“One moment, the world is as it is. The next, it is something entirely different. Something it has never been before.”

-ANNE RICE, author of Pandora

The second quarter of 2018 kicked off with a bang as growing tensions in technology and trade sent investors searching for cover on Monday. In fact, it was the worst April start since… drumroll please… 1929. Technology, which began the week as a focal point, quickly took a back seat to the escalating global trade war. But more on trade next week.

This week, we’d like to present a March missive from one of Evergreen’s favorite guest authors, Grant Williams. In his piece, Grant outlines the Facebook scandal before discussing broader consequences for the technology sector. The main implication, as Grant points out and we very much agree with, is that sentiment has clearly shifted away from its decade-long stance that “Big-Tech-can-do-no-wrong”.

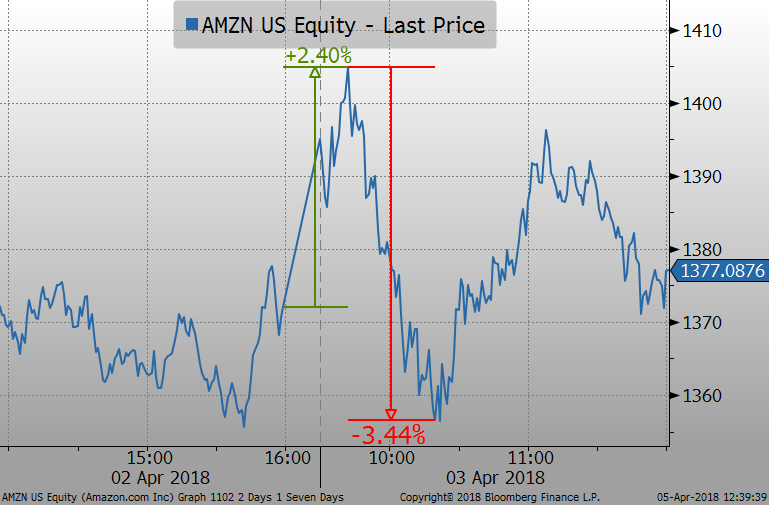

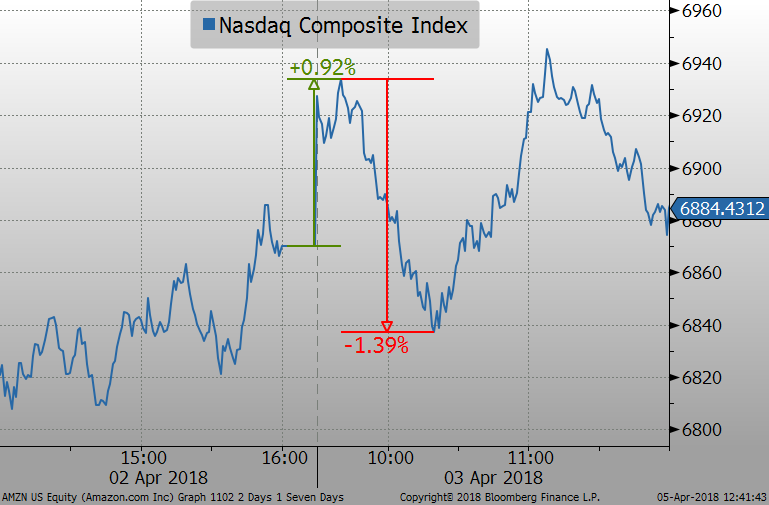

As the mishaps pile up for the big “F” (as in FANG*), others in the long-venerated quartet are taking equally devastating blows. The “A” (as in Amazon), for example, has been caught squarely in Trump’s crosshairs of late. On Tuesday, April 3 at 6:55am (PT), Amazon was up 1.4%. Eleven minutes and one little tweet later, both Amazon and the Nasdaq were in the red.

* FANG stands for Facebook, Amazon, Netflix, Google

Whether the overall environment for technology has permanently shifted, or this is a momentary blip on the radar for the primary catalyst in a very long bull cycle, remains to be seen. However, what is clear is that recent events have undermined the belief that no price is too high to pay for those dealing in the New Age currencies of big data and artificial intelligence. Blind buyers—aka, index investors—beware.

Michael Johnston

Marketing and Communications Manager

To contact Michael, email:

mjohnston@evergreengavekal.com

FACEPALM

By Grant Williams

(*Editor’s note: The article was too long to present in full form. Breaks in writing are marked with ellipses. To read Grant's full piece, please click here.)

Fifty million dollars used to be a lot of money but today, in a world where central bankers talk in trillions, it is, in the scheme of things, an insignificant amount.

Fifty million people, however, is still an amount which will make even the most jaded observer raise an eyebrow.

Fifty million people is the 28th-biggest country in the world. More populous than places such as Kenya, Spain, Argentina or Canada and twice as big as Australia and North Korea.

It’s also the number of Facebook users whose private information Cambridge Analytica harvested in improper fashion via an app called thisisyourdigitallife, the brainchild of one Dr. Aleksander Kogan, an academic at Cambridge University in the UK who, as a neat little sideline, ran a company called Global Science Research.

Kogan’s app was downloaded by about 270,000 people and, when they logged in to take a simple personality test (in return for nominal compensation), the app asked if they would like to log in by clicking a simple, innocuous blue button (you know, to save all the hassle of typing in emails or usernames and passwords).

The button is [just below]... Recognize it?

Of course you do.

That simple, innocuous button which graces so many apps and websites meant that Dr. Kogan’s app was granted access to not only the personal profile information of the lucky 270,000 who signed up for thisisyourdigitallife, but, thanks to their clicking of yet another innocuous button (one of those buttons that are really annoying when they pop up just as you are trying to get into your new app so you hurriedly click on them), and a tweak made to the Facebook terms of service back in 2015, data belonging to all their Facebook friends too.

Apparently, that meant Dr. Kogan’s app harvested the private data of 50,000,000 Americans – data which included (but was not limited to) locations, interests, photos, status updates, check-ins and, of course ‘likes’ – and 50,000,000 Americans is about 25% of those eligible to vote.

Now, given the fact that the average Facebook user has 338 friends, a quick calculation suggests that the potential number of people whose data ended up in the hands of Cambridge Analytica could be as many as 91,000,000... but let’s not go down that little rabbit hole.*

*Editor’s note: It was reported on Wednesday, April 4th that the data of 87,000,000 people was shared.

…

What we will do, however, is look at how the transgressions came to light, what the reaction has been and try to figure out the ramifications for Facebook’s future and, by extension, the future of other ‘Big Tech’. My gut tells me that this is one of those moments when genuine shifts occur.

Back in October 2017, my friend Peter Atwater, author of the indispensable Financial Insyghts letter, welcomed his subscribers to what he called The Backlash Era thus:

Tech Giants, Once Seen as Saviors, are now Viewed as Threats

The FANG bubble peaked in July – just three months ago – and already we are seeing this kind of criticism. Just wait. As confidence drops further, this headline will seem kind...

With some very minor tweaking, I could easily recast and apply these same thoughts to Harvey Weinstein. Powerful, overconfident men are about to face similar backlash – and not just in the media. Again, the worst simply go first.

Bullies are like prison wardens; they require perceptions of complete omnipotence to retain their power. The slightest weakness leads to complete collapse. A prison environment is binary: total control or no control - omnipotence or impotence...

For now, though, the important take away for the week is this: Whether in corporate or individual form, the behaviors associated with chronic overconfidence are being exposed at an accelerating, soon to be alarming, pace. Where trust has been violated, the price to be paid will be extreme.

We’ve now entered “The Backlash Era.”

If Peter is correct (and I truly believe he will be proven so), then the valuations of not just Facebook, but all the extended FANGs, will need to be adjusted.

Downwards.

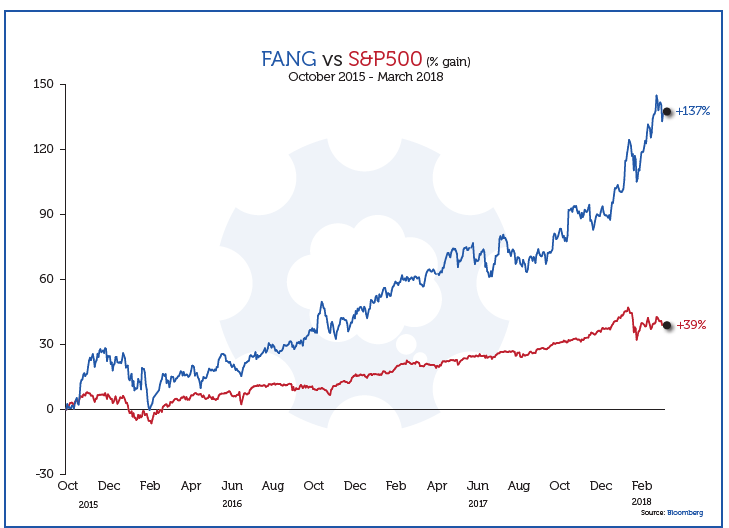

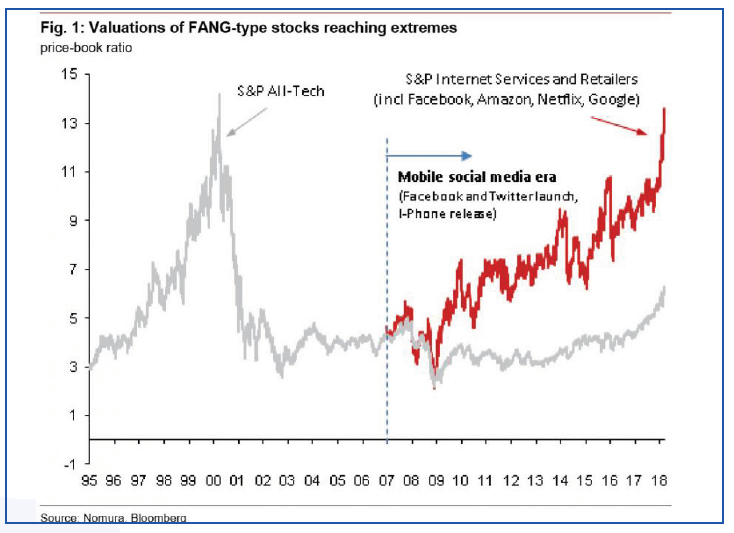

Since 2015, the outperformance of ‘Big Tech’ vs the S&P has been astonishing with the FANG Index up 137% vs the S&P 500's ‘measly’ 39% gain (chart, following page) and that run has lifted valuations to nosebleed levels with the FANG stocks trading at crazy multiples. Versus all tech, the FANGs have absolutely run riot.

Now, from these lofty heights, the first of the FANGs to crack will show the others the way because if you think for one minute that the problems Facebook is facing are exclusive to Mark Zuckerberg’s blue-and-white juggernaut, then you are sorely mistaken.

These issues around data-gathering are central to the business models of all of Big Tech and, as Big Tech = Big Data, the ‘backlash”’ that Peter Atwater talks about so elegantly is coming to them all.

…

[Respected commentators] also volunteered that it was time for steps to be taken to ensure Big Tech (or Big Data as some prefer to call them) is reined in.

None of this is good news for [FANGs]. The highlighting in the passage below is my own but it shows quite clearly the strength of the language being used to frame this debate and demonstrates conclusively the long-in-coming sea-change in attitude towards Big Tech:

(Jeremy Warner): The case against Facebook is that it allowed the data to be exploited without the consent of users, it failed to inform them that their data was being harvested in such a manner, and, I suppose, that it failed to ensure that the data had indeed been destroyed and could therefore not be put to further use.

…

That Facebook didn’t seem even to appreciate it had a problem is indicative not just of the company’s only quite recent entrepreneurial beginnings and consequent lack of politically-savvy, worldly experience, but also of Silicon Valley arrogance, a mindset that in true libertarian spirit revels in iconoclastic disruption of established norms and positively celebrates outrageous behavior.

Economic progress requires such players, but they stray beyond the politically and socially acceptable at their peril. It is rare, beyond the business pages, to hear a good word about technology and the internet these days.

…

All genuinely new industries initially thrive on their ability to stand outside the old conventions and constraints. But there eventually comes a tipping point at which public admiration and consent gives way to anger and condemnation. The “robber barons” of the so-called “gilded age” virtually invited the regulatory and antitrust crackdown that eventually befell them. Rightly or wrongly, the same fate awaits today’s tech giants.

Precisely. And therein lies the rub.

…

So, the Big Tech dam appears to have broken with Facebook being the first company to get caught in the cross-currents.

The stock plunged 7% on the news of the investigations that broke over the weekend, wiping $40 billion from the company’s valuation (and about $3B from Zuckerberg’s own personal wealth) and I personally believe this is just the beginning.

My friend Jared Dillian, author of The Daily Dirtnap agrees and offered some interesting commentary of his own which aligns perfectly with my own thinking and, like me, he is focused on sentiment:

(Daily Dirtnap): You may disagree that [the week of March 19th] was the turning point for FANG, and you may be right, but [the week of March 19th] was the turning point in sentiment, for sure. From here on out, bad news will be bad news, not good news.

This has been one of the toughest trades of all time, because negative sentiment towards tech has been building for a couple of years, but when do you put it on? It doesn’t matter until it matters.

Now it matters. I think you can safely short Facebook, or Amazon, or Netflix, or Google...

How far is this going to go? This is going to go until tech workers are hated more than bankers were 10 years ago. I logged on to FB this morning and there’s all kinds of fake political crap on there. It is a cesspool.

…

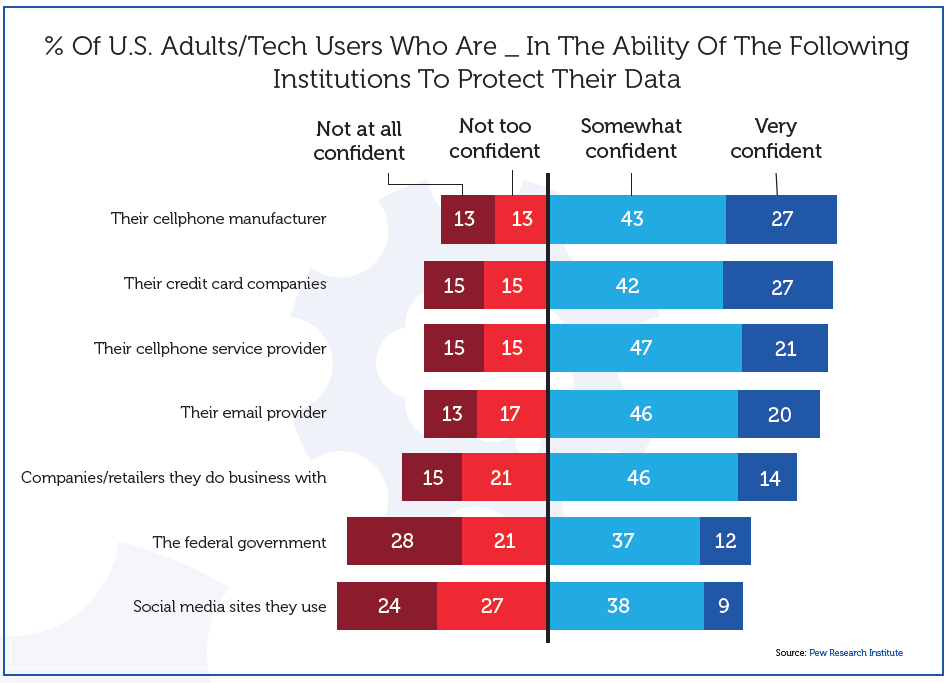

Adding to the problem, way back in March 2016, the confidence U.S. adults had in social media sites when it came to data protection was below even that which they held in the federal government and that takes some doing.

The events of the last couple of weeks sure as hell ain’t gonna help the dynamic which is clear in this chart:

So here we find ourselves, at by far the most critical juncture in the (until now) burgeoning relationship between investors, the general public and Big Tech.

For a decade, that three-pronged relationship has grown swiftly as every bump along the way has quickly been either smoothed over, or ignored by an enthralled public and an enamored investment community but, if we are where I truly think we are then things have changed and will unravel swiftly from here.

…

With Big Tech leading markets higher, any about-turn in sentiment towards them bodes ill not just for the sector, but the broader market and, given the increased volatility we’ve seen since February, the risk of a major tech-led dislocation is dangerously high.

OUR CURRENT LIKES AND DISLIKES

No changes this week.

LIKE

NEUTRAL

DISLIKE

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.