“Better three hours too soon than a minute too late.”

- William Shakespeare

POINTS TO PONDER

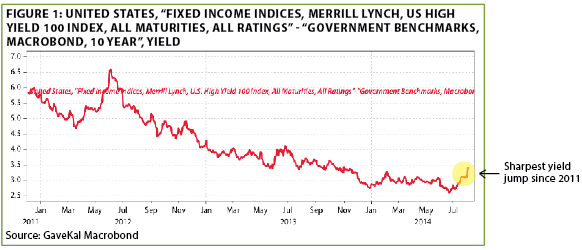

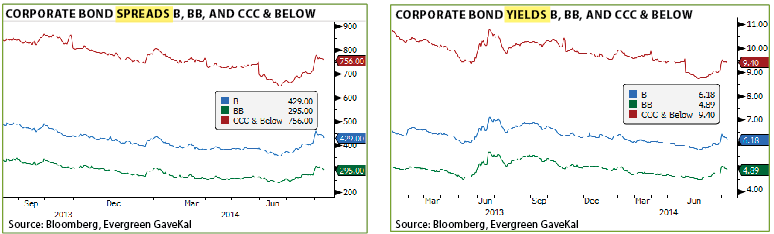

1. A recurring EVA subject of late has been the vulnerability of the lowest-rated bonds due to unrealistically puny yields, as a result of investors pushing the safety envelope in search of income. Beginning in late July, a vicious sell-off hit the junk bond sector with the worst-rated credits getting slammed the hardest. (See Figure 1)

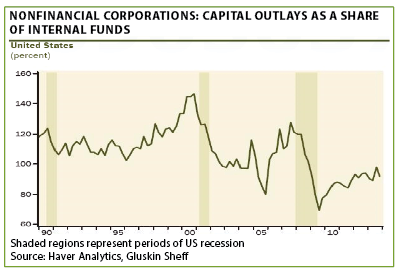

2. An overarching belief by Evergreen is that one reason the US economy will be more growth-challenged going forward is that the days of incurring vast amounts of debt to pull forward demand are ending. Immediately after WWII, an additional dollar of debt translated into over $4 of GDP improvement. Today, $1 of incremental debt produces just 9 cents of growth.

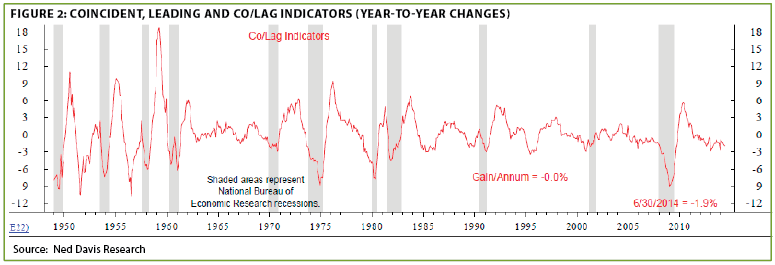

3. Venerated economist David Rosenberg has long maintained that the coincident-to-lagging indicators ratio has had one of the best recession-predictive track records. This metric fell into decisively negative territory last year and has, as yet, shown no sign of reviving. It should be noted, though, that the “Co-Lag” gave false negatives back in the mid-1980s and mid-1990s despite the fact it accurately warned of the 2001 and 2008 recessions. (See Figure 2)

4. Jim Stack, a talented money manager based in Whitefish, Montana, recently picked up on the flurry of media articles with “Boom” in the headlines. He observed that this has happened around market peaks in the past. However, he also noted these can proliferate as much as a year before the bust. Like so many professional investors, he remains bullish, though poised to shift gears.

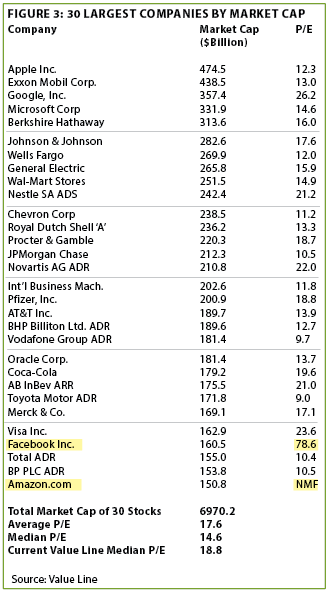

5. The divergence between extremely pricey mid- and small-cap stocks and the largest blue chip companies remains yawning despite this year’s notable lag by smaller company shares. The median P/E (which lessens the impact from the valuation-inflating influence of Amazon and Facebook) on the 30 largest market cap issues is just 14.6 versus a median P/E for the Value Line universe of nearly 19. (See Figure 3)

6. Cracks in the market for initial public offerings (IPOs) have given timely advance warnings of the last two market peaks. Over the last month, several of the most speculative IPOs have been pulled, perhaps indicating the mania for new issues is in its late stages.

7. Although Spanish unemployment remains appallingly high at 24.5%, it has fallen from 26.5% in the last year. Portugal has also seen its jobless rate come in from 17.5% to under 15%.

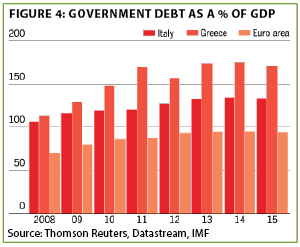

8. Evergreen has repeatedly dissented with the prevailing view that European Central Bank head Mario Draghi’s pledge to do whatever it takes to save the euro magically created recovery condition on the Continent. The fact that Italy is now back in recession (again!) is indicative of how distant enduring improvement is. Moreover, Italy’s sovereign debt burden is today essentially equivalent to where Greece was in 2009. (See Figure 4 on next page)

9. Economic news out of Japan continues mixed, notwithstanding the ambitious goals of its Prime Minister, Shinzo Abe, to revive his long economically moribund country. Although the Bank of Japan has been fabricating yen at a furious rate (equivalent to around $2 trillion of quantitative easing in the US), part-time workers now make up 38% of the work force. As Richard Katz of The Oriental Economist Alert has noted, this is a staggering level for a nation once famous for its lifetime employment and income equality.

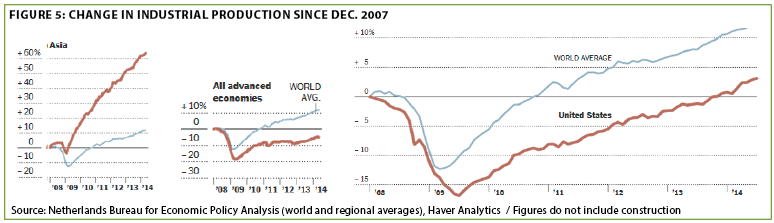

10. Asian stock markets have badly lagged US share prices for years. This is despite the fact that Asia’s industrial production has soared since the global financial crisis, in stark juxtaposition to the stagnation in the “advanced” economies. (See Figure 5)

THE EVERGREEN EXCHANGE

By Mark Nicoletti, Tyler Hay, and David Hay

Winemaking and portfolio construction: An unlikely blend. My family and I live about fifty miles northeast of San Francisco in an area widely considered one of the top wine-growing regions in the world, the Napa Valley. Napa is my wife’s hometown and, admittedly, she ‘coaxed’ me into living and raising our children here several years ago. At the risk of spending political capital with her that I desperately need, I love it.

The fact that wine—great wine—is produced here is, however, nothing special in and of itself. Many places produce wonderful wines. But Napa has also become a culinary mecca, and eating great food happens to be one of my favorite pastimes. Living in Napa has given me a passion for the best. Not just in food and wine, but in everything. And once you get a taste for the best, you can’t help but want more.

With another summer rapidly nearing its end, we’re approaching my favorite time of the year—Fall. Along with the change in climate that the season brings comes color change. Everywhere. I am at once surrounded by indigenous valley oaks, historic redwoods, olive trees, and mustard-colored vines, all framed by rolling hills that lead to mountains on either side of the valley. This may sound trivial, but I believe the beauty of the Napa Valley affects me both materially and spiritually: It is one of those glorious intangibles that makes life worth living—and one look at this view near my house (see photo on right) ought to be enough to convince any holdouts of my sincerity.

Now, in case you think you’ve been sucked into a Hallmark card, stay tuned; I’m cynical too, it’s coming.

From August through November, Napa visitors can observe grapes being harvested. Ripeness in viticulture, largely determined by climate and weather patterns that year, dictates the beginning and end of the harvest. The constituent parts of that ‘ripeness’ is, however, highly subjective and depends on the instincts of the viticulturist/winemaker. Because Mother Nature has a mind of her own, like all perishable farming, there’s an element of risk to grape growing. Waiting too long for grapes to ripen perfectly can result in crop damage or loss.

My daughter’s godfather is a renowned winemaker and has enlightened me over the years on his craft. He believes winemaking is 90% grape quality (although I doubt I could produce a 96 point wine, as he has, even with his grapes). He says some years farming a vineyard is simple; other years it’s difficult and requires meticulous attention to maximize the end crop. After some careful study, and late night consumption of his product, it dawned on me that what we do with our clients’ portfolios is remarkably similar.

Evergreen has tried to indoctrinate our clients with a simple, but strongly-held belief over the years: Portfolio returns are ~90% determined by asset allocation. Unlike the estimate above on the impact of farming on wine quality, this asset allocation metric is verifiably true. We manage client portfolios like a farmer manages a vineyard; we try to maximize outcomes. In a positive climate, you can plant your vines and let benign market conditions ensure your portfolio ripens and flourishes. In more troubled times, you have to painstakingly tend to your portfolio—trimming and pruning as required in order to successfully guide those precious vines into the harvest.

As mean-reversion investors, our firm (and firm’s) philosophy is to be prepared for what lies ahead and forge an unconventional path toward it. Loyal EVA readers know, because of experimental monetary policy and global economic concerns, we do not believe the current favorable climate will continue. We’re at a point where we need to be thinking about full cycles, not diagonal lines.

We’ve had five years of relentless quantitative easing and yield suppression on the part of central banks, and that, in turn, has led to a potentially dangerous reach for returns by investors. Our current asset allocation, which includes cash, is designed to dampen the effects of a market sell-off while still participating in market upside should the silliness continue.

This approach addresses perhaps my greatest frustration with the professional investor community: How routinely overlooked the supreme importance of entry points and the sequence of returns are. There is an article by Ph.D. Craig Israelsen entitled, When the Sequence of Returns Matter, that I find particularly poignant. The difference in potential performance outcomes from his example, based solely on the sequence of returns, is astounding (click here to read). As he notes, published performance data is based on several assumptions and discounts real-world portfolios, which commonly have additions, withdrawals, tax ramifications, and are highly susceptible to inflation. He freely admits that while it’s not possible to precisely craft the sequence of returns, it is possible to tilt a portfolio towards a certain risk level, something retirees absolutely need to be conscious of.

To take it a step further, Evergreen clients making additions to existing accounts, or those who are new relationships and are experiencing our on-boarding process, are treated starkly different than the industry norm.

In a recent prospect meeting, a gentleman contrasted our initial investment process to that of Goldman Sachs, BNY Mellon, and Merrill Lynch—all of whom he had recently interviewed. When discussing the $20 million in liquid assets that he was looking to allocate, all three firms had proposed being fully invested either at, or very near the outset of the relationship and all were averse to cash.

This was of some concern to him. He didn’t condemn their approach (and neither am I, at least not here) or their investment acumen or even their market outlook. He simply couldn’t come to grips with taking his family’s legacy money and investing it all quite so quickly, especially considering the aforementioned distorted market conditions.

As I explained, Evergreen rarely does this. One of the key tenets of active asset management, in our minds, is customizing on-boarding and additions. It’s more onerous from our standpoint, for sure. But we think it’s the right thing to do. Entry points are critical and our tactical implementation of cash is designed for long-term performance reasons, not to simply enhance client comfort levels.

Whether you believe in global warming or not, there is at least some evidence of shifting patterns in temperature volatility across the world over the last three decades. In the same way, whether you believe the Fed’s controversial money multiplication strategy has been effective or not, there is certainly evidence it has driven asset prices to elevated, if not dangerous, levels.

Because of these uncertainties, it seems inherently foolish to pick your grapes on October 15th every year like clockwork, or to rebalance your portfolio on some equally arbitrary date, or to invest large sums simply because they are available. Just as the winemaker spends time in the field testing sugar and acidity levels, and doing everything in his power to try and create the perfect conditions for his crop, money managers need to analyze credit and business cycles, monetary policy, geopolitical risk and company risk, among many other inputs.

Fall is a complex season, but it’s also time when those who pay painfully close attention to subtle shifts in climate and adapt accordingly can separate themselves from the rest, producing a harvest that endures over many years. The grape harvest is followed by the crush, something we don’t want our portfolios to suffer. As stewards of wealth for our clients, we’re more comfortable looking foolish sheltering our harvest well before the storm than exposing it to a brutal blizzard.

![]()

Don’t slip through the cracks. Financial planning, investment management, and wealth management might seem like interchangeable descriptions of financial services, but they are very different. These misconceptions are often perpetuated by a financial professional, or at the very least go un-clarified. Failure to understand the different role each service plays in meeting a client’s goals can leave a client vulnerable to an overreaching “advisor.” I will attempt to clearly define the differences, which will hopefully help readers make more informed decisions regarding their wealth managers.

Using building a house as an analogy, a financial planner acts as the architect in the process. Their job is to create a financial blueprint that reflects a client’s set of goals and objectives. They help answer questions such as: Am I saving enough for retirement? When should I start taking social security? Who’s a good estate-planning attorney? Many of these items occur early in the process of evaluating a client’s financial future. Thereafter, a financial planner will interact more periodically, revisiting the client’s financial situation when a major event, such as selling a business, occurs.

About ten years ago, we considered merging with a financial planning firm, who had wanted to expand their offering. The firm’s founder had expressed frustration that, as a planner, a client only required your services a few times in their life, but as an investment manager you have an ongoing relationship.

At that time, though, our firm was primarily focused on investment management. Sticking with the house analogy, if the financial planner is the architect, then the investment manager is the builder. Their job is to construct investment portfolios that execute the design of the financial plan. Beyond the construction, there is also ongoing upkeep required to prevent deterioration in the quality of the structure. Since investing is not a static exercise, investment managers must continually perform portfolio maintenance to ensure it remains structurally sound.

In the end, our merger didn’t end up happening. We did, however, decide to make significant investments in creating an in-house financial planning division. It was a prerequisite that our planning team attain the Certified Financial Planning designation (a rigorous course and series of tests are required to be accredited with“CFP” status). We were fortunate to also find an individual who had a legal background with emphasis on estate and tax planning. Adding this planning team to our firm’s pre-existing investment team allowed us to offer holistic financial guidance to our clients. It also reclassified us as a wealth manager. While it took significant financial and operational resources to develop this more integrated approach, it’s quickly becoming the standard of managing client wealth.

Now, finding a legitimate wealth manager is easy in theory but hard in practice—largely because many firms just arbitrarily call themselves wealth managers. Routinely, clients with obvious planning needs come to us from brokers or advisers who do not have a C.F.P. Frequently, they also have massive inefficiencies in the architecture of the financial picture, making for big future payments to ol’ Uncle Sam.

Conversely many “wealth managers” are just financial planners in camo. Clients who come to us from these types of firms have portfolios that have been statically “managed” for years with a staggering disregard of market conditions. An increasing number of advisors are convincing clients that a well-diversified portfolio can simply be left on autopilot. But we have a problem with that sentiment. It’s like saying that a well-built structure doesn’t require maintenance. Another trend is the increasing role of financial planners as middlemen. They refuse to personally make investment decisions, often citing conflict of interests. Instead, they charge their clients additional fees to select an outside firm who will make the investments. The convenient thing about this role is that these “advisors” can deflect blame to those making the investment decisions if things go south. Let’s take a step back and think about that. There are individuals who have built their whole career on the hiring and firing of other investment firms, but have never themselves been subject to a standard of performance. Sometimes I think we are in the wrong business.

It can be very hard to hire someone to manage something as critical as your family’s assets. The financial world is full of confusing jargon, quick talkers, and complex investment strategies with “nothing but upside.” Here are two questions that can put much of your uncertainty to rest: 1) Is your financial planning being done by someone who’s at least a C.F.P., and ideally has a legal background? 2) Is the person advising you on the investment of your assets telling you how they are measured, and how they’ve done with REAL money? This isn’t to say they have to be omniscient or infallible, but they should be accountable to you, the client. Don’t be afraid to ask these things of whoever you entrust to manage your wealth. Sure it could be awkward or uncomfortable, but should it be? Not performing proper due diligence puts your money and your future at risk—not the advisors. After all, when buying a house, don’t you ensure the inspection is devoid of cracks in the foundation? Why should investing your hard-earned money be any different?

Another piece falls into place? Among my lengthy collection of favorite sayings is this gem: “You are entitled to your own opinions—but not your own facts!” One application of this aphorism these days pertains to whether or not the stock market is in the middle innings of a long-term (aka, secular) bull market or if it’s in the penultimate inning when, appropriately enough, most teams go to their bull pens.

Evergreen was fortunate last week to host GaveKal Research’s brainy young expert on monetary and economy trends, Will Denyer. Will stayed at our home, giving me ample type to quiz him on some of my most nagging concerns. Much of our discussions took place as we cruised gorgeous Lake Washington in the kind of sublime summer weather only the coastal side of the Pacific Northwest can offer.

One of the topics I repeatedly broached with Will is toward the top of my worry list: The possibility that much of the “wealth creation” we’ve seen over the past 30 years was due to an unprecedented debt splurge—one that is impossible to recreate (barring massive and painful debt liquidation, that would set the stage for the next leveraging-up cycle).

Frankly, this is a topic that I don’t think either Evergreen or GaveKal Research have spent enough time analyzing, even though I’ve raised it a few times in prior EVAs. (It was particularly apt to ponder as we slowly motored by hundreds of multi-million dollar homes along the lake, including one listed for a cool $32 million.)

Knowing Will’s intellectual curiosity, he will reflect deeply on whether we’ve hit the debt wall in the weeks ahead, and produce a thorough and thoughtful reply. From his perspective, one of his most pressing questions was whether the US economy and stock market is in a 2004 or a 2007 phase.

If it is the former, this would mean that both the economy and stocks have several more years of good times ahead. If it’s 2007 déjà vu, then investors should be battening down the hatches as if they were on sail boats off the coast of Hawaii last week with twin hurricanes hurling toward them.

As I’ve repeatedly relayed, the co-founder of GaveKal Research, Anatole Kaletsky, firmly believes we are in a 2004 situation. Will, however, as indicated above, is simply in analytical mode, attempting to objectively weigh the data.

I’m sure it will come as a surprise to precisely zero EVA readers that I made the case for it being much more like 2007 than 2004. Whether it’s the hyperventilating condition of a wide range of asset classes—collector art, fine wine, rare books, luxury real estate, the riskiest stocks and bonds—or the similarly overheated action in new-issues and “M&A” (mergers and acquisitions), the message is the same. This type of activity occurs much later than halfway through the ball game.

Very recently, though, another piece of the puzzle of where we are in the market and economic cycles has fallen into place. This involves the exceedingly vital element of credit spreads. For those who are perplexed whenever they read this term in the financial media, or hear it bandied about on CNBC, it’s actually a most simple metric. It is merely the difference between the yield on US treasury bonds and non-government debt of the same maturity.

Up until the end of July, credit spreads were continuing to tighten as they have done persistently since March of 2009, with a few hiccups along the way. There is little doubt this tremendous spread compression has played a crucial role in levitating stock prices and many other risk-assets as well.

As I’ve conceded before, I really haven’t given the devil his due in this regard. While I’ve repeatedly carped that the Fed’s serial QEs have failed to achieve their main goal of lowering mortgage rates, I’ve failed to emphasize how successfully our central bank has crushed credit spreads. This process has been a prime catalyst in forcing investors to venture into areas they would normally avoid, like the gamiest stocks and bonds, in search of higher returns.

In my view, this is a key reason the real economy has failed to benefit nearly as much as the financial markets have from the Fed’s monetary incontinence. Charles Gave has referred to this dynamic as one of high “financial velocity” and low “economic velocity.” In other words, the trillions of “BernYellen” bucks have gone mostly into financial pursuits at the expense of investing in new factories, robots, workers, their salaries, computers, etc. (Obviously, there’s been some investing in productive assets, but the reality is—fact, not opinion—that this has been the weakest “cap ex” cycle in any post-war expansion.)

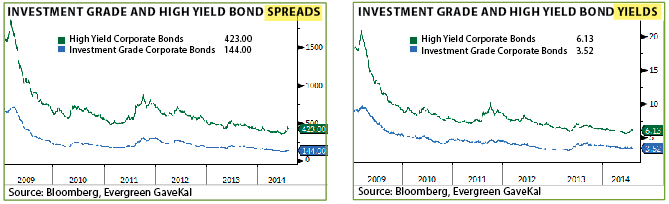

As alluded to in Point to Ponder #1, the end of July saw a sudden and radical shift in credit spreads, at least in the area where we’ve been issuing our most strident warnings: low-grade debt. In fact, it has even spilled over into that somewhat oxymoronic category we refer to as “high-grade junk” (BB-rated bonds). Per the chart below, you can see that higher quality junk did hold up appreciably better than the skuzziest stuff, but it was a spanking even for this safer tranche.

In the Evergreen view, widening junk spreads may well be the carbon monoxide alarm for this lengthy bull run in nearly every high-risk asset class. Almost all other preconditions of a major market adjustment had fallen into place earlier this year (click here to see the May 30th EVA for a top-of-the-market checklist)—save credit spreads.

Among the reasons why we believe spreads matter so much is the earlier statement (again, this is a fact, not an opinion) that debt levels in the US have risen to such Himalayan heights since 1980. Thus, higher interest rates bite very quickly. Additionally, escalating yields on securities like junk bonds pose competitive risks for one of the most generously valued US stock markets of all-time. Due to the extreme reliance on lofty asset prices to juice confidence and spending—i.e., the much vaunted “wealth effect”—any precipitous fall in stock prices has the potential to slam the economy.

The comforting consensus of Wall Street opinions remains aligned with Anatole that the bottom of the 9th for this thrilling game is a long way off. Yet, when I look at the facts, I believe the closer is warming up just beyond the outfield fence. With how overcrowded the great stadiums known as the financial markets are these days, investors should be less interested in the final out and more concerned about getting out.

![]()

Important Disclosures

This report is for informational purposes only and does not constitute a solicitation or an offer to buy or sell any securities mentioned herein. This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. All of the recommendations and assumptions included in this presentation are based upon current market conditions as of the date of this presentation and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. Information contained in this report has been obtained from sources believed to be reliable, Evergreen Capital Management LLC makes no representation as to its accuracy or completeness, except with respect to the Disclosure Section of the report. Any opinions expressed herein reflect our judgment as of the date of the materials and are subject to change without notice. The securities discussed in this report may not be suitable for all investors and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. Investors must make their own investment decisions based on their financial situations and investment objectives.