“I don’t want to go from wild turkey to cold turkey.”

- Richard Fisher, Dallas Fed President, referring to the end of the Fed’s ultra-easy money policies

“The problem with fellows [like central bankers], who believe that the markets cannot be left alone and need to be managed when the circumstances are exceptional, is that pretty quickly they decide that every day the circumstances are exceptional and so they intervene all the time.”

- Charles Gave

Food for thought. Perhaps this scenario has happened to you: You go to a gourmet restaurant with your “foodie” friends. A tasting menu is being served. You don’t want to act like a total rube, so you don’t gag when dishes like sautéed smelt garnished with raspberry vinaigrette are placed in front of you. But the truth is, you just want a good steak and a Caesar salad. So, with great reluctance, you begin to try the various items that sound repulsive to you.

But then, a most surprising development occurs—the smelt actually tastes great! You find yourself liking the weird stuff you never would have ordered in multiple lifetimes. You discover that a truly talented chef can make inedible sounding ingredients taste delectable. And this leads me to introduce this week’s Guest EVA.

As noted in previous EVAs, Anatole Kaletsky is the “Kal” of our partner firm GaveKal Research. He is one of the most renowned European economists, and his rolodex includes nearly all of the shakers and movers on the Continent (where the situation appears to be shaky once again). In addition to being a true intellect and a talented writer, Anatole is also a gifted speaker. I had the pleasure of experiencing his oratory skills first-hand at this year’s Mauldin/Altegris Strategic Investment Conference, where he shared the spotlight with some of the investment world’s most acclaimed personages.

Now, with the kudos out of the way, I also need to admit that Anatole is my version of a 5-star restaurant’s tasting menu. He regularly serves up an extensive menu of ideas and conclusions that I often find unappealing yet, in stark contrast to a certain New York Times Nobel Prize-winning journalist, he does so with such skill and aplomb that his views become alluringly palatable. (Note, that I didn’t say credible, at least to my admittedly stubborn mind).

A classic case in point is his recent essay, “Monetary Policy Is No Threat To Markets.” As even cursory EVA readers are aware, I believe the current “remedies” being administered by most of the developed world’s central banks are a threat to the long-term vitality of the financial markets and the global economy. Yet, as I carefully, albeit skeptically, read Anatole’s piece, I was once again impressed with the persuasive manner in which he makes his case. And, as I have conceded before, his charitable view of Fed actions in recent years has been more in synch with the effervescent (dare I say, bubbly?) performance of stocks than has mine.

For those with a bullish inclination, you should be rooting for Anatole’s benign view of the Fed’s perma-easy stance, a condition he believes will continue almost ad infinitum. The alternate view, one I’ve so frequently expressed, is that the current confidence in central bankers is horribly misplaced and will lead to an outcome similar to the last two Fed-allowed and/or enabled bubbles. Interestingly, his equally formidable partner, Charles Gave, views the world of printing press prosperity with an eye every bit as jaundiced as my own.

One of the many wonderful aspects of GaveKal is that intense opinion exchanges are not only tolerated, they are encouraged. It is in that spirit that I share Anatole’s latest treatise with all of you.

MONETARY POLICY IS NO THREAT TO MARKETS

By Anatole Kaletsky, GaveKal Research

In the first two articles of this series, I argued that the US economy has now clearly reached ‘escape velocity’ and that, with little prospect of a renewed recession in the next year or two, investors are forgetting their earlier fears of secular stagnation and becoming increasingly confident about the extraordinary monetary and fiscal policies adopted by all the major world economies (see The Case For A Structural Bull Market and The Global Obsession With US Data). The obvious risk to this consensus—apart from the possibility that it is plain wrong and that a recession is imminent, as some bond market indicators suggest—is what will happen when monetary policies change direction. My answer is “nothing much”—because the prospects for monetary policy, like the prospects for cyclical conditions, are now much clearer than they have been for many years. Moreover, when the US and UK central banks start to move in the next year or so, the policy shift will be so moderate that it will have almost no effect either on economic conditions or on investor expectations. That may be hard to swallow. In dozens of client meetings before the summer holidays, I encountered more resistance to this idea than to any other. Nevertheless, I am confident that over the next year or two, monetary policy will not be a major driver of financial markets.

Believe in the central bankers

Why, then, am I so sure that interest rates will remain ‘lower for longer’? Mainly because the central bankers say so. Of course, central bankers cannot always be trusted. I have argued in the past that central bankers are ‘licensed to lie’ in a way that would end the careers of democratic politicians. Most analysts today are therefore sceptical about central bankers’ promises, especially Britain and the US. Yet strangely enough, the very modest tightening built into forward yield curves suggests that markets collectively tend to believe the promises of dovish monetary policy, despite the scepticism of professional economists. In my view, there are five reasons to side with the markets and trust dovish central bankers, rather than the more hawkish analysts whose job is to predict what central banks will do next. The first three reasons are familiar, the other two less so:

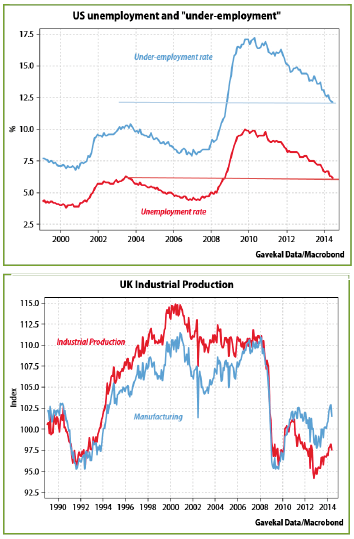

Firstly, the normal cyclical triggers for monetary tightening—inflation, unemployment and capacity utilization—do not yet signal any tightening, even in the US or UK. In the US, unemployment, at 6.1%, is still only just below the previous cyclical peak of 6.3% and is 0.5ppts above the point where the Fed started tightening in 2004, while the under-employment rate (U-6) is 2.5ppts higher than it was then. In the UK, the standard indicators of excess capacity are even more striking.

Unemployment at 6.5% is 1.5ppts above where it was in 2003 when the BoE was still easing, while manufacturing production is still 9% below the level of 2007. Under these circumstances, fear of inflation would be the only standard argument for tighter money, but signs of accelerating inflation are almost entirely absent, at least for now.

The policy mix is turning Japanese

Secondly, while market economists often argue that the 2008 financial crisis lowered trend growth rates and increased structural unemployment, from the policymaker’s standpoint the structural changes since 2008 have created incentives to keep monetary policy extremely loose. Extremely low interest rates reduce government deficits, ease servicing costs for highly leveraged householders and

allow inflation to redistribute wealth from lenders to borrowers. So to the extent that excessive leverage and financial fragility remain serious structural impediments to economic growth, central bankers will continue erring on the side of lower interest rates.

And even if economies start growing robustly enough to withstand substantial policy tightening, the priority should be fiscal tightening to reduce government debt burdens. Wherever fiscal tightening proves politically feasible, as in Japan at present, central banks will be only too happy to support tougher budgets with easy monetary conditions. This Japanese-style policy mix of tighter budgets and looser money will probably be repeated in the US, the UK and Europe whenever politically possible during the next decade.

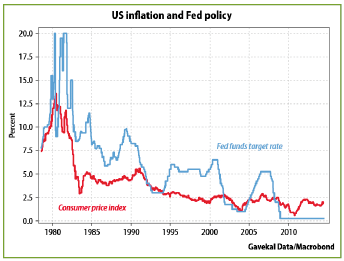

The third reason for believing in ‘lower for longer’ is that the professional central bank-watchers and macro traders who are most sceptical about this doctrine have an inherent bias to predict dramatic monetary moves—and ever since 2008 their bias has proved consistently wrong. Part of the reason for this intellectual partiality is that so many people’s incomes depend on predicting central bank activism, rather than inertia. After all, in a world where the weather never changed from day to day, meteorologists would be redundant. More importantly, every economist educated since 1980 takes it as axiomatic that the main goal of monetary policy is price stability and that every central banker’s nightmare is to “get behind the curve” of rising inflation.

Falling behind the curve

This brings me to my fourth, less familiar, reason for expecting monetary policy to remain essentially on hold for at least another year. Central bankers no longer worry about getting behind the curve of rising inflationary expectations—in fact they positively want to get behind the inflation curve. This is because monetary policy thinking has gradually been transformed by the structural weakening of global demand since 2008. The main objective of monetary policy is no longer simply to control inflation; it is to accelerate nominal GDP growth, while trying to keep inflation within reasonable bounds. How do I know this? Because policymakers keep saying it—and their actions show that they mean what they say. Instead of reacting aggressively to occasional flickers of higher inflation, central bankers openly welcome them and strongly suggest that they want expectations of rising prices and faster income growth to be reembedded into financial, business and consumer thinking. That central bankers want more inflation is widely understood, yet the logical implication is almost never considered: from now on, monetary policy will deliberately and consciously fall ‘behind the curve’ of rising inflation. In fact, the phrase ‘behind the curve’ may soon mutate, evolving from an insult into a badge of honor.

If this sounds preposterous consider the record of Paul Volcker, probably the greatest central banker ever. While Volcker is justly credited with tightening monetary policy in 1979, 1980, 1984 and 1986 to get ahead of rising cyclical inflation, his policy changes were consistently behind the curve of structurally falling inflation. Inflation peaked in the US as early as June 1980. Yet Volcker was still raising interest rates until early 1982. It was not until August 1982, two years after US inflation peaked, that he decisively eased policy—and that was only in response to the Mexican debt default which, on modern accounting rules, rendered all major US banks technically insolvent. In short, during the most important period of his career Volcker was consistently behind the inflation curve. He was reacting to changes in inflation with a long lag rather than trying to anticipate and pre-empt them. His reason for doing this was not, of course, stupidity or incompetence. His goal was to bring inflation down, keep it down and make sure that it never again accelerated to alarming levels. He judged that the only way to do this was to hoist interest rates much higher than almost anyone imagined possible and keep them at extraordinary levels much longer than anyone expected, even after inflation was clearly collapsing. In other words, Volcker wanted to turn the cyclical inflation peak of 1980 into a permanent structural turning point. Only after Volcker had achieved and secured his victory over inflation in 1983-84, did monetary policy shift from a reactive to a pre-emptive mode—the mode it remained in for the next 30 years.

Flirting with disaster

Now apply this lesson to the challenges facing today’s central bankers, most obviously in Japan, but also in the US, UK and even Europe. Volcker decided, after the inflationary traumas of the 1970s, that the US must never again flirt with the disaster of double-digit inflation. Today’s central bankers have decided, after the deflationary traumas of 2008-12, that their economies must never again flirt with

the disaster of near-deflation. More broadly, today’s policymakers, including central bankers, finance ministers and international organizations such as the IMF and the European Commission, have realised that they face fiscal bankruptcy and other disasters (such as breakup of euro) if they ever again experience the abysmally low rates of nominal GDP growth seen in 2008-12.

To try to avoid this fate, today’s central bankers are following the same course as Volcker but in the opposite direction. To make sure that the cyclical lows of inflation and nominal GDP growth of 2009-10 turn into permanent structural lows, central bankers have had to suppress their instinct, acquired during the 30 years of structurally declining inflation, of trying to anticipate inflationary pressures. Instead they have become reactive, waiting not only for stronger growth and inflation, but for proof that the acceleration in nominal GDP will be sustained before they even consider tightening policy. In adopting this reactive approach, policymakers may of course be making a huge mistake, as Charles and many other distinguished economists, including numerous dissidents on the boards of the central banks, have suggested. But rightly or wrongly, this is the policy adopted by the people now in charge at the Fed, the BoE, the BoJ, and more recently even the ECB. And as long as this remains the case, no major central bank will raise interest rates by an economically significant margin (by which I mean more than 25-50bps) before the end of 2015.

The remaining question is whether financial markets could impose a monetary tightening against the dovish preferences of central banks. This leads to the fifth and final reason to believe in ‘lower for longer’. Central banks can now pursue inflationary policies as aggressively as they want without any fear of ‘bond market vigilantes’. These once-mighty beasts, who ruled the financial world by brandishing steep yield curves against inflationary central bankers, are now as extinct as Tyrannosaurus Rex. The main cause of this mass extinction is obvious. Prudential regulation has been transformed into financial repression as solvency requirements have compelled pension and insurance funds to hold long-term government bonds regardless of price, while capital and liquidity requirements have forced banks to buy short-term paper. This financial repression is very convenient for finance ministries, as well as for central banks, and is therefore likely to persist for many years, as in the 1950s, 1960s and 1970s.

Bond market vigilantes paralyzed

In the past few months, however, another, even more powerful international force has paralyzed the small number of bond market vigilantes left in the US and UK who might have ‘disciplined’ the Fed and the BoE. This has been the desperate search for yield by bond investors from Japan and Europe as the BoJ and the ECB have joined the all-out battle against deflation previously waged by the Fed and the BoE. As long as Japanese and European investors view US or British bonds offering 2.5% yields as a ‘deep-value’ investment, the Fed and BoE can laugh at the thought of ‘market pressure’ to bring forward rate hikes. In short, the deflationary pressures in Europe and Japan will allow the Fed and the BoE to stick to ‘lower for longer’, even if this policy is no longer justified by conditions in the US and Britain.

The ultimate consequence of this globalization of monetary policy are hard to predict: perhaps it will cause a stronger than expected recovery, perhaps an inflationary upsurge, or perhaps the capital misallocation and global stagnation suggested by Charles. But whatever may or may not happen in the long run, the bond markets will surely be powerless to impose an unintended monetary tightening on the Fed or the BoE. Which suggests that a big correction in equities, if it hits in the next year or two, is unlikely to be caused by monetary policy expectations. The next article in this series will consider a more likely catalyst.

Important Disclosures

This report is for informational purposes only and does not constitute a solicitation or an offer to buy or sell any securities mentioned herein. This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. All of the recommendations and assumptions included in this presentation are based upon current market conditions as of the date of this presentation and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. Information contained in this report has been obtained from sources believed to be reliable, Evergreen Capital Management LLC makes no representation as to its accuracy or completeness, except with respect to the Disclosure Section of the report. Any opinions expressed herein reflect our judgment as of the date of the materials and are subject to change without notice. The securities discussed in this report may not be suitable for all investors and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. Investors must make their own investment decisions based on their financial situations and investment objectives.