“I don't have to tell you things are bad. Everybody knows things are bad.”

-PETER FINCH playing Howard Beale in the 1976 hit movie Network.

By David Hay / CIO, Evergreen Gavekal

Strange bedfellows: angry voters and market highs. It might seem odd, in the midst of the rampant bullishness engulfing markets since the election—and further stoked by Pres. Trump’s enthusiastically received congressional speech this week—to bring up the topic of social malaise. However, since Evergreen investment team members are congenital contrarians, we will do exactly that in this issue of the Gavekal EVA.

It’s actually not that bizarre to delve into this subject considering Mr. Trump was elected in no small part because blue-collar America, formerly rock‐ribbed Democrats, defected to him in droves. These individuals no doubt feel like they have gotten the short end of the globalization stick, and they are not alone.

Many of you probably saw a recent article that roughly half of retiring Baby Boomers have less than $100,000 on which to retire. If this factoid is right—and we’ve seen a number of reports essentially along the same lines—then millions of my generation are in a world of hurt. Based on the immense size and impact of the boomers, this means the world itself will eventually be hurting, too.

Gavekal’s co‐founder and senior partner Anatole Kaletsky authored this month’s featured piece early in the year, before Trumphoria entered hyper‐drive. Consequently, it’s easy to dismiss his points as dated and out of touch with the glittering new order in which we suddenly find ourselves. However, it’s essential not to confuse jubilant financial markets with true solutions to our most vexing societal problems.

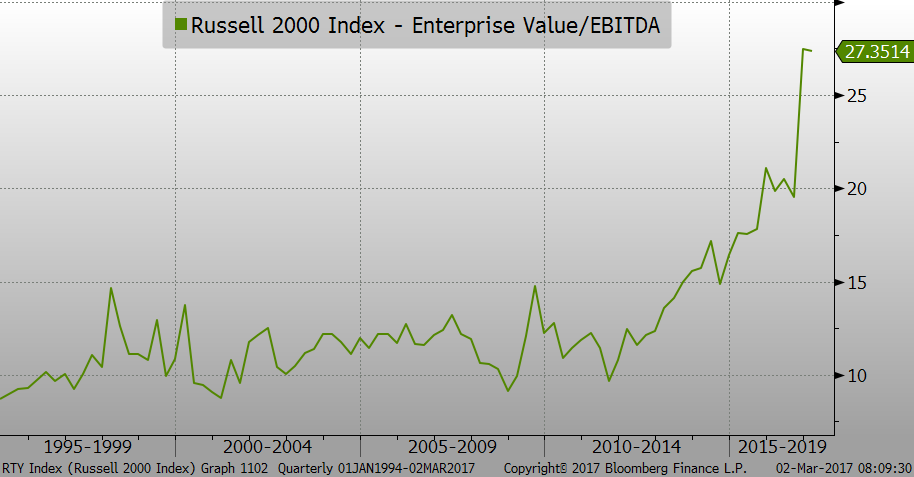

The fact that populist candidates appear to be on the rise in numerous countries is indicative that the forces of discontent supporting them are very much in place. This is quite clearly a “big league” contradiction to the S&P 500’s exuberance, which to our skeptical eyes, is looking increasingly irrational. Moreover, as we’ve frequently expressed in these pages, the Russell 2000 index of smaller companies is in true bubblemania territory.

SMALL CAP INDEX VALUE OF DEBT AND STOCK MARKET VALUE VS. GROSS CASH FLOW

Source: Evergreen GaveKal, Bloomberg

Again, to reiterate for the umpteenth time (an advanced calculus term), there are a number of Mr. Trump’s policies Evergreen has long advocated and thus appreciates. We were also pleased that his congressional speech this week was, by most accounts, of presidential quality and lacked the gloomy tones of his inauguration address. Certainly, the Dow’s 303‐point rally on Wednesday indicated utter ebullience over Mr. Trump’s performance.

If you think there’s a “but” coming, you are spot‐on. While Anatole’s political views are often far removed from my own, I do believe he’s accurately describing the aforementioned dissatisfaction, particularly among middle‐class voters. It’s like that scene in the 1976 cinematic classic Network, which I recently re‐watched, when Peter Finch (a TV anchorman gone rogue) bellows to the world: “I’m mad as hell and I‘m not going to take this anymore!” As you may recall, his rant goes viral, temporarily reviving his once-doomed career. People were scared back in the mid‐1970s and they are scared again.

As Anatole notes in his brief essay, the world was struggling with the breakdown of Keynesian economics in the 1970s, back when Network was a hit film. Up until then, Keynesianism had been the commanding and unchallenged dogma of the day. In fact, it had dominated Western economies and political systems since WWII. As even casual students of modern history know, the discredited Keynesian model was replaced in the early 1980s by supply‐side policies, such as Reaganomics in the US and Thatcherism in the UK. This transition unleashed a new boom that lasted, with minor hiccups, until 2008. The downfall of this paradigm was that four‐letter word highlighted in last week’s Random Thoughts EVA: debt.

The first bill for that debt binge came due during the global financial crisis, which was primarily triggered by the housing bust. Unquestionably, that disaster was a direct function of the exponential growth in mortgage debt, encouraged by misguided government policies and lax regulation. The unwinding of the great Ponzi scheme that was home lending during the first decade of this millennium produced the worst economic contraction since the Great Depression. This left countless millions around the world feeling disenfranchised, confused, and—well—mad as hell.

Capitalism has been proven time and time again to be, by far, the best economic system ever devised. Yet, it has always struggled with equitably distributing the fruits of its awesome output. As Anatole notes, this tends to be a non‐event when times are good. But when the tide goes out—especially when it does so with the speed and force of what happens right before a tsunami—social unrest is almost inevitable. And, per Anatole, that deep dissatisfaction is still out there, despite the stock market’s on‐going ascent into intergalactic space. Further, the transition away from old economic models to new ones—like Trumponomics—is almost always tumultuous, as he observes. In fact, both Ronald Reagan and Margaret Thatcher experienced extremely challenging conditions early in their tenures.

Mr. Trump has shown a remarkable ability to rally enthusiasm—and stock prices—through stirring words about his “phenomenal” tax plan, among other seemingly irresistible proclamations that feed the fire of animal spirits. But soon there needs to be tangible legislation to back up the soaring rhetoric. Mr. Trump must truly believe the devil is in the details because there has been precious few of the latter.

For sure, the late stages of bull markets are fun. But with the stock‐owning percentage of the population in an extended downtrend, particularly among millennials, its spoils are, like so many things these days, most unevenly divided. And that’s not a recipe for long‐term stability, regardless of the message being sent by repeated new highs in the Dow. There are already the largest percentage of males between 18 and 34 living with their parents since 1940, a reality that doesn’t bode well for either future labor force growth or long‐term economic vitality. Further, It’s downright scary to think what that ratio will look like in the next crisis. If Howard Beale was still with us today, you can bet he’d be mad as hell.

THE CRISIS OF MARKET FUNDAMENTALISM

By Anatole Kaletsky

The biggest political surprise of 2016 was that everyone was so surprised. I certainly had no excuse to be caught unawares: soon after the 2008 crisis, I wrote a book suggesting that a collapse of confidence in political institutions would follow the economic collapse, with a lag of five years or so.

We’ve seen this sequence before. The first breakdown of globalization, described by Karl Marx and Friedrich Engels in their 1848 The Communist Manifesto, was followed by reform laws creating unprecedented rights for the working class. The breakdown of British imperialism after World War I was followed by the New Deal and the welfare state. And the breakdown of Keynesian economics after 1968 was followed by the Thatcher-Reagan revolution. In my book Capitalism 4.0, I argued that comparable political upheavals would follow the fourth systemic breakdown of global capitalism heralded by the 2008 crisis.

When a particular model of capitalism is working successfully, material progress relieves political pressures. But when the economy fails—and the failure is not just a transient phase but a symptom of deep contradictions—capitalism’s disruptive social side effects can turn politically toxic.

That is what happened after 2008. Once the failure of free trade, deregulation, and monetarism came to be seen as leading to a “new normal” of permanent austerity and diminished expectations, rather than just to a temporary banking crisis, the inequalities, job losses, and cultural dislocations of the pre-crisis period could no longer be legitimized—just as the extortionate taxes of the 1950s and 1960s lost their legitimacy in the stagflation of the 1970s.

If we are witnessing this kind of transformation, then piecemeal reformers who try to address specific grievances about immigration, trade, or income inequality will lose out to radical politicians who challenge the entire system. And, in some ways, the radicals will be right.

The disappearance of “good” manufacturing jobs cannot be blamed on immigration, trade, or technology. But whereas these vectors of economic competition increase total national income, they do not necessarily distribute income gains in a socially acceptable way. To do that requires deliberate political intervention on at least two fronts.

First, macroeconomic management must ensure that demand always grows as strongly as the supply potential created by technology and globalization. This is the fundamental Keynesian insight that was temporarily rejected in the heyday of monetarism during the early 1980s, successfully reinstated in the 1990s (at least in the US and Britain), but then forgotten again in the deficit panic after 2009.

A return to Keynesian demand management could be the main economic benefit of Donald Trump’s incoming US administration, as expansionary fiscal policies replace much less efficient efforts at monetary stimulus. The US may now be ready to abandon the monetarist dogmas of central-bank independence and inflation targeting, and to restore full employment as the top priority of demand management. For Europe, however, this revolution in macroeconomic thinking is still years away.

At the same time, a second, more momentous, intellectual revolution will be needed regarding government intervention in social outcomes and economic structures. Market fundamentalism conceals a profound contradiction. Free trade, technological progress, and other forces that promote economic “efficiency” are presented as beneficial to society, even if they harm individual workers or businesses, because growing national incomes allow winners to compensate losers, ensuring that nobody is left worse off.

This principle of so-called Pareto optimality underlies all moral claims for free-market economics. Liberalizing policies are justified in theory only by the assumption that political decisions will redistribute some of the gains from winners to losers in socially acceptable ways. But what happens if politicians do the opposite in practice?

By deregulating finance and trade, intensifying competition, and weakening unions, governments created the theoretical conditions that demanded redistribution from winners to losers. But advocates of market fundamentalism did not just forget redistribution; they forbade it.

The pretext was that taxes, welfare payments, and other government interventions impair incentives and distort competition, reducing economic growth for society as a whole. But, as Margaret Thatcher famously said, “[…] there’s no such thing as society. There are individual men and women and there are families.” By focusing on the social benefits of competition while ignoring the costs to specific people, the market fundamentalists disregarded the principle of individualism at the heart of their own ideology.

After last year’s political upheavals, the fatal contradiction between social benefits and individual losses can no longer be ignored. If trade, competition, and technological progress are to power the next phase of capitalism, they will have to be paired with government interventions to redistribute the gains from growth in ways that Thatcher and Reagan declared taboo.

Breaking these taboos need not mean returning to the high tax rates, inflation, and dependency culture of the 1970s. Just as fiscal and monetary policy can be calibrated to minimize both unemployment and inflation, redistribution can be designed not merely to recycle taxes into welfare, but to help more directly when workers and communities suffer from globalization and technological change.

Instead of providing cash handouts that push people from work into long-term unemployment or retirement, governments can redistribute the benefits of growth by supporting employment and incomes with regional and industrial subsidies and minimum-wage laws. Among the most effective interventions of this type, demonstrated in Germany and Scandinavia, is to spend money on high-quality vocational education and re-training for workers and students outside universities, creating non-academic routes to a middle-class standard of living.

These may all sound like obvious nostrums, but governments have mostly done the opposite. They have made tax systems less progressive and slashed spending on education, industrial policies and regional subsidies, pouring money instead into health care, pensions, and cash hand-outs that encourage early retirement and disability. The redistribution has been away from low-paid young workers, whose jobs and wages are genuinely threatened by trade and immigration, and toward the managerial and financial elites, who have gained the most from globalization, and elderly retirees, whose guaranteed pensions protect them from economic disruptions.

Yet this year’s political upheavals have been driven by elderly voters, while young voters mostly supported the status quo. This paradox shows the post-crisis confusion and disillusionment is not yet over. But the search for new economic models that I called “Capitalism 4.1” has clearly started—for better or worse.

OUR CURRENT LIKES AND DISLIKES

No changes this week.

LIKE

NEUTRAL

DISLIKE

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness.