Increased regulatory pressures from the Chinese government have created wild swings in Chinese equities of-late. Technology and education stocks have been hit hardest, as investors have weighed a series of announcements from Beijing aimed at increasing oversight in a wide range of sectors. Continuing news about the crackdown was enough to spook investors at the beginning of the week, as Hong Kong’s Hang Seng index fell -8.2% before rebounding. The question for investors becomes whether this “tug of war” between the Chinese government and capital markets will persist – and for how long.

This week, we are presenting a letter from Evergreen’s partner Louis-Vincent Gave on the subject. Louis is a go-to source for institutional investors trying to interpret global macro risks, including what’s happening in China. Prior to the pandemic, Louis was based in Hong Kong and provides a very unique and noteworthy perspective on the world’s second largest economy. In this letter, he answers many questions for investors trying to make sense of China’s corporate crackdown, including:

Please realize that most major asset managers in the US and Europe are Gavekal clients; thus, Louis’ views are very much worth your time.

In case this report falls into the hands of an unsuspecting minor, I will not show any charts for Chinese education stocks. I’ll just note that they make for some of the most traumatic viewing since the charts of Lehman’s bonds. Take TAL Education: from US$90 per share in February, TAL has fallen to less than US$5. When you look at the company’s cash on hand, that implies a negative value of more than US$2bn. Sharp moves like this and negative equity valuations tend to be triggered either by revelations of fraud or by the sort of dramatic shift in the investment environment only government action can cause—nationalization, regulatory change, or the declaration of war.

The slump in Chinese education stocks reflects a landscape upended by government action. This shift, coming on the back of the cancellation of Ant Group’s IPO, the disappearance from public view of Alibaba and Ant founder Jack Ma, and the crushing in June of Didi Chuxing just days after its US IPO, has cast a severe cloud over the broader markets for Chinese equities. Hong Kong’s Hang Seng index fell -8.2% over Monday and Tuesday. H-shares were down -9.75%.

As you might expect, these events have prompted their fair share of questions from clients. Here are my attempts at answers.

Is what just happened in China a game-changer?

Is what just happened in China a game-changer? The government is openly nationalizing not just companies (for-profit education), but profit pools (by instructing Tencent and Alibaba how to reinvest their earnings, and by forcing Meituan to raise wages). This feels like a revolution. Did Xi Jinping believe that with Donald Trump out of the White House, the world would revert to the old order? And now that Joe Biden has maintained Trump’s anti-China policies, is Xi acting up? I worry that now Xi has torn up the checks and balances put in place by his predecessors, there is nothing to stop the party-state from turning on China’s entrepreneurs and capitalists. This looks big, ugly and frightening. It seems to me that Xi is misplaying a bad hand, or am I missing something?

Yes, the latest decision is a game-changer, but perhaps not for the reasons you think. I can discuss all day the reasons for these moves—as indeed I will. But what matters more for now are their consequences. The first consequence of the crackdown on TAL and others so soon after Didi is that Chinese companies will now find it impossibly challenging to raise capital in the US.

I can’t believe this is an accident and that the Chinese leadership did not think through this obvious first-order effect. And by the way, I don’t just mean that Chinese companies will now find it hard to list on Nasdaq—which they will—but also that a lot of foreign private equity firms operating in Shanghai must now be reexamining the potential investments in their pipeline, and wondering whether to go ahead with them after all.

To illustrate this point, put yourself for a moment in Softbank’s shoes. To a large extent, it was China that saved Softbank from becoming yet more internet 1.0 roadkill. After the 2000 tech bust, Softbank’s share price fell by more than -98%. But Softbank had had the good fortune to back Jack Ma early on. The gains generated by its stake in Alibaba allowed Softbank to rise like a phoenix from its ashes. Now, after losses of US$4bn on Didi, and with all the uncertainty around Ant, Softbank might well start to wonder whether China is simply getting too hard to operate in. Clearly, Xi Jinping’s China is very different from Hu Jintao’s China.

So will foreign private equity investors pack up and leave China? And if they do, will that be a problem for China?

On the capita-raising front: perhaps not. China has plenty of domestic savings to tap into, and promising businesses can grow without foreign capital. But what about the intangibles that foreign private equity funds bring with them —corporate governance, management expertise, network effects and so on? Today, it seems as if China’s leadership is making the bet that China no longer needs these. Or perhaps China’s leaders just believe that given the recent shift in the geopolitical winds, this band-aid needs to be ripped off anyway?

This goes back to the point about Xi playing a poor hand poorly. If the Chinese government has slammed the US capital-raising door for Chinese companies, did it really have much choice in the matter? My colleague Thomas Gatley has been warning of this possibility for the last 12 months and more.

At first, the fear was that US regulators would shut down Chinese listings in the US. Now, it looks like China is doing the breaking-up first. But the relationship has been on the rocks for a while. From now on, Chinese companies that need to raise capital will have to do so either in Shanghai or Shenzhen, or in Hong Kong—in other words, in markets that answer to the Chinese Communist Party, which may prove to be good news for the Hong Kong stock exchange.

I want to imagine that the Chinese leadership did not “accidentally” burn the US capital bridge; and for reasons reviewed on Monday by my colleague Ernan Cui the education sector served as a useful sacrificial victim, allowing the Chinese government to make the points it wanted to convey. In case there is any doubt, these points are:

These messages can hardly be called new, certainly not by anyone who has followed Xi Jinping’s trajectory since 2012. But what perhaps is new is the extent to which the Chinese government is now backing up its implied threats with actions. Xi is showing that he can talk loudly, carry a very big stick, and whack people with that stick. For Western investors accustomed to politicians who, as Anatole Kaletsky said of Donald Trump, “talk loudly, but carry a little stick,” this is a rude awakening.

What is the logic of destroying your own companies?

OK. But I still don’t get the logic of destroying your own companies. Isn’t this like the Ming dynasty ordering all ships to be burnt and closing in on itself? Is this madness on a grand scale? Or is there a rational explanation for the pain the Party is inflicting, first on US investors, but ultimately likely on itself?

I can think of five possible explanations for what to most investors might look like madness. There may well be more.

To illustrate this urgency, think of US scientists at the time of the Manhattan Project. Back in 1943-44, America’s most brilliant scientists signed up to work for the greater good of the war effort. It would have been inconceivable for the best minds to flock to Madison Avenue to sell Coca-Cola or Kellogg’s breakfast cereals.

As Dan put it 2019:

“I find it bizarre that the world has decided that consumer internet is the highest form of technology. It’s not obvious to me that apps like WeChat, Facebook, or Snap are doing the most important work pushing forward our technologically-accelerating civilization. To me, it’s entirely plausible that Facebook and Tencent might be net-negative for technological developments. The apps they develop offer fun, productivity-dragging distractions; and the companies pull smart kids from R&D-intensive fields like materials science or semiconductor manufacturing, into ad optimization and game development...

The internet companies in San Francisco and Beijing are highly skilled at business model innovation and leveraging network effects, not necessarily R&D and the creation of new IP... A large population of people who play games, buy household goods online, and order food delivery does not make a country a technological or scientific leader... These are fine companies, but in my view, the milestones of our technological civilization ought to be found in scientific and industrial achievements instead”.

In early 2020, Dan added:

“It’s become apparent in the last few months that the Chinese leadership has moved towards the view that hard tech is more valuable than products that take us more deeply into the digital world. Xi declared this year that while digitization is important, ‘we must recognize the fundamental importance of the real economy… and never deindustrialize.’”

In other words, maybe the writing has been on the wall for a while.

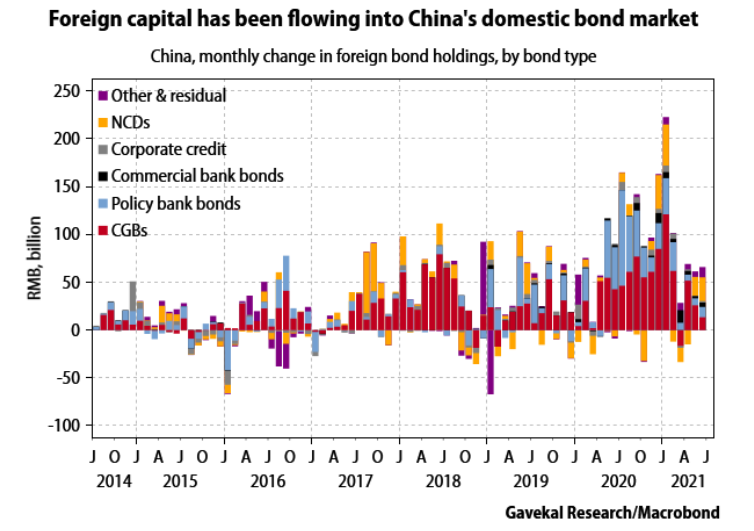

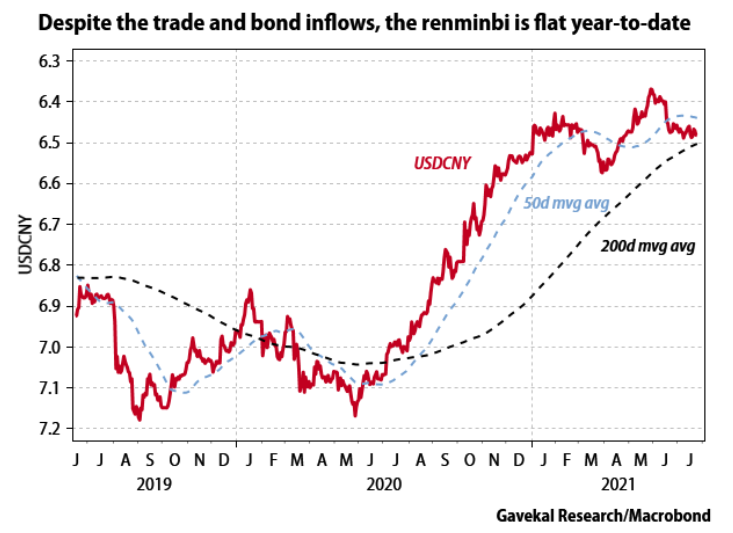

5. The fifth possible explanation (perhaps less a “why” than a “why now”) rests on the fact that China is now experiencing consistent capital inflows. On top of a monthly trade surplus of US$40-60bn, China is seeing persistent flows of US$10-30bn into its bond market. Such large foreign purchases of Chinese bonds is a relatively new development (see the chart below). Combined with the trade surplus, it suggests the renminbi should be shooting up.

However, following the crackdown on Ant, Alibaba, Didi and now the education sector, the exodus of foreign money out of Chinese equities is likely damping expectations of renminbi appreciation.

The bottom line is that there are numerous possible rational reasons for the Communist Party’s course of action. There is no need to conclude Xi has gone mad and that there are no checks and balances to hold him back. As a result, what matters is what these actions will mean for China’s future. The obvious answers are (i) less reliance on foreign capital, (ii) ever more industrial policy and (iii) continued social pressure to act for the “greater good.”

Are luxury goods next?

Does this mean that the luxury goods sector will be next in the line of fire? After all, luxury goods serve little purpose, and arguably exacerbate social divisions by provoking envy and resentment.

I don’t recall seeing any signals recently suggesting the Chinese government might target the luxury sector (maybe I missed something). But I do understand the concern. If China’s leaders are now intent on shifting the economy onto something approaching a war footing, a "war-like" frame of mind, or if they plan to pump ever more resources into attaining self-sufficiency and even dominance in 21st century industries, then private expenditure on luxury goods would appear to be an unwanted diversion.

Against that negative ledger entry, three positive China-related arguments for luxury goods come to mind:

My broader concern is that luxury goods companies today appear aggressively priced, or at least priced to deliver a lot of growth. For now there are no reasons to think Beijing is going to go after the luxury sector. But if it did, the downside could be nasty. In other words, at current valuations, aren’t luxury goods companies a “heads I don’t lose, tails I lose a whole lot” investment?

Isn’t everything China-linked now an asymmetric risk?

On this last point, shouldn’t we assume that China is now a massive asymmetric risk and that investors should avoid anything linked to the Middle Kingdom?

There is no doubt that the decision to take down the tutoring companies ratchets up the asymmetric risk of investing in China plays. Arguably, this is a problem emerging market investors have always faced. In western democracies, policy changes take time. Politicians set out their platforms. There is an election. The victor then tries—often with only limited success —to get his pet project approved by parliament, and finally implemented by the administration. This gives markets plenty of time to price in the eventual outcome.

In emerging markets, a minister can wake up one morning and decide that the negative social effects of, say, education companies outweigh their benefits. And before you’ve had time to pull on your pants, the companies are effectively gone.

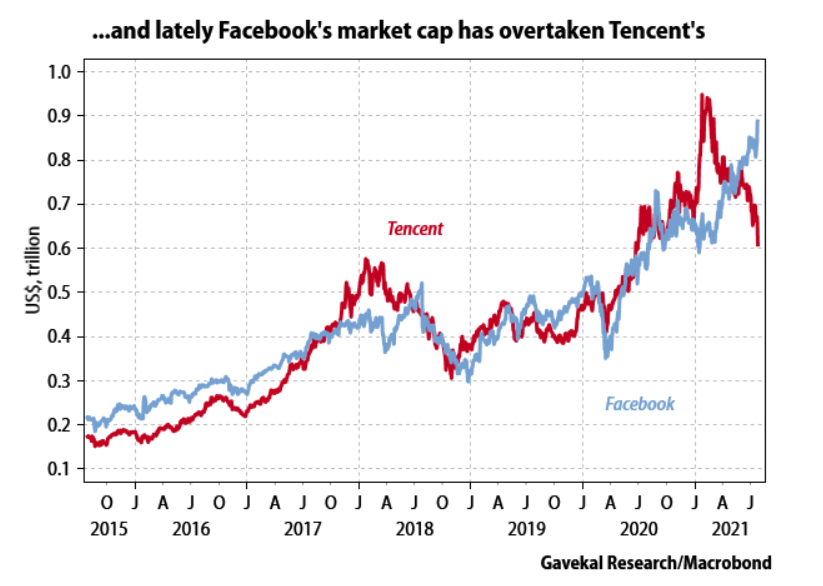

Returning to our earlier example, at their current valuations, luxury goods companies do not appear to reflect this asymmetric risk. However, by now the valuations of stocks closer to the Chinese coalface do. Take as an example, the divergence in market capitalization between Amazon and Alibaba. Back in 2017, the two companies were roughly the same size. Since then, e-commerce has continued to thrive, as have the two companies’ cloud businesses and other business lines. However, their market performances have been starkly different.

The same is true, albeit to a smaller extent and more recently, for Facebook and Tencent.

In short, it seems the segments of the market closest to China already reflect a lot of the “bad China” news in their prices, while the segments less directly linked to China are priced for a more perfect world, and better outcomes.

Are Chinese growth stocks now a buy?

So are China’s large-cap internet companies and other beaten-up Chinese growth stocks now a buy?

On July 15, I suggested that Chinese tech stocks listed in Hong Kong were a buy. Logically, if I liked them then, I must love them now, since they are a good -10% cheaper! Of course, since then we have learned that the Chinese government can, and will, take down any business it considers a problem. But surely the market already knew that? At least, I already knew that. So, yes, the near term is likely to prove challenging, with high volatility and the tape severely affected by the slightest rumor, and by the large numbers of investors looking to get out of Chinese equities regardless of price. But on a one-year to three-year view, building up small positions in China’s e-commerce, gaming and fintech giants should make sense. And yes, I am aware that generally the only thing one gets from picking a bottom is a smelly finger...

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.