“If you are on the wrong road, progress means doing an about-turn and walking back to the right road; and in that case, the man who turns back soonest is the most progressive man.”

- C.S. Lewis

When the Punch Bowl Runs Dry

In this week’s Guest EVA, we harken back to the famous “punch bowl” speech delivered almost sixty years ago by the late, great Federal Reserve Chairman, William McChesney Martin, Jr. This message has never been more relevant, even on the day it was delivered in October 1955.

William McChesney Martin served as Chairman of the Federal Reserve System from 1951 to 1970

William McChesney Martin served as Chairman of the Federal Reserve System from 1951 to 1970

Believe it or not, there was a time—not so long ago—when the Fed served to safeguard the stability of the US financial system. Rather than feeding bubble after bubble in the hope of maximizing economic pleasure and minimizing economic pain, the Fed’s self-described role was to “lean against the winds” of both inflation or deflation and remove the “punch bowl” of easy credit “just as the party was really warming up.”

Monetary policy was embraced as a powerful tool for alleviating the “shortage of currency or credit in times of critical need,” but respected as a dangerous tool that should be used responsibly in normal times to “prevent inflation and thus avoid the inevitable aftermath of deflation.” Instead of attempting to abolish the business cycle or boost a sitting President’s political prospects at the risk of overheating the economy, it was clear—even then—that “if we ask too much of monetary policy, we will not only fail but we will also discredit this useful, and indeed indispensable, tool for shaping our economic development.”

As Martin noted, “The transformation of this country from a wilderness to a highly developed civilization demonstrates the results that can be obtained through a system which is directed toward releasing, not shackling, energies and abilities… We cannot substitute the judgement of a few in authority for the free and independent judgements of the community as they are expressed in the market place.”

If you find yourself nodding in agreement as you read Chairman Martin’s speech, you’re not alone. It smacks of common sense. While Martin admits that the laws of supply and demand may be suspended temporarily in times of great crisis, he goes out of his way to emphasize that the law of the market is like the law of gravity. It “cannot be permanently repealed.”

Unfortunately, the days of a self-restrained Federal Reserve are over. And, in fact, those “good ol’ days” only existed when prudent chairmen with painful real world experience—like Bill Martin and Paul Volcker—fought tooth and nail to (1) defend the Fed’s independence and (2) exercise that independence in the best long-term interests of the nation.

Seventeen years after Martin’s death in 1998, the Federal Open Market Committee (FOMC) he once restored to independence now threatens the very financial system it was created to protect. Under Greenspan, Bernanke, and Yellen, the Fed has evolved to safeguard only the status quo. Rather than removing the punch bowl just as the party gets going, the FOMC now seeks to keep the party going as long as possible. For decades now, the US has enjoyed longer expansions and generally shorter recessions as a result of falling interest rate levels, rising debt loads, a general lack of fiscal restraint, and a central bank balance sheet that appears to have no limit.

But what happens when the punch bowl runs dry?

Seven years into one of the longest—and THE weakest—economic expansions in US history, the Yellen Fed shows no signs of turning back. Interest rates have remained at zero since 2009, trillions of QE-conjured dollars have been poured into the banking system, and trillions more in savings have been forced to seek out higher returns and more acceptable yields in progressively riskier assets. Meanwhile, low interest rates and high uncertainty are incentivizing financial engineering over long-term capital investment even as our aging infrastructure is beginning to crumble.

How much more of this madness can the US economy take? How much more of this can the world economy take? We have no idea, but it can’t last forever. And while a 25 basis point hike to refill the Fed’s punch reserves in September or December 2015 has the potential to trigger accelerated outflows from emerging markets and high yield bonds—and threaten richly-valued US equities —it’s a far cry from the kind of “normalization” that would leave the central bank with credible options in the next (and possibly imminent) recession.

As investors, we have a choice to leave the party early, to shun dangerously over-valued markets, to seek out assets priced to provide a margin of safety and/or steady cash flows in the various economic environments that could follow, and to keep some of our powder dry for the buying opportunities ahead.

I wonder what Chairman Martin—known in the 1930s as the “Wonder of Wall Street” —would do in our situation.

Worth Wray, Chief Economist / email him

Worth Wray, Chief Economist / email him

ADDRESS OF WILLIAM MCCHESNEY MARTIN JR.

Chairman, Board of Governors of the Federal Reserve System

Waldorf Astoria Hotel New York City October 19, 1955

There’s an apocryphal story about a professor of economics that sums up in a way the theme of what I would like to talk about this evening. In final examinations the professor always posed the same questions. When he was asked how his students could possibly fail the test, he replied simply, “Well, it’s true that the questions don’t change, but the answers do.” Here the questions are in large measure hardy perennials: How do we attain and retain prosperity? How do we achieve normal healthy growth? How do we preserve the purchasing power of our money? The answers to these interrelated questions in the 1950’s far differ in important respects from those of earlier decades.

My purpose tonight is to explore with you some of the main currents and undercurrents of thought which have colored and shaped these differing answers.

It is, of course, unorthodox, if not downright poor form, to reach your conclusion in the course of your introductory remarks. But, as a matter of emphasis, I would like to state it now.

In the absence of war, or serious conflict among our people over political or social aims, the road to a substantially higher standard of living lies ahead of us as clear and as smooth as our modern turnpikes. We have passed through the turnstiles and are, in my judgment, out on the open road. This position has been achieved after a good many ups and downs false starts, adaptations to war and preparations for war, false turns, and poor directions. Furthermore, the machine we are driving is adequate and capable of traversing the grades, curves, crossroads, and danger points, provided only that the drivers observe the speed laws, are alert and responsible, and sufficiently trained and experienced in the art of driving to understand the nature of the principles of propulsion, and the goals of the journey they are making. Our ability to travel this road safely depends upon a community of drivers who understand and utilize the time-tested principles which are derived from our inheritance.

It seems rather striking that one of the ideas now firmly imbedded in our articles of material faith, the concept of governmental responsibility for moderating economic gyrations, is almost entirely a product of our own Twentieth Century.

This concept, which is steadily being brought into sharper focus, has evolved from general reaction to a succession of material crises heavy in human hardship. It grew from mass desperation and demand for protection from economic disasters beyond individual control.

The Federal Reserve System, which I have the honor to represent, was our earliest institutional response to such a demand. It emerged out of the urgent need to prevent recurrences of such disasters as the money panic of 1907, and out of the thought that the Government had a definite responsibility to prevent financial crises and should utilize all its powers to do so.

Accordingly, 42 years ago Congress entrusted to the Federal Reserve System responsibility for managing the money supply. This was an historic and revolutionary step. In framing the Federal Reserve Act, great care was taken to safeguard this money management from improper interference by either private or political interests. That is why we talk about the overriding importance of maintaining our independence. Hence we have our system of regional banks, headed up by a coordinating Board in Washington, intended to have only that degree of centralized authority required to discharge effectively a national policy. This constitutes, as those of you in this audience recognize, a blending of public interest and private enterprise uniquely American in character. Too few of us adequately recognize or adequately salute the genius of the framers of our central banking system in providing this organizational bulwark of private banking and business.

Since the Federal Reserve System came into being, the problems of inelasticity of currency and immobility of bank reserves—which so often showed up as shortages of currency or credit in times of critical need—have been eliminated, and money panics have largely disappeared. In this specialized respect there can be no doubt that the System has made notable progress, but in the more fundamental role of stabilizing the economy the record is not so clear. All of us in the System are bending our best efforts to capitalize on the experience of the past, and our current knowledge of money, so as to make as large a contribution as possible in this direction. But a note should be made here that, while money policy can do a great deal, it is by no means all powerful. In other words, we should not place too heavy a burden on monetary policy. It must be accompanied by appropriate fiscal and budgetary measures if we are to achieve our aim of stable progress. If we ask too much of monetary policy we will not only fail but we will also discredit this useful, and indeed indispensable, tool for shaping our economic development.

The answers we sought to the massive problems of the 1930’s increasingly emphasized an enlarging role for Government in our economic life. That role was greatly extended again in the 1940’s when the emergency of World War II led to direct controls over wages, prices, and the distribution of goods ranging from sugar to steel.

That experience led to growing concern over the effect of a straitjacket of controls on the economy’s productive capacity, and the price that would be exacted in terms of individual liberty if the harness of wartime economic controls were carried over into the post-war years.

Such a straitjacketing of the economy is wholly inconsistent with our political institutions and our private enterprise system. The history of despotic rule, of authoritarian rule, not merely in this century but throughout the ages, is acutely repugnant to us. It has taken a frightful toll in human misery and degradation.

The transformation of this country from a wilderness to a highly developed civilization demonstrates the results that can be obtained through a system which is directed toward releasing, not shackling, energies and abilities. The fruits of these energies and labors are shared in growing abundance, not by primitive barter, but by the processes of the market place.

The advantages of a system where supply capacities and demand wants and needs are matched in open markets cannot be measured in economic terms alone. In addition to the advantages of efficiency in the use of economic resources, there are vast gains in terms of personal liberty. Powers of decision are dispersed among the millions affected instead of being centralized in a few persons in authority.

The basic concept of the market system has remained with us since the founding of the nation. It has remained the cornerstone of our society to this day, although we have done some extensive remodeling of the structure as a whole from time to time.

We have in the past done some remodeling for the admirable purpose of correcting structural defects and distortions. Competitive, freely functioning markets are one thing, and rigged markets are another. Rules and regulations to prevent rigging are necessary and essential to a sound structure.

Other remodeling has come about because the American people have refused to accept economic goals as their sole objective. That was true in older generations, as well as our own. Our family inheritances have, I am glad to say, usually included the beliefs that man cannot live by bread alone, and that in a properly equipped home library the Bible should occupy a more important place than a manual of arms or a mail order catalogue. Let it be said, to our credit, that American economic action has often been determined by balancing material advance against other human objectives.

For these reasons, and perhaps others, our market system has been modified continuously throughout this country’s history. Ideas of market places functioning with no rules or regulations except the “law of the jungle” have, quite justly, gone the way of the great buffalo herds. When we speak today of “free markets” we of course mean markets that are only relatively free, as the freedom of speech we enjoy is itself only a relative freedom. The essential characteristics of free markets have nevertheless been retained.

It is true that in a great emergency we have been willing to make a departure from our market structure, but our mood has been that of the man who has to leave home for the confines of a bomb shelter. When a war comes on, we are willing to put up with all sorts of economic controls and dictation of even small details of our economic life. The dignity of the individual gets submerged in the necessity to win the war. The law of supply and demand is suspended temporarily, but it cannot be permanently repealed. It is always with us just as is the law of gravity.

When peace is restored we do not continue to ignore it. We cannot substitute the judgment of a few in authority for the free and independent judgments of the community as they are expressed in the market place. We cannot do so, that is, and retain our concept of freedom in a competitive, private enterprise economy.

I am not unaware that freedom entails certain hardships on the nervous constitution. It gives us opportunity to choose, but it also requires the making of choices. The pleasure of having a choice to make is counterbalanced by not only the necessity for making a choice, but also the responsibility for accepting the consequences of that choice, whether good or bad. Naturally we like the consequences only when our choice proves right. That’s one reason it is easier to make a mistake than to admit one.

It requires no strain on my imagination to suppose that there might be some, even in this audience, who occasionally feel a nostalgia for the pegged money market that came into existence during the war and continued until the Treasury-Federal Reserve accord of March 1951 turned us back in the direction of a freer market.

Free markets, like free economies, have a way of going down as well as up, and thus reminding us that our system is one of profit and loss, entailing penalties as well as rewards. During the last four and a half years the Federal Reserve has pursued a monetary policy characterized by flexibility, or prompt adaptation to the sharply changing needs of a dynamic economy. It has been necessary in this period to combat both the forces of inflation and of deflation.

There are some who contend that a little inflation—a creeping inflation—is necessary and desirable in promoting our goal of maximum employment. My able associate, Allan Sproul, President of the Federal Reserve Bank of New York, put his finger on the fallacy in this contention in testifying before a Congressional committee earlier this year when he said:

“Those who would seek to promote ‘full employment’ by creeping inflation, induced by credit policy, are trying to correct structural maladjustments, which are inevitable in a highly dynamic economy, by debasing the savings of the people. If their advocacy of this course is motivated by concern for ‘the little fellow’, they should explain to the holders of savings bonds, savings deposits, building and loan shares, life insurance policies and pension rights, just how and why a rise in prices of, say, 3 per cent a year is a small price to pay for achieving ‘full employment’. They should also explain to all of us—little, big, and just plain ordinary Americans—what becomes of our whole system of long term contracts, on which so much of our economic activity depends, if it is to be accepted in advance that repayment of long term debt will surely be in badly depreciated coin.”

If inflation would in fact make jobs, no reasonable man would be against it. But as I have frequently emphasized, inflation seems to be putting money into our pockets when in fact it is robbing the saver, the pensioner, the retired workman, the aged--those least able to defend themselves. And when the inevitable aftermath of deflation sets in, businessman, banker, worker, all suffer. That doesn’t mean jobs. It means just the opposite.

There have been some rather wide swings in attitudes toward monetary policy during recent years. In the depression, a great number came to the conclusion that monetary policy was ineffective as an instrument for promoting recovery from economic decline. Following World War II, some were troubled by the move from direct controls to restoration of the general control involved in monetary policy because they feared it could not restrain the inflation then prevalent—not, that is, without being so drastically exerted as to plunge us into a devastating depression.

Nowadays, there is perhaps a tendency to exaggerate the effectiveness of monetary policy in both directions. Recently, opinion has been voiced that the country’ s main danger comes from a roseate belief that monetary policy, backed by flexible tax and debt management policies and aided by a host of built-in stabilizers, has completely conquered the problem of major economic fluctuations and relegated them to ancient history. This, of course, is not so because we are dealing with human beings and human nature.

While the pendulum swings between too little or too much reliance upon credit and monetary policy, there is an emerging realization (more and more widely held and expressed by business, labor and farm organizations) that ruinous depressions are not inevitable, that something can be done about moderating excessive swings of the business cycle. The idea that the business cycle can be altogether abolished seems to me as fanciful as the notion that the law of supply and demand can be repealed. It is hardly necessary to go that far in order to approach the problems of healthy economic growth sensibly and constructively. Laissez faire concepts, the idea that deep depressions are divinely guided retribution for man’s economic follies, the idea that money should be the master instead of the servant, have been discarded because they are no longer valid, if they ever were.

Nor does the discarding of old ideas and the substitution of new ones mean that we are throwing basic laws or principles overboard. It is the return to first principles in many parts of the free world that is the most significant aspect of world-wide recovery and progress outside of the Iron Curtain. And that, in turn, vastly brightens the hope of lasting peace.

By first principles I mean time-tested basic concepts of the market place and the development of competitive private enterprise, with only that degree of Government interference or regulation necessary to prevent abuses and excesses. We see a return to these concepts here and abroad because other concepts have failed, and where there has not yet been a revival of these concepts economic troubles are acute.

As I suggested at the outset, the basic problems, the questions, remain pretty much the same always. The answers are different—and no one would be so rash as to say that we have ultimate solutions for all of our problems. We can say confidently, I think, that we have discarded some wrong answers—that we have returned to some of those fundamental principles under which our society, our institutions, have flourished with incomparable benefits, benefits not merely material.

There will always be some, of course, who think we must go through the wringer periodically to purge the economy. There will always be cynics and defeatists, no doubt, who say that because there have always been disastrous depressions and more disastrous wars, we must accept these visitations as inevitable. If there are enough hopeless Jeremiahs, enough defeatists and cynics, those calamities are indeed inevitable. If we do nothing about it, if we do nothing to prevent inflation and thus avoid the inevitable aftermath of deflation, then of course we are defeated. Today’s generations will accept no such fatalistic philosophy.

If we fail to apply the brakes sufficiently and in time, of course, we shall go over the cliff. If businessmen, bankers, your contemporaries in the business and financial world, stay on the sidelines, concerned only with making profits, letting the Government bear all of the responsibility and the burden of guidance of the economy, we shall surely fail. I am as weary as you are of pious platitudes and after dinner preachments about leadership and financial statesmanship. But the fact is that the Government isn’t something apart and remote from you. It is you—all of us. If those responsible for major decisions in business, finance, labor, agriculture, are irresponsible, Government can’t compel you, short of moving in the direction of dictatorship, to be reasonable, or moderate, or prudent. In the field of monetary and credit policy, precautionary action to prevent inflationary excesses is bound to have some onerous effects—if it did not it would be ineffective and futile. Those who have the task of making such policy don’t expect you to applaud. The Federal Reserve, as one writer put it, after the recent increase in the discount rate, is in the position of the chaperone who has ordered the punch bowl removed just when the party was really warming up.

But unless the business community, leaders in all walks, exhibit moderation, prudence, and understanding, then we will fail and deserve to fail, I cannot believe we will be so blind. I have a deep and abiding faith in that undefinable yet meaningful phrase we frequently use—“the American Way of Life.”

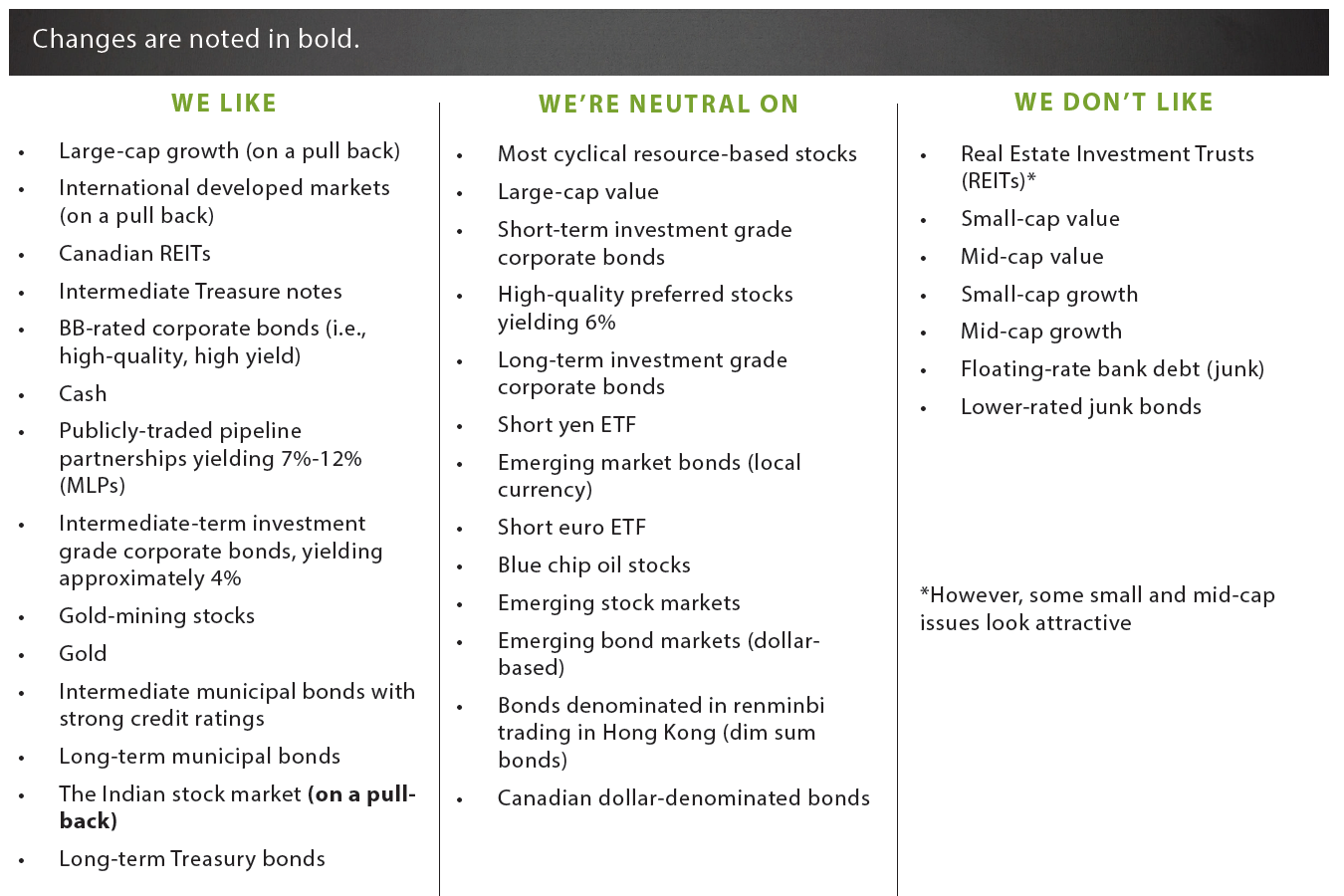

OUR CURRENT LIKES AND DISLIKES

Changes are noted in bold.

DISCLOSURE: This report is for informational purposes only and does not constitute a solicitation or an offer to buy or sell any securities mentioned herein. This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. All of the recommendations and assumptions included in this presentation are based upon current market conditions as of the date of this presentation and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. Information contained in this report has been obtained from sources believed to be reliable, Evergreen Capital Management LLC makes no representation as to its accuracy or completeness, except with respect to the Disclosure Section of the report. Any opinions expressed herein reflect our judgment as of the date of the materials and are subject to change without notice. The securities discussed in this report may not be suitable for all investors and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. Investors must make their own investment decisions based on their financial situations and investment objectives.