"A stable market breeds complacency. Complacency breeds bad investing behavior. Bad investing behavior breeds regret."

- The Motley Fool’s Morgan Housel

"Common sense is not so common."

- Voltaire

What’s that smell? If you detect a distinct odor of smoke in the air, it’s likely coming from that blazing source known as the S&P 500. This has been another year when I need to tip my hat to (and eat considerable crow over) the US stock market, which has continued to rise in a year that has been anything but smokin’ hot for a wide range of asset classes. It’s been basically all S&P, all the time--unless you were contrarian enough to buy very long-term treasury bonds at the start of the year when they were universally detested. In that case, you would have left even the mighty S&P 500 in the dust with a 30% return.

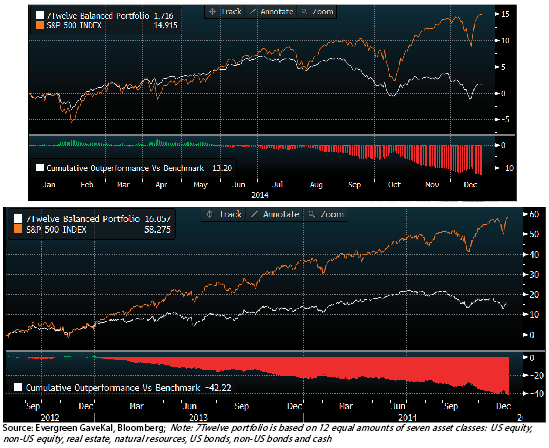

Outside of those two areas, though, it was a mixed year to say the least. US small-cap stocks have been bouncing between slightly up and slightly down this year while commodities have been an utter disaster. Those with highly diversified portfolios are having their faith tested in the wisdom of spreading the risk and mitigating volatility The two charts below, based on Professor Craig Israelsen’s highly regarded "7Twelve Portfolio," vividly illustrates the magnitude of the recent lag, despite its long-term outperformance. (Hint: it’s most likely a terrible time to abandon that historically sea-worthy ship despite a rough voyage over the last few years.)

Returning to the on-fire motif, this week’s Guest EVA is authored by my great friend and partner, Louis Gave, and it is titled "The Burning Questions for 2015." In his essay, Louis does a fine job of outlining the major forces aligning to impact financial markets next year. As you will read, some are definitely of the cooking-with-gas variety (the US dollar, the US stock market, the US economy—do you notice a pattern here?) and those that are in the deep freeze (energy, almost all other commodities, Chinese real estate, Europe, and emerging markets).

One of the key questions Louis raises is a query that Evergreen believes is among the most urgent over the next few years: Has there been a substantial misallocation of capital in the US? This might seem like a silly question with US stocks totally en fuego but,

actually, the latter stages of bull markets are typically when loosey-goosey decisions are made that will burn investors down the road. The mania for internet stocks in 1999 and the mad dash into junk mortgages in 2006 and 2007 are but two relatively recent and glaring examples. In our view, it would be the ultimate exercise in ignoring the past—and being doomed to repeat it—to assume that this boom will not have a bust trailing along in the aftermath of its frothy wake.

For now, we’ve already got a tangible illustration of that in the once equally sizzling energy sector which is suddenly fizzling. It’s likely to be soon revealed that considerable malinvestment occurred in this area, but it’s Evergreen’s belief that ill-advised investing extends far beyond the oil and gas realm. Companies buying back enormous amounts of their own stock at high prices is likely to be one of the prime instances of "silliness in extremis" when this era is viewed retrospectively. On that note, it’s interesting that stock buy-backs among energy companies have ground to a virtual halt—despite stock quotes that are "enjoying" a 40% off-sale (with Chesapeake Energy being a rare exception). Expect that same dynamic to play out in the next general bear market as it did in 2008.

Louis also considers whether his home continent of Europe is going the way of Japan; in other words, devolving into a state of perpetual stagnation. He also brings up the term "deflationary bust" which, if true, has huge implications for financial markets and the global economy. This is a theme we plan to home in on in an EVA coming to you soon.

We’ve trimmed Louis’ original piece down a bit to make it a quicker read but if you would like to see it in its entirety, please click here. Also, if you are super time-pressed, you can just skip to the conclusions on pages 7 and 8.

With that, I’d like to wish all of our EVA readers a joyous and rejuvenating Holiday Season!

![]()

THE BURNING QUESTION FOR 2015

Louis-Vincent Gave

With two reports a day, and often more, readers sometimes complain that keeping tabs on the thoughts of the various Gavekal analysts can be a challenge. So as the year draws to a close, it may be helpful if we recap the main questions confronting investors and the themes we strongly believe in, region by region.

1. A Chinese Marshall Plan?

When we have conversations with clients about China—which typically we do between two and four times a day—the talk invariably revolves around how much Chinese growth is slowing (a good bit, and quite quickly); how undercapitalized Chinese banks are (a good bit, but fat net interest margins and preferred share issues are solving the problem over time); how much overcapacity there is in real estate (a good bit, but—like youth—this is a problem that time will fix); how much overcapacity there is in steel, shipping, university graduates and corrupt officials; how disruptive China’s adoption of assembly line robots will be etc.

All of these questions are urgent, and the problems that prompted them undeniably real, which means that China’s policymakers certainly have their plates full. But this is where things get interesting: in all our conversations with Western investors, their conclusion seems to be that Beijing will have little choice but to print money aggressively, devalue the renminbi, fiscally stimulate the economy, and basically follow the path trail-blazed (with such success?) by Western policymakers since 2008. However, we would argue that this conclusion represents a failure both to think outside the Western box and to read Beijing’s signal flags.

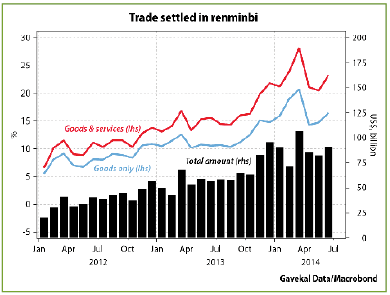

In numerous reports (and in Chapters 11 to 14 of Too Different For Comfort) we have argued that the internationalization of the renminbi has been one of the most significant macro events of recent years. This internationalization is continuing apace: from next to nothing in 2008, almost a quarter of Chinese trade will settle in renminbi in 2014.

This is an important development which could have a very positive impact on a number of emerging markets. Indeed, a typical, non-oil exporting emerging market policymaker (whether in Turkey, the Philippines, Vietnam, South Korea, Argentina or India) usually has to worry about two things that are completely out of his control:

1) A spike in the US dollar. Whenever the US currency shoots up, it presents a hurdle for growth in most emerging markets. The first reason is that most trade takes place in US dollars, so a stronger US dollar means companies having to set aside more money for working capital needs. The second is that most emerging market investors tend to think in two currencies: their own and the US dollar. Catch a cab in Bangkok, Cairo, Cape Town or Jakarta and ask for that day’s US dollar exchange rate and chances are that the driver will know it to within a decimal point. This sensitivity to exchange rates is important because it means that when the US dollar rises, local wealth tends to flow out of local currencies as investors sell domestic assets and into US dollar assets, typically treasuries (when the US dollar falls, the reverse is true).

2) A rapid rise in oil or food prices. Violent spikes in oil and food prices can be highly destabilizing for developing countries, where the median family spends so much more of their income on basic necessities than the typical Western family. Sudden spikes in the price of food or energy can quickly create social and political tensions. And that’s not all; for oil-importing countries, a spike in oil prices can lead to a rapid deterioration in trade balances. These tend to scare foreign investors away, so pushing the local currency lower and domestic interest rates higher, which in turn leads to weaker growth etc…

Looking at these two concerns, it is hard to escape the conclusion that, as things stand, China is helping to mitigate both:

Beyond providing stability to emerging markets, the gradual acceptance of the renminbi as a secondary trading and reserve currency for emerging markets has further implications. The late French economist Jacques Rueff showed convincingly how, when global trade moved from a gold-based settlement system to a US dollar-based system, purchasing power was duplicated. As the authors of a recent Wall Street Journal article citing Reuff’s work explained: "If the Banque de France counts among its reserves dollar claims (and not just gold and French francs)—for example a Banque de France deposit in a New York bank—this increases the money supply in France but without reducing the money supply of the US. So both countries can use these dollar assets to grant credit." Replace Banque de France with Bank Indonesia, and US dollar with renminbi and the same causes will lead to the same effects.

Consider British Columbia’s recently issued AAA-rated two year renminbi dim sum bond. Yielding 2.85%, this bond was actively subscribed to by foreign central banks, which ended up receiving more than 50% of the initial allocation (ten times as much as in the first British Columbia dim sum issue two years ago). After the issue British Columbia takes the proceeds and deposits them in a Chinese bank, thereby capturing a nice spread. In turn, the Chinese bank can multiply this money five times over (so goes money creation in China). Meanwhile, the Indonesian, Korean or Kazakh central banks that bought the bonds now have an asset on their balance sheet which they can use to back an expansion of trade with China…

Of course, for trade to flourish, countries need to be able to specialize in their respective comparative advantages, hence the importance of the kind of free trade deals discussed at the recent APEC meeting. But free trade deals are not enough; countries also need trade infrastructure (ports, airports, telecoms, trade finance banks etc…). This brings us to China’s ‘new silk road’ strategy and the recent announcement by Beijing of a US$40bn fund to help finance road and rail infrastructure in the various ‘stans’ on its western borders in a development that promises to cut the travel time from China to Europe from the current 30 days by sea to ten days or less overland (see Travels Along The New Silk Road: The Economics Of Power, and Blood And Bazaars On The New Silk Road). Needless to say, such a dramatic reduction in transportation time could help prompt some heavy industry to relocate from Europe to Asia.

That’s not all. At July’s BRICS summit in Brazil, leaders of the five member nations signed a treaty launching the US$50bn New Development Bank, which Beijing hopes will be modeled on China Development Bank, and is likely to compete with the World Bank (see A Chinese Bretton Woods). This will be followed by the establishment of a China-dominated BRICS contingency fund (challenging the International Monetary Fund). Also on the cards is an Asian Infrastructure Investment Bank to rival the Asian Development Bank.

So what looks likely to take shape over the next few years is a network of railroads and motorways linking China’s main production centers to Bangkok, Singapore, Karachi, Almaty, Moscow, Yangon, Kolkata (see No Bridgehead Too Far In China’s Expanding Empire). We will see pipelines, dams, and power plants built in Siberia, Central Asia, Pakistan and Myanmar; as well as airports, hotels, business centers… and all of this financed with China’s excess savings, and leverage. Given that China today has excess production capacity in all of these sectors, one does not need a fistful of university diplomas to figure out whose companies will get the pick of the construction contracts.

But to finance all of this, and to transform herself into a capital exporter, China needs stable capital markets and a strong, convertible currency. This explains why, despite Hong Kong’s pro-democracy demonstrations, Beijing is pressing ahead with the internationalization of the renminbi using the former British colony as its proving ground (witness the Shanghai-HK stock connect scheme and the removal of renminbi restrictions on Hong Kong residents). And it is why renminbi bonds have delivered better risk-adjusted returns over the past five years than almost any other fixed income market.

Of course, China’s strategy of internationalizing the renminbi, and integrating its neighbors into its own economy might fall flat on its face. Some neighbors bitterly resent China’s increasing assertiveness (see Beijing Eyes the Bay of Bengal and Perilous Seas). Nonetheless, the big story in China today is not ‘ghost cities’ (how long has that one been around?) or undercapitalized banks. The major story is China’s reluctance to continue funneling its excess savings into US treasuries yielding less than 2%, and its willingness to use that capital instead to integrate its neighbors’ economies with its own; using its own currency and its low funding costs as an ‘appeal product’ (and having its own companies pick up the contracts as a bonus). In essence, is this so different from what the US did in Europe in the 1940s and 1950s with the Marshall Plan?

2. Should we worry about capital misallocation in the US?

The US has now ‘enjoyed’ a free cost of money for some six years (see The High Cost of Free Money). The logic behind the zero-interest rate policy was simple enough: after the trauma of 2008, the animal spirits of entrepreneurs needed to be prodded back to life. Unfortunately, the last few years have reminded everyone that the average entrepreneur or investor typically borrows for one of two reasons:

• Capital spending: Business is expanding, so our entrepreneur borrows to open a new plant, or hire more people, etc.

• Financial engineering: The entrepreneur or investor borrows in order to purchase an existing cash flow, or stream of

income. In this case, our borrower calculates the present value of a given income stream, and if this present value is higher

than the cost of the debt required to own it, then the transaction makes sense.

Unfortunately, the second type of borrowing does not lead to an increase in the stock of capital. It simply leads to a change in the ownership of capital at higher and higher prices, with the ownership of an asset often moving away from entrepreneurs and towards financial middlemen or institutions. So instead of an increase in an economy’s capital stock (as we would get with increased borrowing for capital spending), with financial engineering all we see is a net increase in the total amount of debt and a greater concentration of asset ownership. And the higher the debt levels and ownership concentration, the greater the system’s fragility and its inability to weather shocks.

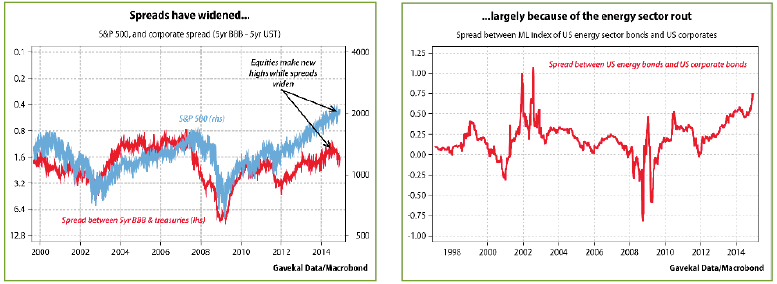

We are not arguing that financial engineering has reached its natural limits in the US. Who knows where those limits stand in a zero interest rate world? However, we would highlight that the recent new highs in US equities have not been accompanied by new lows in corporate spreads. Instead, the spread between 5-year BBB bonds and 5-year US treasuries has widened by more than 30 basis points since this summer.

Behind these wider spreads lies a simple reality: corporate bonds issued by energy sector companies have lately been taken to the woodshed. In fact, the spread between the bonds of energy companies, and those of other US corporates are back at highs not seen since the recession of 2001-2002, when the oil price was at US$30 a barrel.

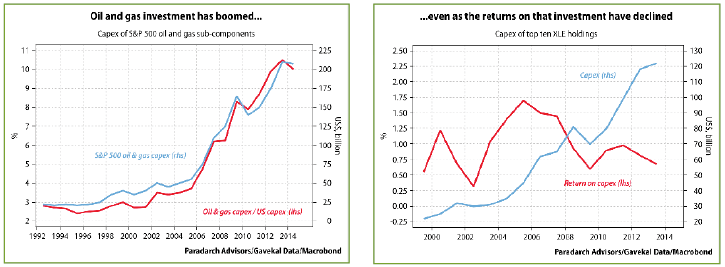

The market’s behavior raises the question whether the energy industry has been the black hole of capital misallocation in the era of quantitative easing. As our friend Josh Ayers of Paradarch Advisors (Josh publishes a weekly entitled The Right Tale, which is a fount of interesting ideas. He can be reached at josh@paradarchadvisors.com) put it in a recent note: "After surviving the resource nadir of the late 1980s and 1990s, oil and gas firms started pumping up capex as the new millennium began. However, it wasn’t until the purported end of the global financial crisis in 2009 that capital expenditure in the oil patch went into hyperdrive, at which point capex from the S&P 500’s oil and gas subcomponents jumped from roughly 7% of total US fixed investment to over 10% today."

"It’s no secret that a decade’s worth of higher global oil prices justified much of the early ramp-up in capex, but a more thoughtful look at the underlying data suggests we’re now deep in the malinvestment phase of the oil and gas business cycle. The chart titled "...even as the returns on that investment have declined" (above, right) displays both the total annual capex and the return on that capex (net income/capex) for the ten largest holdings in the Energy Select Sector SPDR (XLE). The most troublesome aspect of this chart is that, since 2010, returns have been declining as capex outlays are increasing. Furthermore, this divergence is occurring despite WTI crude prices averaging nearly $96 per barrel during that period," Josh noted.

The energy sector may not be the only place where capital has been misallocated on a grand scale. The other industry with a fairly large target on its back is the financial sector. For a start, policymakers around the world have basically decided that, for all intents and purposes, whenever a ‘decision maker’ in the financial industry makes a decision, someone else should be looking over the decision maker’s shoulder to ensure that the decision is appropriate.

This brings us to a theme first explored by our friend Paul Jeffery (see The Disruption That Could Change Banking), who back in September wrote: "In 1994 Bill Gates observed: ‘Banking is necessary, banks are not’. The primary function of a bank is to bring savers and users of capital together in order to facilitate an exchange. In return for their role as [trusted] intermediaries banks charge a generous net spread. To date, this hefty added cost has been accepted by the public due to the lack of a credible alternative, as well as the general oligopolistic structure of the banking industry. What Lending Club and other P2P lenders do is provide an online market-place that connects borrowers and lenders directly; think the eBay of loans and you have the right conceptual grasp.

Why shouldn’t we start to see banks’ high return consumer loan, SME loan and credit card loan businesses replaced, at a faster and faster pace, by peer-to-peer lending? Why should consumers continue to pay high fees for bank transfers, or credit cards when increasingly such services are offered at much lower costs by firms such as TransferWise, services like Alipay and Apple Pay, or simply by new currencies such as Bitcoin? On this point, we should note that in the 17 days that followed the launch of Apple Pay on the iPhone 6, almost 1% of Wholefoods’ transactions were processed using the new payment system.

What happens to a world that moves ‘ex-bank’ and where most new loans are extended peer-to-peer? In such a world, the banking multiplier disappears along with fractional reserve banking (and consequently the need for regulators? Dare to dream…). As bankers stop lending their clients umbrellas when it is sunny, and taking them away when it rains, will our economic cycles become much tamer? As central banks everywhere print money aggressively, could the market be in the process of creating currencies no longer based on the borders of nation states, but instead on the cross-border networks of large corporations (Alipay, Apple Pay...), or even on voluntary communities (Bitcoin). Does this mean we are approaching the Austrian dream of a world with many, non government-supported, currencies?

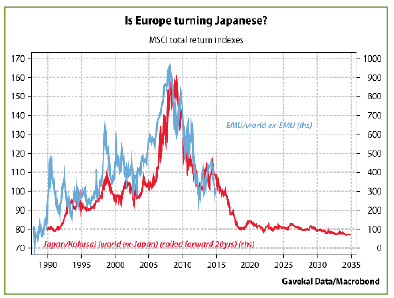

3. Should we care about Europe?

In our September Quarterly Strategy Chartbook, we debated whether the eurozone was set for a revival (the point expounded by François) or a continued period stuck in the doldrums (Charles’s view), or whether we should even care (my point). At the crux of this divergence in views is the question whether euroland is broadly following the Japanese deflationary bust path. Pointing to this possibility are the facts that 11 out of 15 eurozone countries are now registering annual year-on-year declines in CPI, that policy responses have so far been late, unclear and haphazard (as they were in Japan), and that the solutions mooted (e.g. European Commission president Jean-Claude Juncker’s €315bn infrastructure spending plan) recall the solutions adopted in Japan (remember all those bridges to nowhere?). And that’s before going into the structural parallels: ageing populations; dysfunctional, undercapitalized and overcrowded banking systems; influential segments of the population eager to maintain the status quo etc…

With the same causes at work, should we expect the same consequences? Does the continued underperformance of eurozone stocks simply reflect that managing companies in a deflationary environment is a very challenging task? If euroland has really entered a Japanese-style deflationary bust likely to extend years into the future, the conclusion almost draws itself.

The main lesson investors have learned from the Japanese experience of 1990-2013 is that the only time to buy stocks in an economy undergoing a deflationary bust is:

a) when stocks are massively undervalued relative both to their peers and to their own history, and

b) when a significant policy change is on the way.

This was the situation in Japan in 1999 (the first round of QE under PM Keizo Obuchi), 2005 (PM Junichiro Koizumi’s bank recapitalization program) and of course in 2013-14 (Abenomics). Otherwise, in a deflationary environment with no or low growth, there is no real reason to pile into equities. One does much better in debt. So, if the Japan-Europe parallel runs true, it only makes sense to look at eurozone equities when they are both massively undervalued relative to their own histories and there are expectations of a big policy change. This was the case in the spring of 2012 when valuations were at extremes, and Mario Draghi replaced Jean-Claude Trichet as ECB president. In the absence of these two conditions, the marginal dollar looking for equity risk will head for sunnier climes.

With this in mind, there are two possible arguments for an exposure to eurozone equities:

1) The analogy of Japan is misleading as euroland will not experience a deflationary bust (or will soon emerge from deflation) (this was the argument presented by François in September’s Quarterly and in Bet On Reflation, Not Deflation).

2) We are reaching the point when our two conditions—attractive valuations, combined with policy shock and awe—are

about to be met. Thus we could be reaching the point when euroland equities start to deliver outsized returns (in essence, this

is the argument Anatole presented in The Great Policy Convergence).

Proponents of the first argument will want to overweight euroland equities now, as this scenario should lead to a rebound in both the euro and European equities (so anyone underweight in their portfolios would struggle). However, it has to be said that the odds against this first outcome appear to get longer with almost every data release!

Proponents of the second scenario, however, can afford to sit back and wait, because it is likely any outperformance in eurozone equities would be accompanied by euro currency weakness. Hence, as a percentage of a total benchmark, European equities would not surge, because the rise in equities would be offset by the falling euro.

Alternatively, investors who are skeptical about either of these two propositions can—like us—continue to use euroland as a source of, rather than as a destination for, capital. And they can afford safely to ignore events unfolding in euroland as they seek rewarding investment opportunities in the US or Asia. In short, over the coming years investors may adopt the same view towards the eurozone that they took towards Japan for the last decade: ‘Neither loved, nor hated… simply ignored’.

Conclusion:

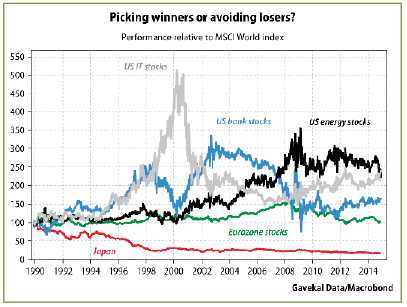

Most investors go about their job trying to identify ‘winners’. But more often than not, investing is about avoiding losers. Like successful gamblers at the racing track, an investor’s starting point should be to eliminate the assets that do not stand a chance, and then spread the rest of one’s capital amongst the remainder.

For example, if in 1981 an investor had decided to forego investing in commodities and simply to diversify his holdings across other asset classes, his decision would have been enough to earn himself a decade at the beach. If our investor had then returned to the office in 1990, and again made just one decision—to own nothing in Japan—he could once again have gone back to sipping margaritas for the next ten years. In 2000, the decision had to be not to own overvalued technology stocks. By 2006, our investor needed to start selling his holdings in financials around the world. And by 2008, the money-saving decision would have been to forego investing in euroland.

The answers to these questions will drive performance for years to come. In the meantime, we continue to believe that a portfolio which avoids a) euroland, b) banks, and c) commodities, will do well—perhaps well enough to continue funding Mediterranean beach holidays—especially as these are likely to go on getting cheaper for anyone not earning euros!

Important Disclosures

This report is for informational purposes only and does not constitute a solicitation or an offer to buy or sell any securities mentioned herein. This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. All of the recommendations and assumptions included in this presentation are based upon current market conditions as of the date of this presentation and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. Information contained in this report has been obtained from sources believed to be reliable, Evergreen Capital Management LLC makes no representation as to its accuracy or completeness, except with respect to the Disclosure Section of the report. Any opinions expressed herein reflect our judgment as of the date of the materials and are subject to change without notice. The securities discussed in this report may not be suitable for all investors and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. Investors must make their own investment decisions based on their financial situations and investment objectives.