“The world economy is like an ocean liner without life boats.”

- Senior HSBC economist, Stephen King.

What Happens When a Dragon Flaps its Wings?

Have you ever heard of the butterfly effect?

It’s the idea in chaos theory that small events in a complex system can result in big changes over time. A butterfly flapping its wings over the Puget Sound can supposedly set a series of events in motion that ultimately hurls a Category 3 hurricane onto the shores of South Louisiana. Or a flock of seagulls flying over the beaches of Brazil can trigger a freak snowstorm in Tel Aviv. In other words, events that appear trivial can change the course of history.

The idea that seemingly small events can have big impacts is particularly relevant in financial markets. As the Bank of England’s Chief Economist, Andrew Haldane, outlined in a recent speech, the global financial system is not a classic complex, adaptive network. It’s a complex, adaptive “system of systems” with an entirely different risk distribution.

As a result of all that complexity, extreme events tend to occur far more frequently than most investors expect. “A four-standard deviation event—a true catastrophe—would under a normal distribution be expected to occur roughly every 15,000 years,” Haldane explains. “Under the estimated distributions for economic and financial systems, such an event would occur every 10 to 15 years.”

Contrary to our recent experience in what my friend Ben Hunt calls the “Golden Age of the Central Banker,” it doesn’t take much to upend the markets in a highly leveraged, highly interconnected “system of systems”… not to mention a system of systems which have all been distorted by years of easy money. Don’t get lulled into complacency, my friends. The fact that it’s been nearly seven years since the last true financial panic should make us more—not less—vigilant about the growing risks. The illusion of stability can’t and won’t last forever. It just takes the right catalyst—the likes of which often seem insignificant until months or years down the road—to usher in a new era of profound instability.

With all that in mind, let’s get back to the butterfly. If a flock of seagulls or a tiny insect can cause such a ruckus, what happens when a dragon flaps its wings?

I think we’re about to find out…

The People’s Bank of China (PBoC) shocked the world last week when it abruptly devalued its currency and introduced an ostensibly more market-driven protocol for guiding the exchange rate over time. Chinese currency policy may seem like an insignificant or overly-esoteric topic to discuss in this week’s EVA, but please bear with me. The un-anchoring of what has been Asia’s most stable currency may be the most important macro event of 2015, and it could have enormous implications for your portfolio.

Beijing has kept a firm grip on the USD/CNY (US dollar/Chinese onshore yuan) exchange rate in recent years by forcing the markets to trade within a narrow band around a midpoint set each day by the PBoC without respect to market forces. For all practical purposes, this protocol has kept the Chinese government in control of the onshore exchange rate (CNY). That perceived stability has generally kept speculators at bay despite significant deviations from the market-driven offshore exchange rate for the Chinese currency (CNH).

As a quick aside, Beijing launched the offshore yuan (CNH) in 2004 as part of an early effort to internationalize China’s renminbi (RMB), which includes both the CNY and the CNH. In addition to a growing list of Hong Kong-offered financial services denominated in the freely-traded CNH, the marked-driven offshore yuan has become the backbone of the rapidly deepening “dim-sum” bond market. This rising demand is keeping interest rates low relative to mainland rates and also encouraging foreign borrowers to finance their operations in yuan, facilitating its widespread adoption as a trade currency.

Beijing eventually plans to reunite the offshore and onshore currency markets into a freely-floating RMB which, within the next few years, will hopefully boast enough global demand to function as both a trade and a reserve currency. In theory, such acceptance would grant the PBoC the exorbitant privilege of expanding its balance sheet in line with growing demand… a huge advantage for a debt-burdened country that needs to finance a Eurasian version of the Marshall Plan (the New Silk Road Economic Belt & 21st Century Maritime Silk Road) in order to boost its potential GDP growth in the coming years. Of course, it would help if the International Monetary Fund (IMF) would lend a little credibility to that cause by including the RMB in its Special Drawing Rights (SDR) basket of reserve currencies sooner rather than later.

That’s why last week’s announcement was so important. While Western media outlets continue to obsess over the multi-day fall in the CNY’s value (admittedly the largest since 1994, but still quite small compared to the recent moves in other currencies), the big story is the new protocol governing the CNY exchange rate.

Rather than arbitrarily fixing the onshore currency’s midpoint each day at a level of its own choosing, the PBoC now anchors each day’s trading band in line with the previous day’s closing price. While daily moves in the USD/CNY are still limited to 2% in either direction, Beijing is sending a message to the world that the market now plays a decisive role in determining the exchange rate’s ultimate direction… as long as you keep in mind that Beijing is often the most dominant player in the CNY market.

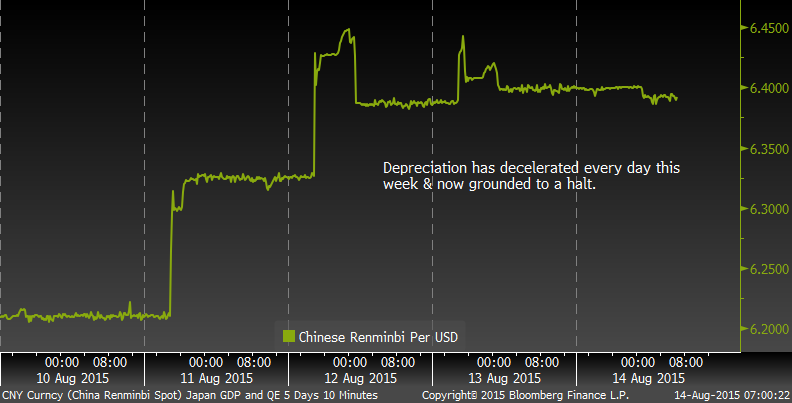

FIGURE 1: CHINESE YUAN 5-DAY  Source: Evergreen GaveKal, Bloomberg

Source: Evergreen GaveKal, Bloomberg

Considering PBoC official Zhang Xiaohui’s comments last Friday—that “the one-time total depreciation of around 3% is largely finished” —it would be easy to think that the CNY slide is over. But there is no guarantee that Beijing will continue to intervene indefinitely in the CNY market as it did last week. China has decisively moved toward a more market-oriented structure at a time when outflows have been accelerating. Moreover, considering Beijing’s confidence-killing response to its falling stock market last month, it’s unlikely that foreign capital will pour in anytime soon to offset domestic money already headed for the door.

With $3.6 trillion in foreign exchange reserves, the PBoC certainly has the resources to hold the line on China’s onshore exchange rate. But who knows what will happen if and when capital outflows accelerate? A major depreciation over time is certainly possible. Yet, even if Beijing chooses to maintain CNY stability in the face of tremendous outflows (which would only empower President Xi Jinping’s critics within the Chinese Communist Party), the mere possibility of further depreciation in China raises the probability of more competitive devaluation somewhere in the world (in fact, this week we’ve seen exactly that in Vietnam and every tourist’s favorite vacation spot, Kazakhstan). This could occur at the very moment that the Federal Reserve looks to raise interest rates.

Make no mistake, China has just changed the game in a thousand ways that are not entirely straightforward. While a 3% devaluation in the USD/CNY exchange rate is not the kind of global deflationary shock that some people are saying, the un-anchoring of expectations and the possibility of further depreciation in the coming months sets a series of events in motion that dramatically raises the odds of a global deflationary bust in the not-so-distant future.

I won’t bore you with all the details, but—even if China is simply moving toward RMB internationalization—I can think of a dozen ways the uncertainty surrounding PBoC’s latest move can destabilize global markets. Even if we were to assume that China can afford to allow capital to flow freely into and out of its debt-burdened economy without inducing a crisis (a big assumption in my opinion), the mere act of a dragon flapping its wings and preparing to fly will have unintended and unanticipated consequences. These include, but are not limited to, accelerating the unwind of fragile emerging market carry trades and raising the odds of global competitive devaluation (this was a key theme of last week’s Chartbook EVA).

Keep this in mind: In a world where everything is connected, where every major economy has a debt problem, where money has flooded the world for seven years, and where volatility remains low even in the face of collapsing commodity markets, the Federal Reserve is tightening at a time the rest of the world has been easing. And in the event that its first rate hike in nearly a decade sends the US dollar higher, Beijing will have the plausible deniability it needs—if it so chooses—to let the USD/CNY exchange rate drop like a stone.

With these risks—and myriad others—in mind, my colleagues and I at Evergreen GaveKal believe it pays to be prudent at this point in the global cycle. Everyone talks about buying low and selling high, but most investors tend to do just the opposite. And while it’s easy to think of ourselves individually as somehow better or wiser than the herd, most of us will instinctively move in the same direction without a self-aware philosophy and a disciplined process to keep us on track.

No one should think they can precisely time the market’s twists and turns—especially a market long distorted by unprecedented quantitative easing—but there comes a time when enough is enough. It’s not worth reaching for more upside when risks are so skewed to the downside. In fact, the greatest opportunities for wealth-creation at the end of a bubbly market cycle lie in reducing equities in favor of a more defensive portfolio posture that earns less in the short term and higher cash reserves that earn nothing for the time being.

Yes, I said wealth creation, not just wealth preservation. The opportunities are enormous, just not where most investors are looking at the moment. Paradoxically, the asset that earns you nothing over time can deliver the highest returns in a panic. Cash is an option that can be traded for any asset at any time, so its value is inversely related with asset prices. That is to say, cash becomes undervalued when markets are overvalued and overvalued when markets are undervalued.

The added deflationary pressure from a CNY shock could turn an already dangerous event for fragile emerging markets into an outright catastrophe for the entire global system—and create one whale of a buying opportunity for investors who still have money to work in that environment.

Worth Wray - wray@evergreengavekal.com

Glutted. For most of my adult life, oil has been something America had just too little of. Our chronic under-production and over-consumption were dual drivers of the nearly constant trade deficits we ran since the 1970s (along with the emergence of China as an export powerhouse). Even worse, at times this recurring crude shortage threatened to starve our economy of its essential fuel.

Then, about 10 years ago, something I never thought I would live long enough to see began to unfold. As a result of the twin breakthroughs of horizontal drilling and hydraulic fracturing (aka, fracking), US oil production, so long in a relentless downtrend, began to soar like one of Bubba Watson’s tee shots.

Almost overnight, US energy companies became prolific enough to rival Saudi Arabia as the “swing producer” of crude. In other words, America’s oil industry, especially the “frackers”, began to set the marginal price. And, just as suddenly, the US was awash in a commodity that many pundits of yesteryear had ardently predicted was to have been almost totally depleted by now. What had been a sad tale morphed into a Hollywood ending worthy of Frank Capra.

Besides investment bankers who financed the boom in exploration and production spending—and, of course, those early frackers who made great fortunes as prices rose to over $100/barrel—another sub-industry flourished as well. The once-obscure realm known as mid-stream energy found itself hitched to a ballistic missile. This sector is made up of the companies that own pipelines, storage facilities, gas processing plants, marine terminals, and a host of other mundane businesses that provide the plumbing for our nation’s flow of hydrocarbons across its vast stretches.

Consequently, even as the US stock market has labored to produce a mere 4% total return over the past 15 years, the security of choice for many of the mid-stream energy operators—master limited partnerships (MLPs)—shot the lights out. MLPs have generated 15% total returns annually since 12/31/99—despite what only can be described as a cataclysm since last summer.

FIGURE 2: MLP INDEX TOTAL RETURN SINCE 12/31/99

Source: Evergreen GaveKal, Bloomberg

Source: Evergreen GaveKal, Bloomberg

As noted in prior EVAs, Evergreen became quite concerned that these utility-like investments were far too in-vogue by the late spring of last year. The May 10, 2014 EVA observed that the main MLP confab, held in May, 2014, in Jacksonville, Florida, had the feeling of a tech conference circa 1999. Little did we know how close we were to the peak of the MLP love-fest, or the severity of their fall from grace.

Normally, MLPs aren’t particularly sensitive to the price of oil and gas. However, when crude falls by nearly 70%, the usual tendencies don’t apply. Even reliable “toll-collectors”, as MLPs are often known, become viewed as potentially not-so-reliable when such a big boom goes kaboom.

Given current conditions—bordering on an industry-specific depression—such fears are understandable. But there’s now little doubt that a key factor in what has slapped a long list of MLPs down 50% or more, in many cases a greater decline than even highly cyclical producers and oil-service companies have suffered, was that nasty four-letter word: DEBT.

Numerous past EVAs, going all the way back to before the Great Recession, have highlighted the risks posed by the carry trade. This is the investment “strategy” where short-term debt is used to finance long-term securities. When money can be borrowed for negligible rates, as has been the case for so long, the carry trade can be extremely lucrative. This is especially true when it involves an asset class like MLPs that produce high cash flows. And when they are also rising in price, as they did for many years leading up to last summer, this becomes the leveraged investors’ equivalent of a grand slam.

Unfortunately, since then, the word “slam” has taken on a far different meaning.

Valuation analysis still has value. Worth noted in his section of this EVA the importance of methodically raising cash reserves as markets become increasingly over-valued. Such reasoning seems logical, but realize that in this era where passive investing and the efficient market hypothesis are so dominant there is no such thing as “over-valued.” The most recent quote is by definition the correct price. Those attempting to make a case for fundamental analysis are often derided as hopelessly antiquated or certain victims of the overwhelming power of momentum investors—who care not a whit about excessive valuations.

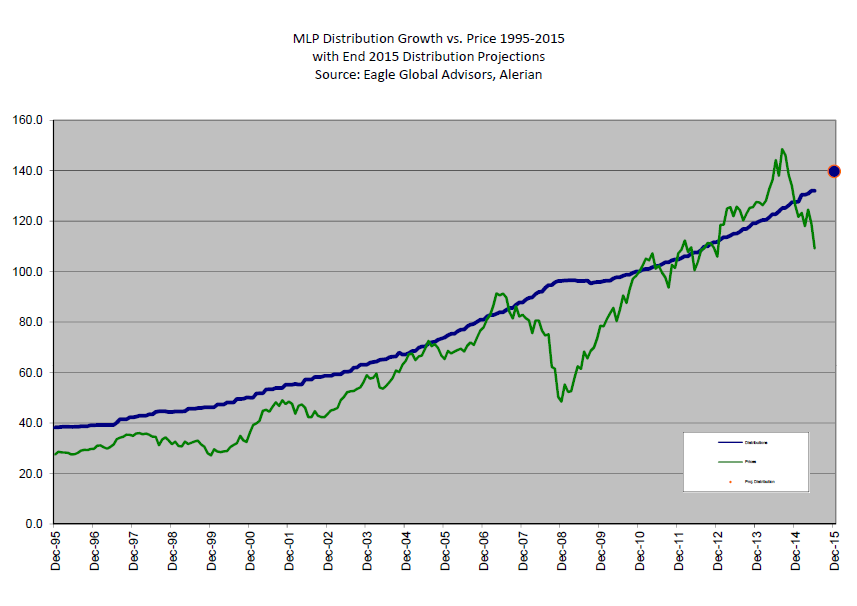

Yet, 14 months ago, MLPs were trading at their priciest level ever on several metrics. As we say at our firm, “ever” is a pretty long time. There were numerous ways to back up that assertion but the following chart, showing the MLP index versus its long-time distribution growth rate trend-line, was clearly indicating nose-bleed territory. Today, this sector is bleeding profusely—and not just from its nose.

FIGURE 3: MLP DISTRIBUTION GROWTH VERSUS PRICE 1995-2015 WITH END 2015 DISTRIBUTION PROJECTIONS

Source: Eagle Global Advisors, Alerian

It goes without saying that what is over-valued can become insanely over-valued. For example, a recurring warning we’ve made is that the S&P 500’s median price-to-sales ratio exceeded its highest point EVER back in 2013. This didn’t stop it from going up another roughly 20%, raising the price-to-sales ratio above where it was even at the frothiest point of the infamous late ‘90’s stock bubble.

The MLP shellacking has been painful for buy-and-hold investors but for those who liberally used borrowed money to goose returns it has been an utter disaster, perhaps a total wipe-out. Starting last month, it began to look as though the most leveraged MLP players (read: hedge funds) were being sold out by their brokers’ margin clerks. Then, in the first week of August, we began to hear rumblings of even closed-end mutual funds succumbing to the same terrible fate. Certainly, the indiscriminate and brutal selling that brought routine 5% to 10% down days two weeks ago, for nearly all mid-stream MLPs, was indicative of forced liquidation.

MLP-dedicated closed-end funds have been around for years but, predictably, the more they rose, the more popular they became, especially with yield-starved investors (which, truth be told, all income investors are these days). Naturally, Wall Street was only too happy to feed the quacking ducks, as the old saying goes. Accordingly, over the last few years the issuance of new MLP funds, to use a highly technical term, “went bonkers.”

Closed-end funds are not leverage pigs like hedge hogs funds, but their constant issuance as prices further detached from fair value represented the opposite of what Worth suggests. Instead of a systematic reduction of risk, myriad investors were taking on leveraged exposure at inflated prices (sorry, there I go again being judgmental, in the valuation sense of the word).

The problem is that when prices drop 50%, as many MLPs have done in the past year, even a relatively modest debt level of 30% becomes problematic. The end result is that dreaded event known as a margin call. This then forces prices lower yet, triggering even more involuntary selling.

Fortunately, at least for those of us who have been buying into the implosion, about 10 days ago this conflagration seemed to burn itself out. But for those forced to liquidate, it was too late. The damage was done, and the losses locked in for good (or, actually, bad).

To get a sense just how brutalized MLP closed-end funds have been, check out the Specialized Equity Funds section in Barron’s. The number of funds with big minus signs in front of their 52-week market “returns” is astounding. Some are mining-related but most have “MLP” in their title. The majority are down 25% to 30% but some are in the 35% to 40% range with one unlucky fund down a whopping 44%. Had it not been for a few takeovers of large cap MLPs, these numbers would assuredly been much worse—not that they need to be.

The burning question is, of course: What happens next?

When bad things happen to good stories. It’s more than a touch ironic that oil has experienced another down-leg because production, especially in the US, is assumed to continue to ramp, though at a slightly slower pace. Yet, MLPs have been crushed because output is believed to be ready to fall off the cliff. Obviously, one of these views is misplaced.

The problem is clearly not demand. The Energy Information Agency (EIA) just raised its global demand forecast for at least the fourth time in the last year. Similarly, Barclays is predicting total demand to be 94 million barrels per day (bpd) up from 92.6 million last year. For next year, demand is projected at 95.4 million bpd.

We recently heard from the CEO of one of the largest over-the-water shipper of crude that worldwide demand for gasoline is rabid. And this is despite a global economy that makes the word “flaccid” sound overly optimistic.

Meanwhile, the US drilling rig count has plunged close to 60%. Offsetting this, though, is the much greater efficiency producers are realizing due to mothballing their least efficient rigs and focusing on their best resource prospects.

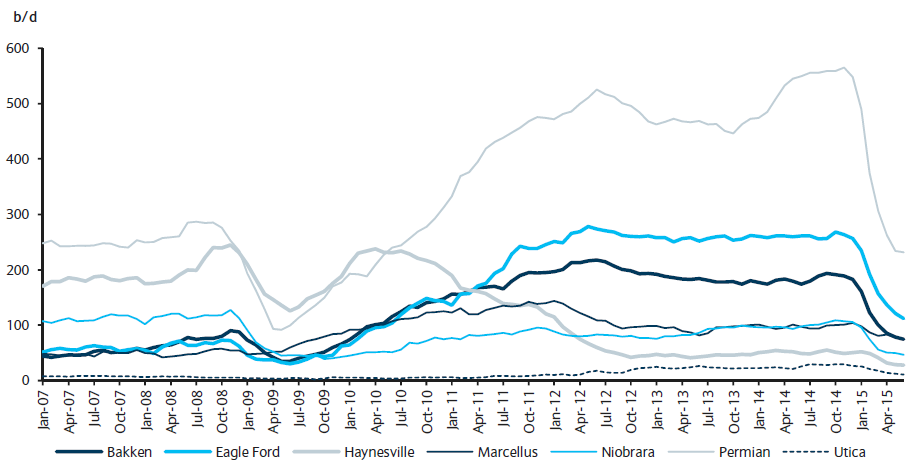

FIGURE 4: US TIGHT OIL AND SHALE GAS REGIONS--RIG COUNT

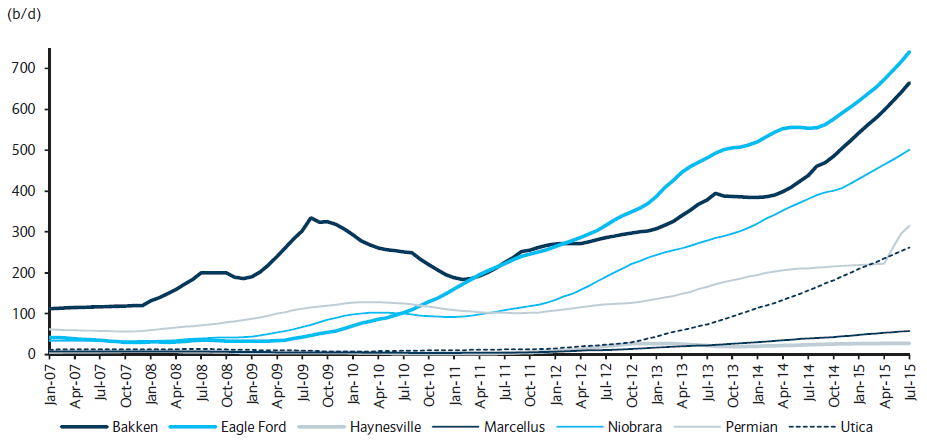

FIGURE 5: US TIGHT OIL AND SHALE GAS REGIONS--PRODUCTION PER RIG

Source: EIA

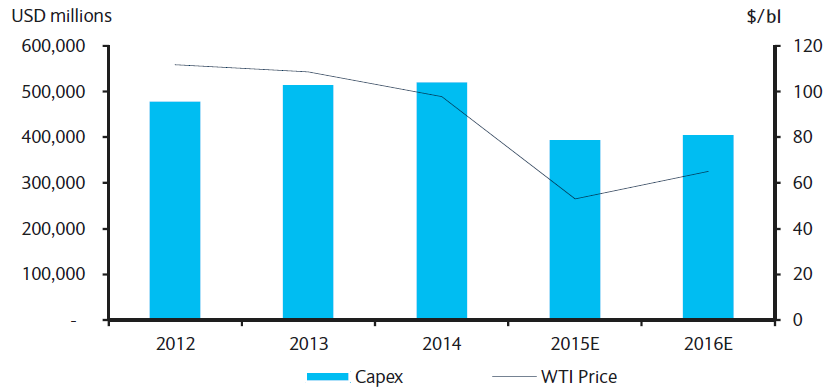

However, as observed in past EVAs, the reality of the fracking boom is that these wells deplete very quickly, like by 80% after the first year. Thus, there needs to be a lot of drilling, or efficiencies, simply to run in place. Also, the global supply of crude runs about 95 million barrels per day (bpd) and there is roughly a 5% depletion rate on that. Accordingly, close to 5 million bpd need to be found just to stay even. Yet, global capital spending is projected to contract by $130 billion this year and that assumes $54 oil not $40! (Incredibly, Canadian crude has fallen to $23 due to pipeline problems; this creates a major opportunity for MLPs that ship Canadian oil sands by rail, including one Evergreen owns for clients that is yielding over 10%.)

FIGURE 6: WORLDWIDE UPSTREAM CAPEX FOR COMPANIES UNDER BARCLAYS' COVERAGE AND WEST TEXAS INTERMEDIATE PRICE

Source: Barclays Research, Company Data

This is not to say there aren’t problems in MLP-land. For sure, distribution growth rates are coming down, in some cases dramatically. However, we believe most of the stronger entities will continue to boost their payouts, even if modestly. The losers in this tougher environment are likely to be the low-yielding general partner (GP) MLPs whose high-prices were based on their fat cut of formerly fast-growing distributions.

This sudden and punishing bear market for MLPs shows what can happen when a prevailing belief system, or narrative, falls apart. As we have commented to a number of clients, if the highest quality MLP enterprise (there’s that hint again) can fall 40%, pushing its yield up to 6% when it bottomed (hopefully) week before last, imagine what can happen to the small cap ETF—yielding only 1.4% and increasingly exposed to outrageously priced small biotech stocks—when it begins to tumble. Presently, the meme of a strong dollar benefiting small caps is dominant but that’s not going to prop them up forever.

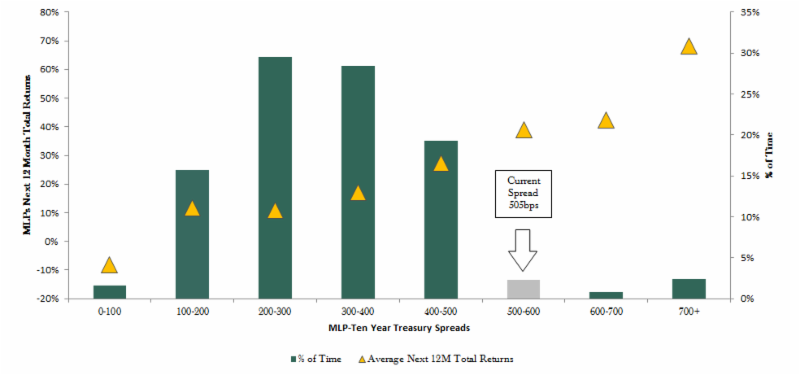

Nor is the much vaunted concept of an equity risk premium (ERP) in a low interest rate environment likely to save the day. The idea with this is that when interest rates are very low, stock prices should be high. Yet, as you can see below, MLPs now yield 500 basis points (5%) more than 10-year treasuries and that hasn’t supported them, until very recently. It is encouraging how rarely this has happened (only about 5% of the time have comparative yields been this high or higher). More importantly, it shows how lofty future returns have been in the past when relative yields have been as elevated as they are now.

FIGURE 7: HISTORICAL MLP YIELD PREMIUM VERSUS 10-YEAR TREASURIES

(Left hand scale is next 12 months return; right hand scale is time within yield spread band; bottom axis is yield differential band or excess MLP yields versus 10-year treasury)

Source: Yorkville Capital

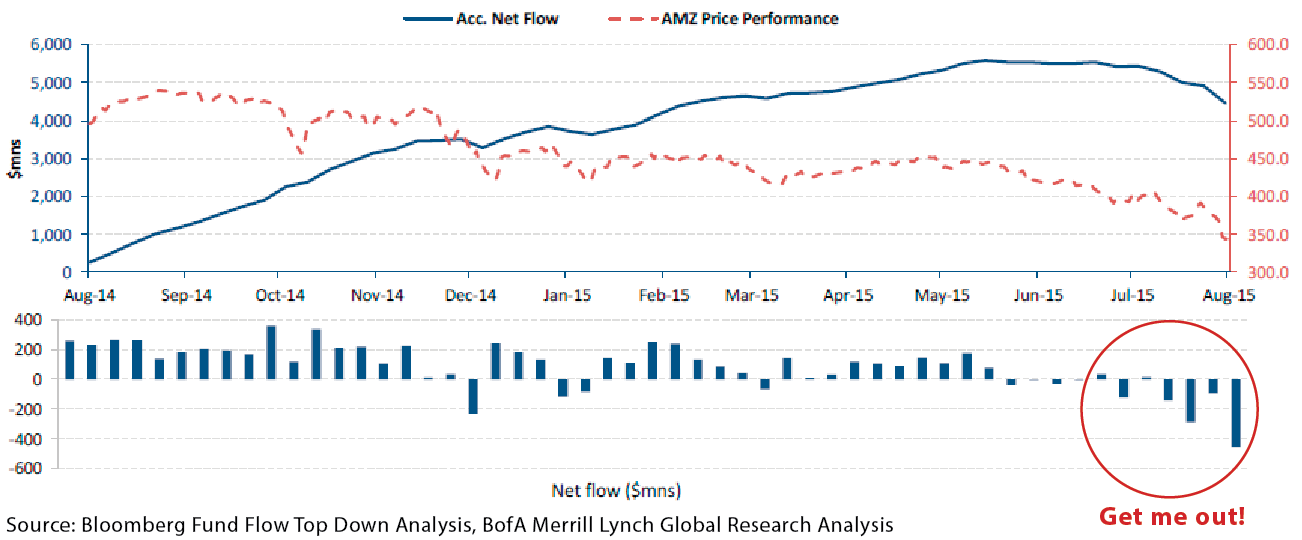

But for those investors on margin or who failed to raise cash when MLPs were flying, what’s happened since last summer isn’t an opportunity—it’s a nightmare scenario. Predictably, they are fleeing in droves and sacrificing the sumptuous cash flows on offer today.

FIGURE 8: MLP OPEN-END FUND FLOWS VERSUS ALERIAN MLP INDEX

Sadly, buying high and selling low is what millions of investors do best. If you believe it will be different with the overall market, I’ve got some oceanfront property in North Dakota to sell you.

David Hay - dhay@evergreengavekal.com

OUR CURRENT LIKES AND DISLIKES

Changes are noted in bold.

DISCLOSURE: This report is for informational purposes only and does not constitute a solicitation or an offer to buy or sell any securities mentioned herein. This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. All of the recommendations and assumptions included in this presentation are based upon current market conditions as of the date of this presentation and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. Information contained in this report has been obtained from sources believed to be reliable, Evergreen Capital Management LLC makes no representation as to its accuracy or completeness, except with respect to the Disclosure Section of the report. Any opinions expressed herein reflect our judgment as of the date of the materials and are subject to change without notice. The securities discussed in this report may not be suitable for all investors and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. Investors must make their own investment decisions based on their financial situations and investment objectives.