Quote

"We think the VC model is outdated. It creates an odd dynamic between us and founders, where on the eve of an IPO they're asking if we're going to have to get off their boards and quickly distribute the stock. Why should that be the default, particularly when so much value creation happens later?"

- Sequoia Capital partner, Roelof Botha

Introduction

The modern venture capital industry, popularly referred to as “VC”, is known for leading early-stage investments in some of the most innovative ideas of the 20th and 21st century. Companies such as Alibaba, WhatsApp, Google, Twitter, Uber, Coinbase and, of course, Facebook Meta have been birthed by daring venture capitalists that often saw an opportunity before a business or vertical was established. But for an industry that’s been so successful at backing innovators, the industry itself has done very little to innovate…until recently.

In August, we ran a newsletter highlighting a shift in the European venture capital model, when several European VCs made headlines by announcing public listings of their own securities. At the time, we wrote:

The advantages of accessing deeper pools of capital – whether it be from institutional investors who prefer to invest in liquid securities or retail investors – make it possible for [European] VCs to experiment with long-term oriented models where ‘permanent capital’ allows them to be even more patient with their investment selections…

While the average investor is unlikely to gain access to deal-flow from Sequoia Capital or Andreessen-Horowitz anytime soon, the new European model cracks the door open to the possibility that retail investors might be able to access the United States VC asset class someday.

Coincidentally, one of the funds we highlighted back in August – Sequoia Capital – has recently made headlines for “blowing up” the traditional VC fund model. For those that are unfamiliar with Sequoia, the VC is one of the oldest and most successful venture capital firms in the world, backing companies that now represent roughly $3.3 trillion in combined stock market value (equivalent to 22% of the Nasdaq). Some of the companies they’ve backed over the years include Apple, Dropbox, Google, Instagram, LinkedIn, Reddit, Snowflake, Stripe, WhatsApp, Yahoo!, YouTube and Zoom.

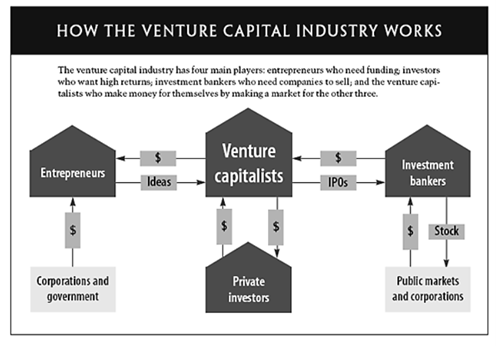

Given Sequoia’s long and successful track record in the venture capital industry, it begs the question: why “blow up” a good thing? To get to the bottom of that question, it’s important to understand how traditional VCs operate today. Structurally, today’s venture capital fund is similar to its 1970s and early-1980s predecessors. General partners (GPs) and limited partners (LPs) make up a partnership, and the fund usually makes initial investments into privately held companies over the course of two to three years. The entire life of a fund is typically seven to ten years, and the fund generally harvests returns for its investors through exit or liquidation events (such as acquisition and IPO) over the last two to three years.

However, as noted by the Harvard Business Review:

“Both the size of the typical fund and the amount of money managed per partner have changed dramatically. In 1980, the average fund was about $20 million, and its two or three general partners each managed three to five investments…Today the average fund is ten times larger, and each partner manages two to five times as many investments.”

Like the majority of the VC industry, Sequoia has operated under this model since it was founded in Menlo Park by Don Valentine in the early 1970s. However, Sequoia recently announced that it is forming a single fund – uncreatively dubbed The Sequoia Fund – to hold all of its European and US investments, including stakes in publicly traded corporations.

According to Sequoia, this fund will serve as an open-ended capital vehicle and will be the sole limited partner for all future Sequoia "sub-funds" (venture, seed, growth, etc.). Additionally, Sequoia said it plans to become a registered investment advisor, which could let it expand its investments in areas like cryptocurrencies and secondary markets. However, unlike its European counterparts, the firm has communicated to its LPs that it doesn't plan to land on public markets.

Which brings us back to the question: why “blow up” a good thing?

In Sequoia’s own words:

“For the first time, this structure means Sequoia’s partnerships can be every bit as enduring as the companies we work with. This move lets us foster deeper relationships with the principal drivers of innovation and value creation — our founders and their companies. We look forward to building lasting value with them as they realize the full scale of their ambition.”

Practicality, what that boils down to is that due to the constraints of the traditional VC model described above, the firm has been obligated to sell shares in its investments “too early” in their growth journey. One internal analysis of distributions over the past 15 years shows that had Sequoia held onto shares for another year, it would have resulted in over $8 billion in added returns. However, due to the volatility in public markets, one criticism of the single fund structure is that The Sequoia Fund’s value could be significantly impacted by stock swings.

Another consideration is whether Sequoia is attempting to change the fundraising paradigm by creating a perpetual fund that allows them to invest across a wide range of disciplines (i.e., venture capital, private equity, debt, cryptocurrencies, etc.) and that gives investors exposure to multiple asset classes. Given that a larger constituent of massive, venture-backed unicorns are staying private for longer (see our July 2019 article titled The Mysterious Case of the Elongated IPO) and may not even see an IPO/takeover as their final destination, Sequoia could view this new fund as their chance to play ball in later innings than was previously possible.

Whichever way you slice it, Sequoia’s pivot is a fundamental disruption to the venture capital model. In an industry that’s all about fast follows, rival firms are likely debating whether this long-term oriented model will be the new standard for an industry that’s largely still playing under decades-old rules. Given Sequoia’s unusually large portfolio of publicly listed companies, odds are that the disruption won’t lead to a sweeping change across the industry. Rather, it will likely stay contained to a handful of funds that want to evolve and might be able to get investors to agree to a similar structure. Then again, with its track record of successfully investing in innovative ideas over several decades, the pivot could ripple across the industry for years to come as VCs evaluate how to conduct business in the rapidly changing 21st century.

Michael Johnston

Tech Contributor

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.