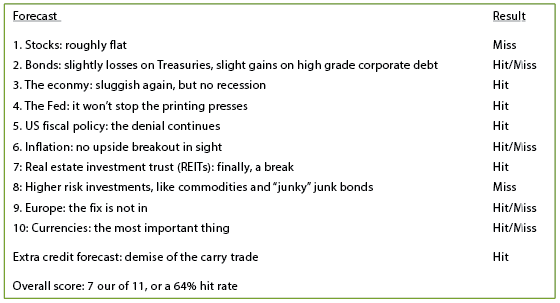

"If the experience of the past few years teaches us anything, it is that we should be cautious in our forecasts."

- BEN BERNANKE, in his final official speech last week.

Time rolls on! One of my friends has a less than elegant saying that is nevertheless quite accurate at my age: Life is like a roll of toilet paper; the closer you get to the end, the faster it goes. Underscoring how fast my roll is spinning these days, the Hay family rang in the New Year with the birth of our fourth grandchild, literally on January 1st. Wow, four grandkids! It was only three years ago when we had none. Regardless of the mortality check this represents to Grandpa Dave, we’re thrilled with the arrival of Ava Hay.

Also, driving home the fact that the years are flying by at the speed of light in a perfect vacuum (aka, the cranial cavity of your typical congressional representative), it’s also time to do our annual forecasts. As usual, with these issues there’s a lot to cover, so let’s get to it…

First, I’ll do a quick recap of last year’s "anticipations." As was the case in 2012, even though my overall score was respectable, missing on the stock market feels like it nullifies almost all of the good calls. However, I do want to clarify that our official forecast was for a sideways, not a down, market. Still, that call was akin to saying the Seahawks were going to have a decent season (if they keep this up, I might have to quit making fun of Seattle sports, which would be a huge relief to Jeff Eulberg, Evergreen’s fanatical fan of local teams).

A few of the above require some elaboration. First, despite being far too conservative on the market, my endorsement of more cyclical companies over defensive issues was solid. Further, I thought master limited partnerships (MLPs) would be an exception to the lackluster performance by other equity income areas, such as REITs and utilities. But my underestimation of how much the market would rise, despite a mushy economy and corporate earnings growth that flattened out, deserves a zero credit "award."

Also, the bond call would have been stellar had I not mentioned that corporate bonds would be slightly positive, and also touted emerging market debt, which struggled. My overarching point of preparing for higher rates was correct, but my bond prognostication still only deserves partial credit.

Regarding REITs, this score could be a bit charitable given that, even though they were down slightly on a price basis, they finished marginally up in 2013. However, REITs lagged the stock market by a whopping 30% (including dividends), and also were left in the dust by their kindred asset class, MLPs. It’s worth noting that I recommended MLPs a year ago, and they produced nearly S&P-like returns of 27.5%. (The MLPs Evergreen held for clients did even better, returning roughly 40%, for those that owned them for the full year). REITs have been tremendously popular in recent years, too popular in my opinion, but they have now trailed the stock market by roughly 50% since the start of 2010. This justifies an EVA view from 2010 and 2011 that stocks were much more attractive than REITs at that time, as were MLPs (which have also out-legged REITs over the last three years by a cumulative 20%).

On the flip side, I scored myself tough on inflation because, although I correctly anticipated it staying subdued (and, in fact, it was actually decelerating by year-end), I threw in some positive comments about gold that were dead wrong. Yet, the gold forecast was applicable to commodities where I gave myself a goose egg.

As far as Europe goes, I took just a half-score because while its economy was weak through most of the year, with unemployment continuing to rise, eurozone markets ignored bad economic news. This disconnect once again illustrated the elevating power of the trillions fabricated by central banks around the world.

Finally, my extra credit call was important because there was an utter bloodbath in the "carry trade" (borrowing short to invest long with very high leverage) last summer. This gave us the chance to buy numerous income investments, especially moderately leveraged closed-end bond funds, at extremely depressed prices and pre-crisis-like yields.

Now onto what the Evergreen team sees coming in 2014…

There’s no "I" in team. First, I’d like to bring up an important issue: As Evergreen has grown and evolved, younger members of our investment committee have been taking on added responsibilities. There is no way our firm could have doubled in size as it has since 2007, with assets under management now around $1.2 billion, without their extraordinary efforts.

Several of them have been with Evergreen for many years and have worked very hard to deserve the right to be more involved in the investment process (Evergreen clients, please realize that I continue to act as chief investment officer and make the final decisions, which, lately, you might wish wasn’t the case!). As a result, I’m going to make a bit of a shift and switch the tone from "I and me" to "us and we," reflecting the input and influence they have on our forecasts, as well as our positioning.

Forecast #1: The stock market. Given that I’ve been wrong about stocks in 2012 and 2013, after a string of years of being right, many of you might wonder why you should pay any attention to me/us. Besides the old argument about a stopped clock, we believe the body of hard evidence is on our side (of course, doesn’t anyone making more than a seat-of-the-pants forecast?). The reality is that virtually every indicator of future long-term returns, that has been proven historically accurate, is flashing at least orange, if not red, right now.

In fairness, a year ago these same measures were in the yellow category and that didn’t prevent the market from going up 30% in 2012. So, it’s certainly possible the market will rise from the orange/red zone into bright red by sprinting another 20%, or more, this year. The scarlet flag now, though, is that we’re seeing extreme examples of risk acceptance and speculation such as with 100 plus P/E stocks and the most dangerous junk bonds greatly outperforming high-quality debt.

Because past EVAs have reviewed in detail the various metrics indicating that the US stock market is dangerously overvalued, we won’t rehash those. But please allow us to bring up something that is fairly simple and, we think, truly novel (at least none of us has read it elsewhere).

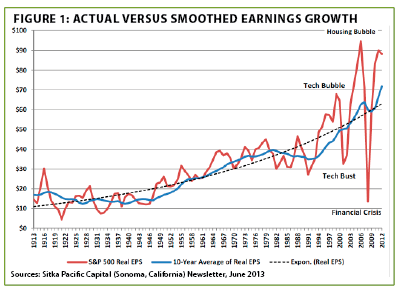

The S&P 500 can, and we believe should, be looked at like a cyclical stock, meaning that its earnings fluctuate dramatically over a full economic cycle. In fact, as noted in past EVAs and illustrated below, S&P 500 profits have become even more volatile over the last 15 years. (See Figure 1 on above.)

Experienced money managers know that one of the classic investment mistakes is to pay a low P/E for a cyclical stock, especially after years of strong earnings and a big price increase. Typically, a cyclical stock is a sell when it’s trading at, say, eight times peak earnings. This is because, being a cyclical entity, its profits plunge when business turns down and the P/E shoots up despite a falling share price. Then, around the bottom of the economic cycle, with earnings in the dumpster and, as a result, its P/E astronomically high, it’s time to be a buyer (assuming it’s inherently sound).

There is even a worse mistake, however: Paying a fairly generous P/E for top-of-the-cycle earnings. And that’s exactly what US investors are doing right now.

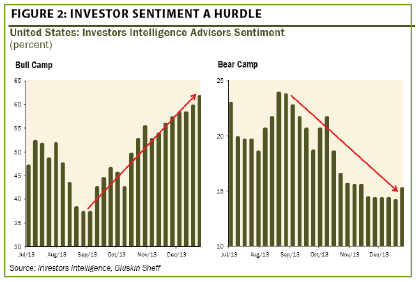

We also believe the odds of a "melt-up" are fading given the number of so-called bears who are calling for a hockey stick climax and the increasingly tired behavior of stocks recently. An "uplosion" could still happen, but it seems less likely. Regardless, the chances of a crashette this year are unusually high in our view. (Note: We are not predicting a crash, we are just saying the probabilities of a sudden 20%-type wind shear are much higher than normal.) The extreme skew in investor sentiment right now, with bulls greatly outnumbering bears, is one of many reasons this market remains exceptionally vulnerable to a radical attitude adjustment.

The bottom line is that we see stocks down in 2014, possibly sharply. A year-end rally could occur if the Fed loses its taper resolve and begins to binge-print again. However, that would simply delay a return to fair value on the S&P 500, which likely lies between 1200 and 1400. (Jeff Eulberg worries that eventually the markets will wise up to the ineffectiveness of the Fed’s Great Levitation, even for stocks.) It is Evergreen’s plan to, as usual, buy into any panic that develops. It’s been a long time since we’ve had that chance with stocks, but 2014 should provide such an opening. Caveat speculator!

Forecast #2: High-grade bonds. Speaking of panics, as noted above, we had a veritable freak-out in the bond market after the "taper tantrum" flared up starting last June. Frankly, this happened faster than we thought it would, the exact opposite of the stock market. There is already considerable value in certain parts of the income world, such as one of our favorite bonds yielding nearly 8% and numerous quality preferred stocks in that vicinity with some price appreciation potential to boot.

Yet, we are totally mindful and very respectful of momentum. Right now, the "mo" ain’t a go for bonds. We freely concede our cluelessness on whether the psychologically crucial 3% line will hold on 10-year Treasuries. Yet, while only time will tell if 3% is the peak, or just a stop along the way to the ultimate apex, we do believe very strongly that if rates truly rocket northward and approach 4%, this will put considerable pressure on many parts of what is still a very leveraged global financial system. Thus, we believe any vertical moves by yields will be self-correcting, quite possibly by triggering the aforementioned stock market reality check, similar to the shocker back in ‘87 (that would be 1987, not 1887).

Our best guess is that rates do move higher, and then come down rapidly during some kind of financial market convulsion. Overall, we’re calling for a flat-to-low return year from high-quality bonds in general but with better performance from those income vehicles

which suffered so severely last year. And for those with the fortitude to buy into a further yield eruption, should it occur, returns could be surprisingly good.

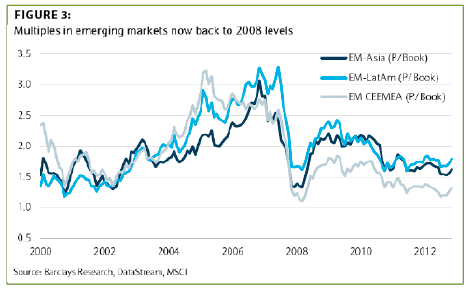

Forecast #3: International stock markets. After years of underperforming US stocks, most overseas markets now trade at major markdowns relative to the US. Based on price-to-book value, both European and emerging stock markets are exceedingly cheap vis à vis the S&P 500.

Viewing things through the prism of the Shiller P/E, which uses normalized earnings over the past decade (i.e., the cyclically adjusted P/E), overseas markets are also very inexpensive relative to the US. They may not perform in stellar fashion this year, should weakness in US shares reverberate around the world as it so often does, but they are likely to provide better, or less bad, returns. However, Europe still has the potential to disappoint; paraphrasing the legendary Kyle Bass: European policymakers have never missed the opportunity to miss an opportunity.

Forecast #4: The economy. We’re moving into the camp that 2014 is shaping up to be the best year of this not very expansive expansion. Don’t get us wrong: We’re not looking for anything spectacular, just better. Ironically, this could be the catalyst for a stock market shakeout as there has been a molecule-tight linkage between inflation (make that blotation) in the Fed’s balance sheet and stock prices.

Keeping short-term interest rates at zero and printing at almost a $1 trillion annual rate are totally inconsistent with even a lackluster economy. Such mind-spinning monetary largesse should only occur during deep recessions, bordering on depressions. If the economy grows north of 3% this year, as we think possible, the Fed’s stance will become increasingly indefensible. Even if 2014 turns out to be another year in which there is early strength followed by mid-year softness, which certainly could happen, the Fed will be hard-pressed to maintain its frenetic money spinning.

Given that stocks reacted so well to the initial tiny taper (emphasis on tiny), our central bank may feel emboldened to crank that up to a $20 billion a month taper. And, should the economic news look as husky as a lot of bright folks believe in the months ahead (including the once perma-dour David Rosenberg), the Fed might have to skip the taper and go right for the off switch on its overheating printing presses. That could be tough on bonds for a while but even worse for stocks. After all, bonds have actually fallen in price during the various QEs while the stock market has gone postal.

Forecast #5: Inflation. We’re feeling a little conflicted on this important topic these days. We agree with the David Rosenberg view that there is mounting wage pressure for those lucky enough to be employed and who possess valuable job skills. However, we also believe there is a serious disinflationary, almost deflationary, impact from currency devaluations such as Japan’s last year. Rumblings are that South Korea is preparing to devalue its won in retaliation over the yen’s buzz cut, which has rendered its exports less competitive.

We see these opposing forces roughly neutralizing and, as a result, we feel inflation will reverse its downward trend but stay contained, at least through this year. A caveat is that if there is a major financial accident, or a series of them, inflation could surprise on the downside. (A 20% fall in the US stock market wouldn’t qualify in this regard, but a 40% shrinkage certainly would.)

Forecast #6: Emerging market debt and US junk bonds. It might be unfair to lump these two together given the higher quality of developing world bonds these days. Yet the reality is they generally trade together with 2013 being a glaring exception to that rule. Junk bonds provided among the best returns in the fixed-income world in a very tough environment, while emerging market debt lost 10% on a total return basis in local currencies and was off 3.3% for bonds issued in US dollars.

This year, we’re calling for a reversal of fortune. In fact, closed-end funds in emerging market debt are right up there with our favorite investment themes at the moment. Yields are higher than with most US less-than-investment-grade debt and the credit quality is far superior. Not all nations are created equal in this regard, however, and it is wise to focus on those with the best balance sheets and current account conditions. The weaker countries are likely to suffer the most if we’re right about the Fed’s rapid downshift of QE (again, until, when, and if, the US stock market cries uncle).

Forecast #7: MLPs and REITs. Regular EVA readers would have been hard-pressed over the years not to notice our affinity for MLPs, in addition to our preference for them over REITs. As indicated above, MLPs have pulled decisively ahead over the past three years (and are way out in front over the last fifteen years). But we do worry that they are extended, particularly the new issues that have gone public recently. As with other initial public offerings (IPOs), these seem to be caught up in a mania where their higher growth rate versus those that have been around for a number of years is driving them to extremely lofty levels. Therefore, a shakeout in these is probable, but the more seasoned entities should hold up better buttressed by yields in the 6% range. We’re going to wimp out here a bit and forecast a slightly up to slightly down year for MLPs.

As far as REITs go, many smaller issues have come down very hard and look to be close to fair value, if not even below. We’ve begun to nibble a bit among these, but we still believe the big REITs look overvalued and might suffer some serious dyspepsia in an aggressive Fed-tapering environment. We see an actual negative return year for REITs in 2014.

Forecast #8: Commodities, including precious metals. Even though the US economy may well be at least taxiing hard down the runway, even if unable to truly achieve the long-sought "escape velocity," we’re not buying into the notion of a global boom, a fantasy an idea that seems to be gaining adherents. In fact, when it comes to the uber-important country of China, especially as it pertains to commodity prices, we think it is hunkering down to deal with the excesses it allowed to accumulate to combat the global financial crisis.

China might also suffer from the dry-docking of the not-so-good ship, QE3. So, we’ll go out on a bit of a limb and forecast another down year for most commodities. However, gold and silver, so thrashed in 2013, could well be the exceptions to the rule. We are intrigued by the stabilization occurring in the precious metal mining stocks, even in the absence of better price action by the metals themselves. The miners signaled trouble coming for bullion well in advance (we wish we’d paid more attention to that at the time), and they may now be giving an advance indication of an upside reversal. In sum, we like this sector, especially the producers, as a contrarian snap-back play this year.

Forecast #9: Currencies. We made a big deal about this topic a year ago and it did turn out to be quite important. Sharp declines in many currencies undercut the returns US investors realized on their overseas investments. The greatest currency erosion was incurred in countries with bloated trade and budget deficits, such as India and Brazil (former investor favorites), as well as Japan with its intentional yen debasement.

Yet even Canada, with much healthier fundamentals, saw its loonie swoon versus our not-so-almighty dollar. This was a negative surprise for us as we liked, and still do, bonds issued in Canadian dollars as a hedge against a potential US dollar crisis, particularly based on our unaddressed long-term federal budget problems (more on this in Forecast #10). On the other hand, we also liked Chinese dim sum bonds, and these performed exceptionally well relative to almost every other bond market on the planet, aided by a rising renminbi (China’s currency).

For this year, we see the Canadian dollar perking up, the renminbi slowly appreciating, the yen dropping a bit more, and the euro correcting hard after its recent surprising appreciation. So far, the US has been able to get away with its $3 trillion fabrication of funny money but—call us stubborn—we continue to believe there will be a price to pay, some day, some way.

Forecasts #10: Facing facts. We’re using this heading as a substitute for what we called "fiscal policy" last year. Specifically, it relates to the urgency of addressing long-festering issues such as entitlement reform, infrastructure rebuilding, tax simplification, regulatory rationalization, and a host of other debilitating issues. Unfortunately, we still see no meaningful headway in this regard despite some hints of bipartisan problem-solving recently.

We believe our elected officials continue to be lulled by a lofty stock market and negligible short-term interest rates, blinding them to the eventual perils in financing $8 trillion of government debt accrued in just the last six years. The complacency is shocking, even by congressional standards. It remains our belief that these political Rip Van Winkles are going to get the mother of all wake-up calls.

The fact of the matter is that despite an illusion of prosperity caused by the Fed’s great money dump, we are still facing some very daunting challenges. (Please click on this link from the usually bullish Investors’ Business Daily to see its eleven sobering trends.) We believe they can be solved but not by the current cast of clowns characters in Washington, D.C.

Extra credit prediction: Small cap massacre. Like last year’s forecast about the looming demise of the carry trade, we feel very passionately about the coming come-uppance for this market sector. US small cap shares are trading at 23 times earnings, a 50% premium to the S&P 500 which, as articulated above, is materially overpriced. Even the typically bubble oblivious Fed, has just issued a warning about this degree of valuation inflation.

Going into this year, small cap bulls justified the fact that they were trading more expensively than the market itself by confidently predicting 20% earnings growth. We commented at the time that this was ludicrous in the extreme, and here’s how it turned out: Small cap earnings actually fell in 2013! Naturally, in this age of limitless liquidity, that didn’t prevent them from rising by 36%. They have now been outperforming the S&P 500 for thirteen years and we believe that when the overall market gives back much of its Fed-fabricated gains, small cap valuations are going to get much smaller in a hurry. Thus, we continue to believe betting against this sector offers investors an excellent hedge against the next bear market.

Lost time horizon—the dangers of short-term thinking. To bring this forecast EVA to an end, I would like to discuss what I think is one of the most dangerous words in the English language, at least when it comes to investing: Extrapolation. Let me explain. According to Dalbar, the most authoritative source on the average mutual fund investors’ long-term performance, for the 20-year period ending 12/31/11 their returns were a piddly 2.1% per year. This is merely roughly equivalent to inflation, at least before taxes. A 50/50 blend of stocks and bonds would have generated 7.2% annually over that time frame.

Dalbar, through various comprehensive studies, has determined that the main reason for this shocking shortfall is the recurring tendency of most retail investors to invest via the rearview mirror. What has done well is assumed to continue to do well and what has done poorly is presumed to stay in the penalty box. Consequently, they sell out of their underachievers and put the proceeds into the hot areas, generally after several years of divergent performance. Invariably, this shift occurs not long before these trends reverse and the ugly ducklings become swans and vice versa.

While it’s impossible to know when US stocks will enter their next bearish phase, the fact that small investors are charging into stocks is concerning, especially given all the other warning flags snapping in the breeze these days. History tells us this won’t end well. It never has, and the more stocks inflate, the worse the deflation will be.

As Ben Bernanke admitted recently, forecasting is tricky business. Certainly, based on his track record, he’s got good reason to feel that way. And, as one who has had some big whiffs in recent years, despite a solid overall track record, I can empathize. Yet, the key isn’t to be right in the short run, like in a given year, or even over two, but in the long run. There remains little doubt in my mind that due to an extreme overreliance on the power of the printing press, and the avoidance of essential fundamental corrections to so many areas of our system that are clearly broken, we have another crisis heading our way.

It’s also my long-term belief that America will come to terms with its challenges and emerge stronger than ever. My best guess is that we’ll see a very different approach to managing our country starting in 2017, with both parties moving away from the dogmatic and toward the pragmatic. Yes, that’s a ways off, and there could be a lot of heartburn in the meantime. But for those willing to buy when the herd is stampeding away from risk—instead of blindly embracing it, as is the case now—the rewards will be immense.

IMPORTANT DISCLOSURES

This report is for informational purposes only and does not constitute a solicitation or an offer to buy or sell any securities mentioned herein. This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. All of the recommendations and assumptions included in this presentation are based upon current market conditions as of the date of this presentation and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. Information contained in this report has been obtained from sources believed to be reliable, Evergreen Capital Management LLC makes no representation as to its accuracy or completeness, except with respect to the Disclosure Section of the report. Any opinions expressed herein reflect our judgment as of the date of the materials and are subject to change without notice. The securities discussed in this report may not be suitable for all investors and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. Investors must make their own investment decisions based on their financial situations and investment objectives.