“There’s less to lose sleep about now than in a long time.”

-JANET YELLEN, at her press conference last week

“The debt issuance is pretty much off the charts everywhere.”

-Bank of America Merrill Lynch’s AL MURPHY

“We can ignore reality, but we cannot ignore the consequences of ignoring reality.”

-AYN RAND

A Christmas Peril. With the Holiday Season upon us, this might seem like an odd time to launch this new version of our Evergreen Virtual Adviser (EVA) considering the subject matter. However, no one ever accused me of being normal! Yet, to show that I’m not a distant descendant of Ebenezer Scrooge (at least that I know of), I do want to point out right up front that there are attractive places to invest money these days despite the reality—to be outlined below—that Bubble-mania is fast approaching a fever pitch.

In fact, some of the intriguing investment areas stand to benefit from the eventual flushing out of excessive speculation and pervasive complacency. A case in point in our view is Chinese government bonds. China has been tightening policy, as has our own Fed. But, unlike in the US, longer term interest rates have also been rising this year. Consequently, 10-year Chinese government bonds yield 4%, denominated in its currency, which we believe is likely to be stronger than the US dollar, and most other developed country currencies over time. When the bubbly conditions end in the West, money is likely to flow toward the relative safety of China—perhaps in torrents. (We realize the bear story on China is excessive debt but, unlike in most of the “rich” world, its savings rate is “yuge”.)

We’ve made the bull case on energy securities so many times over the last couple of years that I won’t rehash that again – other than to offer a brief caveat. Unlike in the summer, when crude was depressed and negative speculative sentiment reigned supreme – leading us to predict a meaningful rally – conditions are presently inverted. Sentiment today is extremely bullish and the price has risen by around 35%. Yet, most energy issues have severely lagged and offer excellent long-term returns, in our view, once a mild correction cools off the gaggle of speculators now loaded up on the various oil-related commodities.

We also believe gold and gold miners could be poised for another early-year rally such as they have seen since the end of 2013. The average pop just in the first few months of years 2014 through 2017 has been 42%, with the lowest being 36% (in 2016 the miners went on to soar 143% by the third quarter before correcting hard; kudos to Steelhead Partner’s Mike Ridgeway for pointing this out to me). Both bullion and shares look cheap and they could benefit from the blowing to smithereens we see coming in…oops, that’s getting ahead of myself. You’ll have to wait just a bit on that one.

The Ghost of Bubbles Past. Before going further into why we believe we are experiencing the biggest bubble ever, let me provide a brief history of my contentious relationship with these peculiar phenomena. (For those of you who have heard or read this before, please feel free to skip to the end of this section.)

My first encounter with “Bubble-bursting” occurred way back in the late 1980s when I became convinced that the Japanese stock and real estate markets were absurdly overvalued. The Nikkei, Japan’s primary stock index, proceeded to double from that point. Nice call, Dave! But once the helium came out of that balloon it continued to do so for many years despite some explosive counter-trend rallies along the way. Earlier this year, the Nikkei was finally back up to where I said it was nutty in 1987! (It hit this a few times since then before consistently swooning.)

Because few of my clients had exposure to Japanese stocks, it wasn’t a make or break call (though I do remember selling Honda, Panasonic and Fanuc back then and watching them scream higher). But my next close encounter of the bubble kind was a much bigger deal.

Being based in Seattle–the twin epicenter of the tech bubble, along with Silicon Valley–made that period one of the most traumatic of my life. As the dot.com frenzy heated up to thermonuclear temperatures, I was urging clients to take profits. For the portfolios where I had the ability to implement transactions of my own volition (i.e., I had discretion), I was systematically selling down tech stocks, including many I had bought for clients during the Asian crisis of 1998 when they were absolutely crushed. Among those was Qualcomm which proceeded to rise 2600% in 1999. Unsurprisingly, many clients were incensed when they would see sell slips telling them they had sold a portion of one of their biggest winners. Making matters worse, most of the time after I had sold them, they kept on running wild.

Meanwhile, interest rates had been rising and income securities were on the ash heap. Many preferred stocks were selling at 20% discounts with 8% to 9% yields. MLPs, the operators of mid-stream energy assets like pipelines, were deeply depressed with similar yields, much like today. Even treasury bonds were offering nearly 7% yields.

It was at that point that I approached the team members I was working with at the time (a totally different set of individuals than the ones I am privileged to work with currently) about running a radio and/or TV ad, at least in the Seattle area. The message was going to be that those who had struck it rich with tech stocks should sell at least some of their holdings and buy the beaten-down income securities mentioned above. My associates at the time essentially told me I was crazy.

Frankly, I’ve always regretted that act of omission and I don’t want to repeat my lack of courage again. But, once again, I’m out-running the story. There was an even more important bubble to battle a few years later.

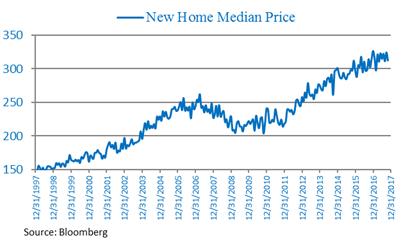

The Evergreen Virtual Adviser came into being in 2005 and a key reason for its creation was the escalating housing bubble in those days. At that point, I had left the cozy confines of a leading brokerage firm (now subsumed by Morgan Stanley) and had bought a majority interest in Evergreen Capital Management, as we were known at the time. Being outside of the wire-house world gave me the freedom to call what was happening in housing and mortgage lending for what it was: mass lunacy.

Once again, it wasn’t a popular view. For one thing, housing prices had never actually declined in the post-WWII era. To say that they might fall—and fall hard—seemed, even to me at times, ludicrous. But what I was sure of was that the incredible recklessness that was going on with sub-prime home lending and the packaging of those securities into supposedly high-grade debt securities was going to end in disaster. However, as bearish as I was on the housing market, never in my wildest dreams did I anticipate that its demise would nearly destroy the global financial system—and economy.

As we all know, central banks came to the rescue back in late 2008 and early 2009. In those days, I welcomed their radical measures to restore confidence and prevent the further collapse of asset prices. It was my belief at the time that crashing values of almost everything was the main reason the financial system appeared on the edge of extinction. In fact, I was pleading for a TARP type of program even before the US treasury clumsily brought it to life. This, combined with many other extreme interventions to stem the hemorrhaging, finally did the trick. But it was in those scary months prior to the full remedy set being implemented that this newsletter repeatedly urged investors to buy nearly anything…other than cash and US government bonds.

Over the past five years, however, I have become increasingly alarmed at what is happening. Policies that made sense during the worst of the panic have been maintained even as economies have fully recovered and the US stock market has moved up to one of its most overvalued levels ever. As the legendary Jim Grant recently wrote, “(Today’s) amazing trinity: depression-level interest rates, boomtime-level equity prices and graveyard-level volatility readings. Each observation would be singular in its own right. But the three of them together? Never before seen, as far as we know.”

The reason he doesn’t know it is because we’ve never, ever, seen this set of circumstances before.

Like yours truly, Jim Grant has been wrongfooted by how long this bubble—or set of bubbles—has been able to expand. But now it’s no longer the case of a pricey market having morphed into a very expensive market, which then evolved into arguably (and I know many will) the most surreal bull market in history. The US stock market simply doesn’t go down anymore, which is definitely not the way things are supposed to work. If you don’t believe me, please check out the below chart (by the way, it’s nearly certain December will also be green, making this the first year in market history without a single down month).

But what has really caused me to unveil the Bubble Watch EVA has nothing to do with stocks.

Scrooged again? Past EVAs have made the point, in this case inarguable, that interest rates are the lowest in recorded history. We (ok, mostly me) have further contended that this, combined with over $10 trillion of central bank faux money (yes, there is absolutely a connection), has created what we have called “The biggest bubble ever across the major asset classes of stocks, bonds, and real estate”. When money is as plentiful and cheap as it has been, people do really stupid stuff—especially when the “good times” last for so long.

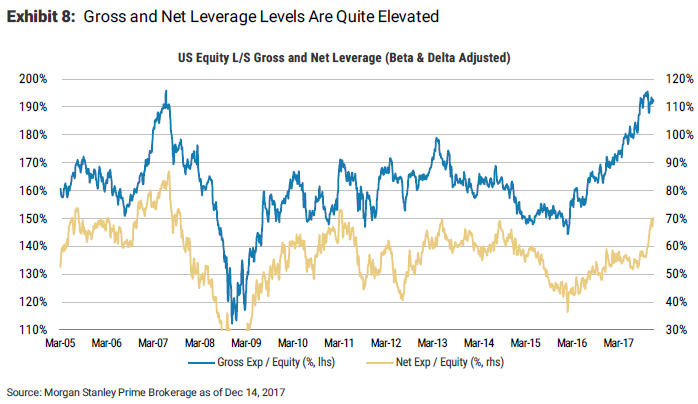

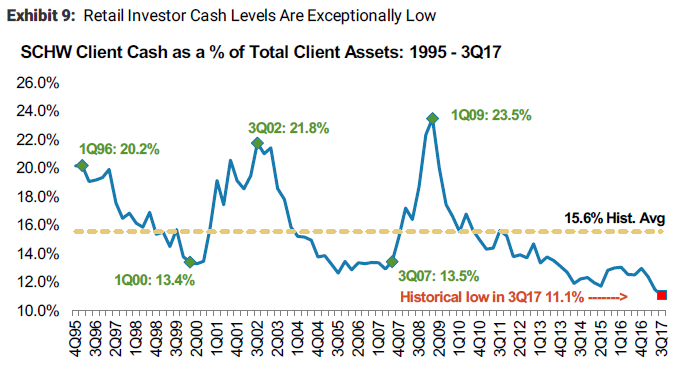

It’s hard to quibble with bonds being the priciest ever per the above. Stocks and real estate continue to have many ardent defenders. This is a topic I plan to examine in more detail through future Bubble Watch EVAs but in the meantime, please take a moment to review the below charts (the first two courtesy of Jones Trading’s Mike O’Rourke, stiletto-sharp author of The Closing Print.)

DOMESTIC FINANCIAL ASSETS TO GDP

Additionally, hedge funds are way out over their skis with leverage while retail investors have drawn their cash down to alarming levels.

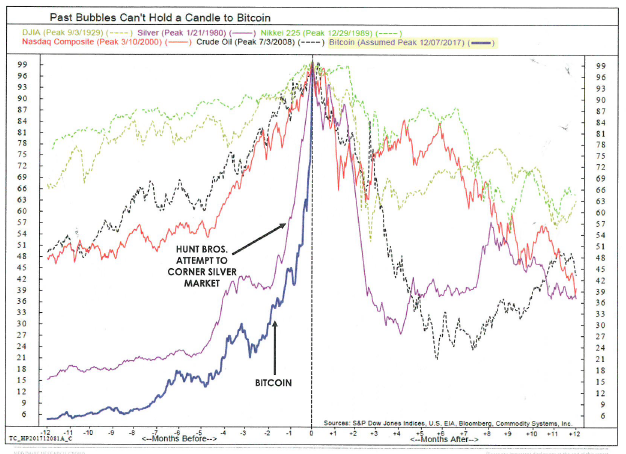

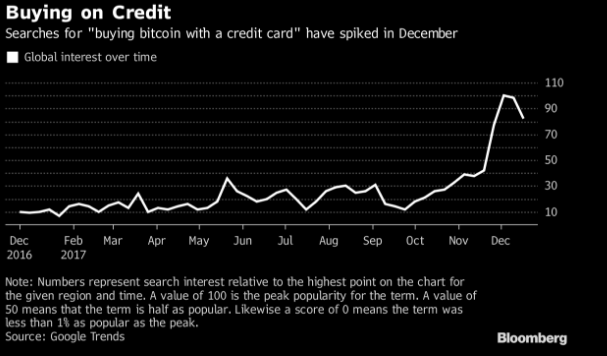

But that “biggest bubble ever” looks like something in a champagne glass compared to what’s going on with cryptocurrencies such as Bitcoin right now. We are talking about a bubble that is nearly unparalleled in mankind’s existence, possibly only rivaled by the Tulip mania 400 years ago. *

* This section was written on Wednesday, December 20th, when Bitcoin was hovering above $18,000. As of this publication date, Bitcoin has come crashing down to below $13,000, having touched as low as $11,000 intra-day on Friday.

When I hear people on CNBC explain, as they do almost every day, that Bitcoin, et al, is not a bubble I want to gently and graciously reply: “Are you kidding me?!!!” Anyone, and I mean any sane person, who can look at charts like the one above and say it’s not a total bubble is either completely delirious or someone who got in early and is egging on the newbies to create an immensely profitable exit strategy. (For example, per the New York Times, the enigmatic creator of Bitcoin is believed to have a Bitcoin stash of roughly $19 billion—if he hasn’t been dumping them into the frenzy.) The only rational way to look at something that is admittedly totally irrational is to say it’s an enormous bubble that could become even more enormous. But to deny its obvious nature is absurd.

It wasn’t long ago that I heard people downplaying the Bubble 3.0 thesis because there wasn’t anything that was truly insanely overpriced this time, as was obviously the case with tech and housing. (It’s funny how they admit that in hindsight but certainly not at the time; I’ve got the mental scars to prove it!). Well, hello the latest example of mass depravity!

Up until now, Bitcoin-mania has been a pretty fringy thing, mostly the domain of hackers, drug dealers, money launderers and other nefarious pursuits certain governments–who shall remain nameless but you can easily figure out–usually like to control. And that’s a big part of the problem: governments around the world are realizing they are losing their grip on this phenomenon.

Even usually snoozy US security regulators are increasingly expressing alarm over reports of Jane and Joe Six-pack taking out home equity lines or using their already overheated credit cards to play the cryptos.

Moreover, the mania is spreading beyond cryptos like Bitcoin and infecting the stock market. The Wall Street Journal reported last week that a Mr. Michael Poutre briefly became one of America’s richest men when his 20% ownership of Crypto Co. vaulted to nearly a $13 billion valuation. By the way, it was essentially worthless as recently as September and was at the time a sports bra designer (there must be some connection I’m missing between crypto currencies and sports bras!).

Along similarly insane lines, a microlender came public last week, opening at $6.65 before trading as low as $4.69. Two days later, the company announced the takeover of a “blockchain microlending” company (blockchain is the technology behind the cryptos). This week it traded up just a bit—a truly Bitcoin bit—to $143. (A big hat tip again to Mike O’Rourke for this gem.)

Then there are the ICOs. You may remember the IPO (initial public offering) feeding-frenzy from the dot.com days and this iteration is its wild child – initial coin offerings. With these, companies are issuing coins instead of shares. A recent ICO for a company called block.one raised $700 million in a nano-second (ok, maybe a few) and, so far, the rank speculators investors in it are thrilled. It’s market value has already zoomed to $4.5 billion. By the way, its main product, digital tokens, have “no purpose” by the company’s own admission.

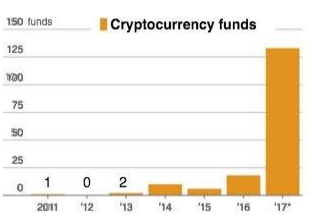

If you needed more proof this phenomenon has totally gone down the rabbit hole, there are now over 100 hedge funds dedicated to trading the cryptos. One of them—the Pantera Bitcoin Fund—is up rather robustly this year…like 25,000%. And you thought your Vanguard Growth Stock Index fund was doing well!

Source: Michael Lewitt, The Credit Strategist

Source: Michael Lewitt, The Credit Strategist

Further, the crypto craze is much more than merely an American sensation. It has gone truly global just as the tech bubble did 18 years ago. Roughly 40% of Bitcoin’s trading volume comes from Japan with other Asian countries enthusiastic participants as well. My great friend and partner, Louis Gave, who lived in Asia for nearly two decades, constantly is pointing out that Asian investors love “investments” that are going up at a 90-degree slope. Therefore, the cryptos are a dream come true for them—until it turns into a nightmare.

However, Asian regulators are a very different story. They realize the risk that this monstrous bubble poses to their financial systems. China has banned trading in the cryptos though no doubt many Chinese are taking the risk to trade it…well…cryptically.

This bubble has become so big, so fast, that even the money-for-nothing purveyors—aka, the central banks –are taking notice. And that may be the most important ramification of this latest speculative orgy. It may finally cause the planet’s monetary mandarins to realize the Frankenstein they have printed to life. It’s one thing to have stocks, bonds, and real estate priced so high as to virtually guarantee return-free risk in the years ahead but it’s quite another to have the money flowing in torrents toward a dodgy, anti-establishment “asset” like Bitcoin.

All right, that’s enough of a rant for this inaugural issue of the Bubble Watch EVA. In the months ahead (Lord, I sure hope it isn’t years!), I will provide additional updates, as the spirit moves me, on the Biggest Bubble which is beginning to take on the dimensions of a stellar Red Giant. By the way, if you didn’t know it, those always collapse. What comes next is that astronomical phenomenon known as a Black Hole and not even Santa with all of his reindeer pulling him can escape from one of those.

David Hay

Chief Investment Officer

To contact Dave, email:

dhay@evergreengavekal.com

OUR CURRENT LIKES AND DISLIKES

No changes this week.

LIKE

NEUTRAL

DISLIKE

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.