This week’s edition of the Evergreen Virtual Advisor (EVA) is a return to one of our most popular formats, the Evergreen Exchange. This structure gives three of our team members the chance to agree, disagree, or simply comment on a topic of interest (with the constant hope that our readers care about these, too).

The theme of this issue revolves around how Wall Street often focuses more on its own best interests, frequently at the expense of its clients. Lately, “The Street” has been such a punching bag for politicians that perhaps “Everlast” should be chiseled in stone above the grand entrance to the New York Stock Exchange.

Therefore, to avoid accusations of beating a dead horse, we will endeavor to be fair in our criticisms—however difficult that may be. Also, some of our complaints are actually directed against our corner of the investment world, the so-called “buy side”, otherwise known as the money management industry.

In this Evergreen Exchange, I take a look at the long-term results of hedge funds, contrasting their modest realized returns with the utterly immodest fee structure still utilized by most of them (though we do note some positive changes underway). Then, Jeff Dicks shines his spotlight on IPOs (initial public offerings) which generate so much hype and excitement, yet, in the long run, such disappointing returns. To finish up, Tyler Hay is focusing on the rip-off known as closet indexing, basically paying high fees to receive an index fund in drag.

As we often do with our Exchange issue, we are asking readers to select which case was made most persuasively. We would greatly appreciate it if you’d take the time to submit your vote. Thank you!

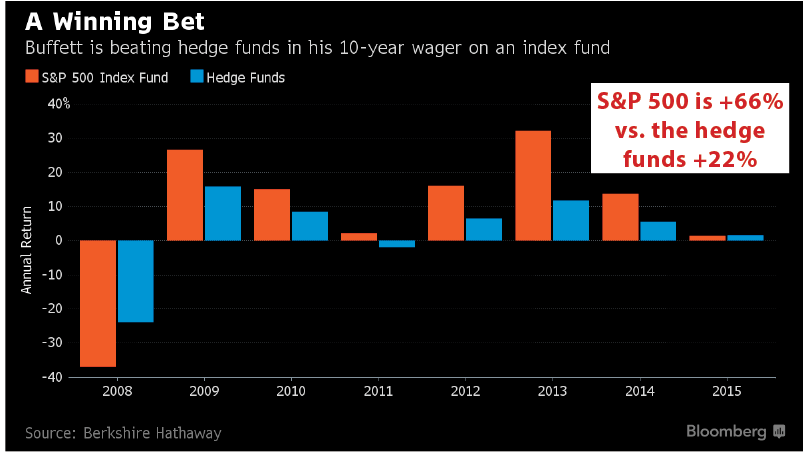

“I was willing to bet that the Vanguard S&P index fund would beat five hedge funds picked by experts over 10 years.”

-WARREN BUFFETT, at this year’s Berkshire Hathaway annual meeting, referring to a million-dollar wager he made in 2007.

Long-time EVA readers know that I love to quote Buffett. However, it’s Warren who’s been my go-to quipster, not Jimmy. Yet, for this issue I think the latter’s indecisive musical musing is much more relevant.

Regular EVA-teers also know that I am no fan of hedge funds (by the way, nor is the Omaha-based Buffett). In fact, at an investment event in late 2014, where I was jousting with two other chief investment officers from local competitors, I incurred the wrath of one of them by being highly critical of the hedge fund (HF) model. And I am the first to admit a certain sense of schadenfreude over the fall from grace hedge funds have suffered after having been ridiculed at times by some of our competition because we have steadfastly kept Evergreen clients out of them.

If you haven’t noticed, the adverse news has been coming at the hedge fund community at a fast and furious pace recently. Perhaps the most damning indictments have come from some of the iconic members of this rarified world. At this year’s signature hedge fund confab—the SkyBridge Alternatives Conference—Leon Cooperman, one of the marquee names in this space, was quoted as saying: “The hedge fund model is under challenge. It’s under assault.”

Short-selling hedge fund superstar Jim Chanos (among the limited number of survivors of that dark art) told the SALT attendees: “Fees are too high. I’m surprised they’ve stayed this high for this long.”

Even more disturbing for devotees of this structure was the observation by a spectacularly successful young Turk of the hedge fund world, Dan Loeb: “There is no doubt that we are in the first innings of a washout in hedge funds.”

But what must have caused nearly every hedge fund operator to quake in his Gucci loafers--or Jimmy Choo pumps--was a statement by Roslyn Zhang who runs alternatives for China’s Sovereign Wealth Fund (globally, the second largest investor in this area): “I’m sort of disappointed with the performance, to say the least, of the industry.”

Perhaps the most vexing aspect about hedge funds has been their results during periods of market stress. One of their big selling points was downside protection, possibly even negative correlation (meaning, if the market went down, a well-positioned hedge fund might actually rise a bit).

Yet, as you can see below, they have had a tight linkage with the direction of the S&P 500, particularly during 2008’s ultimate “stress-test”, when the hedge fund index fell 23%. Yes, that was better than the S&P’s 37% crash but it was still a very painful “drawdown”, causing many, including this author, to ask: “Where the hedge?” (in tribute to that old Wendy’s TV commercial, for all you old-timers like me out there). In other, less draconian market declines since 2008, the overall hedge fund index has continued to struggle.

Source: Evergreen Gavekal, Bloomberg

Source: Evergreen Gavekal, Bloomberg

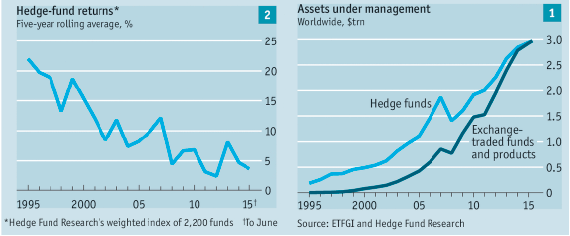

Further, this performance deficiency, at best, has been going on for years. Per the below chart from The Economist, you can see that hedge fund returns have been in a grinding bear market since the mid-1990s. But what’s even more remarkable is the continuing rise, until very recently, in their assets under management (AUM).

Source: The Economist

Source: The Economist

Clearly, the preference of primarily institutional investors for a vehicle which allegedly provides decent returns with reduced downside has been strong enough to overlook some serious over-promising and under-delivering. This is all the more stunning given the typical fee structure: “2 and 20”. What this means in English is that most hedge funds charge a minimum 2% of asset value plus 20% of the profits over a “hurdle rate”, say, 8%.

In days of yore, when these masters of the universe were pumping out 20%-type annual returns, few were begrudging them their lavish compensation. A few did so well as to become billionaires in their own right. But it’s a far different matter to be charging 2 and 20 when, in aggregate, returns have shrunk to the 5% range. Infuriatingly, the top 25 hedge managers “earned” $11.6 billion in compensation in 2014, despite the hedge fund universe producing a paltry 3% that year, far below the S&P.

Another rather unappealing trait is the tendency of far too many hedge funds to do splendidly for years and then blow-up in a space of weeks. The high leverage many hedge vehicles employ is no doubt a prime reason they can vaporize almost instantaneously.

For the reasons just mentioned, among others, Buffett the elder, as in Warren, famously bet against a carefully chosen group of hedge funds back in 2007, per the quote at the top. In case you were curious how this is turning out, the following table gives you the latest results.

Consequently, some of the largest institutional investors have announced deep reductions in their hedge fund allocation. In the case of one of the biggest, CalPERS*, it is slashing its exposure by 40%.

Lest you think it’s “I told you so” time, I’m beginning to have a Jimmy Buffett moment. Despite the ferocious negativity that is mounting toward this very large corner of the investment world, I feel moved to offer up some defense. Before I do, though, I want to reiterate that I think the present fee structure—given a financial landscape nearly devoid of decent, much less high, returns—is unconscionable. It truly does amount to a collective fleecing of the underlying investors (or should they be called “sheeple”, people who behave like sheep and deserve to be sheared?). There’s simply no question a fee-structure reset needs to occur. In fact, this seems to be underway, mostly due to pressure from the institutions that have belatedly woken up to the inequity.

Thus, there’s no question a fee-structure reset needs to occur. In fact, this seems to be underway, mostly due to pressure from the institutions that have belatedly woken up to the inequity.

Beyond what should be much better affordability, another longer-term advantage is likely to come from a far smaller footprint. There were, unquestionably, way too many hedge funds, with way too much money, chasing an ever-shrinking pool of attractive ideas.

But now, with an accelerating shift of assets into passive (i.e, no-think) strategies like index funds, this dynamic should gradually shift back in favor of investors who actually do research (with the emphasis on “gradually”). And few investment entities can match the intensive investigations done by hedge funds. After all, it was several intrepid hedge fund managers who were behind “The Big Short” of sub-prime mortgages. These hardy souls were willing to fight the consensus view on Wall Street that housing wasn’t a bubble back in 2006 and short the bejesus out of the caca the Street was pumping out to the rest of the unsuspecting investing populace (including almost every major bank!).

Now, brace yourself for another one of my far, far out-on-a-limb predictions: I believe a few select hedge funds will once again generate enormous profits for their investors. It’s my contention hedge funds will be among the few vehicles to capitalize on what is almost certain to be The Big Short 2.0—the coming bloodbath in government bond markets. Before you send me flame mails about Evergreen holding a significant position in US treasuries, which we do, let me clarify that we believe it’s the Japanese and European government bond markets that are most at-risk. And we also don’t believe this is a near-term event, though it’s always possible tomorrow could be when the pin meets the bubble.

Warren Buffett’s favorite journalist, Carol Loomis, once penned a scathing Fortune article on hedge funds. It’s fair to say she was just a bit ahead of her time since she wrote this back in 2003 and hedge fund assets went parabolic after her unflattering critique. My point is that the rumors of this industry’s demise have been greatly exaggerated in the past. Hedge funds will survive and the best will flourish by being able to capitalize, through targeted short sales, on the pervasive insanity we are seeing in so many asset prices today. If the era of riding on the coattails of central banks—which has made blindly buying and holding passive index funds a no-brainer (literally!)—is nearing its sell-by date, it might be time for many of these formerly shining stars to glitter once again.

David Hay

Chief Investment Officer

To contact Dave, email:

dhay@evergreengavekal.com

*The California Public Employees’ Retirement System

“It’s almost a mathematical impossibility to imagine that, out of the thousands of things for sale on a given day, the most attractively priced is the one being sold by a knowledgeable seller (company insiders) to a less-knowledgeable buyer (investors).”

–WARREN BUFFETT, referring to new issues.

“It is clear that buying IPOs, like buying lottery tickets, is a losing long-term strategy.”

–JEREMY SIEGEL

Initial public offerings (IPOs), also known as “new issues”, have always carried a distinct appeal to investors. This could be attributed to the idea that you are getting in early on a company. Or perhaps it’s because these offerings tend to occur in the best-performing industry at any given time (think internet stocks in the late 90s). As a quick refresher, an IPO is the process where a privately-held company transitions to a publicly-traded company by offering its shares to the public. As a result, this is the first opportunity, outside of private equity, investors have to invest in the company. But, should these deals really carry such a positive aura? The truth is IPOs as a group have been chronic underperformers. The number of offerings also tends to occur in bunches late in economic and/or industry cycles, which is usually the worst possible time to invest capital. Lastly, these offerings carry very high placement fees. For all these reasons, I believe one of the biggest scams on Wall Street is investing in IPOs.

In terms of performance, one of the most comprehensive studies of IPO returns was conducted by legendary Wharton professor Jeremy Siegel. Professor Siegel examined thousands of individual stocks that went public since 1968 and analyzed their returns through 2003. His study found that 80% of these companies underperformed the broad market and on average trailed by a staggering 2-3% per year. Moreover, out of the 80% that lagged, half of those companies underperformed the market by an inconceivable 20% per year! Sure, there are individual companies that are massive success stories, but in general the group performance has been shockingly poor.

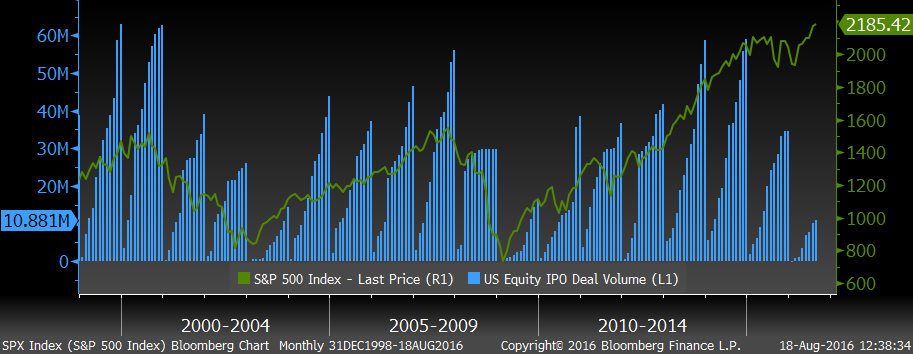

We think there is a very good reason for this chronic lag. As Warren Buffett’s quote indicates, insiders know radically more about their companies compared with individual investors. That’s why insider trading is illegal. When taking a company public, though, it’s perfectly legal to sell shares at absurdly high prices. In fact, it’s management’s job to raise the most capital for private shareholders. And, in most cases, those same execs are private owners themselves. It’s should be no surprise, then, that they are looking to sell high. It also shouldn’t be a shock that these events tend to happen late in economic cycles when stocks are at the high-end of their range. As you can see in the chart on the next page, this is exactly the case. IPO’s spiked during the late ‘90’s. They also were much higher from 2004-2007 compared with 2001-2003. Both of these surges occurred leading up to major market meltdowns. Another key point to note is that during each downturn IPO volume fell off a cliff. This would have been the best time to be a buyer of IPOs, or stocks in general, given valuations were depressed. This clearly shows why there is an inherent conflict of interest embedded in the IPO market.

US EQUITY IPO VOLUME AND THE S&P 500 Source: Evergreen Gavekal, Bloomberg

Source: Evergreen Gavekal, Bloomberg

Finally, there are absurd expenses embedded in the placement of IPOs. The bank who underwrites the deal receives a fixed percentage of the dollar amount of securities sold. This works out typically to around 7% according to prominent legal firm Morrison and Foerster. To be fair, the underwriter does take on the risk of not being able to place the full amount of shares. Additionally, that firm no doubt has significant contacts on the “buy-side” (basically, the money management community), which makes their job a critical one in terms of generating necessary demand. However, a fee based on the dollar amount of securities sold incentivizes the investment bank to sell at the highest possible price. This adds even another layer that puts the buyer at a disadvantage.

In a nutshell, IPO investments continue to be one of the mystifying areas within financial markets and, as is so often the case, cognitive biases—such as the latent human desire to get into something “hot” —appear to have led to irrationality. These deals continue to garner significant investor attention despite their notably underwhelming results. If you look back at the chart on page 3, you can see that deal volume has once again picked up late-cycle (though one could reasonably note that perhaps 2014 was the peak of this up-phase despite the nominal new high in the S&P 500 since then)*. It’s also worth noting, for publicly-traded companies, the number of insiders buying stocks, according to John Mauldin, have decreased 44% over the last 12 months. Both of these are concerning and have previously been clear warning signs that trouble is likely lurking ahead for stocks.

Jeff Dicks, CFA

Portfolio Director

To contact Jeff, email:

jdicks@evergreengavekal.com

*As we have also observed, the broader market measure, the NYSE composite, did top out in 2014.

“There’s been far, far, far, more money made by people in Wall Street through salesmanship abilities than through investment abilities.”

-WARREN BUFFETT

Wall Street’s reputation in the eyes of the average investor is, shall we say, less than sterling. In fact, if we played a word association game with Wall Street, popular descriptors would likely be: greedy, liars, thieves, vultures, etc. Thanks to the infamous Ponzi scheme of Madoff, the abuse of lending by the big banks, Enron’s account scandal, countless insider trading events, and many other nefarious incidents, Wall Street’s approval rating might be the lowest in its history.

However, the egregious behavior described above is nowhere near the biggest crime perpetrated on investors. This is because all the offenses occurred against a backdrop of increasing regulatory oversight. Unfortunately, based on the lax enforcement, it was more like the other definition of oversight—as in, an unintentional failure to notice. The SEC tries to prevent fraudulent schemes. The Federal Reserve and other government agencies attempt to regulate bank behavior. Accounting standards exist to prevent companies from cooking the books.

The biggest bilkings, though, tend to occur because no one is looking for them. In this regard, the most disturbing trend affecting investors is the many managers who are turning to closet indexing and depriving their clients of future return. Closet indexing is the practice of building portfolios, which will closely track their benchmark index without exactly replicating the index.

Imagine you hire a tailor to build you a custom suit. You’re willing to pay a premium over department store prices because you expect him to painstakingly craft a garment designed to meet your exact specifications. Later, you come to find out he skips down to the nearest store, buys one off the shelf, and makes a few minor adjustments. This is analogous to the closet indexing many managers are employing.

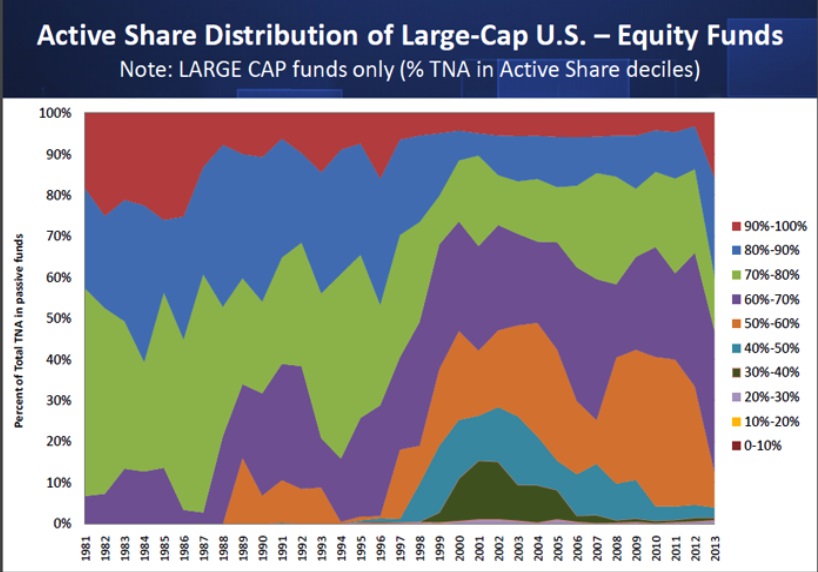

There’s an investing term, known as “active share”, coined in a research paper by Martijn Cremers and Antti Petajisto that was published in 2009. (No, the spelling of their first names are not typos.) They created a grading scale between 0-100 that tells how “custom your suit is”—or how unique is the portfolio your money manager has designed. (Any investment manager can easily calculate the amount of active share in your portfolio in minutes, a good question for all investors to ask.) The study concluded that if an investor’s portfolio was made up of too many securities also found in the benchmark they would experience very similar results. Therefore, in order to generate returns different from your benchmark you must own a portfolio that is meaningfully distinctive(the study found scores under 60 to be “closet indexers”, and deemed scored over 80 to be “active”).

We have now established that an investor must be willing to depart from rhythm of the benchmark if they expect to outperform. At times, this will inevitably lead to periods where active managers do worse than the benchmark, so, contrary to popular belief, underperforming periodically is a required step in the outperformance process! To support this notion of underperformance leading to outperformance, I recently came across an interesting statistic from the bright managers at Oakmark Funds who figured out that they underperformed the benchmark in 80% of the quarters over a 10-year period. Intuitively, one may assume this means that they probably had poor results. But in fact, their cumulative return over the period was 74% versus the benchmark of 15%.

How important is making actual portfolio bets to outperformance? The study I mentioned found that funds with very high active share outperform those with low active share by 1% annually. Simply stating that managers who are hugging their benchmarks and skimming unwarranted fees from clients doesn’t alone make a convincing argument that closet benchmarking is the biggest crime on Wall Street. To solidify this argument, we need to examine how widespread this practice has become in the industry. According to their study, in late 2008 nearly 1 in every 3 supposedly actively-managed US Large Cap mutual funds was closet indexing. In 2001, just prior to the tech blow up it was over 45%! That means, at one point, nearly half of the entire US Large-Cap mutual fund industry was taking a fee from clients who had virtually no chance of outperforming. Let’s use 2008 to put this in dollar terms. In 2008, the total assets managed by the mutual fund industry was $9.6 TRILLION. If we assume an average fee of 1% based on the amount of assets in Large Cap mutual funds ($3.2 trillion) at the time investors paid mutual fund companies over $100 billion in completely undeserved fees that year alone! (33% * 3.2 trillion * 1% = $105.6 billion)

Source: Martijn Cremers Professor of Finance University of Notre Dame

Source: Martijn Cremers Professor of Finance University of Notre Dame

I’ve included a histogram that captures the ebb and flow into and out of closet indexing over the last 20 plus years. Recall, funds with a score below 60% are considered closet indexers. Mutual funds with a score above 80% are considered “active.” (I want to remind readers that active doesn’t relate to the turnover of the portfolio, instead it represents the level of dissimilarity between a portfolio and its benchmark.) As I said earlier, the peaks occurred in 2001-2002 and in 2008. To be fair, since the great heist of 2008 the egregious offenders, those with scores below 60%, has shrunk fairly dramatically. The bulk of mutual funds today now operate in the grey area. They aren’t closet indexers but most still aren’t willing to stick out their necks and deviate significantly from their benchmark.

Even if overt closet indexing has eased, a more subtle form remains solidly entrenched. This means investors continue to pay high fees for what are essentially “me-too” vehicles. How come? Some of the blame lies on Wall Street for taking undeserved fees. However, investors deserve some of the blame. As investors have become increasingly benchmarkfocused and short term oriented, many managers have figured out that clients can only stand deviating from their benchmark if it means beating it. No manager beats it all the time, not even Buffett!

The reality is that it can take time, patience, and discipline to finally see success as an investor. As a firm that manages money and runs portfolios with an extremely high active share, in our core portfolios, we can sympathize with the discomfort that comes with this approach. Despite the hardship it brings at times, we remain convinced that if we are charging a fee, we better earn our keep. Last year, for example, energy was a big drag on portfolios. Some portfolios lagged their benchmarks and we heard about it. Instead of selling our energy exposure to look more like the benchmark, we did the opposite and added to it, something over which clients also expressed some concern. Yet, it’s a good thing we did this as many of the depressed energy names of last year are strong performers this year.

Another contrarian benchmark bet occurred last year as we took an increasingly overweight position in longer-term treasury bonds. Some clients called to complain that anything paying only a 2% yield couldn’t possibly be a decent investment. Thankfully, it turned out to be more than decent as the US 10-year dipped below 1.5%. This call and other good ones have allowed 2016 to be as gratifying as 2015 was painful. It is extremely difficult attracting clients who understand this approach—and who literally buy into it—but it’s an essential piece of successful investing. We try very hard to identify clients who have the disposition for success, which, frankly, isn’t the norm. They are willing to underperform occasionally because, like us, they understand that without being wrong, or, at least, different, you will never be right.

TYLER HAY

Chief Executive Officer

To contact Tyler, email:

thay@evergreengavekal.com

Cast your vote for who makes the most compelling case.

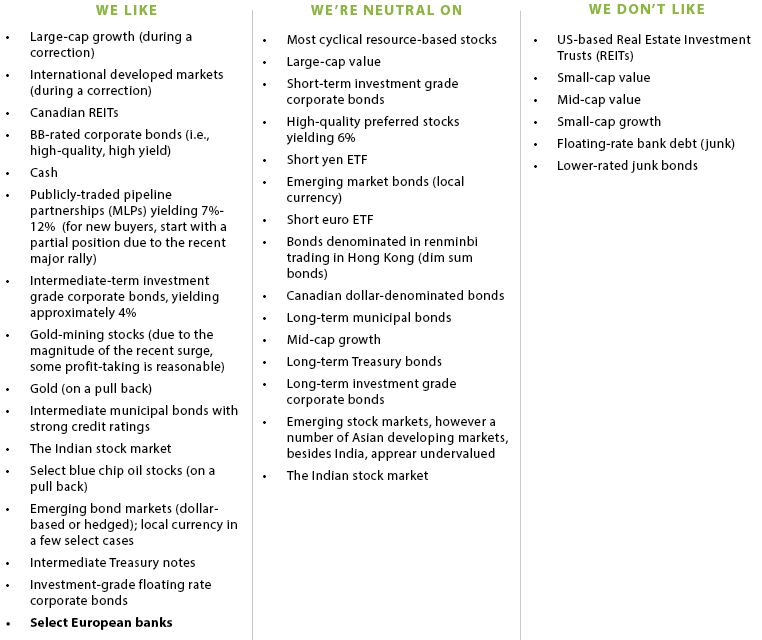

OUR CURRENT LIKES AND DISLIKES

Changes in bold below.

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness.