After listening to the array of speakers, many of great notoriety, at the Mauldin/Altegris Strategic Investment Conference (SIC) held in San Diego last week, the Evergreen Exchange team elected to select one speaker—and his/her main theme—to highlight for our respective section of this month’s edition. Our selections were driven by what we felt was the most urgent topic based on the current state of the financial markets. In addition, each of us will try to persuade readers why their choice was the most important. You, as readers, will be asked to vote on which of us made the best case (the voting link can be found on page 7).

Picking between so many brilliant minds is a bit like identifying the prettiest girl in the Miss America Pageant—there aren’t any bad choices, only better ones. My pick was the brash New York hedge fund manager, Peter Briger of Fortress Investment Group. However, if he was a contestant in a pageant, I doubt he would have scored too well in the likeability department. Among some of his more callous remarks were:

“I hate all of my competitors, every single one of them. I have nothing nice to say about them.”

“I get excited when a train crashes into a bunch of cars.” (Hopefully, he meant this figuratively, but I’m not sure.)

“I stay awake at night just hoping something bad will happen somewhere.”

“I try to walk into a situation of misfortune and walk out with a bag of money.”

And, when one attendee asked a slightly off-the-wall question, Briger responded with:

“To be honest, I haven’t spent a single second thinking about that.”

Needless to say, I don’t expect to see Peter Briger running a PR firm anytime soon. But, investing isn’t a beauty pageant or popularity contest. Investors aren’t interested in how polite the person is who manages their money. They want results. Briger’s firm has delivered and he personally gets considerable credit for the extraordinary profits they have produced. His specialty is distressed debt. Simply, he lends money in markets where traditional investors aren’t willing to operate. Briger has been spectacularly successful being what he calls “a garbage collector.” In one example, he cited making loans to the Michael Jackson estate and on Chicago’s famous Trump Tower. Briger has made himself into a billionaire as a garbage collector—proving once again there’s cash in trash—and I think his current mindset should be sounding an alarm for investors.

When explaining the current landscape, he called it boring. In order to make money, he believes a great investor needs a market environment that has a high amount of perceived risk but where the reality is much less worrisome. To illustrate an instance where perceived fear is high but actual risk is low, consider the following: Bungee jumpers, on average, have a 1 in 500,000 chance of death each time they jump, making it more than three times safer than bicycling. I doubt anyone’s heart races as much on a bike as it does when plummeting to the ground hoping a reflexive rope performs its job.

Why is this? How come something statistically safer generates more fear? One could argue that most people are simply unaware that bungee jumping is safer than bike riding, but that brings up an even more interesting point. After telling people that bungee jumping is 300% safer than riding a bike, do you think it would change your fear level just before you leapt off of a bridge? I don’t. There’s something extremely powerful about our psyche’s role in the relationship between our emotions and rational thought or, said differently, perceived risk and real risk. In certain situations, emotions become so powerful that we lose the ability to properly measure the probability of an outcome. In fact, it takes people entering this state of delirium for the best investors in the world to do their best work.

In early 2008, Briger said he saw a tremendous amount of real risk while most investors perceived there was minimal danger. He could foresee the looming disaster due to lenders finding a way to lend to anyone with a pulse. The credit bubble did pop and he made a lot of money for his investors and himself when it did. Today, he’s frustrated not because the perception of risk is low but because he doesn’t see any real risk. In other words, people investors seem dangerously complacent but Briger can’t identify a catalyst.

I think Peter Briger’s concept of real risk versus perceived risk was the most powerful concept I heard, because I believe most investors think about it inversely. Most people fear real risk when the true enemy is perceived risk. Real risk can’t be avoided—it’s everywhere. What can be affected is how much an investor gets paid to assume that risk, which is exactly influenced by the level of perceived risk. Here’s an analogy. Real risk is the rate of speed a car travels and perceived risk is the attention level of the driver. Clearly, the worst-case scenario is when real risk is high (car traveling fast) and perceived risk (not paying attention) from the driver is low. But just because the car is traveling at a “safe” speed doesn’t mean a driver can stop paying attention. Neglecting the proper attention, even at a slow velocity is still very dangerous. You don’t have to be moving fast to run a red light, veer down an embankment, or run over a biker (which may be why it’s more dangerous to bike than bungee jump!).

In today’s market, I agree with Peter Briger that real risk is hard to identify. What exactly will trigger a market decline isn’t obvious. However, exogenous (i.e., outside) shocks, like a severe geopolitical crisis, have the most market impact when investors least expect them. Beyond “geopol”, there are some obvious candidates but none seem to be a clear favorite. What I do think is present and more dangerous is the amount of perceived risk in the market place—or, more accurately, the lack thereof. Flow data into ETFs has spiked suggesting a massive shift away from investors with professional managers in favor a do-it-yourself approach. This phenomenon was also present right before the global financial crisis. The VIX, a market gauge of volatility, has remained at near historically low levels. A stock market, where downside volatility has gone missing, has helped medicate investors into a deep sleep. And if the market has been drugged, central bankers have been the anesthesiologists.

Briger’s comments resonated with me because I realized that it doesn’t really matter if you can’t always identify specific risks threatening the markets. What is far more important is the lack of perceived risk that begins to override our psyche and let our guard down. Historically, attendees and speakers at the SIC generally are quite bearish. It’s therefore of significant interest that this year’s presenters and audience had assumed a much more bipartisan constituency. This is a bit like seeing half the attendees at a conference of atheists saying a prayer before their meals.

The reason I chose Briger is because I think he challenged the fundamental way investors think about risk. Actual risk is secondary to the investor’s perception of risk. Most people spend all their time trying to forecast real risk and so little time understanding it’s the perception of it that really counts. I’m convinced, like Briger, that the biggest risk is when the investment community believe risk has been eradicated—such as by central bankers and their printing presses. While Briger lurks patiently, waiting to pounce on the next financial catastrophe, investors would be wise to use his insight to build a fortress around their portfolio—before the barbarians show up at the gates.

There’s a persistent rumor going around that I have a man-crush on Lacy Hunt, one of America’s most successful bond managers. While I can assure you that’s not true, I do concede that, in addition to my deep admiration for his money management skills, I also believe he’s onto the number one reason the global economy continues to limp along like a three-legged dog. In a word—and it’s of the four-letter variety—that would be DEBT. This is why I believe his presentation was the most meaningful at this year’s Strategic Investment Conference (SIC).

Actually, I was supposed to interview Lacy while we were both at last week’s SIC but, unfortunately, his schedule did not permit. On the fortuitous side, I did get the chance to appear on stage with my great friend and partner, Louis Gave, and ask him various questions, some of which were mine. Most, though, were from the audience relayed to me in real-time on an iPad. As the kids used to say, way cool! (Louis and I also recorded an interview for Real Vision TV; we will provide the link to this at a future date.)

Long-time EVA readers may recall that I’ve attended and written about this confab for nearly a decade. The numerous warnings put forth at the SIC back in 2006 and 2007 definitely played a big role in formulating Evergreen’s damage minimization plans eight years ago, when the housing bubble was poised to do its imitation of the Hindenburg disaster.

And just to show there really is no “bro-mance” between Lacy and I, I’m also going to quote some other speakers whose points overlap with Dr. Hunt’s main thesis, including several from the elegant and eloquent Stephanie Pomboy (who most definitely doesn’t look like a tomboy!).

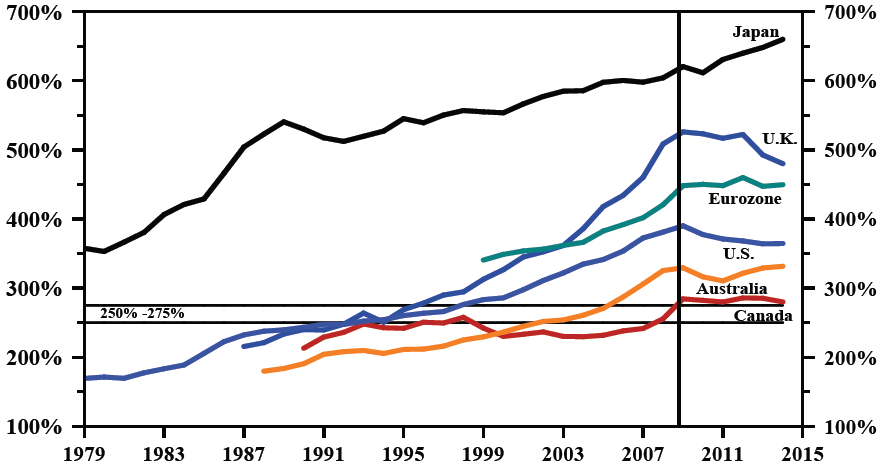

One of the reasons Lacy has been so successful running bond money is that he has gotten the long-term trend right and he’s stayed with it. It’s been his belief for close to 20 years that the overarching problem is that most of the developed world has created too much debt. He also believes you can’t solve an over-indebted condition with more debt. This seems pretty elemental and virtually inarguable, but very few prominent investors and/or strategists discuss this—especially not those whose paychecks are produced by that debt multiplication machine known as Wall Street. (However, the Bond King, Bill Gross, just chimed in on this in his most recent newsletter.)

TOTAL PRIVATE & PUBLIC DEBT AS A % GDP MAJOR COUNTRIES (ANNUAL)

Source: Bank of Japan, Cabinet Office, Statistics Canada, Federal Reserve, Bureau of Economic Analysis, Office for National Statistics of UK, Statistical Office of the European Communities, Reserve Bank of Australia. Haver Analytics. Through Q2 2014. US thru Q4.

Source: Bank of Japan, Cabinet Office, Statistics Canada, Federal Reserve, Bureau of Economic Analysis, Office for National Statistics of UK, Statistical Office of the European Communities, Reserve Bank of Australia. Haver Analytics. Through Q2 2014. US thru Q4.

Lacy’s contention is that there are certain definitive indicators of having hit the debt wall. If said collision has indeed taken place, you would expect the following:

-Because of the burden of excessive debts, inverted yield curves aren’t required to trigger downturns (this is a huge topic and I’ll revisit it in a bit).

-Productivity deteriorates (as noted in last week’s EVA), but it is not inflationary.

-Monetary policy becomes ineffective at catalyzing real economic growth.

-Despite super easy money, inflation weakens and there are even whiffs of deflation.

-Bond yields fall dramatically but they fail to stimulate.

If you think this sounds remarkably similar to current conditions, you win a one-year free subscription to EVA! Also, please realize that he’s been saying this for years, well before his thesis was proven by real-world developments.

Echoing the preceding list, Dr. Hunt also notes the following tendencies of over-indebted eras:

a. They are a global phenomenon;

b. They trigger rolling currency devaluations;

c. “Currency wars” produce only temporary benefits even for the early movers/debasers;

d. These debasements intensify global disinflationary, or even deflationary, conditions.

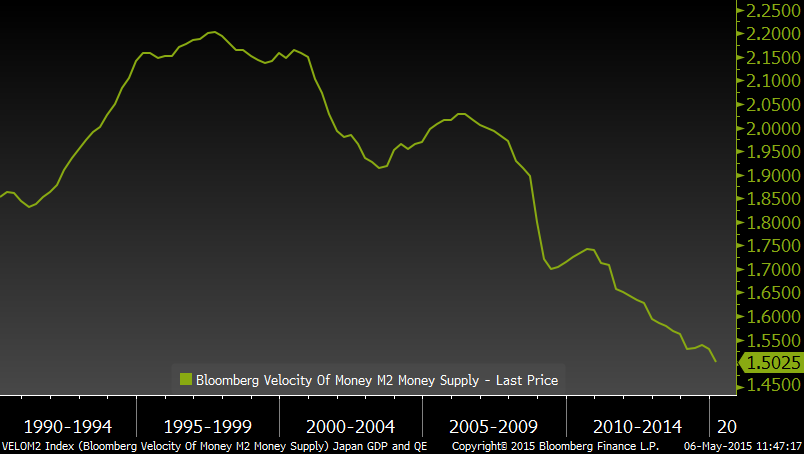

e. Falling money velocity negates the central bank largesse because there is too much debt of the wrong kind (i.e., used to fund unproductive activities).

US MONEY VELOCITY

Source: Evergreen GaveKal, Bloomberg

Source: Evergreen GaveKal, Bloomberg

Although the SIC has a rap of being a bit of a bear-fest, those of a Keynesian persuasion (i.e., with views 180 degrees removed from Lacy’s) were strutting around last week like roosters after a wild run in the hen house. Even David Rosenberg, certainly not normally a proponent of easy money policies, was in a sunny mood (if you’ve read him over the years, you know how unusual that is!).

Unlike Lacy Hunt, David seems utterly unconcerned about red-lining on debt. Rosie—who’s really living up to that nickname these days—sees no recession because the Fed hasn’t even begun tightening, much less inverting the yield curve, which he believes is an absolute pre-condition for a contraction. And without a recession, voila, there will be no bear market.

However, this is where I feel one of Lacy’s key views—that monetary policy becomes ineffective when debt levels are stultifying—comes into play. Stephanie Pomboy concurred with this in her presentation and then articulated what I have conveyed in past EVAs: The next recession is not likely to be triggered by an inverted yield curve but by some type of financial accident. In other words, instead of a recession causing a bear market in stocks, the order may be reversed.

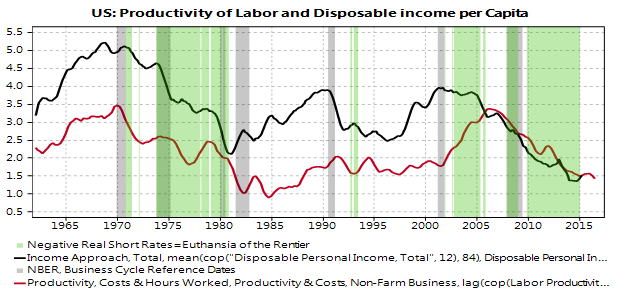

Louis weighed in on the subject of ineffectual monetary policies on a SIC panel of financial mega-stars. He brought up the still highly controversial notion that instead of zero interest rates being the solution, they might be the problem—another way of saying monetary policy is whiffing. Nearly the whole world seems to believe nanoscopic interest rates are beneficial. Yet Louis’ father, Charles Gave, has been writing prolifically on this theme in recent months. He has linked the Fed’s mostly squishy money regime over the last 15 years with the twin erosions in productivity and disposable income per capita, as graphically displayed next.

Consequently, if Lacy, Stephanie, Louis, Charles, and a growing number of others are right, then either we stay stuck in this never-never land of stop-start growth or we bite the bullet and incur the wrath of the financial markets by normalizing short-term interest rates. Longer term rates may not react much to this due to the inflation-inhibiting impact of a tighter Fed (in fact, the aspiring Bond King, Jeff Gundlach, believes they might fall should the Fed at long last raise rates).

However, there are an incalculable number of carry trade players—who have borrowed short to invest longer—and they are sitting right on top of the financial equivalent of the San Andreas Fault. Their world would be rocked like San Francisco in 1906 should the era of money-for-nothing end. The reality is there is no easy out when the dependency on debt and cheap money have become so ingrained and policy makers have fed (no pun intended) the addiction for such a long time.

US PRODUCTIVITY OF LABOR AND DISPOSABLE INCOME PER CAPITA

Source: GaveKal Research

Okay, my Exchange section has run over already so I’d better tie this all together in double-time. Global authorities have tried in vain to solve a debt glut with more IOUs (globally, these are up to $57 trillion since 2007, as noted in last week’s EVA, yet they have produced just $21 trillion in incremental GDP). To ease the pain—especially for the governments they represent—central banks have collapsed interest rates. But the private sector is not responding to the lower rates, other than to speculate in financial assets, because debt is already too high in the real economy. The soaring amount of borrowings, such as margin debt, is helping to drive up asset prices but is also sowing the seeds of the next market disaster. This, in turn, will trigger the next recession, not an inverted yield curve or a series of Fed rate hikes. Interest rates gone missing are hindering true economic growth due to the misallocation of capital (e.g., forming bubbles), the disincentives to make actual business loans (versus just funding takeovers, buy-backs, etc.), and the huge hit to cash flows in an aging society that needs yield on which to live (the war on savers, with Baby Boomers as the notable victims).

If Lacy continues to be right, as I think he will, any blip up in longer-term rates—or selling spasms in things like MLPs and, lately, smaller US REITs and even municipal bonds—is a crucial chance to secure livable cash flow at a time when it’s never been harder to find. According to Lacy Hunt, in a debt-drenched world, rates can flare up, but they won’t stay up. In other words, investors need to jump on these fleeting opportunities. And, to my simple mind, this may be the most important insight conveyed at this extraordinary meeting of great minds.

Last week, Mark Dow, a Washington-based hedge fund manager and blogger, joked over Twitter that he wasn’t able to attend the SIC because he wasn’t bearish enough to be allowed inside. While the conference’s speaker list was certainly filled with many cautious investors, EVA readers might be surprised to hear that two of the most bullish speakers were actually Evergreen GaveKal team members. During the conference, Louis Gave, Grant Williams and David Hay all shared the stage with some of the foremost thinkers in the investing world. While many of the presentations did in fact focus on the multitude of issues surrounding the global investing landscape, Grant and Louis decided to look beyond the immediate concerns in the developed world and chose to highlight other regions more likely to provide substantial long-term returns for investors. Keep in mind, at this stage of a bull market, when the low-hanging fruit has already been plucked, the only place you’ll find value today is by looking where everyone else is afraid—or too complacent—to look.

Grant, who presented with his founding partner of Real Vision TV, Raoul Pal, focused on what they’ve dubbed the Monsoon Countries. The Monsoon Countries are primarily located in Southwest Asia and Africa. These countries have used the seasonal monsoon winds to facilitate trade amongst each other for centuries. Raoul and Grant concentrated on 4 countries, Iran, Morocco, India, and Ethiopia. While each is in different stages of development, the long-term trends and tailwinds are astounding for many countries in this region.

For Louis’ presentation, if you’ve been reading EVA, you probably could’ve guessed that he talked about China. Louis gave a compelling presentation discussing the growth that is still ahead for this large nation, the cheap valuations of increasingly investable businesses and the dramatic under-investment by foreign investors in China’s financial markets. He even went as far as calling the global underweight of Chinese equities the most overcrowded traded in the world. And, based on the size of the throng at our GaveKal Evergreen mutual fund booth after Louis’ presentation, I obviously wasn’t the only one who found his case persuasive.

Certainly, each country mentioned by Grant and Louis represented an intriguing investment thesis in its own right. However, what really struck me was not how cheap each country looked individually, but rather the dramatic changes within the political landscape of each region. Ultimately to me, the message was one of change. A change from a region controlled by dictators, to one where democracy and capitalism will continue to gain traction. Thus, in the long run, investing in countries where democracy and capitalism are overcoming years of oppression, and now offer safer alternatives for growth, is clearly going to be one of the most rewarding investment themes of the coming decades.

As we’ve pointed out in the past (too many times to count), assets of the developed world trade at a significant premium to those in emerging nations. “Rich” country debts levels, compared to many emerging markets, are much higher. Growth in the developed world is a pittance compared to a basket of emerging market countries. Yet, today, in many of these countries, the premium placed on developed world assets may still be justifiable due to poor rule of law, the lack of significant financial centers, and the rampant corruption that still plagues what was once known as the Third World. However, as Grant and Louis both eloquently pointed out, these negative trends are changing. The growth of the Internet has given many of the world’s poorest people access to knowledge and a view of the world beyond their immediate surroundings. It’s allowed individuals to strengthen their voices by organizing and has presented a forum to voice displeasure and demand change. Repressive leaders can only fend off the expansion of democracy for so long. Eventually, all constituents will demand a say, and vital reforms will be enacted, erasing the main disadvantage of emerging markets. This is turn is likely to place pressure on the premium prices that flatter developed world asset today.

By this point, I’m sure many of you are thinking that democracy in countries like Iran or China will never happen, and you’re shocked at my impressive level of naiveté. However, based on a 2010 study done by Stanford University, the trend is absolutely in my favor. In 1974 there were only 40 democracies in the world, by 2010 that number had tripled to over 120 democracies globally (over 60% of the independent states).

Obviously, I don’t think we’re going to see broad and dramatic change tomorrow, but we need to be open to studying the significant steps that are being made in a positive direction. For example, China, as Louis points out, is far from becoming an open market that allows freedom of thought and expression. However, its leaders are taking substantial steps to be considered a key player in international trade. In fact, it is currently lobbying tirelessly to get the IMF to approve its monetary unit, the renminbi (also known as the yuan), as a Special Drawing Rights currency. To Louis, this is akin to 1980 when Japan allowed the yen to be liberalized, leading to an upgrade of Japan in most global equity indices and sparking a massive rally. Further, through the Shanghai Connect Program, the government is opening up mainland stock markets to allow for greater foreign investment through the Hong Kong stock exchange. The opportunity is substantial; in spite of being 15% of global GDP, China is currently a measly 1.7% of MSCI’s All-Country Equity Index.

Ask yourself this: If tomorrow, in a surprising announcement, China’s leaders fully open their financial markets and make the renminbi completely convertible into other currencies, how quickly would the world shift investable assets to that region? With China such a miniscule part of global indices—and assuming it is assigned a 10% weighting (roughly equivalent to the share of mainland stocks relative to the rest of the world)—the inward rush of foreign assets might swell into a virtual tidal wave.

How about Iran? As Raoul points out, it’s a highly educated and young country that is yearning for prosperity and the end to mullah rule. It has a long-established stock exchange and valuations are extremely depressed for obvious reasons. But the history of countries like this is that enormous profits are made as they begin to open up to the outside world. (If you think I’ve really lost it—even more than usual—please check out this video clip by Jim Rogers, the former partner of George Soros and one of the most successful investors ever in “frontier” markets.)

While events seem to be moving swiftly in China now toward much greater representation in global benchmarks, the progress in most of these countries is likely to be much more measured. However, we did find it fascinating that bond guru Jeff Gundlach told the SIC audience that he felt another Monsoon Country, India, was one of his favorite buy-and-hold-forever investments.

Now here’s the problem: As a fiduciary for our clients’ funds we have to be concerned about timing. We can’t just invest in emerging regions and have faith that at some point democracy and capitalism will prevail. We can’t risk our clients’ assets without having the confidence that our investments will be placed in a financial system that is fair and just. However, we’d also be doing a disservice to our clients if we weren’t constantly seeking regions that could provide better long-term growth opportunities than the pricey and slow-growing developed world we live in today.

For us, the biggest current concerns surrounding our favorite emerging markets—those where reforms are taking hold—is not the lack of stability seen in these regions, but rather the overvaluation of stocks in the developed world. In a global developed market correction, emerging markets are sure to go down as much, if not more than the larger markets. Therefore, based on the fact that we’re cautious on developed market prices in general, we’re hesitant to make a dramatic investment in the emerging markets at this point in time. We’re using the current environment to cautiously invest in the markets that we find attractive, while keeping the bulk of our assets in high quality investments that will weather the storm well.