“We don’t see things as they are, we see them as we are.” -ANAIS NIN, essayist

“Education is a civil defense against media fallout.” -MARSHALL MCLUHAN, philosopher

Our partners at Gavekal have long written about the four key quadrants of investing:

1) Inflationary booms (mid-1960s to early 1970s)

2) Inflationary busts (mid-1970 to early 1980s)

3) Disinflationary booms (mid-1980s to late 1990s)

4) Deflationary busts (1930s, 2007 to 2009).

Of course, it’s always a lot easier with hindsight to look back and make those determinations. Currently, though, the financial markets are taking their cue from the Trump election and decisively voting for the inflationary boom scenario. This is a function of Mr. Trump’s campaign promises regarding massive tax cuts and infrastructure spending. It’s quite possible, though, that markets are getting way out over their skis—with some serious moguls up ahead.

-Financial markets have reacted to the Trump election at the speed of light in a vacuum. Infrastructure and financial stocks have been big winners; nearly everything yield-related has been hit hard. Bonds in particular have been slammed.

-The markets may be running ahead of themselves especially in making assumptions about the positive impact from a large-scale infrastructure program. These have notoriously long-lead times and many will likely produce fierce local opposition.

-As bond prices tumble, yields automatically rise. A market rate increase of this magnitude poses a threat to the global economy. In the US, the third quarter GDP looked superficially healthy. However, adjusting for a surge in soybean exports to China and a rise in already high inventories, the growth rate was a limp 1 ½%, consistent with recent years.

-Gavekal’s Charles Gave and Will Denyer have been growing increasingly concerned about a US recession in 2017. The significant rise in bond yields is making them even more wary.

-On the positive side, some important US data—like consumer spending—has been better than expected of late. Also, the critical leading indicator of credit spreads is benign currently.

-There may be a “yuge” tug-of-war brewing between Mr. Trump’s proposed pro-growth policies and the immediate smack-down from the increased cost of capital. (Housing and autos may be particularly vulnerable.)

-Another instantaneous impact is the US dollar. Higher rates have pushed it up sharply and it may be in the process of breaking through prior important resistance (roughly 100 on the dollar index). An expensive dollar hurts the competitiveness of US exporters and it also reduces the value of overseas profits for American companies.

-Rising rates and a stronger dollar also wreak havoc in emerging markets (EMs). Problems in EMs were a prime factor in the market breaks in August of 2015 and again early this year.

-Team Trump seems to be aware that it’s essential to have a proper cost of capital. It also likely realizes getting there is almost certain to be painful. Consequently, it may seek to incur the pain early in their presidential term.

-Monetary policies of the last eight years have led to a remarkable increase in the value of stocks, bonds, and real estate, despite the weakest recovery on record. Moving away from “money for nothing” might reverse the effect: hurting asset prices, while helping the economy’s long-term growth potential. Initially, though it will be a difficult not to have weak markets feed back into the economy.

-Trump’s mercurial personality and constantly “evolving” views make it hard to know what is real and what is Memorex. However, he does seem serious about moving away from conditions that have created “a big fat bubble”, as do his key economic advisers.

(Too?) Great Expectations. While most residents of the planet earth were still reeling from last week’s election stunner, the financial markets wasted no time in picking winners and losers. Among the former were financial and infrastructure-related stocks. The latter category was made up of pretty much everything yield-oriented, with the fortunate—for Evergreen—exception of mid-stream energy securities (master limited partnerships, aka, MLPs).

The moves in construction-based and financial stocks were truly breathtaking.

Source: Evergreen Gavekal, Bloomberg

Source: Evergreen Gavekal, Bloomberg

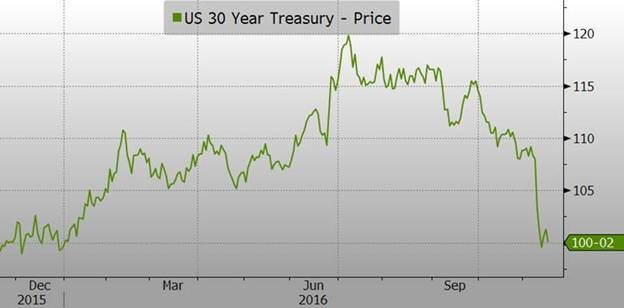

The logic for infrastructure shares is pretty straightforward, though, as we will discuss in a bit, perhaps a bit unrealistic. For financial stocks, it’s somewhat more complex in that they often weaken when bond prices get hit. And, as you can see below, bonds have been slammed like a Bubba Watson drive.

Source: Evergreen Gavekal, Bloomberg

Source: Evergreen Gavekal, Bloomberg

But in the bizarre world of zero and even negative interest rates, financials are perceived to be major beneficiaries of rising rates and, particularly, a steepening yield curve (where longer rates rise more than short rates). This is because banks borrow short-term and lend long-term. Thus, what we’ve seen lately, with longer rates zooming and short rates staying anchored by the Fed, is a dream come true for the Jamie Dimons of the world. (Intriguingly, rumors continue to swirl that Mr. Dimon will be offered the position of Treasury Secretary, despite being a life-long Democrat and an icon of Wall Street, the world’s biggest “venal” colony.)

Regarding infrastructure plays, President-elect Trump’s “yuge” proposed numbers for replacing bridges, rebuilding airports, constructing pipelines, etc., has been an obvious and powerful catalyst for their share prices. As a long-time proponent of a “Domestic Marshall Plan”, I’m pleased to see so much momentum building for such a program.

Yet, I think it’s important to be realistic about how soon the benefits will accrue, either to rectify the long degradation of the facilities themselves or to benefit the economy. During and right after the Great Recession, my plea was to put the legions of unemployed construction workers idled by the residential and commercial real estate bust back to work on infrastructure projects that apolitical experts deemed to have the highest societal benefit. But those laborers are, for the most part, back building homes, or they’ve moved on to other occupations, or they’ve retired. Some of those formerly toiling in the construction trade have returned home to Mexico and we know how hard it’s going to be to get those folks back! According to Bloomberg, we now have the lowest level of unemployed construction workers since 2000.

But the bigger road-block, pun intended, is almost certain to be that wonderful American tradition of NIMBY: Not In My Back Yard. To build out major projects in the US these days requires running a regulatory approval gauntlet that would intimidate Robert Downey, Jr., in full Iron Man attire. Additionally, the opposing litigation that occurs, often even after the myriad regulatory bodies sign off on large-scale projects, is another significant impediment.

A case in point is the Tappan Zee Bridge that straddles New York’s Hudson River. It was built back in the early 1950s during the Korean War when there was a shortage of construction materials. Accordingly, it was only supposed to last 50 years at the time it went into service in 1955 (which is, coincidentally, when yours truly did as well).

By 2008, the powers-that-be decided it was time to quit pushing their luck and hoping disaster wouldn’t strike. However, despite being “fast-tracked” by the Obama Administration, construction didn’t start until 2013, largely for the reasons cited above. This is notwithstanding the fact that the new bridge essentially uses the “right of ways” of the old one. In other words, this should have been comparatively simple from an environmental, regulatory, and local opposition standpoint.

Undoubtedly, Mr. Trump intends to cut through the red tape and get things built much sooner than the new Tappen Zee Bridge. And, for sure, he has considerable experience in completing complex construction projects. But he’s going to be fighting against some highly implacable and resistant forces, many at the state and local level where these projects actually need to be initiated.

Will we see an acceleration of building and re-building? Hopefully, but probably not as fast as the stock market is currently anticipating, in its usual ADHD way.

Just a hill of beans? Interest rates were on the rise even before Mr. Trump’s shocker. Partially, this was due to perceptions of stronger US and global economic growth. (A growing suspicion that central banks were finally losing faith in zero and negative interest rates was another factor.) The initial report on third quarter US GDP provided some evidence of a pick-up. It showed America’s economy grew by 2.9%, more than double the rate of the first six months. That’s nice but, once again, the devil was in the details. A big part of this almost-back-to-normal growth was exports, which popped an extraordinary 10% in Q3. Naturally, there’s nothing wrong with a spurt in US exports but almost all of that was agriculture, particularly soybeans due to a massive order shipment to China. Backing out soybeans, the growth rate was a much more lackluster—and familiar—1.9%.

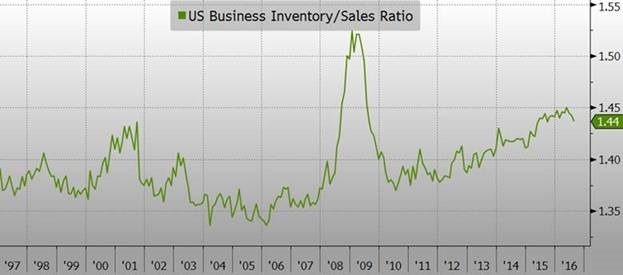

And even that was flattered by another unsustainable event: a jump in inventories. The problem with this aspect is the present dangerously elevated level of inventories. As you can see, despite some improvement lately, they remain close to their peaks. The further build-up of unsold goods is not a long-term positive.

Source: Evergreen Gavekal, Bloomberg

Source: Evergreen Gavekal, Bloomberg

Beyond inventories, it’s also hard to overlook how many companies are reporting disappointing earnings. Unquestionably, there are a number that are “beating” (though often results that were previously downwardly revised) but more are underachieving. This includes a large number of America’s finest enterprises.

Another marker that the economy wasn’t as vibrant as reported last quarter was that final sales slid from a 2.4% ascent rate to just 1.6%. This jives with a number of consumer-facing companies reporting disappointing sales and profits, ranging from general retailers to apparel makers to restaurant operators (though some store chains have high hopes for this Holiday Season and this week’s retail sales number was healthy).

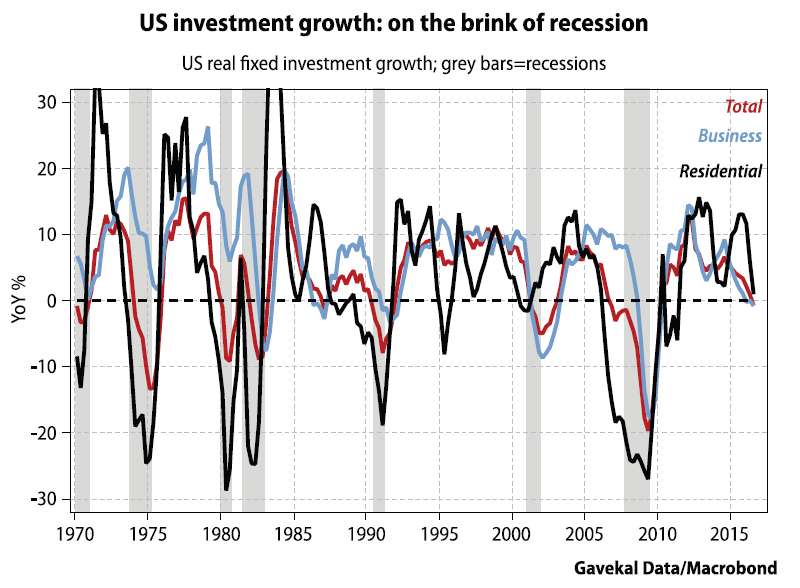

Our partners at Gavekal, who have, like us, been downplaying the risks of a US economic contraction for years, are now also increasingly wary. In a recent report titled “On the Brink of Recession”, they observed that US investment growth, including the once booming residential area, has decisively turned down.

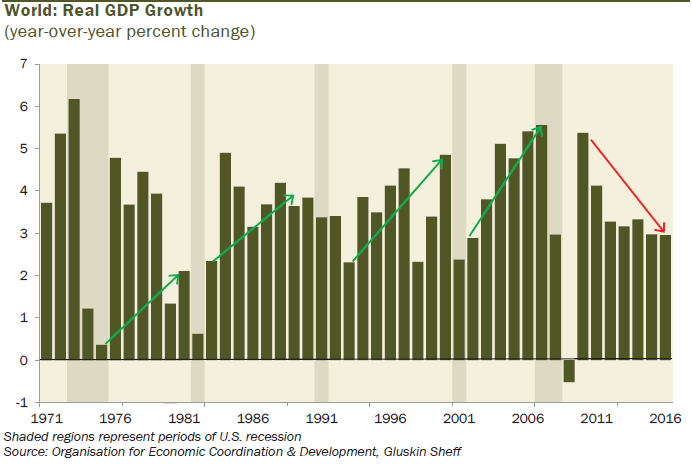

Looking globally, the chart below, again from David Rosenberg, shows the trend-line in real, or after-inflation, GDP growth. Clearly, there has never been an economic up-cycle that has looked like this one. International trade has also been contracting to a degree not seen outside of recessions.

THE GLOBAL GROWTH CYCLE NEVER GOT OFF THE GROUND

Certainly, this could be a growth scare similar to 2011. A number of Wall Street and economic forecasting firms are trumpeting an emerging up-turn in the planet’s business conditions. Frankly, we aren’t seeing much to corroborate that view, including a recent pronounced down-shift in German industrial activity, but we’ll keep our eyes—and minds—open.

The multi-trillion dollar question in our view is how much higher do interest rates need to move before an already fragile and debt-laden global economy begins to falter?

The Great Tug-of-War. The stock market has gone from dreading a Trump presidency as of last Tuesday night—when overnight futures crashed as his election became generally assumed—to celebrating it with gusto…at least in the favored sectors, per page 1.

But I would respectfully suggest to the supposedly all-knowing, ultimate discounting machine known as the S&P 500 that this optimism could be more than a little overdone. As observed last week (click to access), the potential growth-enhancing benefits of tax- and regulatory-reform, as well as the infrastructure initiatives, need to be weighed against the contractionary impact of significantly higher interest rates. With the 10-year Treasury note yield pushing above 2 ¼% this week, up almost a full percent since July, this is getting serious for industries like home-building and autos, both of which are highly interest rate-sensitive.

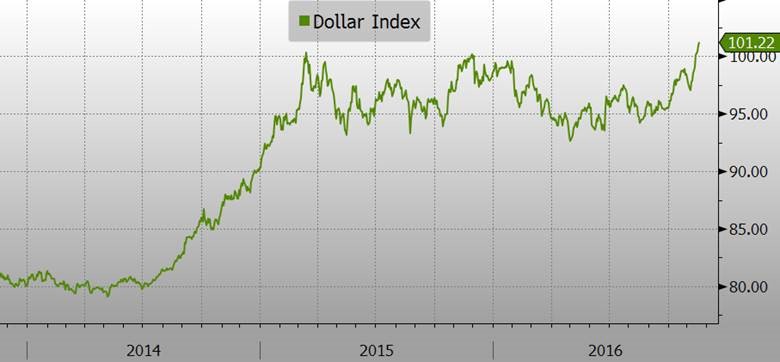

The big spurt in yields is also causing the US dollar to surge. This puts further pressure on Corporate America’s profits, which have already been in a long downtrend. At this point in time, the dollar index is on the cusp of shattering major resistance at 100. This is its third attempt and it will either be a triple top (meaning a likely peak to be followed by a sharp decline) or a critical break-out. If it’s the latter, this is definitely not good news for S&P earnings. You can see from the chart below that the dollar began its big run in the summer of 2014, which was also when the profit cycle turned down. It could be a coincidence but I doubt it due to the earnings-crimping nature of big bull markets in the greenback. (To be fair, there’s also scant question that oil prices tanking in the same time-frame aggravated the profits recession.)

US DOLLAR INDEX

Source: Evergreen Gavekal, Bloomberg

As usual, the surge by US interest rates and the dollar are hurting emerging markets. While the S&P has bumped up 2.3% since the Trump triumph (it seems like more, doesn’t it?), emerging markets have tumbled 7.25%. Gavekal’s co-founder, Charles Gave, as relayed in last week’s EVA, was one of the few to predict Trump’s win. He has also been pointing out a multi-trillion dollar short position in the US currency, particularly among emerging markets. This often arises when developing countries borrow in dollars. If they generate significant dollar revenues, the risk can be manageable. If not, it can create serious problems. Trauma in emerging markets caused by the muscular dollar played a key role in the market turbulence in 2015 and into this year. Thus, it’s prudent to keep a close eye on whether the 100 level holds for the dollar index and how severe the damage gets in developing markets.

But the truly epic battle is happening in the aforementioned bond market where trillions have been lost around the world almost overnight. Trump’s economic advisers, particularly David Malpass, believe that absurdly easy monetary policies have back-fired on the Fed and the other leading central banks, a view I have often conveyed in these pages. They feel that it’s essential to have a proper cost of capital in a capitalistic system and zero, or thereabouts, for sure ain’t it. Charles Gave has written repeatedly and passionately on this topic, as far back as 2011 in his classic essay, The High Cost of Free Money.

The Trump team may well take a page out of the old Reagan playbook and decide to take the pain of higher interest rates—as well as the distinct possibility of a related US recession—as soon as possible. (By the way, one of his top economic sages, Larry Kudlow, served as an adviser to Pres. Reagan.) Mr. Trump can then plausibly point the finger (I’m not going to speculate as to which one) at Pres. Obama and Fed chief Janet Yellen. You may have noticed that Mr. Trump excels at the blame-game, an “attribute” that may come in quite handy once he moves into the Oval Office.

It’s fair to note, as some Evergreen team members have, that even 2.3% on the 10-year treasury note isn’t exactly nose-bleed high. Perhaps even more positive, is the fact that credit spreads (the yield gap between corporate and government bonds) are far from the danger zone. This is a material improvement versus back in January when markets were reeling.

However, an interest rate increase of the degree seen since July, combined with a rocketing dollar, still represents a serious tightening of financial conditions. It’s also highly probable that our ever-timid Fed will raise rates next month. Thus, the ingredients are in place for a potential panic by retail investors between now and the end of the year. This could be aggravated by the underlying illiquidity of the corporate bond market and year-end tax-selling. Should ten-year treasuries approach 3%, as they did during the 2013 taper-tantrum, that could create some nasty shock waves.

In a recent email to me, Charles Gave confirmed he’s very concerned about the risk that the bond market melt-down poses to the US economy. Like me, he worries about the timing disparity between the immediate hit to economic activity from higher rates versus the delayed upside from reforms that haven’t even been enacted yet. It’s possible that increased confidence in the future provides a more immediate boost to consumer and business attitudes but it’s likely to be quite a tussle with the downward pressure from the bond market.

Back in the 1990s, Bill Clinton’s big spending plans were derailed by a group of traders known as the “bond vigilantes”. These shadowy enforcers of fiscal rectitude have been hiding in parts unknown for many years. But they appear to be riding their black horses once again, helping Mr. Trump in some ways—like interest rate normalization—but also threatening to tip an already frail economy over the edge.

The outcome of this contest between higher rates and improved confidence is likely to be as close as the popular vote was in last week’s election (note, I didn’t say the electoral outcome). Stay tuned…

The myth of the immaculate correction. If you listen to the Wall Street economic forecasting community—the investment world’s equivalent of political pollsters—there is about as much chance of a US recession hitting next year as there was of the UK voting to leave the EU or Donald Trump being elected president. Kind of makes you stop and think, doesn’t it?

For a moment, let’s go back and look at the history of the past eight years. The stock market has returned 15% annually, without a single down year, under a president who was widely believed to be anti-business. We’ve also had the weakest recovery on record despite history indicating that the deeper the recession, the stronger the rebound. Moreover, we’ve doubled our national debt and engaged in the most extreme monetary experiment in our history (QEs 1, 2, and 3, as well as a zero interest rate policy).

One could make the case, as I have, that among the main reasons for this is the lack of confidence in the future. This zero-confidence in zero-interest rate policies, has caused all the fabricated money to just lie there, “like an infertile egg”, as one of our clients is given to say. This has been reflected in, as observed in numerous EVAs, the total collapse in money velocity (which has been approaching Great Depression levels). But the synthetically-created trillions have done wonders for stocks, real estate, bonds, and many other asset classes. This is such familiar territory for regular readers of this newsletter I’m almost embarrassed to bring it up. But the reason I am is to ask: What if this is changing?

What would happen if those infertile trillions suddenly become fruitful and multiply? Catalysts for that could be swelling confidence due to the proposed tax cuts and regulatory rollbacks. (By the way, we seriously doubt the tax reductions will be anywhere near as radical as Mr. Trump is proposing; the same is probably true with his spending plans. Congress is unlikely to be his willing apprentice.)

Certainly, the stock market seems to be buying into (literally) the inflationary boom scenario with the “big-league” (pronounced “bigly”) rallies in nearly all cyclical stocks since November 9th. If money velocity does decidedly turn north, the Fed will need to jack rates up far and fast to avoid a major inflation eruption. And then Janet Yellen can point her finger back at Donald Trump who has promised to fire her (though that, like many of his pre-election threats, now appears improbable). So, what might be beneficial to the real economy could be devastating to the financial world, the exact opposite of what we have seen under Mr. Obama.

Do I think that is the most likely scenario? Not really, but it’s a lot more of a possibility than it was a week ago. The primary reason I don’t is the significant tightening noted above by bonds and the dollar, putting immediate downward pressure on the economy. Further, should Mr. Trump impose tariffs on certain countries, as he has vowed to do, a global trade war might well erupt, causing a severe panic and a likely global contraction (again, he may be all bluster and no—or little—bite).

In other words, I think market problems will hit sooner, not later—if rates and the dollar keep soaring. Should the market break hard, that will slap the economy upside the head when it is already staggering a bit.

For sure, it’s hard to know how to position as an investor. What was already a bizarre and unprecedented set of circumstances has become more so. Mr. Trump changes his views so quickly and often, it’s hard to know what’s real and what’s Memorex. As Bloomberg’s Matt Levine wrote this week: “If you ever find yourself writing a sentence in which Donald Trump is the subject, maybe don’t start it with ‘surely’.”

But it’s also fair to say that Mr. Trump might be crazy like a fox, as he has been throughout the campaign season. He may really believe that there is no way out of what he has repeatedly called “a big fat bubble” due to Fed policies. Some of his key advisers, like David Malpass, whose views I respect, have made that case less bluntly.

Getting rates up to more normal levels is essential for the long run viability of the economy and it will ultimately be great news for retired and soon-to-be retiring investors who have been so punished by the Fed’s crusade against return on savings. Who knows? We may witness the first-time a president is pressuring the Fed to raise, rather than cut, interest rates. Yes, I realize that’s a stretch but even if Ms. Yellen continues to hike rates at the speed of the glacier on Mount Rainier, the bond market has already shown it won’t react in slow-motion. And it’s naïve to think that a meaningful increase by interest rates can happen without turmoil in markets that have become hooked on negligible interest rates.

Consequently, those who are betting on a continuation of the TTT (Trump Triumph Trade) may be making a big fat error, sort of like all those pollsters and bookies that were so sure Hillary Clinton would be our next president.

Voting update: One astute EVA reader emailed us to point out that our factoid about Donald Trump receiving two million less votes than Mitt Romney did in 2012 became erroneous as additional tabulations were made. He was absolutely correct. As of the latest tally, Mr. Trump has garnered 61.3 million votes, versus Mr. Romney’s total of just under 61 million in 2012. There remain a million or so absentee ballots left to count.

However, Hillary Clinton’s popular vote lead continues to grow and is expected to: She currently has about 62.4 million total votes. On a percentage basis, it works out to 46.8% for Mr. Trump and 47.7% for Mrs. Clinton. In 2012, Mr. Romney received about 47.2% of the total votes cast. There are about 227 million eligible voters now versus 215 million in 2012.

Republicans and Democrats combined received 3.2 million votes less than they did in 2012, despite the larger pool of qualified voters, reflecting both voter apathy and more votes flowing to independent candidates.

David Hay

Chief Investment Officer

To contact Dave, email:

dhay@evergreengavekal.com

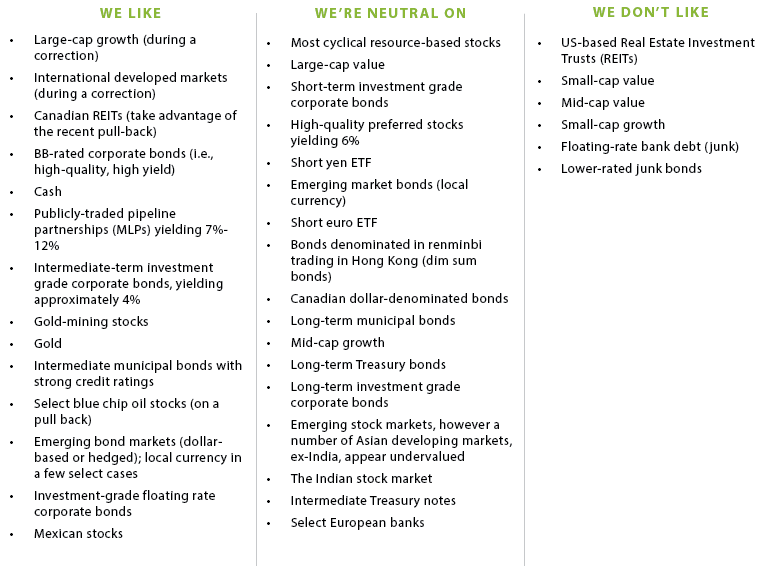

OUR CURRENT LIKES AND DISLIKES

No changes this week.

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness.