"It’s not the strongest of the species that survive, nor the most intelligent, but the one most responsive to change."

-CHARLES DARWIN

POINTS TO PONDER

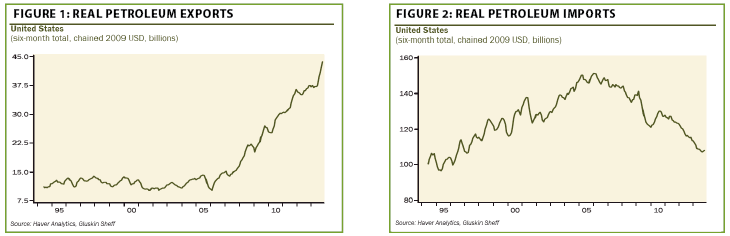

1. Although the US energy renaissance is now well known, it is nonetheless impressive to view the degree to which exports are soaring and imports are plunging. (See Figures 1 and 2)

2. The streak of highly conflicting and confusing US economic data continues. The important US ISM (Institute of Supply Managers) survey recently came out at a two-year high and yet, as one expert noted, there remains a disconnect between bouncy survey readings and "hard data" which hasn’t been all that hard (even the upwardly revised Q3 GDP was heavily driven by inventory accumulation).

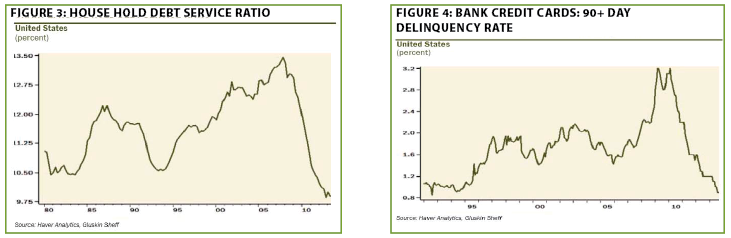

3. Despite a low official savings rate, US consumers are in good shape on the basis of both the very low household debt service ratio and a literal implosion in credit card defaults. (See Figures 3 and 4)

4. Unquestionably, the US budget deficit has improved materially in recent years. However, one of the few islands of impartial rationality in a viciously partisan Washington, D.C., is the Congressional Budget Office (CBO). It has recently issued a warning that federal fiscal deficits will start rising again as more "Boomers" draw benefits. Moreover, the CBO warns that the sequester is cutting the wrong expenditures, protecting entitlements while slashing those programs that foster long-term growth.

5. It was noted in the November 22 EVA that the Fed chairwoman nominee Janet Yellen recently conceded that the true US unemployment rate is 10% or higher. Given that almost 91 million Americans of working age are no longer in the labor force, there is a mounting risk that the US is becoming "Entitlement Nation," posing a serious long-term drag on economic vitality.

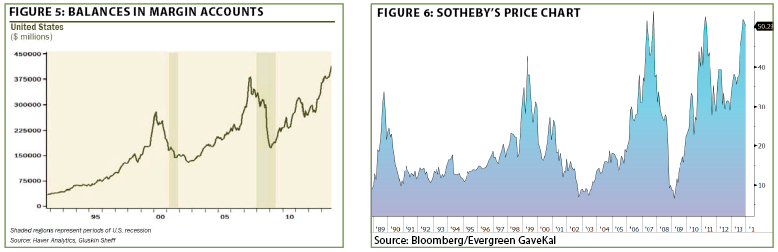

6. It could be sheer coincidence but high levels of margin debt have coincided with the last two major market tops. Also, the stock price of auction house Sotheby’s has previously given an early warning of excessive bullishness, likely because it reflects over-exuberance in high-end art and properties that often presage serious shakeouts (including ahead of the steep correction in 2011). (See Figures 5 and 6)

7. Bond bears are sure that Fed tapering, which started this week, will crush the debt markets. However, based on how much the federal deficit has dropped, at least for now, even a dramatic curtailment of Fed bond purchases will mean it is still acquiring roughly the same percentage of new government debt issuance as it was during QE2.

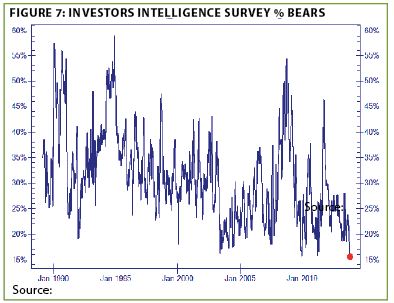

8. Another factoid that should put prudent investors on guard is that bulls now outnumber bears by 4 to 1, the highest since the fateful year of 1987. Additionally, the chart below makes it quite clear that we are witnessing a total capitulation by the bears. (See Figure 7 below)

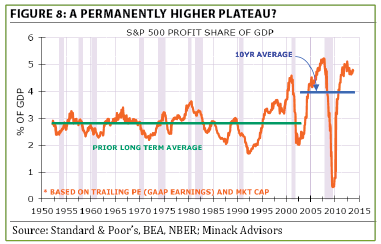

9. One of the criticisms of the cyclically adjusted P/E (CAPE) ratio is that the 2008-2009 profit atomization excessively skewed the calculation of the past 10 years’ earnings average to the downside. Yet, due to two record-breaking profit up-cycles in the last decade, the 10-year profit mean is the highest in the post-war period. Thus, if anything, the CAPE is likely understating how expensive US stocks are presently. (See Figure 8 below)

10. Last week’s EVA noted that ultra-loose monetary and fiscal policies for most of the last decade, and especially the last five years, created far more problems than they solved. Even though the popular belief is that by following extreme Keynesian economic prescriptions the rich should be hurt and the poor aided, the top 10% of Americans now control 74% of total net worth versus 71% in 2007.

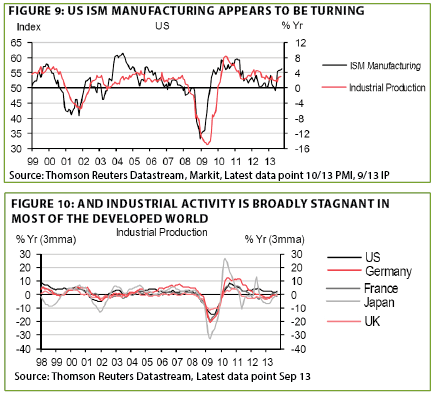

11. US manufacturing looks to be picking up strength, as does certain economic data out of China. However, industrial production around the world remains extremely subdued. (See Figures 9 and 10)

12. Contradicting the notion that Germany is an invincible industrial juggernaut, total gross fixed investment has been on a steady decline over the last 20 years, falling from 24% of GDP to 18%. Additionally, much of the improvement in its unemployment rate has been due to rapid growth in low-paying and part-time jobs. According to the Financial Times, it now has the largest percentage of workers at the bottom of the wage scale compared to national income in Western Europe.

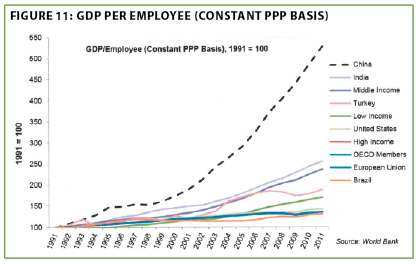

13. Despite China’s considerable challenges, which to its credit, it is forcefully addressing, its economic growth rate per worker continues to be stunningly robust. (See Figure 11 below)

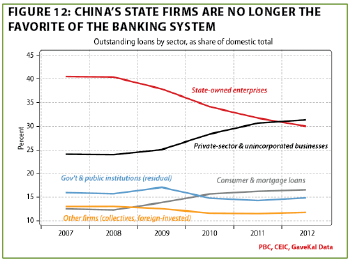

14. In another sign of deregulation and less government dominance in China’s economy, for the first time on record, loans to private businesses exceeded those to the lumbering State-Owned Enterprises in 2012. (See Figure 12 below)

15. Even as the US continues to suppress short-term interest rates, running the risk of encouraging capital misallocation (such as financial market speculation), China is allowing interest rates to be set by the free market.

Taper with a very small "t." Well, it finally happened and just in time to give investors what had been a missing-in-action Santa Claus rally. The taper is now upon us—sort of. CNBC’s Rick Santelli might have summarized it best, and certainly in the most concise way, by referring to it as simply "tuh," with the "a-p-e-r" presumably to follow at some point.

Stocks soared on the news, most likely because it was such a timid taper, yet the reality is that December is essentially flat for the S&P, quite unusual in a romping bull market. Bonds, on the other hand, certainly didn’t soar but they hung in there slightly below the 3% level on the 10-year Treasury and many, though not all, issues in the pulverized yield sector rallied sharply. But the focus of this week’s EVA isn’t on the much-anticipated taper but rather on a region that has been in lunar eclipse for a very long time.

Several years ago, when investing in Asia and other emerging markets was all the rage, a recurring EVA theme was that their over-popularity would eventually return them to their old familiar status, as in "submerging". Valuations had moved to a slight premium versus the US market, a rare occurrence over the last 15 years. Further, while the US equity market was enduring relentless outflows by disenchanted retail investors, the BRICs (Brazil, Russia, India, China), in particular, were massive money magnets.

A key linchpin of the bull story was that the developing stock markets deserved both the premium valuation and the massive inflows due to what one investment firm repeatedly called their "structurally higher growth rate". Our counter-point was that they also had a structurally higher risk profile.

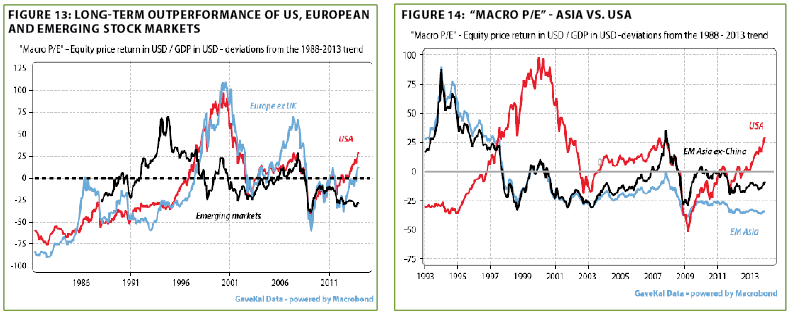

But given three years of persistent underachieving, it’s time for a serious reappraisal. Emerging markets in general have lagged the US market by roughly 50% over the last three years. Furthermore, the Asian developing markets are now trading at a discount to US stocks unseen since the bleakest days of the Asian crisis. (See Figures 13 and 14)

It’s also encouraging that the former mantra of emerging market optimists concerning the disparity between their share of global output and their market value has been totally drowned out by a ripping US stock market. As a result of the multi-year performance lag illustrated above, the gap the former bulls were so excited about is now almost a cosmic chasm. And due to what really has been faster growth, the emerging markets now produce a bit over half of the planet’s economic activity. Yet, the overall stock market value of the "rich" countries is three times that of the emerging world.

For sure, these aspiring nations have, in many cases, given investors good reason to abandon them. Governments in the former Third World often force their leading companies to take actions that are politically expedient for the ruling class but financially devastating to shareholders. A classic case in point is what the Brazilian government has done to its world-class oil company, Petrobras, by forcing it to significantly overpay to acquire offshore reserves and to use expensive domestic suppliers.

Perhaps the biggest reason, however, for the tremendous performance disparity has been the fact that the emerging market central banks have not resorted to that wonderful monetary experiment known as large scale asset purchases, more popularly referred to as quantitative easing, which now in the US, at least, appears to be in easing-off mode, though by a very modest quantity (the Fed is still creating "pseudough" at a $900 billion annual clip.)

Perhaps these countries lack the financial sophistication to realize how easy it is to generate lasting wealth with a printing press. Or maybe they remember their Econ 101 better than we do…

The high cost of free money.* Many EVA readers are aware that Charles Gave is one of my favorite economic and market mavens. Lately, he has done extensive work on the important concept of money velocity, a recurring EVA subject in recent years. It has been my oft-repeated contention that as long as money velocity was suppressed inflation would stay that way as well and the economy would limp rather than leap.

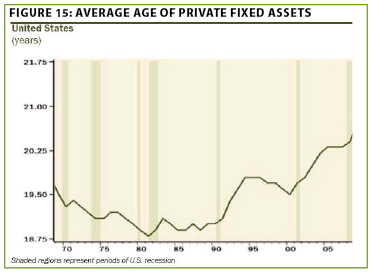

Charles has taken that issue to a higher plane by separating velocity between its financial and economic components. In his view, which recent experience seems to corroborate, having short-term interest rates essentially at zero creates an extremely elevated level of financial velocity while simultaneously repressing economic velocity. One consequence of this is that corporate America is incentivized to use low rates, especially with short maturities, to buy back stock or acquire competitors rather than add new plants and equipment, despite record-breaking profitability. That’s likely why debt issuance is running at a frenetic pace while US capital stock is the most antiquated it has been in at least 40 years. (See Figure 15 below)

Microscopic interest rates in the two- to three-year maturity range also make banks extremely wary of taking the credit risk on corporate loans, which tend to be relatively short-term. Why lend money, that may not come back, for such paltry returns? This weighs on economic money velocity as well.

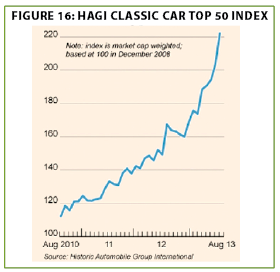

However, almost zero cost money on the short end of the "yield curve" flows freely into asset prices. Per Point to Ponder 6, high-brow art and luxury real estate markets are absolutely en fuego. This is also the case with the classic car market, as is clear from the chart above courtesy of my pal and financial newsletter scribe extraordinaire, Grant Williams. (See Figure 16 below)

One of my many gripes seven years ago regarding the housing frenzy was that all the trillions flowing into that sector did not add to America’s productive capacity. (In fact, this may well be why private fixed assets began to age rapidly per figure 15 above, starting around 2003). The same is true today. It doesn’t build enduring national wealth to pump up the prices of art, New York penthouses, Ferraris, or, for that matter, stock prices. Basically, these things aren’t investments, they are speculations and I would include "punting" on small-cap stocks and the go-go names like NetFlix in that designation given today’s hyperventilating market in these issues.

The even bigger problem, as we should all have learned by now, is that these speculative equivalents of solar flares don’t last forever and they have all ended miserably—starting with the very first one in Holland involving those little horticultural items known as tulip bulbs.

*Credit for this nifty epigram goes to none other than Charles Gave.

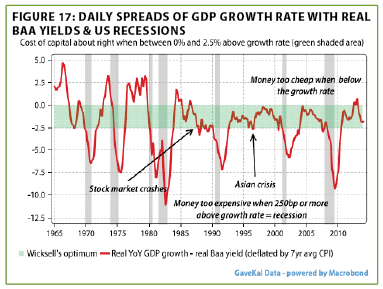

Meanwhile, for high-quality bonds with maturities of seven years or longer it’s a very different situation. The well-publicized "taper tantrum" that rocked debt markets worldwide has pushed up the long-term cost of financing. In fact, Charles Gave points out that BBB corporate bond yields are now at a dangerous point given how sluggish nominal (i.e., including inflation) GDP is presently. Should the spread between these interest rates and the economy’s growth pace widen further, this could pose a serious threat to our still tremulous expansion. (See Figure 17)

However, there is a country—and I’ve been quite critical of in the past—that is taking a most different path.

Reform with a very big "R." One of the few bubbles this newsletter managed to call without being at least a year early was the Chinese stock market mania in 2007. Somehow, undoubtedly due to absolute dumb luck, we nailed it almost to the day.

In addition to tech bubble-like valuations, we also felt China was still far too wedded at that time to its centrally-planned and excessively export-oriented economic system. It was our belief that once the real estate and lending bubble burst in the US, consumer demand for Chinese goods would plunge, with disastrous implications for their economy.

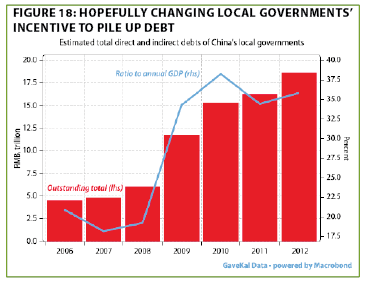

That’s pretty much how things played out, but rather than endure a long and painful recession, China opted for arguably the most extravagant stimulus program the world has ever seen. This was a major factor in ending the Great Recession, but it also saddled the Middle Kingdom with even more unneeded production capacity, most of it financed with debt issued by local governments. As a result, they made a bad situation even worse. (See Figure 18)

China also assiduously avoided making the difficult economic and policy reforms it so desperately needed, similar to the present head-in-the-sand "strategy" of US and European policymakers. That is, until recently…

GaveKal Research, being Hong Kong-domiciled, has extensively covered China’s recent Third Plenum, basically an executive summit for its most powerful politicians. Expectations going in were quite modest, but GaveKal and other China-watchers have been astounded by the radical reforms unveiled at that event.

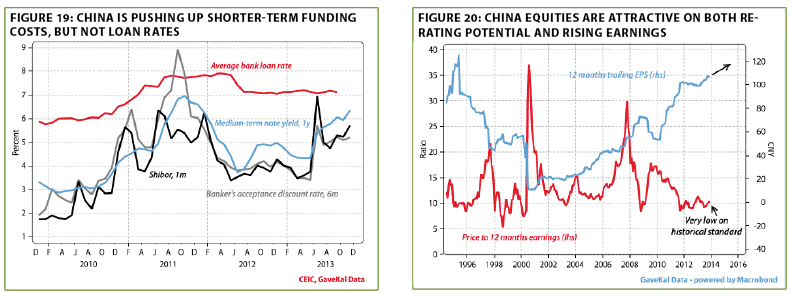

One of the more immediate and tangible results has been a further deregulation of interest rates. An overarching objective of this is to crush financial speculation. GaveKal’s Joyce Poon and Andrew Batson say it best: "Small banks and trust companies in particular have been using their access to low rates to make a range of bets—from leveraged investments in treasury bonds to high rate loans to credit-starved real estate projects. These kind of financial transactions expand banks’ balance sheets but don’t actually lead to much productive investments. To kill the incentive to engage in such financial engineering, the central bank is forcing the gap between short-term rates and longer-term borrowing costs to narrow…it has been largely successful in getting short-term rates to rise, with much less effect on longer-term borrowing costs." Figure 19 illustrates this very clearly. (See Figures 19 and 20)

In other words, China is following a monetary policy nearly 180 degrees removed from the Fed’s both in terms of allowing the market to set short-term interest rates and, of course, not relying on the fabrication of trillions of ersatz money. However, its reforms go far beyond this crucially important financial deregulation. China is also reducing the regulatory burden on the private sector (while we go the other way, big time). It is additionally relaxing the notorious "one-child" rule, eliminating forced labor "re-education" camps, and instituting sweeping land and tax reforms. Further, it is establishing free trade zones and making it easier for private companies, both internal and external, to compete with its ossified SOEs (state-owned enterprises).

Folks, this is really important stuff and I think if Charles Darwin was still kicking he’d admire China’s responsiveness to the world in which it now finds itself. Frankly, I think what it is doing is far more impressive than the halfhearted reforms occurring in Japan where the main reliance, as in the US, is on a central bank’s printing press (truly in hyperdrive in the Land of the Sinking Yen).

Of course, such radical changes to a long-standing economic paradigm are certain to produce negatives as well as positives. Growth is expected by GaveKal to be more volatile and there are likely to be a number of high-profile bankruptcies from formerly coddled state-sponsored companies that can no longer cut it against real competition. The equity market may not be a stand-out performer in the near-term. But, looking further out, this is exceedingly bullish in my mind and, more importantly, in the opinion of the GaveKal brain trust. Fortunately, China’s stock market is very inexpensive, mitigating a lot of the transition risk. (See Figure 20 above, right)

A safer way to play China’s changing landscape is with its bond market. As recently noted in these pages, it’s now possible to get 6.25% on AAA-rated Chinese corporate bonds due in five years (in their currency, the renminbi). Inflation has fallen to around 3%, meaning the real yield is most attractive, especially compared to the puny after-inflation returns available in the US, Japan, and Europe on short-term AAA-rated debt.

(Evergreen in conjunction with its partners at GaveKal has recently brought out a new mutual fund available for US investors to invest in a balanced portfolio of Asian stocks and bonds, with considerable exposure to China. This is the first time non-institutional investors have been able to access GaveKal’s investment expertise in Asia. Based on the above facts, we believe the timing is propitious.)

It’s a big world out there and US investors don’t need to feel compelled to keep most of their money in an overheated, overvalued American stock market. Despite the market’s euphoric initial reaction to the "tuh," there’s a new era starting, one that will involve much less magically manufactured money. There’s a lot of hope that economic growth can take over from the Fed. However, given our leaders’ resolute inability to institute the type of radical restructuring China is undertaking, that may be expecting much too much from an economy still under siege by its own government.

Special message: A week ago today, I had the great privilege of presenting Captain William Swenson, who was awarded the Medal of Honor by President Obama on October 15th, with an envelope containing nearly $16,000. I also had the pleasure of having lunch with him, and over the next two hours I gained even greater appreciation for the courage and integrity of this exceptional young man. He not only had to brave a harrowing 90-minute firefight in Afghanistan, where he saved numerous of his comrades, he also had to battle the US Army’s bureaucracy in order to receive his commendation. In fact, it was announced on Wednesday that the primary US commander for the Persian Gulf has ordered an inquiry into how battlefield awards are processed as a result of Captain Swenson’s difficulties and those of other decorated soldiers.

As previously mentioned in an earlier EVA, Captain Swenson has an intense passion to help other returning veterans assimilate back into "normal" life. After listening to him, I believe he’s going to create a successful program based on utilizing and further developing the skills they’ve acquired during their military careers.

Thanks to all the EVA readers, and Evergreen employees, who made this possible with their generosity and concern for one of America’s legitimate heroes!

IMPORTANT DISCLOSURES

This report is for informational purposes only and does not constitute a solicitation or an offer to buy or sell any securities mentioned herein. This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. All of the recommendations and assumptions included in this presentation are based upon current market conditions as of the date of this presentation and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. Information contained in this report has been obtained from sources believed to be reliable, Evergreen Capital Management LLC makes no representation as to its accuracy or completeness, except with respect to the Disclosure Section of the report. Any opinions expressed herein reflect our judgment as of the date of the materials and are subject to change without notice. The securities discussed in this report may not be suitable for all investors and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. Investors must make their own investment decisions based on their financial situations and investment objectives.