“I’m convinced that everything that’s important in investing is counterintuitive, and everything that’s obvious is wrong.”

-Superstar investor, Howard Marks, from his acclaimed recent essay Dare to be Great II

POINTS TO PONDER

1. Most economists seem to believe the negative effects of last year’s massive tax hike impacted 2013 economic activity. However, with affluent individuals having just sent in their IRS payments this month, 2014 may be the year the actual drag is felt. Additionally, this latest increase has further shifted the tax burden even more onto the top 1% (which also reflects that income has become more upwardly skewed). (See Figure 1)

2. Highlighting how important the US energy revival is to job creation, Investor’s Business Daily reports that since the end of 2006, oil- and gas-related hiring has increased 58% versus a mere 0.21% bump for total nonfarm employment in general.

3. US stocks remain up roughly 50% since the start of 2012, despite the modest recent correction. Ironically, 2012 was the last time aggregate earnings estimates were raised rather than cut.

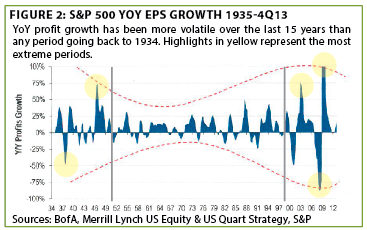

4. It’s interesting to look back at nearly 90 years of US stock market history with regard to the long-term trend in earnings fluctuations. It appears that there have been three distinct phases in terms of profit variability. The 1930s and 1940s were characterized by a fair degree of earnings volatility. Then, from 1950 to the late 1990s profits were in a fairly steady uptrend. Since 2000, however, the volatility of profitability has exceeded even the Great Depression and WWII eras. (See Figure 2)

5. Prior EVAs have noted that many foreign markets are trading much less expensively than the US. One of those is right across our northern border; the current PEG ratio (price/earnings to growth rate) for stocks listed on the Toronto exchange is just 0.87 compared to 1.42X for the S&P 500.

6. “Europhoria” continues to be the prevailing attitude toward the once left-for-dead continent. Yet, France has just admitted that its budget deficit is surpassing the previously raised ceiling of 4.1% of GDP. French unemployment also recently hit a new high. Perhaps this is why an extreme right-wing party is gaining considerable influence on France’s political scene (as is the case in several other key European countries).

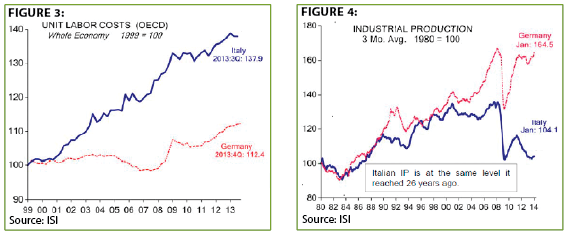

7. Bond yields have plunged throughout Europe, even in the most heavily indebted countries like Italy. This is clearly positive news but, as in France, fundamental problems remain largely unresolved. Italy’s labor cost disadvantage versus Germany’s continues to be gaping, likely a prime reason why its industrial production has massively lagged relative to its northern neighbor since the euro was introduced in 2000. (See Figures 3 and 4)

8. In a world on a starvation diet when it comes to yield, Chinese government bonds denominated in their currency are a rare haven of decent return. Their 10-year sovereign debt yields 4.5%, far above the US and even, incredibly, Italy and Spain (where yields are around 3%). Moreover, after the recent weakness in China’s currency, the renminbi, there may also be appreciation potential, at least against countries that are printing money or running huge budget deficits.

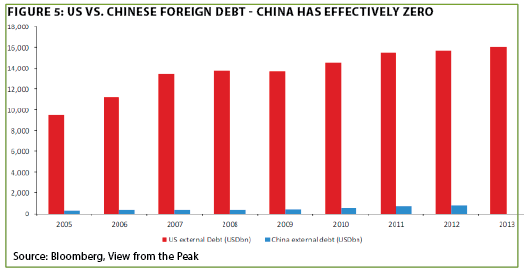

9. We are among those who believe China is in a controlled credit crisis. However, it is crucial to realize its debt is essentially all owed internally. (See Figure 5)

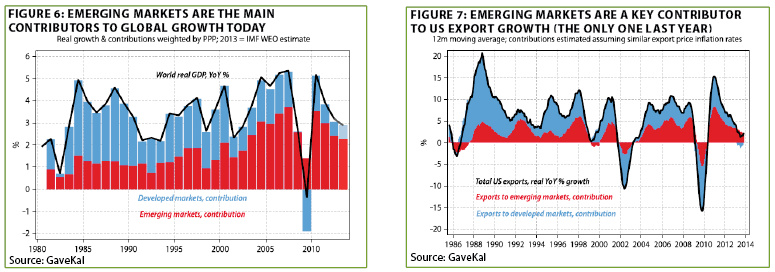

10. Investors have largely given up on emerging markets, but the global economy will have a harder time moving on. Developing countries have been generating an increasing share of the planet’s economic growth over the last decade. Even for the US, export expansion is highly reliant on these countries. (See Figures 6 and 7 below)

THE EVERGREEN EXCHANGE

By David Hay, Jeff Eulberg, and Tyler Hay

The Chart Heard ‘Round the World? Liz Ann Sonders is one of those abundantly blessed human beings. In addition to being Charles Schwab and Co.’s Chief Investment Strategist, she carries a AAA rating: attractive, astute and articulate. She’s also had, to the best of my recollection, a commendable record in anticipating both good and bad times, unlike so many of her competitors at the traditional Wall Street firms (Schwab continues to march to its own client-first drummer out on the “Left Coast”).

Lately, she has garnered a bit more attention than even her AAA status typically attracts by telling the financial news service Business Insider about what she thinks is the “most important chart in the world.” Because I’ve followed Liz Ann for a number of years and, consequently, am aware that she’s not given to hyperbole, this definitely caught my eye. In case you missed it, here’s the chart in question (See Figure 8):

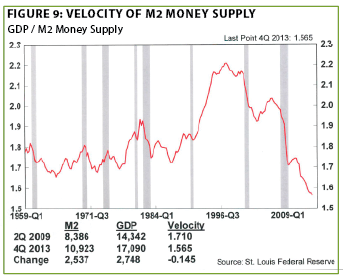

Consistent EVA readers realize that the velocity of money issue, per Liz Ann’s quote above the preceding chart is, in fact, right up there with what we believe to be one of the most vital issues for the financial markets. As a quick refresher, “money velocity” measures the speed with which money circulates within the economy. A reading on that essential statistic from a few months ago is shown below. (See Figure 9)

Again, at the risk of repeating a point we’ve made in multiple EVAs, money velocity in recent years has plunged at a rate unseen in the postwar era (roughly equivalent to Justin Beiber’s popularity dive since he was arrested the last time—or is that the last ten times?). This is the primary reason the Fed’s magical creation of over $3 trillion of bogus bucks has failed to kick-start a normal expansion or to maintain inflation at its desired 2% level (much less causing consumer prices to soar as so many have feared).

In the December 20, 2013 EVA, we elaborated on this issue, citing the unique analysis of our partner Charles Gave, who has postulated that there are now two types of velocity: economic and financial. As economic velocity has cratered in the wonderful world of repetitive QEs, financial velocity has behaved in a polar opposite fashion—pretty much going parabolic. This bifurcation of money velocity has been not so hot for Main Street but fantastic for Wall Street.

Accordingly, if economic velocity is about to change, Liz Ann may indeed be spot-on that this is an exceptionally important development. We could be on the cusp of the real economy finally attaining 3% type after-inflation (i.e., “real”) growth, a pace we used to take for granted but which has lately become as scarce as seeing Tiger Woods’ name on the Sunday leader board of a major golf championship.

The bullish spin on such a development is that what’s good for the economy is good for the stock market. Generally, that’s a reasonable assumption, but in this topsy-turvy world of trillions of the Fed’s funny-money, it may be a dangerous one.

Normally, the $3.3 trillion the Fed has whipped up would be multiplied about 10:1 by the banking system, meaning it would equate to about $33 trillion of loan demand, capital investments, real estate purchases, and other economically stimulating activities. Once such an enormous sum, roughly two times annual GDP, was energized, it would assuredly cause both the economy and inflation to overheat to a degree unseen in our country’s history. Therefore, the Fed would have no choice but to tighten like a crew frantically cranking the valves on a sub whose hull was just hit by a depth-charge.

A point I made at our Annual Outlook event is that one of the worst stock market events of all time happened in the fourth quarter of 1987, when the US economy was expanding at the full-blown boom clip of 6.8% (again, real). Oh, yes, and the Fed was tightening aggressively in the months leading up to that fateful day in October of ‘87.

We aren’t ready to concede that the preconditions for a change in velocity are at hand. But we are definitely on high alert and we think you should be as well.

Out is the new in. As embarrassing as it is to admit, on most Friday nights I can be found with my family watching one of my favorite programs, Shark Tank, on ABC. My affinity for this program likely shocks no one who knows me well. Conversely, most who know my wife would probably find it quite interesting that she too enjoys the program. For those with more to do on a Friday night than watch a reality TV program, Shark Tank is a very simple concept. The show is based around four successful entrepreneurs being pitched by real life business owners attempting to raise capital to grow their respective companies. The “Sharks,” as the four entrepreneurs are affectionately referred to, are then presented with the opportunity to buy equity in the firms, lend capital, and even secure royalties. If the Sharks are not interested in investing their own money, they will then use the catch phrase “I’m out” to decline the opportunity. The interested parties proceed to negotiate the deal right there for the world to see.

When I get the chance to watch the program with others, I’m always amazed at how rational everyone reacts to the dealings. Revenue growth is required, large margins are a must, a vast moat around the business model is a pre-requisite, and there better be earnings! When opportunities are presented on Shark Tank, conservatism is always respected. Yet, when many of these same people consider investing their actual money in hot new initial public offerings (IPOs), fundamentals are often ignored. As anyone in our business knows, we are constantly being asked about the latest, chic IPO. For me, these are my Shark Tank moments. Unfortunately, I often find that my audience is not very entertained or inspired by my answers.

Most of the recent IPOs appear eerily similar to many of the newly-listed companies of the late 1990s and early 2000s. In fact, according to a recent Merrill Lynch report, “Valuations of today’s IPOs are higher than the tech bubble with a greater percentage of unprofitable companies coming to market.” These firms have little revenue, lots of debt, and often no earnings to speak of. When you purchase these shares at astronomical valuations, you need to be very confident that earnings will eventually grow to justify the price. That can prove quite difficult, though, as IPOs typically gain momentum on expectations—not fundamentals. In 2000, web page visits were the driving force behind many new IPOs receiving lofty valuations. The story at the time was that eyeballs on webpages were all that mattered; revenues and earnings would follow as companies found ways to monetize users. Today, if you look at some of the messaging services, online streaming companies, review sites, or even the new social media firms that have had successful IPOs, this same story is being re-told and re-bought (unfortunately, in our view).

It’s certainly true that some venture capitalists have been adept at finding young companies and helping them realize their full potential. But what many retail investors fail to see are the myriad strikeouts that precede the highly publicized home runs. At Evergreen, we don’t believe it’s wise to invest our clients’ funds at such high multiples with so much of the future unknown. We don’t feel that we have the ability to decipher if the next trendy IPO might be the new Google, or the latest version of the disastrous Pets.com.

That being said, we do dip our toe into the IPO market periodically. Over the last few years, for example, we’ve participated in several offerings of newly-listed public energy partnerships (commonly known as MLPs). These companies tend to have the opposite fundamental structure of the firms mentioned above. In fact, we recently bought a new-issue MLP because it offered an attractive 6% yield, a realistic 10% distribution growth rate, low leverage, and ownership of assets in promising growth areas.* This security experienced a nice move on the first day of trading, but that was not the sole reason we wanted to participate in the IPO. This firm will never be the next Facebook, but compared with the average IPO these days we believe it can provide a solid return with much less downside for our clients over the long run, particularly once the current appetite for risky “investments” subsides.

Due to the multitude of recent IPOs, we’ve had a lot of practice pretending to be sharks. Many of these companies, like the ones of the late ‘90s, have high hopes built on a new platform which may very well become transformative. Some will inevitably be successful. Others will run out of borrowed money and time. For our clients, we will continue to search out any opportunity that will present good long-term returns and/or steady cash flow to shareholders. Companies that have poor fundamentals, but lots of hope and excitement, will always leave us saying, “We’re out.”

*Due to the fact that such offerings typically have limited availability, we are required to perform a lottery to see which clients receive shares in these IPOs. Consequently, only a minority of Evergreen clients were involved in this transaction; however, over the past two years many of our accounts have participated in new issue MLP underwritings.

Why you shouldn’t play portfolio roulette. On a recent trip to Hong Kong to visit my friend and business partner, Louis Gave, he told me a story about gambling at a casino in Macau, which I think relates perfectly to investors. While playing roulette with his co-workers, Louis watched the color red win eleven consecutive times. After seeing this, he decided to switch his bet to black. His co-workers were astonished and convinced this would be a mistake. He assured them after such a run black was due to come up. The group looked at him in amazement and said, “You’re crazy to bet on black, because tonight is red’s night.” I don’t know what was rolled next, which probably means another red, as I’m sure Louis would’ve included that detail in his story. But for the purpose of this missive, what was rolled next is irrelevant. This story is meant to illustrate the psychological divide between two very different mindsets which I believe spills over into how people invest.

A few weeks ago in EVA, we summarized Louis Gave’s three disciplines for investing. For those who may have skimmed or missed that edition, he says all investors use one of the three following investing methods: reversion to the mean (or value), momentum (or growth), and carry trades. Here’s a quick example of the three. Reversion-to-the-mean investors behave using the old adage, “This too shall pass.” Basically, that no matter how good or bad things get, conditions will normalize at some point, if you’re patient. Growth investors believe that momentum is a powerful force that should be ridden. This type of investor typically sees higher highs and lower lows than their value counterparts. The carry trade is a slightly more sophisticated and less prevalent strategy; typically performed by professional investors such as hedge funds, pension funds, and other institutional type investors. Being overly simplistic, carry trade investors borrow at a low rate and reinvest at a slightly higher rate. Generally, the margin between the borrowing rate and reinvestment rate is quite skinny and thus leverage is needed to amplify returns. As the saying goes, it’s like picking up pennies in front of a steamroller. This strategy is more esoteric and often used as a complimentary element to a portfolio, so I’ll omit this from the following commentary.

Growth investors don’t simply buy growth stocks, while value investors don’t simply buy value stocks. One great example of how there can be two faces of the same coin can be illustrated by looking at China. Seven years ago, if you didn’t have a direct way to play China you were considered to be behind the curve. At the time, many value managers were leery of its unsustainable growth trajectory. Meanwhile, growth managers felt that the enormous demographic forces and deregulation of markets deserved the high multiple. Today, it’s a much different story as the Chinese markets have languished and now trade at their cheapest valuation to US stocks in over a decade. Buying a specific type of asset class doesn’t make you a growth or value investor. In fact, it has nothing to do with the kinds of securities that differentiate the two-investor types; it’s timing that separates them. Growth investors will buy an investment on the way up and are not deterred, but rather emboldened, the higher it goes. Their top performing positions are their most beloved holdings, and their poorest performers are always on the chopping block. High valuations represent attractive growth rates not “irrational exuberance.” A growth investor can’t stand missing out on a rising market, and cash is seen as an irritating and useless drag on portfolio returns.

This is totally contrary to a value investor who is uncomfortable as the market ascends from its historical anchors. High valuations in markets are a warning sign, not a welcome sign. Struggling companies in the portfolio are often seen as bargains and tomorrow’s winners. Watching others fearlessly ride the wave of a bull market requires discipline and is rewarded when the inevitable bubble bursts. Keeping cash in their account is a reserve for buying into market panics and they are accustomed to negative reinforcement from the media (Jim Cramer). They spend more time being wrong than right as markets tend to rise for long periods and then correct severely but quickly. They value the avoidance of risk over the allure of quick returns.

Many investors like to think of themselves as growth or value, but the proof is in the pudding returns. I challenge you to go online, or into your files, and locate your financial statements from 2006-2007 (or 1999 if you can go back that far). How much were you buying versus selling? If you were a large buyer in 1999-2000 and 2006-2007 you are likely a momentum investor. On the other hand, what were you doing during the financial crisis? Were you moving to cash “until the dust settles,” or were you putting to work the cash you had a set aside for a (very) rainy day? If you found yourself excited at the number of great companies that traded so cheap because the baby was thrown out with the bathwater, you’re likely a value investor.

Determining what type of investor you’re pre-disposed to be is only part of the puzzle. Evergreen believes a client should take only as much risk as they need to meet their financial goals. If you have saved enough money to retire with ease, leave money to your heirs, or other beloved causes, by earning 4-6% annually, you don’t need to try to shoot the lights out—or speculate on the stock market’s version of a hot run at the roulette table. To achieve these goals, shouldn’t you construct a portfolio with moderate risk? Many investors violate this strikingly obvious notion and fixate on keeping up with the S&P 500, their neighbors’ returns, or some other irrelevant metric to their unique personal situation.

Believe it or not, reaching for higher return isn’t the most egregious sin. What is particularly dangerous are the firms (or investors) who reinvent themselves depending on what’s happening in the market. At an annual investing conference five years ago the CEO at one of our competitors was boasting about the sex appeal of alternative investments (hedge funds) had to affluent clients and how we were missing out. He asked if we were still doing the same old “vanilla” stock and bond strategy. Recently, he told his clients that alternative investments lacked the same risk/reward profile (see: haven’t performed well) and that he was migrating them back to more “reliable” (see: stock and bond) investment strategies.

What type of investor are you? It doesn’t matter. Either investor style can work over time. The key is “over time.” If you started as a growth investor in 2000-2001, it took what seemed like an eternity to be vindicated. As a value investor, the wait can be extremely painful as the markets continue to stay irrational beyond your wildest expectations. It’s extremely tempting to jump ship when your style goes out of favor and—trust me—it will. Show me an investor who has never felt lonely, and I’ll show you a terrible investor. Show me an investor who says their strategy makes money in any market environment, and I’ll show you the second coming of Bernie Madoff. No investment style has all gain and no pain. Investing is a skill; it’s not roulette. When was the last time you met a professional roulette player? If there are any, you can be assured their careers will be short-lived. There are, however, some tremendously talented investors with superb long-term returns. The one trait they have in common: They’ve stayed true to their style through thick and thin. Stay true to your style and your style will stay true to you.

![]()

IMPORTANT DISCLOSURES

This report is for informational purposes only and does not constitute a solicitation or an offer to buy or sell any securities mentioned herein. This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. All of the recommendations and assumptions included in this presentation are based upon current market conditions as of the date of this presentation and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. Information contained in this report has been obtained from sources believed to be reliable, Evergreen Capital Management LLC makes no representation as to its accuracy or completeness, except with respect to the Disclosure Section of the report. Any opinions expressed herein reflect our judgment as of the date of the materials and are subject to change without notice. The securities discussed in this report may not be suitable for all investors and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. Investors must make their own investment decisions based on their financial situations and investment objectives.