“First to mind when asked what 'the cloud' is, a majority respond it’s either an actual cloud, the sky, or something related to weather.”

– Citrix Cloud Survey Guide, August 2012

“At no other point in time has there ever been such a need for the instant availability of IT resources enabled by the cloud than during this coronavirus pandemic… the cloud will continue to be a fundamental enabler for decades to come.”

– Forbes article, March 2020

For years, the concept of ‘the cloud’ was as cloudy as a winter morning in Seattle, Washington. It seemed that only the techiest of tech people understood what the term meant and even fewer had a grasp on how the technology would revolutionize businesses, industries, and economies. The closest analogy I can think of to an emerging modern-day technology with an equally high ceiling that still confounds a lot of people is blockchain tech. But I’m going to stay away from that rabbit hole for the purposes of this newsletter… (For those interested in a quick read on the subject, please see our piece from November 2019 titled, “All In On Blockchain?”).

It took years for ‘the cloud’ to become a digestible household term, but now it’s almost inconceivable to think of the word in any other terms. In fact, if you type ‘cloud’ into Google, you won’t find any reference to the plumes of water and dust particles floating around most of earth’s atmosphere for many pages’ worth of search results. Instead, you’ll find articles on cloud computing and web links to leading cloud providers.

To underscore how rapid the ascent of ‘the cloud’ has been in business and everyday life, consider an article that Vox ran in 2015 titled, “Too Embarrassed to Ask: What Is 'The Cloud' and How Does It Work? It has nothing to do with white fluffy things in the sky.” The title is almost comical considering that only five years later nearly all of us rely on cloud-based services for at least some aspect of daily life (i.e. ordering goods from Amazon, streaming shows on Netflix, getting food delivered from DoorDash, posting on Instagram or LinkedIn, listening to music on Spotify, hailing a ride from Uber or Lyft…the list goes on, and on).

For those that utilize cloud services, but might still be a little cloudy on what the term actually means, the same Vox article mentioned above does a good job of summarizing the basic concept:

“When tech companies say your data is in the cloud, or that you can work in the cloud, it has nothing to do with white fluffy things in the sky. Your data isn’t actually in heaven or in the wind. It has a terrestrial home. It’s stored somewhere — lots of somewheres — and the network of servers find what you need and deliver it.

The cloud refers to software and services that run on the Internet, instead of locally on your computer. Most cloud services can be accessed through a Web browser like Firefox or Google Chrome, and some companies offer dedicated mobile apps.”

Covid-19: Accelerant or Change Agent?

Over the weekend, Scott Galloway, an esteemed marketing professor at NYU Stern School of Business, made a very interesting point on one of CNN’s flagship shows. During a discussion on the future of higher education, he stated, “if you think about it, Covid-19 is more of an accelerant than a change agent.” While he was specifically discussing his views on imminent changes to the higher education industry, the same thought can be applied to a number of industries – specifically, the technology industry and, even more specifically, cloud technologies.

Consider the following: prior to the Covid-19 pandemic, 17% of employees worked at-home full-time. In less than three months, the number has skyrocketed to over 50%. While this surge has undoubtedly been fueled by recent stay-at-home orders and will come back to earth as restrictions are lifted, major tech giants such as Amazon and Microsoft have told employees not to come back to work until at least October, while other big tech companies like Twitter and Facebook have told workers to stay home permanently. CEO and founder of Shopify, Tobi Lutke, tweeted the following last week, emphasizing the “remote work revolution” that’s currently underway:

“As of today, Shopify is a digital by default company. We will keep our offices closed until 2021 so that we can rework them for this new reality. And after that, most will permanently work remotely. Office centricity is over. Until recently, work happened in the office. We’ve always had some people remote, but they used the internet as a bridge to the office. This will reverse now. The future of the office is to act as an on-ramp to the same digital workplace that you can access from your #WFH setup.”

To reiterate Professor Galloway’s point, the Covid-19 pandemic is more of an accelerant than an outright change agent. Many employees in a variety of industries worked from home at least part-time prior to Covid-19, but the pandemic has fast-tracked this trend out of necessity, with implications that will last well beyond the end of the epidemic. Specifically, the remote work revolution will impact:

Aside from an acceleration in the “remote work revolution”, the Covid-19 pandemic will also create a tailwind for technology companies that sell services, subscriptions, and software rather than physical goods. As Louis-Vincent Gave, CEO of Gavekal Research, and Tyler Hay, CEO of Evergreen Gavekal, highlighted in early May, supply chain disruption will be one of the major outcomes of the Covid-19 pandemic and cloud companies will not have to spend significant time, capital, or resources to make major changes to their operations. This stands in sharp contrast to companies that manufacture and produce physical goods. These companies will likely be forced to disrupt their supply chains so that they can produce items closer to home as the result of both Covid-19 and escalating tension between the Chinese and US governments (which might intensify as we approach the November presidential election). In turn, these disruptions will raise operating costs and end-prices for consumers. Score another one for the cloud.

‘The Cloud’ in ‘The New World’

The Covid-19 crisis has led to a truly unprecedented environment for economies, markets, and societies. This ‘new world’ has hampered many industries in the short-term while providing a boon to others. The question for investors now becomes, “who will emerge from the crisis as a long-term beneficiary?” At the beginning of April, Louis Gave published a piece titled “Who Will Win the War on Covid-19?” that speaks to this question at a macro level. Looking at the question more microscopically, we believe one specific beneficiary of this ‘new world’ is the tech industry – specifically cloud tech.

Of course, not all cloud companies stand to benefit from this ‘new world’ equally. Technology companies that sell nonessential services to small- and medium-sized businesses (SMBs) will undoubtedly face challenges growing (and maintaining) revenue as SMBs cut costs and, in some cases, cease operating altogether.

Other companies will benefit greatly from the accelerated shift to the cloud. During the heat of the Covid-19 pandemic in March, Forbes ran an article stating:

“At no other point in time has there ever been such a need for the instant availability of IT resources enabled by the cloud than during this coronavirus pandemic… the cloud will continue to be a fundamental enabler for decades to come.”

Over the past few months, this need was extremely evident for virtual collaboration tools that provide the very foundation for remote work. For example, the user base for Microsoft’s Teams product jumped to 75 million active users (a 70% increase) in less than two months. In general, business productivity and collaboration software that enables virtual work will likely see lasting demand. Telemedicine, tele-education, and streaming services are other cloud services that have thrived out of necessity in the short-term, and will likely reshape how consumers think about healthcare, education, and entertainment in the long-term.

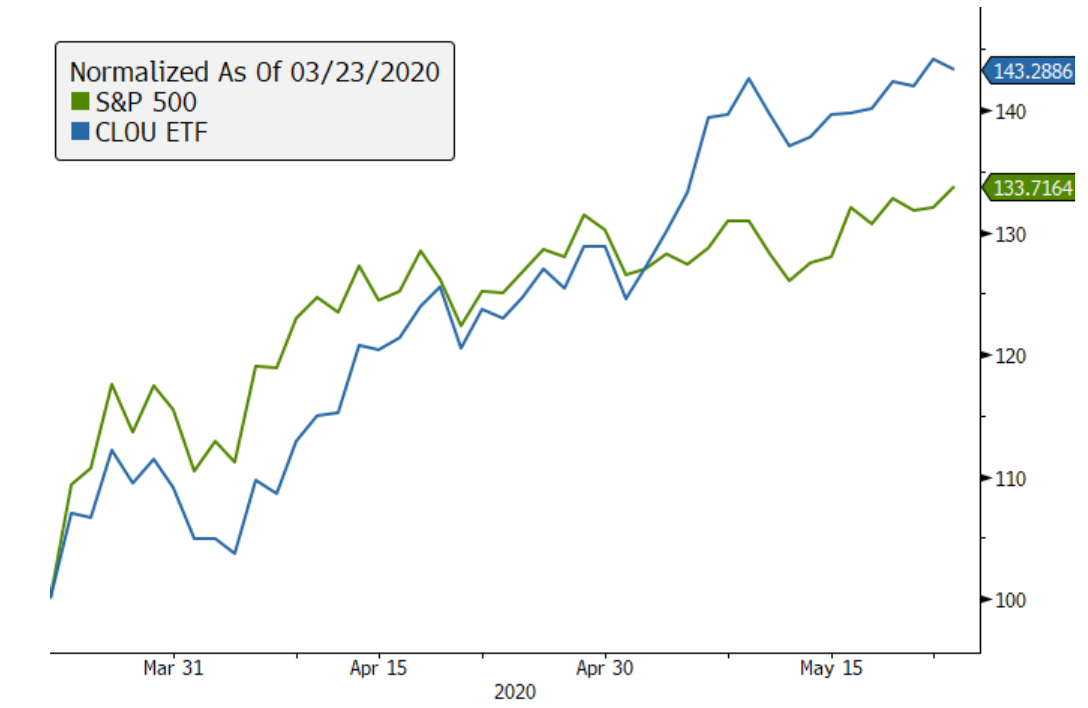

Up, Up, and Away?

The S&P 500 has risen nearly 34% since its late-March low. By contrast, CLOU (the ETF that offers equity exposure to cloud computing firms) has risen a whopping 43%.*

CLOU ETF vs. S&P 500 Since March 23rd, 2020 Low

*Source: Bloomberg, Evergreen Gavekal. As of May 26th, 2020.

Prior to the Covid-19 pandemic, “big tech” was under extreme scrutiny from regulators. However, tech stands out as one of the sectors that will likely dodge a bullet for the time being, as governments focus their attention on other sectors of the economy (i.e. health care, finance, real estate, and utilities). This is yet another godsend for several cloud and technology companies that already have the wind at their backs.

Despite these tailwinds, many publicly traded technology companies are trading near all-time highs, failing to provide investors with an overwhelmingly attractive entry point. Because of this, Evergreen believes that specific private technology investments are particularly desirable in this market environment. The future of the cloud is anything but cloudy, and we believe there are several meatball-sized opportunities in the space for investors that know where to look.

Michael Johnston

Tech Contributor

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.