Two nays and a yea. There’s little doubt that the two most important developments in the financial markets over the last six months have been the stunning rise in the US dollar and the equally shocking collapse by oil prices. In this month’s edition of the Evergreen Exchange, we are taking a closer look at the former and debating whether the buck’s bolt might be coming to an end.

We’re treating readers by incorporating GaveKal’s co-founder Anatole Kaletsky, one of Europe’s most influential financial commentators, in this debate. As you will soon see, Anatole is very much of the belief that the dollar’s sprint is nearing the finish line, at least versus the euro.

In my section, I argue the case for why it may also be petering out against a number of other currencies as well, based on how expensive it is on a purchasing power parity basis. However, I do concede that a further overshoot is possible.

Tyler, on the other hand, contends that there’s more upside for the greenback than just a final blow-off. That’s certainly a distinct possibility, considering how expensive the dollar got during its two previous upside explosions during the mid-1980s and the late-1990s. (However, notice that, per my charts, the bigger the spike, the sharper the decline—a pattern eerily similar to the stock market’s past behavior.)

If your travel plans this summer involve going abroad, or if you’re starting to sense that foreign stocks might be where the best future returns reside, you will want to keep reading.

The following Exchange is by Anatole Kaletsky:

The Darkest Hour Before Euro Dawn. Two weeks ago, we suggested that the euro’s decline against the US dollar—probably the clearest consensus trade of 2015—could soon be over. As luck would have it, we published an article titled “Beware The Euro Consensus” on the very day the euro rebounded from a 12-year low against the US dollar of US$1.05. Dumb luck of this kind is certainly not evidence of wisdom or special insight. But now that the modest bounce following the euro’s March 13 nadir has closed out the worst quarter in the single currency’s 15-year history it seems worth reiterating some of the arguments we presented here two weeks ago.

As longstanding euro-skeptics (with a small “e”—it’s the single currency we are skeptical about, not the whole EU project) it gives us no pleasure to say this, but the euro now looks stronger than it has for years; both in terms of its survival prospects and of its likely exchange rate trajectory.

This may seem a surprising statement, given the signs that Yanis Varoufakis and Alexis Tsipras have negotiated Greece into a corner from which Grexit may be the only way out. But under the present conditions, even if Grexit happened it would probably not do the euro much harm. To understand why, we have to consider the truly historic event that took place in Europe over the last few months. This was not, of course, the Greek election, but the astonishing program of quantitative easing announced on January 22 by European Central Bank (ECB) president Mario Draghi and launched on March 9.

Radical Implications. The scale of this QE operation is far bigger than anyone imagined possible even a few months ago. Instead of placating German opposition by settling on a half-hearted version of the US, British or Japanese programs, Draghi managed successfully to face down and out-maneuver the Bundesbank—with radical implications that many market participants have not yet fully understood.

The ECB has pledged to buy €60bn of sovereign and asset-backed bonds every month until September 2016, a sum equivalent to 250% of the total net bond issuance of all eurozone governments over this period. As François has pointed out, this program is three times bigger relative to government borrowing than the Federal Reserve’s US purchases, double the size of QE in Britain, and 1.5 times larger than QE in Japan. On top of this, the impact of Europe’s QE program is amplified by the ECB’s audacious experiment with negative interest rates, never before attempted by a major central bank.

With the ECB now effectively underwriting the entire bond issuance of all eurozone governments (with the significant exception of Greece) and also monetizing a significant proportion of the outstanding stock of government debt, the economic underpinnings of the single currency have been transformed in at least four ways.

1) The ECB has virtually guaranteed that long-term interest rates in Italy, Spain and other struggling “peripheral” economies will continue to fall sharply, almost to the near-zero level of Germany, thereby providing a major boost to these economies and their credit systems.

2) The ECB’s willingness to finance not just the eurozone’s deficits but also a substantial portion of its stock of outstanding government debts has demolished the Maastricht taboo against mutual debt guarantees between different European nations. The ECB has effectively created a common European fiscal policy, and as a result has addressed the deepest structural flaw in the single currency’s design and the greatest threat to the euro’s long-term survival.

3) The convergence of core and peripheral bond yields guaranteed by the ECB’s indiscriminate buying of all eurozone sovereigns (apart from Greece of course) is rapidly reversing the financial fragmentation that imposed huge additional costs both on governments and on private borrowers in Europe’s weakest regions. This de-fragmentation provides a unique channel for QE to stimulate real economic activity and implies that QE could unexpectedly prove a more powerful tool in Europe than in the US, Britain or Japan.

4) The QE program effectively eliminates the threat of contagion in the event of a Greek exit, since the ECB is now guaranteeing full funding for the other Mediterranean governments at near-zero interest rates, regardless of any losses that may be suffered by investors in Greece.

That the QE policy has strengthened the euro’s chances of survival is obvious. More controversial is the idea that bigger than expected QE in Europe could lead to a strengthening of the euro against the US dollar (and perhaps even more plausibly, against the British pound).

No-brainer. Conventional wisdom holds that a currency is bound to weaken in response to QE and this seems particularly obvious in the case of the euro, because of the negative short rates in Europe and the expectations of at least a modest tightening in the US. This monetary policy divergence seems to make the weak euro/strong US dollar story a no-brainer. Perhaps—but obvious no-brainers have a habit of turning out to be wrong (that, after all, is what the term implies).

While monetary divergence is often the most powerful influence on currencies, it is not the only influence and is sometimes not even the dominant one. Current account imbalances have to be financed, and when these imbalances are very large so is the scale of capital flows required to ensure that monetary divergence dominates over trade flows. Last year the net capital flow required to weaken the euro against the US dollar was roughly US$350bn (averaging the US current account deficit of US$440bn and the eurozone surplus of US$260bn). This year, the flow will have to be considerably bigger than that, since the eurozone’s surplus is bound to increase substantially as a result of the devaluation that the euro has already seen. As a result, the euro will automatically strengthen unless capital flows from Europe into the US turn out to be substantially larger in 2015 than they were in 2014. Such an increase in capital flows is possible, but is it as certain as the market consensus suggests?

Record flows. While monetary divergence is widely expected to encourage bond flows from euros into US dollars, the strengthening of the eurozone economy is likely to have the opposite effect on equity and direct investment flows. And how sure can we be that bond flows from Europe to the US will really accelerate? These flows were already running at record levels in 2014, and the possibility of a steepening in the US yield curve as the Fed starts to tighten makes long term bond holdings more risky in the US than they are in Europe, since Draghi has essentially guaranteed that yield curves cannot steepen anywhere in the eurozone until after September 2016.

Finally, there is the behavior of foreign central banks and sovereign wealth funds. These institutions saw the creation of the euro as an opportunity to shift part of their currency reserves out of the US sphere of influence. They are now more likely to accelerate this diversification than to reverse it. While very low euro interest rates will to some extent discourage diversification, this small financial deterrent will be more than offset in the minds of many Asian and Middle Eastern politicians by the newfound enthusiasm in Washington for applying economic sanctions to advance US geopolitical interests. This process is sometimes described by US officials as “weaponizing the dollar”. Assuming that the single currency’s survival is no longer in question, the euro may well seem more attractive to many investors, even with negative interest rates, than a US dollar that is being weaponized, and that is now 20% more expensive against the euro than it was just a few months ago

The following Exchange is by David Hay:

Who knew? If most affluent Americans were totally honest, they would admit they were convinced that when Barrack Obama was first elected in 2008 his policies would be harmful both to the economy and the financial markets. They would also concede their fears were intensified when he was re-elected in 2012, notwithstanding the fact that the economy had mounted a feeble recovery, while the stock market had rallied rambunctiously for nearly four straight years. As we all know now, wrong on both counts.

In the case of this author, I asserted that Mr. Obama would gradually move to the center, and that his policies would not prevent the market from recovering after the devastation it suffered in 2008 and early 2009. Make that wrong and right (I’d rather be right for the wrong reason than wrong for the right reason!).

The pushback I received on my bullish views during Mr. Obama’s first term was considerable and relentless. However, it was equally intense toward my even more against-the-grain positive stance on the US dollar. At the time, I strongly believed the greenback was seriously cheap relative to many other currencies, particularly the euro and the yen. Although Evergreen has stayed with its anti-euro and anti–yen positions—taking some profits along the way—I became too cautious on the US stock market by 2012, as most EVA readers are aware.

Incredibly, the US stock market has gone up for all six years of Mr. Obama’s presidency. This is despite what I think is safe to say have been the most progressive policies (cynics might call them “regressive policies”) since at least Jimmy Carter, including the biggest tax hike in history. Yet, the stock market has celebrated those very policies to a degree unseen since the late 1990s, when another Democrat—but one with a far different economic agenda—was in the White House. Clearly, as we wrote when Mr. Obama was first elected, stock markets often do better under Democratic presidents than those from the Grand Old Party.

Much the same could be said of the US dollar. It bottomed not long after Mr. Obama took his first oath of office. Its initial rise was moderate and erratic but, recently, it has experienced one of its most impressive rallies of all-time. Again, how many investors thought that was in the tarot cards?

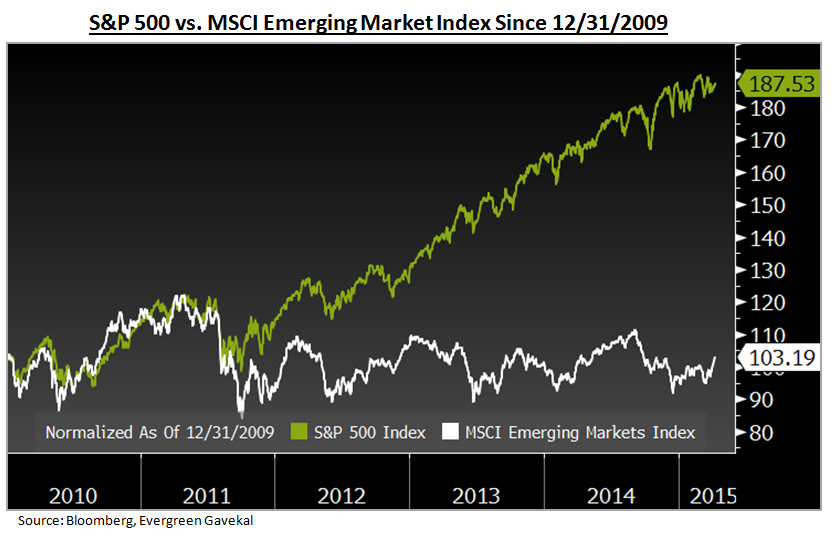

One of the bullish arguments for the dollar (put forth by Evergreen back in 2010 through 2012) was that currencies are a relative, not an absolute game. By this we meant that you can’t just look at a country, like the US, and conclude its currency is a loser due to its many national flaws without considering the sorry state of its peers. Consequently, we argued repeatedly that the US was in better (or, at least, less bad) shape than most other countries, but especially relative to the eurozone (sorry, I know it’s not exactly a country) and Japan. This viewpoint also led us to be less than enamored with emerging markets.

Those twin contrarian views caused us almost as much ridicule back then as our negative stance on US stocks does today. Ironically, emerging markets did in fact deliver the fastest economic growth, but that didn’t prevent them from massively lagging the S&P 500.

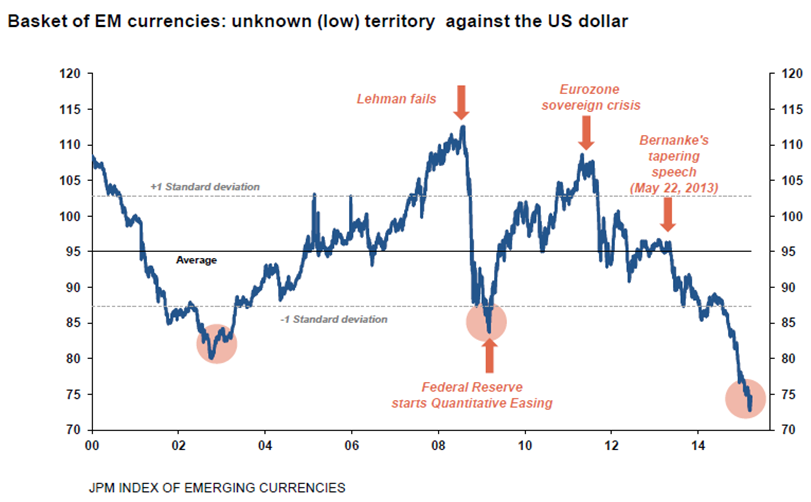

The same is also true of the US dollar in this regard. It was almost as widely accepted that the US dollar would continue to fall against developing world currencies as it was that Mr. Obama represented the Grim Reaper for the financial markets. Emerging market corporations were so sure the dollar would only erode that they, in essence, established a $9 trillion short position against the buck by borrowing in US dollars, often to finance projects with little prospect of earning economic returns (think Brazil and China, just to name two). Once again, this groupthink was a woefully errant exercise.

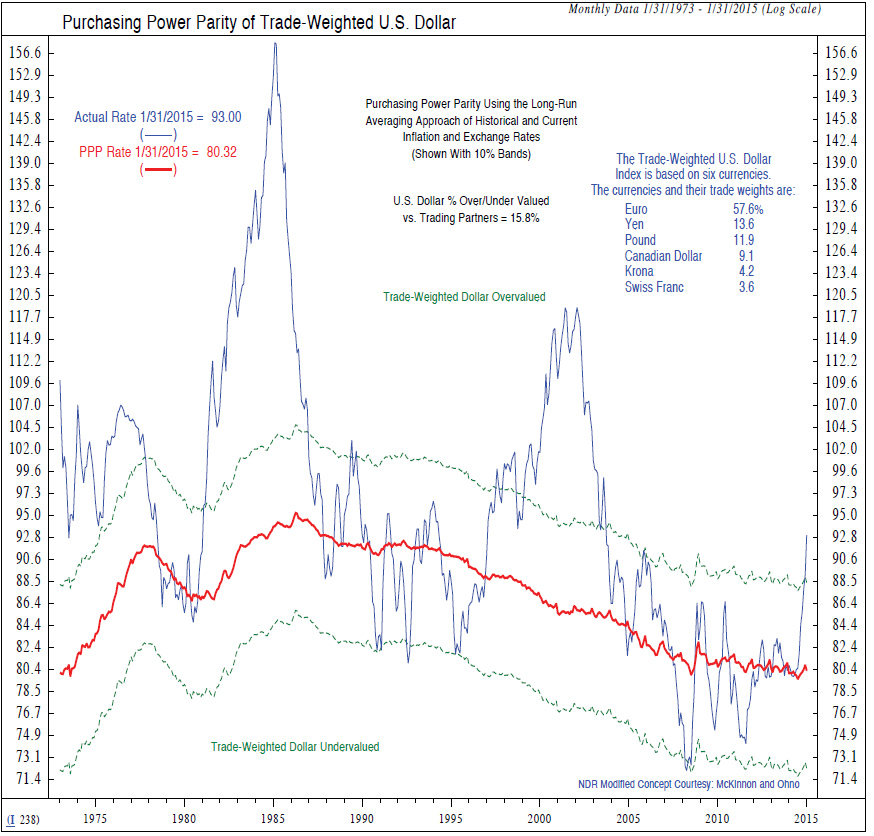

Today, bullishness toward the US dollar is running as feverish as it is toward our stock market, despite a slight cooling of late. And, unlike several years ago, the dollar is now very expensive on a Purchasing Power Parity (PPP) basis, though it has been more so in the past. And the ascent from fair to overvaluation has occurred with remarkable speed.

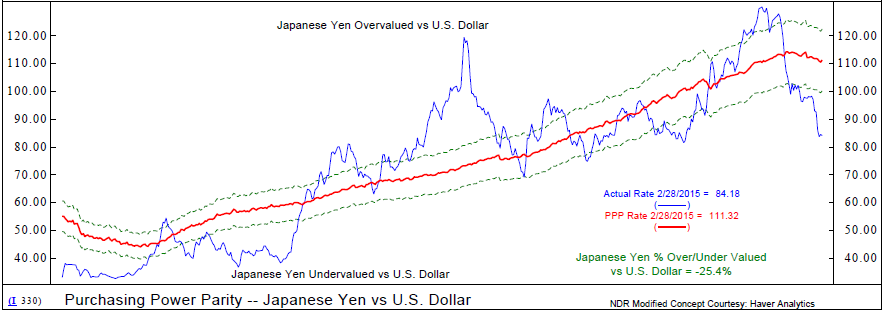

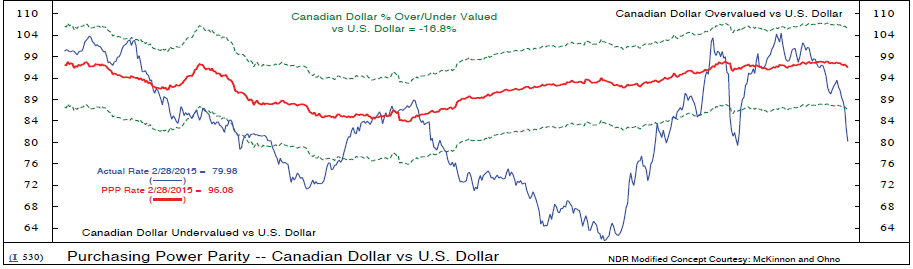

Anatole did an excellent job in his section of pointing out that the euro is now materially undervalued versus the dollar, but I wanted to focus on the yen and the Canadian dollar (surprise!). As you can see, both are in deeply discounted territory versus their PPP with the greenback.

In a momentum-driven world such as we increasingly find ourselves, the dollar can certainly become even more expensive. At least on a near-term basis, though, I believe a sharp correction is probable. (Full disclosure: Evergreen maintains short positions on the yen and the euro as partial hedges against our positions in Japanese and European stocks; however, we have reduced those in recent months.)

Perhaps you’ve noticed that the supposedly hitting-on-all-cylinders US economy has been misfiring more than a little lately. It’s fair to note that another brutal winter on the east coast and the dock strike on the “left coast” have been factors but economic data released after those impacts have faded continue to look squishy. Thus, it’s reasonable to conclude that the extraordinary spurt by the dollar is biting. As previously noted in these pages, credible estimates are that the dollar’s surge has been equivalent to a two percent rate (200 basis points) increase by the Fed.

Consequently, the current loser in the global currency war is the US with the greenback now nearly the most expensive currency in the world, save for the Swiss franc (CHF in the chart below). As Anatole points out in his piece, the dramatically weaker euro is already boosting the long comatose European economy. And, per last week’s EVA, corporate Japan is feasting almost like it’s the 1980s all over again, thanks to the deeply undervalued yen.

This is why Evergreen’s long-time negative view of the yen and euro is shifting. Currencies are typically self-correcting, as an overpriced monetary unit often causes economic weakness that eventually drives down said currency (and vice versa). Because this appears to be happening in the US, it certainly gives the Fed—always on the look-out for reasons not to raise rates—more cover to remain as easy as Keith Carradine in Nashville. This also undercuts one of the main reasons to be dollar-bullish.

It’s a crazy world out there with the assumption that debasing money is a good thing, a view that I still believe will be shattered at some point. But in this wild race to the bottom, the US appears to be falling behind—for now.

The following Exchange is by Tyler Hay:

King Dollar Regains Its Crown. At Evergreen, agreeing with a consensus viewpoint can be a vulnerable position in the long run, even though it is often rewarding in the short run. In fact, we take pride in avoiding “groupthink.” After all, we believe it defies logic to expect to achieve an outcome superior to the norm while utilizing a mainstream approach. Thus, it is with careful consideration that I make my case regarding the strength of the US dollar given the stance of my fellow investment team members. We believe that debate and disagreement is a healthy part of the opinion-forming process at Evergreen.

Currently, the investment community is predominantly bullish on the US dollar, which does admittedly cause me some pause. However, in this case, I believe that the consensus is correct and that the dollar will remain strong against most major currencies for an extended period of time. There are a few powerful forces on the investment horizon that are likely to provide significant support to what has, once again, become King Dollar.

For example, current US yields stand markedly higher than almost the entire developed world. It’s not simply important to observe that the absolute levels of US government bond yields are more attractive than those in Europe or Japan and therefore capital will continue to flow stateside. The crucial aspect is the divergent roadmap the US is on relative to most of the developed world. As Anatole points out, the QE program recently announced by the European Central Bank is three times the size of what the Fed attempted in the US. Meanwhile, Janet Yellen is preparing to move in exactly the opposite direction with a rate hike, which looks like it will occur in the third quarter of this year. In the context of a currency war, the Fed looks to be retreating while the rest of its peers are calling in the cavalry. Investors who are expecting the dollar to weaken will have to answer how much money stands to flow out of the dollar while the yield differentials on government bonds likely become more skewed in favor of US Treasuries.

Another unavoidable reality for those who are calling for a currency correction is the current level of stocks in the States. Among a growing number of valuation metrics, the US bull market (which we’ve covered extensively) is nearing historic milestones in terms of both its length and strength. In the event of a serious US stock market sell-off, which would likely rapidly spread around the world, global investors are almost certain to run for safety. If the financial crisis taught us anything, it’s that the investors still view US Treasuries—and the dollar—as the ultimate safe harbors when financial storms strike.

Aside from the structural tailwinds for the dollar I highlighted above, currencies don’t always adjust based on perceived parity. It wasn’t long ago that the euro traded at over 1.40 to the dollar. Many market experts, including our team, our partners at GaveKal, and others felt the premium was unwarranted given the economic position of Europe relative to that of US. For years, unemployment, and GDP growth results out of Europe were much weaker than in the US, and yet the euro refused to crack against the dollar. So, for those who are making the argument that the purchasing power parity of the dollar is too extended, currency markets can remain “mis-valued” for an extended period of time. Bond savant Jeffrey Gundlach comments that currency trends are often “persistent and long lived.”

If you are wondering what might make me reverse my stance on the dollar, the Fed holds the key. Though I’ve long been skeptical the Fed would actually have the courage to pursue a rate increase, they look to be close to pulling the trigger. This is despite warnings from many investors—including Larry Fink, CEO of mutual fund giant Blackrock—that the Fed can’t dare to raise rates as planned. Higher rates will likely send the dollar even higher, putting American exporters at a further disadvantage. If the Fed becomes skittish and were to change its stance—or, even worse, launch additional rounds of QE—this could admittedly cause a serious weakening of the dollar.

The dollar’s rally has been swift and impressive. While I concede that currencies are inherently range-bound and self-correcting, it doesn’t always happen immediately. While certain countries, especially those that are not blatantly debasing their currency, have seen dramatic collapses versus the dollar (i.e. Canada), and may provide a profitable place to deploy some assets, I suggest caution. I don’t believe that investors should think that playing a US dollar weakening is a theme that will prove to work broadly. And companies with significant negative exposure to a strong dollar are likely to continue to face prolonged challenges. In our present environment, so heavily manipulated by central bankers, I reserve the right to reverse course but, for now, it’s full speed ahead for the USS dollar.