“It’s funny. All you have to do is say something nobody understands and they’ll do practically anything you want them to.”

- J.D. Salinger, The Catcher in the Rye

“The investor’s chief problem—and even his worst enemy—is likely to be himself.”

- Benjamin Graham, Warren Buffett’s mentor

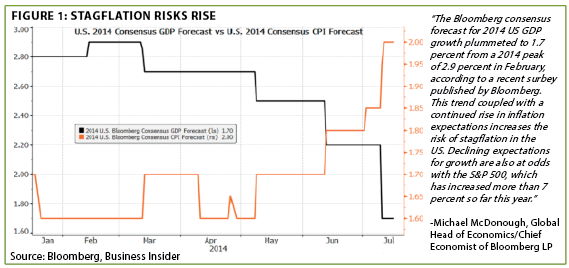

1. Reinforcing Evergreen’s escalating concerns about a “stagflation” scenario, GDP forecasts have been reduced while inflation projections have been raised. (See Figure 1)

2. Stanley Druckenmiller is one of the world’s most noted financiers. He was George Soros’ right-hand man during the latter’s glory years when his multi-billion dollar fortune was amassed. Mr. Druckenmiller was recently interviewed at CNBC’s Delivering Alpha conference, where he made the intriguing point that although economic activity is running slightly above average (technically, the 40th percentile), Fed policy is essentially the easiest it has ever been. (For more on Mr. Druckenmiller’s insights, see Jeff’s section on Page 6.)

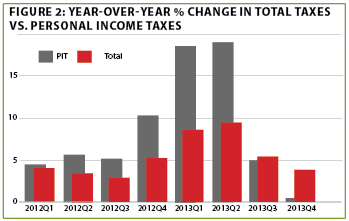

3. Despite the shockingly weak first quarter (-2.1% after this week’s upward revision), this author believes recent US economic data is generally perkier. In fact, employment, industrial production, and retail sales data for Q1 seem likely to lead to further positive revisions to the official GDP number. However, one important factoid—state tax collections—is at odds with an accelerating economy. (See Figure 2)

4. Echoing Mr. Druckenmiller, Dallas Federal Reserve Bank president Richard Fisher wrote a persuasive op-ed for the Wall Street Journal on July 28th (click here to read) arguing the Fed has stayed “too loose, too long.” He is also seeing evidence of rising wages and inflation that may cause the Fed to play tightening catch-up, a response that has “almost always resulted in recession, the last thing we need,” in Mr. Fisher’s words.

5. Stock market complacency and risk-acceptance have been extensively discussed in the financial media. Less well-known, though, is the same devil-may-care attitude in the bond world. Spreads (i.e., the difference between corporate and US treasury bond yields) are now within a whisker of their 2007 credit-bubble lows.

6. Some central banks are not satisfied with merely printing money and are resorting to using these fabricated funds to directly buy common stocks. Globally, $1 trillion has been invested into equities by government banks. In some cases, like China, accumulated foreign exchange reserves are being used to fund the purchases. It will be interesting to see if the Fed resists the urge to do this the next time the US market experiences severe selling pressure.

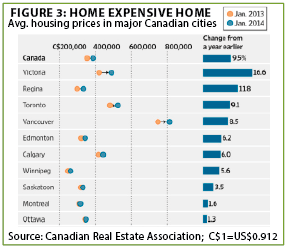

7. For years, bears on Canada have alleged that there is a US-style housing bust looming just over the horizon. Yet, outside of Toronto and Vancouver, prices don’t seem excessive. Undoubtedly, in the case of Vancouver, a massive influx of Chinese money has driven home values to an exorbitant level. (See Figure 3)

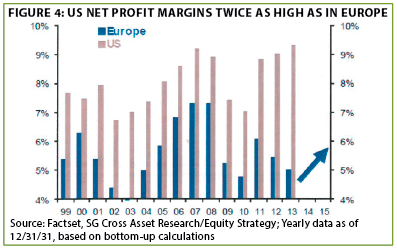

8. US companies have consistently been more profitable than their eurozone counterparts. In recent years, though, the gap has become enormous. (See Figure 4)

9. “The Brazilian Economic Miracle” has morphed into the “Brazilian Economic Debacle.” Yet, Brazil’s manifold challenges may not be worse than what southern Europe continues to face. Accordingly, buying 10-year Brazilian government debt in its currency at yields of 11.8% is likely to be a far better long-term investment than buying Portugal’s 10-year sovereign debt at a mere 3.6%. In fact, most of Europe’s bond markets look like a short-seller’s dream these days.

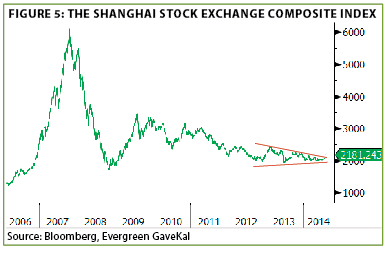

10. While the US stock market has nearly tripled from its 2009 low, the Shanghai Composite is minimally above where it was trading during that apocalyptic time. Predictably, Chinese equity funds were seeing record-breaking outflows earlier this year when prices were at their weakest point. Lately, though, China’s main market appears to be in the process of a significant upside reversal. (See Figure 5)

THE EVERGREEN EXCHANGE

By David Hay, Tyler Hay, and Jeff Eulberg

Torts “R” US. America is a great country! We’ve all heard that expression countless times, and many of us have likely said it ourselves. But what makes America great?

There are, of course, almost countless answers to that question. Yet, I would submit a most unlikely response: Failure. Specifically, I believe that one of America’s most enduring advantages is its societal tolerance—even embrace—of failure.

The “lovable loser” is well-ensconced in the national psyche. Americans simply love it when the underdog, the perennial also-ran, overcomes serial disasters and comes out on top. But it’s more than just an attractive narrative structure. In many ways, “failure tolerance” is what has enabled our country’s unmatched tradition of innovation. The great inventor, Thomas Edison, failed nearly 2,000 times trying to make the cotton-thread filament for the incandescent light bulb. When a reporter asked him about it he said, “I didn’t fail. I found 2,000 ways not to make a light bulb.” This is the type of enduring spirit and triumph against-all-odds that America was built upon. And, most who have started small businesses, and have seen them through to break-through status, have also endured the same painstaking disappointment Mr. Edison faced time after time.

America’s venture capital industry, which is literally without a global peer, is the ultimate example of this dynamic. “VCs” (not to be confused with our arch military enemy from the late 1960s) accept the fact that most of the companies they invest in will indeed fail. Undaunted by this reality, VCs have helped catalyze the most breathtaking series of inventions and new business births ever seen in human history.

What is particularly ironic about our cultural fondness for failure is America’s equally powerful affinity for, and almost addiction to, litigation. Suing as a national past-time is, if you think about it, directly at odds with our carefree attitude toward failure. Perhaps we were seduced by the tech mania, incurring heavy losses when it blew up, or became overleveraged during the real estate boom, possibly losing even more due to the debt involved. For red-blooded Americans, it seems the gut reaction is to want to pull out the “sue card” when reality bites us in our collective derrieres. Clearly, as a country, our embrace of losers has its limits, at least when it comes to our personal capital.

Some veteran EVA readers may recall that back in 2007, I predicted a wave of litigation would result from the excesses in real estate lending at the time. Well, it’s time to dust off that forecast and apply it to the next tort attorney welfare program: the investment industry.

Actually, securities firms have long been the legal profession’s version of a slow-moving gold train with attorneys playing the role of Mexican bandidos. Brokers have been sued repeatedly ever since the crash of 1987, but I think this time could be worse. Further, I also believe it could involve the investment advisory firms, which typically have largely been immune from the tortures of the tort process.

My reasoning is based on the fact that my team and I have recently reviewed a number of portfolios for clients in their 60s and 70s who have 70-80% of their assets in stocks. One of our local competitors is intentionally raising the stock exposure of “mature” investors to around this level, well above their stock allocation five years ago when prices were depressed. Their reasoning is that risks have been greatly reduced since then.

Excuse-moi, but I have this quaint notion that the higher stock prices rise, the riskier they become. It also seems to me that there are a number of disturbing trends occurring around the world these days—not to mention an overreliance on central bank printing presses to keep them all at bay. Similarly, I’m definitely among those who believe risks are highest when they appear lowest, and vice versa.

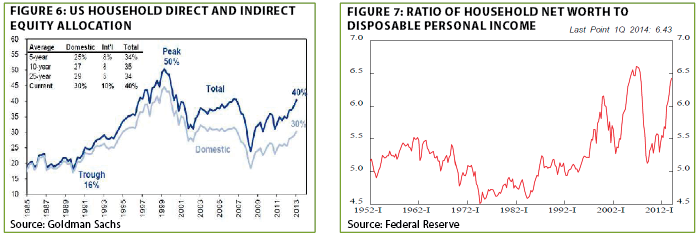

The following charts depict the elevated exposure Americans now have to more volatile assets (note that the reason these lines have moved up and down as much as they have in the past is because of extreme stock and/or real estate value fluctuations).

Several research services have cited the right-hand chart above as a bullish factor. Once again, maybe it’s just my weird way of looking at the world, but I beg to differ. To me, it looks like asset values are back up on a stilt, similar to their precarious perches in 2000 and 2007.

As the estimable Ned Davis personally wrote in a July 23rd essay to institutional clients: “Finally, if there is ‘no excessive optimism’, why is the S&P 500 Price-to-Sales ratio at the second highest level ever, after the ‘Bubble of 2000’ peak? Most likely due to Fed policy and the lack of alternatives, the public is clearly ‘in’ the market, heavily invested.” (I should point out the Ned Davis Research remains bullish on stocks, as is almost everyone—except, of course, yours truly and the Evergreen Investment Team.)

One of the huge risks of having excessive stock exposure for retired clients, who typically need cash flow to live on, is that when values plunge and the withdrawals continue, investors may find themselves in a hole from which they can never recover. Take portfolio values down 30%, along with a few years of 4% withdrawals, and it becomes very challenging to ever get back to your pre-plunge position.

Presently, there is precious little thought being given to downside, perhaps because most advisors agree with our competitor that risks are much reduced from several years ago. But if financial market history tells us anything, it’s that risk never really goes away—it just calmly waits to ambush on the complacent and unprepared.

Yes, it is lonely being a contrarian currently, just as it was back in 2000 and 2007. But I’d rather be lonely than be in the legal profession’s crosshairs when America’s next hissy fit over losing money manifests itself again. As we’ve repeatedly seen, when it comes to investing, failure is not an option—at least not one a multitude of US investors are willing to tolerate. Caveat advisor!

![]()

Luck and skill. With the NFL season just around the corner, teams have started training camp and fan enthusiasm is ramping up. But excitement among NFL fans isn’t limited exclusively to their favorite team’s prospects. Many football lovers take their passion a step further and participate in “fantasy football.” Some estimates have pegged there to be upwards of thirty million participants. This shouldn’t be all that surprising. NFL football is the alpha male of American sports. A recent survey showed that for 46% of America, their favorite sport is football. Baseball, long considered America’s “pastime”, was a distant second at 14%. The rabid following of the NFL clearly indicates that the torch has been passed and football truly is America’s game.

For those not familiar with fantasy football, here’s a quick introduction. A group of 10-12 participants, known as “owners”, engage in a 15-round draft process. Each owner selects players from different positions and teams around the league to build a roster. The goal is to select a team of players who are likely to perform best over the course of the season. Player performance is computed by compiling each player’s weekly statistics. Players who account for the largest proportion of their team’s statistics are those most valuable.

In the most basic sense, the goal of fantasy football can be stated like this: With finite resources, individuals sift through mountains of conflicting information attempting to forecast the future and determine whether or not the future prospects are bright or bleak. This sounds eerily similar to the world of finance, and there are some cogent parallels that exist between being in a fantasy football league and portfolio management.

1. Be Wary of “Expert” Advice: Every August, just before the start of a new football season, magazines flood airport shops, convenience stores, grocery chains, etc. For fantasy participants, these magazines provide a sneak preview of how the upcoming season could unfold. Look around and you’ll notice that it’s happening everywhere. On the airplane, you’ll see grown men (and women) “cramming” as they prep for their league’s draft. In coffee shops, they study the research published by revered institutions such as ESPN, CNNSI, YAHOO! SPORTS or, my personal favorite, ROTOWIRE. Buyer beware, though—these so-called experts have had some pretty serious whiffs.

Last year, an “expert” from ESPN projected San Diego Chargers quarterback Philip Rivers would finish the nineteenth most productive quarterback in the NFL. The real outcome? Rivers finished as the sixth best fantasy player at his position. The same pundit ranked Ray Rice (a running back for the Baltimore Ravens) as the second best overall player. He didn’t even finish in the top seventy-five. Often times players (or, in the case of investing, stocks) that are perceived to be unexciting, get overlooked. Pundits love to tell a story that’s sexy, often blinding the less thrilling truth that’s staring them right in the face. This lesson is evident in the world of investing, too. Telling investors to buy GE because it offers a reliable, albeit slower, growth rate isn’t exciting.

The lesson here: These expert analysts are paid to entertain as much as they are to inform. The old saying, “Those who can’t do, teach,” applies to investing. Successful money managers earn a lot more money than most market analysts. It kind of makes you wonder why those commentators aren’t managing money if they know so much, right? The reality is they are far from perfect. A recent study from 2013 showed that half of analysts missed their forecasts. While I’m not telling you to ignore them, I do think the Jim Cramers of the world are overly revered. Here’s one clip (click here) from youtube where one disgruntled viewer highlights a few of his recent blunbers.

2. Leverage your local knowledge: Frequently, fantasy owners know more about their favorite team and its closest rivals than the “experts.” Local fans that follow their favorite athletes on social media typically pick up news stories before any national reporters. Similarly, investors, either from their occupations or simply as consumers, often have deeper and more unique knowledge of certain industries or companies than do many New York-domiciled pundits. Often, people with industry knowledge, or even just plain common sense, underestimate their own knowledge or insight.

This can also be looked at in reverse. Buying into areas of the market where you have limited knowledge can be risky. When your favorite player on your favorite team has a bad game, you can put it into perspective. You’ve seen enough of their track record to convince yourself he will bounce back. The less you know about a player (or company) the less likely you are to keep the faith in times of struggle.

The lesson here: If you have familiarity with a company or industry, trust your experience. Just because experts make eloquent, persuasive, or loud arguments doesn’t make them right. Legendary fund manager Peter Lynch argued that astute end-consumers are often the best resource for identifying good investment opportunities.

3. Sell on Potential, Buy on Results: Almost every fantasy owner is enchanted by the idea of pulling off some incredible trade. Ideally, you give up as little as possible and in return you get a treasure trove of talented players, as well as bragging rights as the

shrewdest of negotiators. Investors can relate to this as well. The media is full of advertisements promising eye-popping returns with very little risk. It seems almost impossible that anyone could fall for such a proposition, but it happens in fantasy leagues and investment marketplaces all too frequently. While everyone knows that the idea to buy low and sell high is at the heart of any investment decision, some are able to do this easier than others.

The lesson here: Once in a while, flash-in-the pan players (stocks) become superstars, but usually they crash and burn. For every Amazon or Microsoft there’s a hundred Infospaces, Kozmo.coms, or Fiskers. Simply, good investors or fantasy owners use momentum to their advantage by selling into it. If you can swap the Wall Street darlings, and their astronomical valuations, for companies with proven track records and much less demanding prices, you’ll likely lower portfolio risk while adding return. This is particularly true in markets like the one we’ve been in for the last two years where speculation has been all the rage and prudence has been a handicap.

Certainly, fantasy football and investing don’t have a ton in common at first blush. However, there are similarities as both rely on making decisions based around uncertain future performance. The three points I discussed above are by no means the silver bullet to outperforming the markets. But hopefully this has been a fun, albeit unexpected, way to analyze some decision-making principles related to stocks. Without a doubt, investing and fantasy football require both luck and skill. Teams poised for greatness can be decimated with a single injury or ill-advised trade. Similarly, portfolios can be completely wiped out in the blink of an eye with just a few bad decisions. So before you spend time putting together your fantasy team’s draft strategy, make sure your portfolio is poised for a winning season. Because when it comes to investing, there’s no such thing as a do-over.

Time to call the Feds bluff. As a member of the Evergreen Investment Committee—and to uphold my fiduciary responsibility to our clients—much of my free time is spent perusing opinions and analysis from valuable sources. This research helps me to better understand complex ideologies, strengthen my conviction, and/or challenge prevailing thinking. At Evergreen, we’re very fortunate to have our partners at Gavekal—one of the top macro-economic research firms in the world—at our disposal. When looking for outside research, the key element we covet is a track record of success. We pay close attention to those who’ve repeatedly made the right call in different market environments.

When it comes to successful investment track records, Stanley Druckenmiller can put his up against almost anyone in Wall Street history. He worked with George Soros as the lead investment manager of the Soros fund for over a decade. In fact, he played a big part in “breaking the Pound” in the early 1990s. By essentially trading against the UK Central Bank, Druckenmiller earned a reported $1 billion. In 1981, he started his own hedge fund, Duquesne Capital LLC., only to close it in 2010 and return nearly $10 billion to his investors. From an industry perspective, closing a fund after returning over 30% annually to investors, is virtually unprecedented. As you can imagine, when he speaks, people listen.

Recently, at the Delivering Alpha conference, Druckenmiller gave a very clear warning (click here to watch). Over his 30-year career, he’s never seen a more puzzling monetary policy than what we’re witnessing today. Elaborating further, he says that today’s Fed policies are more baffling than what he saw in 2003 to 2004, which eventually led to the housing crisis. As EVA readers know, we are also quite perplexed by the market’s faith in current monetary policy. While Druckenmiller admits to making mistakes over his career, he also says he’s earned his largest returns when betting against unsound Fed policy.

In an interview at the same conference, Druckenmiller admitted he doesn’t see a systemic financial market risk. He thinks the current situation is different than what we saw in 2008. And although he isn’t sure how this poor policy will manifest itself, or even if it will end badly, he is convinced of one thing: “The Fed is making a bad bet.”

In the introduction to his presentation, Druckenmiller recalls a lesson he shared with his Duquesne team in 2004. At the time, he asked his partners to review a series of economic charts, pretend they were on Mars for five years, and then guess the current Fed funds rate. All of his partners guessed much higher than the current 1% level. This simple exercise reinforced his belief that the Fed was making a terrible mistake.

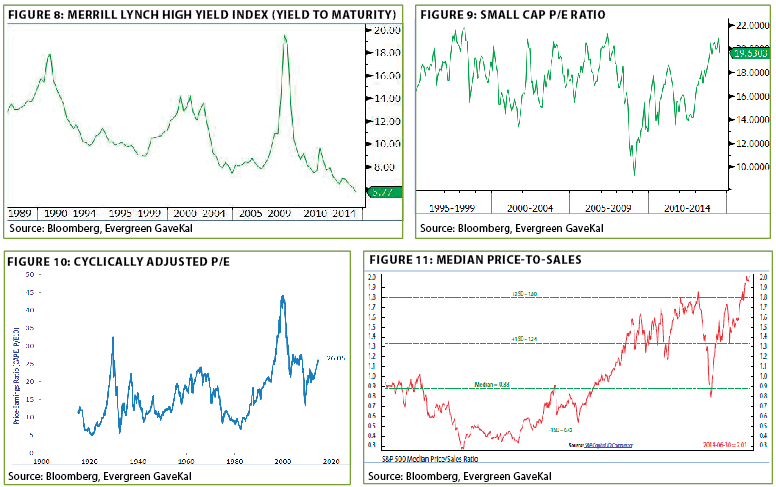

To discover where current Fed policies may be inflating investor enthusiasm, let’s recreate Druckenmiller’s exercise. Close your eyes and imagine you’ve spent the last five years in outer space, and are returning to earth to collect a large inheritance. Now, examining the four charts below, how excited are you to invest your newfound wealth in junk bonds, small-cap stocks, or even the S&P 500?

When purchasing “high yield” bonds, you’ll be earning the lowest yields in the last 30 years. For small-cap stocks, you’ll be paying one of the highest dollars per share amount, per dollar earned, over the past 20 years. For the S&P 500, you’ll be paying the 4th highest dollar per share amount, per average dollar earned over the last 10 years, since 1870. Also related to the S&P, you’ll be buying when the median stock trades at the highest price-to-sales ratio in history.

In 2006, Druckenmiller admits he was too early to defensively position his hedge fund. That being said, any successful investor knows it’s better to be early than late. To that point, although he was a couple of years earlier, in the disastrous market year of 2008, he reportedly made $260 million from managing his hedge fund and far more for his clients. Much like Druckenmiller stuck to his guns in 2006, our team at Evergreen firmly believes our early defensive stance will pay off when the Fed’s latest bad bet is called.

Important Disclosures

This report is for informational purposes only and does not constitute a solicitation or an offer to buy or sell any securities mentioned herein. This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. All of the recommendations and assumptions included in this presentation are based upon current market conditions as of the date of this presentation and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. Information contained in this report has been obtained from sources believed to be reliable, Evergreen Capital Management LLC makes no representation as to its accuracy or completeness, except with respect to the Disclosure Section of the report. Any opinions expressed herein reflect our judgment as of the date of the materials and are subject to change without notice. The securities discussed in this report may not be suitable for all investors and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. Investors must make their own investment decisions based on their financial situations and investment objectives.