"The Fed is distorting markets and risking asset bubbles by keeping real rates negative when real growth rates are positive—the excess of this moves into financial assets, as opposed to the real economy."

- Noted economist, David Rosenberg

POINTS TO PONDER

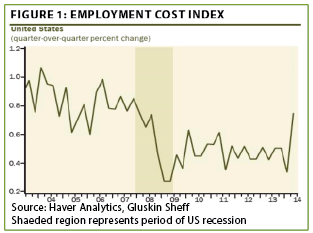

1. The recent surge by the Employment Cost Index (ECI) is elevating the odds the Fed will need to launch its own (and, hopefully, far more successful) version of "fast and furious" by raising interest rates. Given that the ECI is among Janet Yellen’s favorite inflation barometers, if it continues rising, she may have no choice but to move away from her dovish stance. Moreover, the latest Fed minutes reveal growing internal pressure to begin normalizing interest rates. (See Figure 1)

2. After a growth spurt from 1996 to 2004, the rate at which US productivity is increasing has fallen by half to just 1.3%. Since productivity combined with population expansion is what drives overall economic growth, this is a serious problem—particularly based on America’s declining fertility rate and aging demographics.

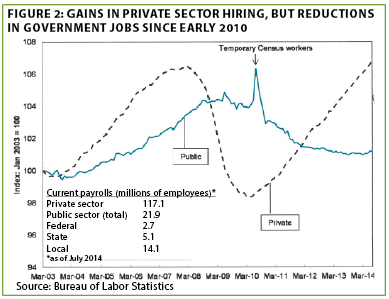

3. The US labor market is far from fully healed but the growth in private workers compared to the shrinkage in the public sector work force is a clear positive (the former being what generates economic activity while the latter is overhead). (See Figure 2)

4. Evergreen continues to believe that high-quality US growth companies (excluding Facebook and Amazon) offer reasonable value in a hyper-stimulated domestic stock market. Driving this point home, Barron’s recently quoted Leuthold Funds’ Chief Investment Officer, Doug Ramsey, who noted that large tech stocks are trading at the lowest price-to-earnings and price-to-cash flow ratios relative to the S&P 500 in 25 years.

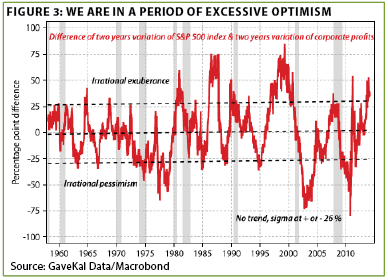

5. GaveKal Research’s Charles Gave, widely acknowledged as one of the world’s most insightful economists, has developed an interesting process for determining if stock values are too frothy. He compares the two-year rate of change in the S&P 500 market price against corporate profits. The current disparity on the overly optimistic side is at a level that has consistently preceded sharp declines (for those with a discerning eye, even in 2011). (See Figure 3)

6. Morningstar has attempted to quantify the cost of the typical mutual fund investor’s recurring tendency to buy late in bull markets and sell during times of stress. They estimate that on average investors sacrifice two and a half percent per year though this "wrong cycle" behavior. And while Exchange Traded Funds’ returns are harder to calculate, researchers at Vanguard have found that ETF investors were more than twice as likely to check their accounts daily, a trait that almost always leads to even worse buy and sell decisions.

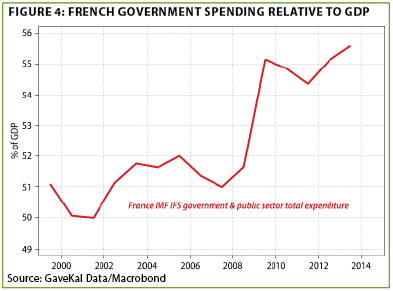

7. France’s debt load is alarming on its own, but when you consider how much of its economic activity is government-related, the implications are even more ominous. Just 43% of GDP is produced by the private sector, meaning that this shrinking share carries a massive and growing debt load. This impossible situation recalls Herb Stein’s famous quote that if something can’t continue, it won’t. (See Figure 4)

8. Underscoring how long Europe has been in an economic funk, eurozone companies have failed to match expectations for the past eight earnings seasons. With the Continent appearing to be entering its third recession in the last six years, this disappointing streak is likely to be sustained.

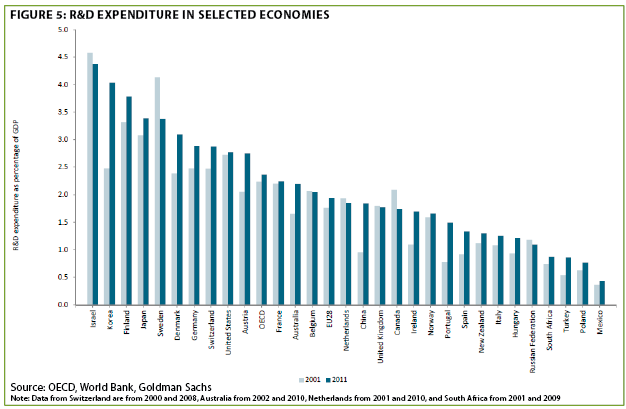

9. It would be logical to assume that high research and development (R&D) spending would equate to superior economic growth. Japan, though, has disproven that thesis, possibly due to the deleterious long-term effects of its seemingly perpetual zero interest rate policy (ZIRP). (See Figure 5)

10. While the US stock market has nearly tripled from its March 2009 panic low, the Shanghai Composite is minimally above its level at that time. (It is also down about two-thirds from when Evergreen warned investors of its dangerous overvaluation in November, 2007.) Lately, however, the Chinese stock market has been showing nascent signs of a turnaround. (See Figure 6)

THE EVERGREEN EXCHANGE

By Tyler Hay, David Hay, and Jeff Eulberg

An Uber-sized battle between new and old economies. Around 25 A.D. Pliny the Elder, one of Rome’s most notable writers, witnessed something reminiscent of the struggle currently underway in today’s modern economy. Under the rule of the emperor Tiberius, in front of an imperial court, a Roman glassmaker displayed a mind-blowing invention: unbreakable glass, or "vitrum flexile" in Latin. The glassmaker dropped an object, which everyone thought to be glass, but it did not shatter when it hit the ground—it merely dented. Astonished, Tiberius asked the glassmaker if he had told anyone of this secret. As soon as the glassmaker assured him that he alone possessed the genius to produce this material, Tiberius executed him. To the emperor, this unknown, new, and innovative material was a potentially disruptive threat to his imperial wealth.

History is littered with many more examples of clashes between the old and the new. Today, we are all witnessing this familiar battle as the Silicon startup Uber has begun to revolutionize, not only the traditional taxi business, but also commerce as a whole. Uber is software (or in other words, an app) installed on smartphones that allows willing individuals to work as ad hoc taxi drivers. Riders, using the same app, send out an alert from their phone and Uber uses GPS to dispatch the nearest driver for pick up. After the ride, no money is exchanged because the passenger’s credit card information is stored with Uber, who claims 20% of the fare and passes the rest along to the driver.

The growing popularity of this "rideshare" service is staggering. Young people everywhere are shunning taxis for the cheaper more convenient e-hailing of these on-demand drivers. While Uber has refused to reveal ridership numbers to the public, you don’t have to be too tech savvy to notice its popularity. Ask someone under fifty how he or she got home from the bar the last time they were "over-served," and they will say, "I Uber-ed home." Ask someone over fifty the same question, and they will say, "I had someone younger help me Uber home." Anytime a noun becomes a verb, as with Xerox and Google, you can be assured it has arrived (which is particularly appropriate given Uber’s line of business!).

Uber’s success comes from something more than its popularity among passengers. Those who’ve signed up to drive for Uber love it, too. Besides having a car, the hurdles to becoming a driver are quite low. You don’t even need a smart phone—you get one for free when you sign up to drive. After uploading some fairly straightforward information to Uber’s website (i.e., drivers license, proof of insurance, and consent for a background check) you’re ready to begin collecting fares. Uber drivers make a pretty decent living. It’s estimated that a driver working 40 hours a week in New York City can make $90,000 annually. In San Francisco, drivers make about $72,000 for a year’s work.

Is it me, or does this seems too good to be true? A Silicon Valley startup wrote an app that allows people to transport themselves around a city with less waiting and more convenience, and generally a much cheaper alternative to a taxi. Further, it created a job market for individuals who own a car that might have otherwise sat idle. Instead of sitting drenched in boredom while wives shop, husbands can shuttle a few passengers around town. It seems that this Uber app has created productivity out of thin air (something Janet Yellen and Ben Bernanke have been trying to do this since 2009).

But not everyone is enchanted with Uber’s rapid thrust into the limelight. Taxi drivers hate it. Many taxi drivers have to work hard to pay off the high cost of licenses that most municipalities charge to operate a taxi, undercutting years of hard work paying off these debts. While most cities haven’t been able to slow Uber’s adoption, it’s not for lack of trying.

In Paris, a taxi strike turned violent when an Uber driver and passenger were assaulted near Charles-de-Gaulle airport. In London, cab drivers went on strike to protest the company’s presence. That backfired as Uber driver registrations jumped 850%! The fight is far from over. Taxi drivers have turned to government lobbyists to enact laws that limit the company’s ability to operate. In the US, some Uber attacks have succeeded. Houston, Miami, and Portland have all banned the service. Internationally, Berlin, Brussels, and Seoul have said "no thanks." One report suggested that taxi companies had spent $3,500 for every Uber’s $1 in lobbying dollars!!!

Government officials have started to issue more regulations to "protect" consumers. In February, Seattle Mayor Ed Murray warned that he would shut down Uber if they didn’t require drivers to carry more insurance. Uber responded that their drivers already have more insurance coverage than traditional taxi drivers. (See Figure 7 on the previous page for more detail.)

Seattle based rap megastar Macklemore took to twitter, along with his 2.5 million followers, to issue his support. Other web-wise Uber users have created internet petitions to inform their government representative of their dissatisfaction. The tremendous following of Uber users is having a serious impact. One politician even expressed outrage as their e-mail inbox became clogged with messages demanding access to Uber. At least in America, it’s hard to fight the "exUberance" a truly great idea generates.

Calling Uber merely a ridesharing service is kind of like saying Amazon is just a website. It’s true, but it fails to define their real value proposition. Ridesharing helps you get from point A to point B. Uber didn’t just find a way to accurately price the act of hitchhiking. Uber is something far more interesting; it’s become like a stock exchange for services between people with time and those willing to pay for it. It should be called a need-matching company. People with idle time can lend their services to someone near them who desires their service. A market is being made and productivity is being created because people are able to more easily communicate their need and, in reverse, their services. What’s really exciting is when one begins to imagine the countless other applications for connecting consumers to service providers through a more intelligent exchange. Babysitters is a "G" rated example of a marketplace that’s long operated with low efficiency in terms of matching willing sitters with families. It’s been relegated to a word of mouth exercise with only a few reliable websites that offer far less efficiency than Uber’s. Some other, less than G-rated, applications have sprung up as well. It’s really no surprise that services across all spectrums have gravitated to this more efficient method of exchange.

A few months ago, I heard Newt Gingrich give a speech about the "pioneers of the future, and the prison guards of the past." While he is typically viewed as a partisan Republican, I found it interesting that he believed an ideological battle was brewing. Not one that would be fought between political parties, races, genders, or religion but between those who support progress and those who oppose it. Uber is an economic breakthrough that is good for the consumer and jobs. There is a tidal wave of support that is allowing it to break down the usual political barriers because when workers and consumers win, the prison guards become outnumbered. Uber’s ability to unite people through the creation of an innovative technology brings to the forefront what makes our economy the greatest in the world. In America, we still allow people to create at-will and to speak out. So despite a Federal Reserve in the middle of a policy experiment, a back-to-the-1930s hands-off approach to foreign policy, and a seemingly over-heated stock market, companies like Uber are reasons to believe that "Made in the U.S.A." will continue to represent that most important product known to humanity—innovation.

Does Anybody Really Know What Year It Is? In the August 15th EVA, I discussed a profound question asked by GaveKal’s brainy young monetary analyst, Will Denyer, when he was in Bellevue earlier this month. To wit: Are we seeing a repeat, or at least a rhyme, of 2004 or 2007? As I wrote two weeks ago, the investment implications of the answer are enormous.

Accordingly, I’ve been doing some serious pondering over Will’s musing, including exchanging a number of emails since then with him on this subject. Recently, a reasonable answer dawned on me: yes and yes.

Like most newsletter scribes, I’d like to take the credit for any blinding bolts of brilliance but, as is so often the case, I really need to extend the accolades to Charles Gave. In an EVA earlier this year, I discussed a theory he developed—one I believe is essential to understanding the surreal world we find ourselves in these days.

Myriad past EVAs have harped on the economic constant known as money velocity. Unlike many items upon which economists pontificate, this is a hard fact, not a theory. It is an output derived from dividing GDP by the money supply (M2). And, as these pages have relayed ad nauseam, velocity has been in one of the most relentless bear markets of all time.

Many years ago, when the Fed’s balance sheet was several trillion dollars lighter, we disagreed with the popular view back then that its plan to crank up the printing presses would lead to high inflation. This was due to our recognition that money turnover, or velocity, was doing a cliff dive. The unprecedented plunge in velocity, outside of the 1930s, is why consumer prices have stayed so muted (at least as officially calculated), despite the fact the Fed has now conjured up over $3 trillion of bogus bucks.

As discussed in prior EVAs, Charles has separated what he calls economic velocity from financial velocity. He is the only leading economist, as far as I know, who has identified this bifurcation. At this point, his thesis is unproven, and perhaps it never will be formally validated. But, based on common sense and real world conditions, I believe it’s very hard to dispute his contention.

To review his theory, Charles asserts that for years there has been rapid creation and circulation of money, or liquidity, when it comes to asset prices. Consequently, almost everything people—especially the wealthy—invest in has "gone Ballmer" (if you’ve seen the videos of Steve Ballmer hyperactive antics at his Clippers’ press conference, you know exactly what I mean!). In fact, his $2 billion purchase of the LA Clippers (we’re not talking the Lakers here, my friends) might be one of those signature, top-of-the-mania events we look back on and shake our heads about in a few years.

On the other hand, money velocity that impacts the real economy has for the most part been doing the inverse. (Admittedly, there is recent evidence of a pick up in lending, which might finally revive the sclerotic condition of money circulation; the jury is still out on this issue.)

One reason Charles’ theory rings true with me is that it explains how there can be such a dichotomy between markets "gone Ballmer" across almost every asset class, and a global economy that continues to underachieve like, well, the LA Clippers—the poster-boys for NBA mediocrity. (See, I’m sticking to my pledge of not slamming Seattle sports teams. Hey, even the Mariners are winning!)

So, to Will’s point, maybe the economy is somewhat equivalent to 2004 when that recovery was in its early phases and fears still lingered (especially from a certain New York Times economist) about a jobless recovery. When you think about it, if Charles is right, after five years of high financial velocity and low economic velocity, it’s totally plausible for the markets to be at a 2007 point while the economy remains several years from recession, as it was in 2004.

This is why we continue to see lead items in the media, such as this front page Wall Street Journal squib from last Friday: "Central bankers gathering in Jackson Hole, Wyoming, confront a global economy that has again disappointed, leaving them reluctant in some places and unable in others to turn off spigots of easy money."

Do you think that at some point it would dawn on the planet’s monetary mandarins, as Jim Grant refers to our esteemed central bankers, that they may be the problem, not the solution? Might they read some of the extensive expert commentary-- including, of course, from Charles Gave, but also David Rosenberg, John Hussman, Lacy Hunt, Bill Gross, and many others—that providing "money for nothing" attenuates, not accentuates, economic growth? Apparently not—despite the evidence that’s mounting on a daily basis. To drive home this point, courtesy of Gary Shilling, as Fed policies have become increasingly lax over the last twenty years, and particularly most of the last decade, economic growth has also been in a structural bear market. Japan, of course, blazed the trial with zero interest rates and its economy has been about as far from blazing as you can get.

David Rosenberg recently concisely summarized this situation: "Maybe, just maybe, the tonic for a better performing economy actually comes from the Fed gradually raising rates, allowing for money velocity to expand…" The big sell-side Wall Street firms (i.e. brokers and investment banks) have remained mostly silent on this issue, perhaps because the present environment of booming financial markets and a limping economy is ideal for their bottom-lines.

Unfortunately, though, this game can’t continue indefinitely. After years of under-investing in productive assets, Corporate America is starting to bump up against capacity limits, despite the feeble expansion. As mentioned in previous EVAs, this creates fertile conditions for the dreaded "S" word in economics: stagflation. This is definitely not one of the parallels with 2004, and is a reason why I remain dubious that the economy has considerable room to run.

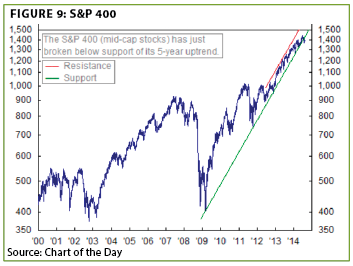

To close, though, I thought I would display a variation of past charts on the overall stock market. Instead of showing the S&P 500, I wanted to focus on the mid-cap index. Similar to its small cap cousin, this index has been on a tear, not just from the 2009 lows, but even going all the way back to the dawn of the millennium. Unlike in 2004, when mid-cap shares were up a modest 25% from the bottom, they have now risen 240% from their nadir. They are also trading at 23 times earnings versus the S&P at an overall P/E of 18.

Not to worry, though—Wall Street is assuring us all that there are no bubbles in the stock market. Boy, I feel better. Don’t you?

![]()

Jack of all trades, master of none. In the prior edition of the Evergreen Exchange, Tyler Hay did an excellent job discussing some common misconceptions surrounding the wealth management industry. As the Director of Wealth Management at Evergreen, I thought this would be an excellent opportunity to piggy-back on his most recent writings and outline how we strive to exceed our client’s expectations.

As a brief background, I’ve been in the investment management industry for over thirteen years. I graduated from law school with a focus on estate planning and tax law, and am a Certified Financial Planner. While studying law, I worked as an equity analyst here at Evergreen and focused solely on our clients’ investments. But, I am also the first to concede that I am not an expert in everything related to your finances. If you meet with an advisor who claims to be one, I would advise you to run as quickly as you can in the opposite direction. I’ve spent years studying the tax code and have become familiar with the different insurance options available. I can assist with many different retirement planning questions, and I’ve helped build our current investment portfolios. In spite of my broad background, our entire wealth management strategy is predicated on allowing experts to excel in their individual specialties.

As wealth managers, we take on many different roles. We need to anticipate shifts in the markets, changes in tax law, foresee business planning transitions, understand estate planning nuances and be knowledgeable in a myriad of different capacities. Most importantly, we need to understand how all of these changes holistically affect our clients’ financial situation.

The wealth management role is often outlined and presented as being a CFO for a family’s assets. This sounds great in theory, but we think this analogy is inaccurate. A CFO reports to a very active CEO. But, many of our clients are retired, and quite frankly, don’t want to play an active role in the investment process. We take this desire very seriously, too! For the families who engage our wealth management services, we hold ourselves out as the active leading member of their team. We’re accountable to the client, and in our eyes, they are akin to the Chairman of the Board of Directors for their portfolio—i.e., in a supervisory rather than active management role.

Accordingly, as Tyler mentioned, we assist in building the framework for our client’s financial future. Depending on the complexities of the client’s situation, this process likely includes interviewing numerous professionals to determine the path to financial success that best suits them. Frequently, other wealth mangers will exclude this step because they’ve developed important relationships to their business. For instance, they utilize a single CPA, estate attorney, investment banker, and/or investment manager to handle most of their clients’ needs. Often these relationships are built off many years of referral reciprocity—not because it’s best for the client. At Evergreen, we won’t universally prescribe a professional’s help for our clients. We work with the expert that presents the best ideas for our clients. Our role is to scour the industry, find the best solution, and present the strongest proposal to our clients. Furthermore, it is our job to make sure the client understands each concept and the intricacies that come along with the proposed solutions. If the client is uneasy with a decision, but we believe it is in their best interest, it is also our job to convince them that the uncomfortable path is the best to take. Ultimately, though, the client makes the final call.

Once the foundation has been laid, the wealth manager’s job is to oversee the team that’s been employed. We stay in constant contact with our client’s CPAs, estate attorneys, and other chosen professionals. Finally, we participate in reporting back to the client concerning any adjustments.

Job done, time to move on. All too often, we see wealth managers overstepping on many different levels. The most common area of obtrusion, however, is on the investment side. It’s our belief that this is the realm that needs the highest level of expertise. All of our planning that’s done before managing someone’s money is predicated on some sort of return assumption made by an estate planning attorney, CPA, CFP or other financial expert. Often, and especially for ultra-high net worth clients, investment managers use a simplistic investment strategy. This leaves clients’ assets either overly exposed to unnecessary loss of capital, or conversely, underutilizes capital available to achieve reasonable growth. We’ve inherited several client portfolios where poor asset allocation decisions have been made by a wealth manager. Unfortunately, these errors are often only discovered after the market experiences a significant decline, usually resulting in major capital loss to the client. Income investing is probably the most egregious area where we see poor management. In one case, an advisor allowed an outside firm to manage a laddered investment grade municipal bond portfolio and charge an annual fee to the client. There was no active management of the portfolio, just a fee taken by the investment firm and the wealth manager. These are the scenarios that give our industry a bad name!

Compounding these issues, wealth managers will often charge their fee, and then on top of that allow another fee to be charged by the firms chosen to invest the funds. Based on the high probability of low future returns from most investment sectors, this double-fee structure is a major hurdle to overcome for any asset manager!

Why would a wealth manager prefer this positioning? It’s very simple: They incur no accountability. If the investment manager’s performance is poor, they fire the manager. How do you know your wealth manager is hiring and firing the actual money managers in a prudent way? To what benchmark is he or she tracked against? In our experience, all too often wealth managers and their close cousins, investment consultants, are overly reliant on rear view mirror investing and risk analysis models that are just as backward-looking. As Buffett has repeatedly said, earning superior returns is simple but it’s not easy. And if making money was as easy as looking at the past, historians would be investment superstars!

At Evergreen, we present all solutions proposed. We meet with the selected experts and review the clients’ strategy regularly (with them and their team) and manage their funds in accordance to the specific plan. Ultimately, we hold ourselves accountable for achieving the assumptions that we’ve outlined. In other words, we are accountable—we want our clients to know they are taken care of, whether they are on the beach in Hawaii, or stuck in an office working on their next big deal. We may use managers outside of Evergreen, but we make that decision on behalf of the client and are, when all is said and done, responsible for the total investment returns. Wealth management is not a process that is executed over a short time period and forgotten. It is constantly reviewed, nurtured, and adjusted accordingly, so that a clients’ legacy can endure generations.

Important Disclosures

This report is for informational purposes only and does not constitute a solicitation or an offer to buy or sell any securities mentioned herein. This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. All of the recommendations and assumptions included in this presentation are based upon current market conditions as of the date of this presentation and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. Information contained in this report has been obtained from sources believed to be reliable, Evergreen Capital Management LLC makes no representation as to its accuracy or completeness, except with respect to the Disclosure Section of the report. Any opinions expressed herein reflect our judgment as of the date of the materials and are subject to change without notice. The securities discussed in this report may not be suitable for all investors and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. Investors must make their own investment decisions based on their financial situations and investment objectives.