_____________________________________________________________________________________________________

In this week’s newsletter, Gavekal’s Will Denyer talks about how the US Treasury continues to grapple with figuring out how much money it should pump into the American economy. With the government already running a staggering deficit, how they decide to proceed appears to be a largely looming question for the precedent of American fiscal policy going forward.

Going into 4Q21, a worry for me had been that asset prices faced the prospect of not one, but two tightening moves to US liquidity. First, any resolution to the debt ceiling stand-off meant the Treasury would stop dumping cash into the US financial system and start sucking it out through treasury bond issuance. Second, the Federal Reserve had signaled an intent to taper its money printing and asset purchase programs. Yet, with Congress now punting a debt-ceiling reckoning to December, this could, in turn, delay the Fed’s taper announcement to December, or even January. Thus, yesterday’s deal on Capitol Hill could allow temporary relief on the liquidity front.

The Senate yesterday passed a US$480bn increase of the debt limit through December 3. Some 11 Republicans joined Democrats to break a filibuster and pass the bill by normal procedures. The Republicans were not keen, but they caved in after President Joe Biden threatened the “nuclear option” of ditching the filibuster altogether. Recently, Congress also authorized government spending through December 3 to avert a “government shutdown”. Yesterday’s deal, if passed by the House, will authorize the Treasury to borrow enough money to fund that spending and service existing debt through December 3. In short, the can has duly been kicked down the road until that date.

Yesterday’s market rally was probably down to two factors. First, the risk, however remote, that the US government defaults on its debt has been punted to December. And if there was ever doubt, it is again clear that when push comes to shove, the US government will raise, or suspend, the debt ceiling, keep borrowing and keep spending. Second, is the hope mentioned above of respite from impending tightening moves to liquidity by both the Treasury and the Fed. In fact, the temporary impact on Treasury cash management will be slight, and the same likely applies to the Fed’s taper plans. But given the market’s sensitivity to Fed plans, that may have been enough.

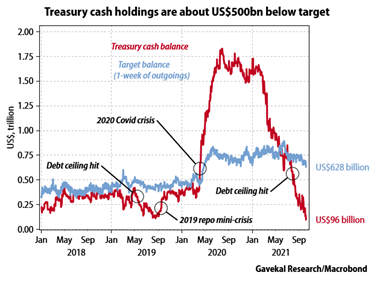

Consider the possible impact on Treasury cash management. The Treasury has been dumping cash since February, first to reduce its excess cash balances and then out of necessity. On August 1, after the debt ceiling was reimposed, it had to pay bills with existing cash, rather than new borrowing. As a result Treasury cash balances have fallen to less than US$100bn, or about US$500bn below its target of keeping a week’s worth of government outflows on hand. Hence, since the US government’s funding arm has almost no cash left to dump, it cannot be anything other than a contributor to tighter liquidity—whatever Congress does. The only question is how quickly the Treasury drains cash from the private sector, in order to replenish its own depleted balances.

The agreement to temporarily raise the debt-ceiling limit by US$480bn will presumably let the Treasury hurriedly issue a bunch of debt and get its cash hoard almost back on target. If it goes this route, there will be no delay to the great Treasury cash suck, and investors should brace for a rise in yields and a dip in asset prices. Even if the Treasury issues just enough debt to cover its deficits between now and December (maybe less than US$200bn), this will still represent a shift from dumping cash, to draining cash.

I have expressed the view that this Treasury cash suck, contrary to 2019, will neither cause a liquidity crisis in money markets, nor drive the Fed to reverse course on monetary policy. This time the system has far more excess cash and the Fed is better prepared to handle shortages that may arise with targeted facilities. The risk is more that long-term assets do not take kindly to the twin deteriorations in liquidity flows.

Still, the Fed would like to see the debt ceiling lifted and the Treasury replenish its cash before it commits to tapering. The Fed seems to be betting that money markets can handle the Treasury liquidity drain, but it may want confirmation before taking away the punchbowl. Hence, while I stand by my view that the taper is coming, it is now more likely to be announced after policy-setting meetings on December 15 or January 26, rather than November 3. Investors may welcome that delay, but asset prices remain under threat and portfolios should be positioned carefully.

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.