to force the yen to 130/$ or 140/$ (down another 10% to 15% versus the dollar) with rate cuts, additional asset purchases, or both.

Cutting rates from 0% to -0.1% may not sound like a huge deal considering this Wednesday’s massive yen rally back to 117/$ as if last week’s BoJ surprise never happened. But think of it as dipping a toe in the water to test out the temperature before taking an even bigger plunge. We haven’t seen the big splash yet, but BoJ Governor Haruhiko Kuroda effectively just yelled “cannonball!” for all the world to hear.

Eventually, the Federal Reserve will be forced to do an about face to its own negative interest rate policy and probably resort to QE4. It will likely lead to a sharp reversal in the US dollar and shift the world into a new economic regime. But for the time being, the Fed is standing still, Europe and Japan are going sub-zero, and China may be running out of options.

It’s safe to say the growling sound you hear these days isn’t coming from your neighbor’s dog.

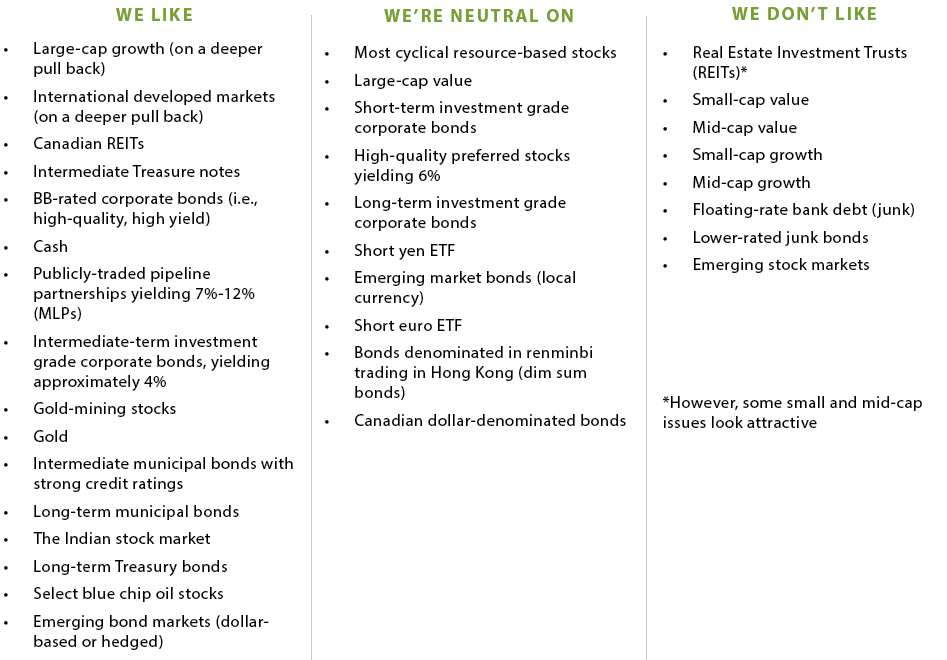

OUR LIKES AND DISLIKES.

No changes this week.

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness.