“Three percent is the longer-run normal federal funds rate that participants estimate...with a two percent inflation objective. That’s one percent in real terms.”

-JANET YELLEN, Fed chair, at this Wednesday’s Federal Open Market Committee (FOMC) press conference

Fed Storm Rising. It’s been roughly 13 years since I borrowed—and modified—that title from Tom Clancy for our old hardcopy client newsletter, The Strategist. It was written during the early stages of the last Fed tightening cycle, a hiking campaign which was to last for two years, jacking up its overnight rate from the previously-unimaginable level of 1% to a peak of 5 1/4% in June, 2006.

Despite the fact the Fed increased rates at 17 consecutive meetings from 2004 to 2006, the S&P 500 rose pretty much steadily throughout this period. Stocks even made a slightly higher high in October of 2007, in the wake of the Fed’s somewhat panicky 50 basis points (1/2%) cut, in September of that year, due to the escalating crisis in the housing market. On the day this sharp rate reduction occurred, the Dow spiked 2.5% while the S&P 500 vaulted an even larger 3%. Investors were clearly remembering the old Wall Street maxim that you don’t fight the Fed.

However, over the next 15 months, the Fed proceeded to slash its key rate all the way to the drill bit-like level of ¼%, creating another “despite”: Notwithstanding this 95% reduction in the fed funds rate, the S&P 500 fell from 1550 in October, 2007, to the satanic intraday low of 666, on March 6th, 2009. So much for not fighting the Fed! Investors who followed that logic ended up fighting mad—and a heck of a lot poorer.

Consequently, when one reflects back upon both the bull and bear phases of the 2004 to early 2009 timeframe, it’s clear that markets can ignore even repeated and significant Fed-orchestrated rate movements for a very long time. But, then, as many other similar episodes have shown, eventually stocks react. Of course, the ultimate question is: When?

Earlier in this young year, Evergreen was in its usual lonely position. We were one of the few investment firms proclaiming that the Fed would—at long last—actually stay true to its word and raise rates multiple times this year. (So much for our conventional wisdom label we were given lately!). To that point, as Greg Ip wrote in Monday’s Wall Street Journal: “A few months ago, virtually no one expected the Federal Reserve to raise interest rates this week. Now, almost everyone does.”

In our January “Unexpected Outcomes” EVA, we went so far as to speculate that the Fed might wrong-foot the complacent consensus by hiking four times in 2017. That seemed somewhat outlandish at the time but now several leading Wall Street sources are saying four bumps this year is a distinct possibility.

The author of the excellent Daily Blog Hedgopia (click here to check it out), Paban Pandey, and I even made a small wager a few weeks ago about the odds of a March increase, with yours truly, of course, taking the long-shot bet that the Fed would raise. When the odds suddenly soared toward 90% from 30% in mid-February, he asked what had led me to believe that a hike was probable. My answer was multi-faceted but it had very much to do with politics and a long-dead Swedish economist.

Say what?

Going big before going home? As previously conveyed in these pages, I believe there is very little love lost between Janet Yellen, as well as her closest colleagues, and Donald Trump. Accordingly, Yellen and Co. seem to be wearing much different lenses as they survey the economy than they did during the prior Administration.

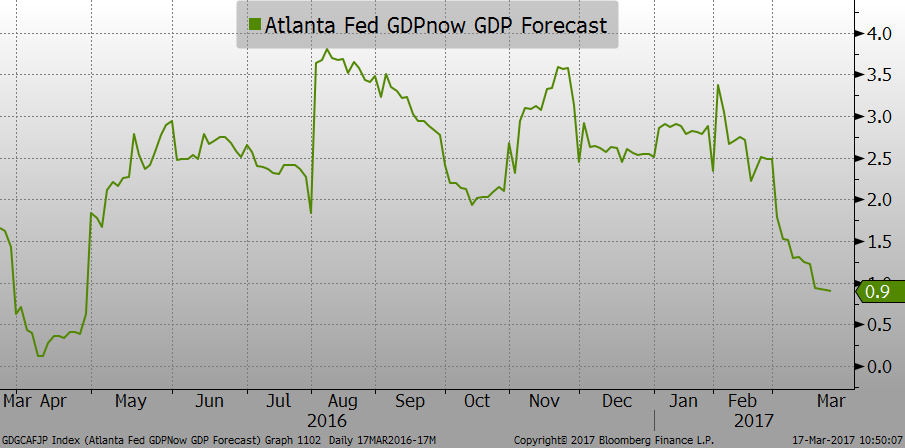

For example, it’s hard to believe the Fed would have raised rates twice in three months, as it has just done (after just two throughout one of the longest expansions in history!), based on a fourth quarter GDP increase of a mere 1.9% and what looks like a flaccid first quarter growth rate around 1%. The latter number comes from the Atlanta Fed’s GDPNow survey and, as you can see, it’s been plunging like an internet stock circa 2001.

One would think that the so-called “animal spirits” unleashed by Trumphoria should be positively impacting current economic activity by now but, based on the above, that’s clearly not the case. Thus, the Trump effect remains MIA when it comes to the most comprehensive measure of the US economy’s vitality.

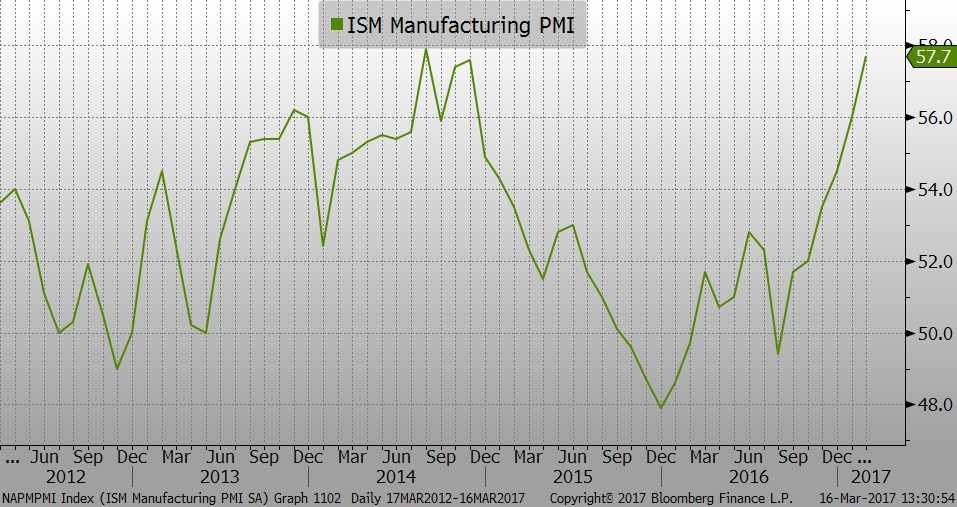

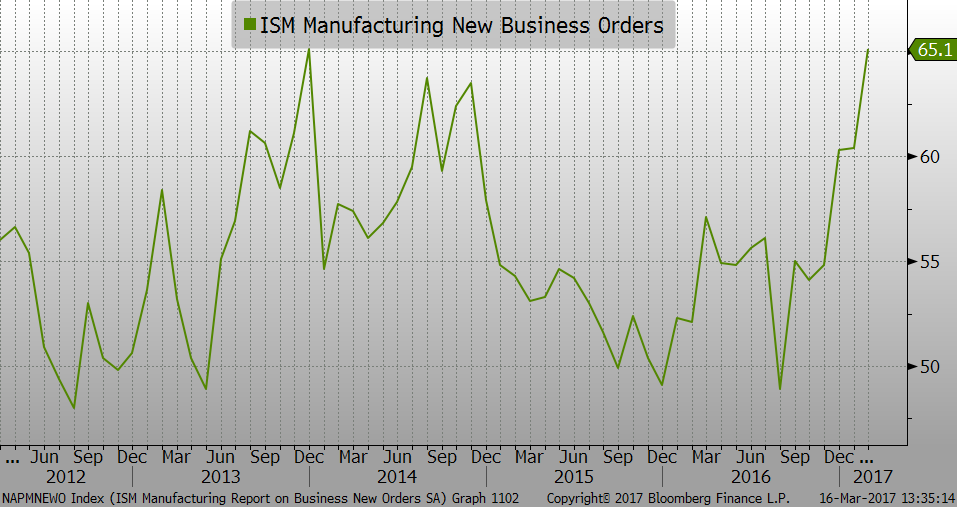

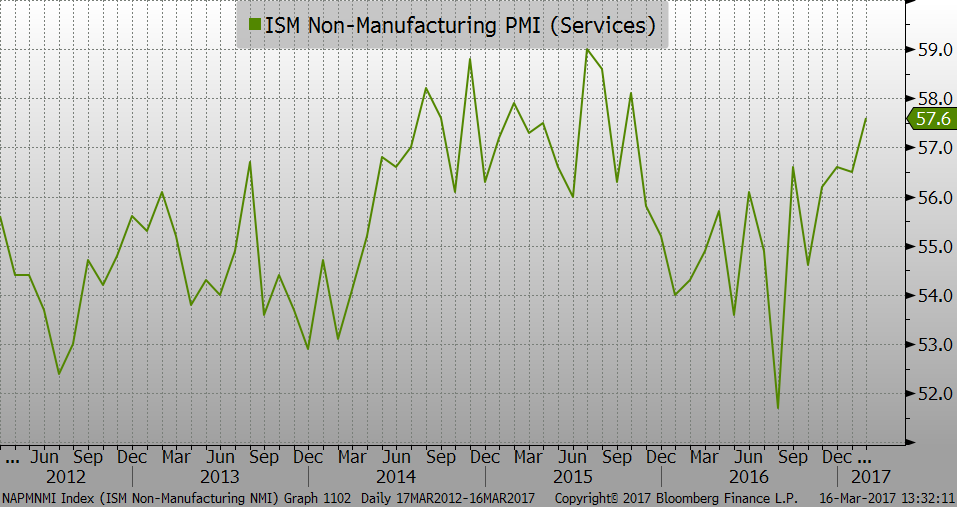

Of course, as far as sentiment surveys (otherwise known as “soft data” versus “hard data”, like actual GDP numbers) are concerned, the future looks as rosy as the New Year’s Day parade in Pasadena.

INSTITUTE OF SUPPLY MANAGEMENT (ISM) MANUFACTURING SURVEY

ISM NEW BUSINESS ORDERS SURVEY

ISM SERVICES SURVEY

Source: Evergreen GaveKal, Bloomberg

Source: Evergreen GaveKal, Bloomberg

Even the appropriately jaded Danielle DiMartino Booth—author of our January Guest EVA and now of sudden CNBC fame—is anticipating a blockbuster second quarter based on surveys like those shown above. Part of the reason for this optimism is what was perceived to be a boffo February jobs report released last Friday. But, as even Danielle conceded, unusually warm weather played a major part in boosting the numbers. In fact, crack economist David Rosenberg—so often quoted not only in EVAs but in nearly every major financial media—estimates that with normal February weather, the jobs gain would have been a disappointing 50,000 rather than an exhilarating 235,000.

Therefore, if the Fed were inclined to take a more cautious view of the economic landscape, it would have ample evidence to do so; but that’s clearly not the case. It’s probable that the buoyant stock market, even after two rate bumps of late, is emboldening the Fed. However, I also believe, humans being humans, it’s a high likelihood that many, if not most, of the top Fed officials realize their days are numbered. Ergo, why not go out in a blaze of central bank glory, firing off rate increases at a clip unseen since the belated Bernanke attempt to deflate the housing bubble? These folks can then take credit for having achieved the treacherous job of, at a minimum, partial rate normalization. This, of course, would give their successors ample room for future rate cuts during the next crisis. There are far worse legacies for which Ms. Yellen and her crew could go down in history at the Federal Reserve.

The notion of a “retro” tightening cycle actually raises an interesting point. This is because Janet Yellen is on record stating that, in hindsight, she regrets being party to the Fed’s aforementioned slow and steady increases leading up to the financial crisis. She was quoted as saying she now believes the predictable and deliberate nature of the Fed’s tightening cycle back then contributed to excessive speculation. (Ya think?!!)

If she really means that (always tough to know with senior government officials), then she should be extremely wary about repeating the same mistake. For sure, one could persuasively make the case it’s already much too late for such concerns (put me in that camp); however, the Fed believes that there aren’t many bubbles around these days, other than perhaps commercial real estate. If so, then it still has time to tighten preemptively to forestall another disaster. But slow and gradual ¼ point hikes won’t do the trick. Thus, there’s a decent chance we might see a ½ point hike at one of the upcoming meetings and that likely would get the market’s attention.

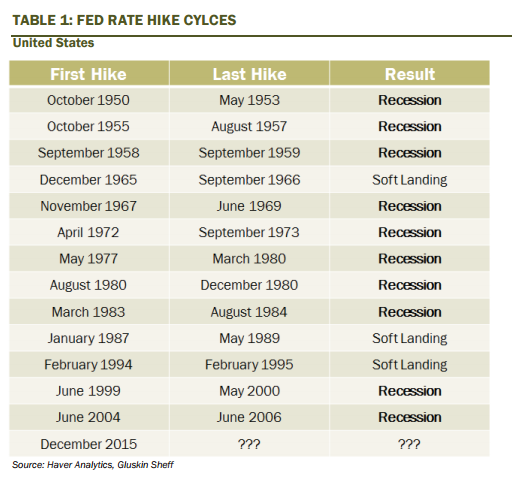

David Rosenberg has pointed out, as relayed a few weeks ago in this letter, that 10 out of 13 Fed hiking cycles since WWII have ended in recessions and/or bear markets. The evidence backing up his claim is displayed below.

POST-WWII FED TIGHTENINGS

Source: Haver Analytics, Gluskin Sheff

Source: Haver Analytics, Gluskin Sheff

But what he hasn’t said is that two of the three “happy endings” weren’t all that joyous. One was 1966, which happens to have been on the eve of 16-year bear markets in both stocks and bonds. The other was the 1987 to 1989 rate-hiking sequence. Not only did this timeframe bring the epic crash of 1987, it also led to the S&L crisis, the worst banking convulsion (up until then) since the Great Depression. This, in turn, set the stage for the early 1990s recession. So I would argue the record is more like 12 out of 13, with only the mid-1990s enjoying the ever-elusive “soft-landing”.

Now what about that long-deceased economist?

A century-old “new” rule. It’s no secret to regular EVA readers that I’m an ardent admirer of my septuagenarian partner, Charles Gave. Charles, in turn, for years, has written glowingly on the work of Swedish economist Knut Wicksell who died nearly 100 years ago.

Interestingly, Mr. Wicksell died in 1926 right in the middle of the greatest credit and stock market bubble in history…up to that point. One of the reasons for that gargantuan speculative orgy—and the subsequent crash, which led to near-extinction of capitalism around the world—was a problem at the heart of Wicksell’s theorem. He believed that interest rates at too low a level encourage speculation and economic overheating. Eventually, rates soar as they play catch up with the prior suppression, causing the asset bubbles inflated by low rates to implode. That’s pretty much what happened during the 1920s; excessively cheap money led to stock prices going postal and interest rates eventually did the same.

The broker “call money” rate more than tripled from 1925 to the summer of 1929, eventually peaking at 15%. This encouraged blue chip companies to lend their excess capital into securities markets rather than invest in their operations. Thus, almost the entire country became engulfed in a casino mentality, with the stock market in essence evolving (or devolving) into a gigantic craps table. As always, the combination of rapidly rising stock prices and interest rates was an accident waiting to happen. In October of 1929, the waiting was over.

This chain of events would have been no surprise to Mr. Wicksell. His bedrock belief was that there was a “natural rate” of interest, one that the market would set properly in the absence of interference from well-intentioned, but often misguided, entities like the Fed. If the natural rate and the market rate were roughly in equilibrium, then credit creation, inflation, and market prices would all increase at a pace that wasn’t too hot or too cold. In other words, they would approximate “Goldilocks” conditions.

For years, Charles was a lonely voice championing the logic of this approach. Yet, in the wake of the global financial crisis and the worst economic contraction since Great Depression, America’s central bank turned a deaf ear to such urgings. Instead, it opted for a seat-of-the-pants approach that rejected a rules-based system such as what Wicksell proposed so many decades ago. It also jettisoned the “Taylor Rule” which it had unofficially followed for years and bore some resemblance to Wicksellian theories.

Now get ready for a serious plot twist: Suddenly, Yellen and Co. have discovered Wicksell. In one of the most important Wall Street Journal Op-Eds in recent memory, Donald Luskin, chief investment officer of Trend Macrolytics, outlined the remarkable mind-set shift that has occurred at the Fed lately. Stanley Fischer, the Fed’s Vice-Chair and intellectual guiding light, has been repeatedly and publicly embracing Mr. Wicksell’s work. Ms. Yellen has been more subtle—but not much. She has been talking about a neutral rate, one that is, as Mr. Luskin quoted her, “the interest rate that is neither expansionary or contractionary”; i.e., in Goldilocks-speak, “it’s just right”. The ultimate indication of a Goldilocks fed funds rate is if inflation is near its proper level, at least in the Fed’s view.

With inflation returning to the 2% range the Fed desires, its new-found appreciation of Wicksell means it is time to fully “normalize” rates. Using his natural rates as a guide, it will stay on its tightening arc as long as the CPI hovers around 2%. However, should inflation flare up much more than that the Fed will feel compelled to hike more aggressively. Therefore, what we’ve got is a throw-back Fed tightening cycle that is likely to last quite awhile.

Which gets back to that always irksome “when” question from page one…

Are good things coming for those who wait? On Wednesday, the day the Fed announced its most recent rate hike, CNBC ran an extensive interview with the new King of Bonds, Doubleline’s Jeff Gundlach. Even though he shuns the label of contrarian, Mr. Gundlach thinks that way—and that’s a key reason why I listen to him so intently, in addition to his long history of prescient market calls.

My affinity for his views rose even higher on Wednesday as he lucidly outlined his outlook, which sounds a lot like what I’ve conveyed in these pages in recent months. (So, if I’m going to be wrong at least I’ll be in some very elite company!) Specifically, he, like Evergreen, is expecting the yield curve to flatten. In English, this means short rates will rise faster than longer rates. Similar to our view, he doesn’t see the 10-year treasury yield moving much above 2.5% to 2.6% where it trades today. He does allow that it might spike to 3% but, basically, he sees an “old-school” Fed tightening cycle that should continue until something breaks in the system. To which we say: Precisely! After all, that’s what the “12 out of 13 times” history of past tightening cycles is all about.

Also like Evergreen, he believes the bearish consensus on longer bonds is a prime reason for why they are likely to rally. As we’ve noted ad nauseam (and EVA readers likely have the upset stomachs to show for it), when markets are heavily betting one way they are extremely prone to move in exactly the opposite direction, a tendency Mr. Gundlach cited on Wednesday.

The knee-jerk reaction is that a tightening Fed means higher long rates but as he quipped: “What’s wrong with the cop being on the beat?” He went on to reference, as we have, the 2004 to 2006 Fed rate-hiking episode when nearly all the increase in longer treasury yields occurred BEFORE it bumped even once. Proving his point, though perhaps only temporarily, treasury prices actually rallied after Wednesday’s rate-hike announcement.

Jeffrey went onto say that he doesn’t see a recession looming this year even though he and his team were picking up worrisome signals last summer, again, as were we. But he believes the post-election confidence surge, so evident in the various surveys we show on pages 2 and 3, is no fluke. In fact, he believes this may lead the Fed to adopt an increasingly hawkish tone, with the long-end of the yield curve reacting more and more favorably as our central bank gets deeper into its rate-boosting campaign.

Consequently, the most probable answer to the “when” question is the shape of the yield curve. Until the market rate on the 2-year treasury note approaches that of the 10-year, the party may well continue. But, just like trying to get out of stocks before there is a major trend reversal, this is a tricky and dangerous gambit.

Presently, the 2-year yields 1.3%, well below the 2.5% level the 10-year closed at yesterday. Thus, we could be several rate hikes from when the ice will start making that eerie cracking sound. Since there are four more Fed meetings over the next six months, in the late third quarter is when things could truly get dicey.

And don’t forget about our old trusty leading indicator, credit spreads. Should they start widening in a major way, at the same time that the yield curve is flattening, the dollar is rising, and, possibly, the Fed is allowing its obese balance sheet to contract, we could be talking about a quadruple whammy.

By the fall, it’s quite possible we will be seeing this scenario play out, much to the stock market’s chagrin. We learned a long time ago that October can be a most interesting month when vast sums are lost by those who bought too high and too carelessly, while equally big money is made by those who waited for the inevitable panic. It’s been a very long wait which means it’s also likely to be very great opportunity.

David Hay

Chief Investment Officer

To contact Dave, email:

dhay@evergreengavekal.com

OUR CURRENT LIKES AND DISLIKES

Changes in bold.

LIKE

NEUTRAL

DISLIKE

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness.