“The world currently has an excess of every manufactured good.”

-JOHANN RUPERT, CEO of luxury consumer products company, Richemont.

“Clearly, our consumers’ budgets are pinched.”

-Dollar General CEO, TODD VASOS

First of all, Evergreen would like to wish all of its clients, friends, and EVA readers a Merry Christmas and an abundantly happy Holiday Season. Considering how 2016 started out, with stocks plunging and credit spreads soaring, we should all feel exceedingly grateful that it’s turned out to be a nicely profitable year for US-focused investors.

Evergreen definitely has an “attitude of gratitude” for the tremendous reversal of fortune the energy sector has enjoyed from the depths of early February. As most EVA readers are aware, we were adamant that energy stocks and bonds offered massive upside after the pasting they experienced from the summer of 2014 into the start of this year. Frankly, we have been pleasantly surprised by both the speed and power of their resurgence. We believe there is more upside ahead in 2017, particularly with the high-income mid-stream energy infrastructure (MLPs) securities. Despite their monster recovery, master limited partnerships remain down 42% from their 2014 highs.

There’s a lot to cover in this Random Thoughts edition so let’s get to it!

Last week was one of the busiest of the year for your occasionally overwhelmed EVA scribe. Consequently, I neglected to create a summary for last week’s issue. Please accept my apologies. The following recaps the key points of today’s issue and, as usual with our Random Thoughts edition, it’s easy to jump to the section, or sections, you care about most and skip those that fail to pique your interest.

BONDS:

-Investors are increasingly stressed-out about the recent extreme weakness in bonds. Often, when anxiety reaches this intensity level a turnaround is close at hand.

-Market sentiment toward fixed-income has rarely been as negative as it is now. Along similar lines, the Bloomberg Relative Strength Index for bonds is at 40 year lows.

-Fortunately, credit spreads* have been well-behaved, allowing non-government bonds to hold up better than treasuries.

INFLATION:

-It’s tough to experience a major bear market in bonds when CPI readings are as subdued as they are presently.

-To the extent inflation has up-ticked of late, this is a function of oil prices rising from very depressed levels a year ago. The CPI excluding energy is running at about 1 ¾% and falling.

-Low capacity utilization in the US and a rising dollar should serve to keep price increases tame.

SOLAR:

-Due to the collapse in solar equipment prices, “sun-power” is becoming competitive with fossil fuels, even on a non-subsidized basis. This is particularly true in the developing world. China has installed enough solar capacity to power nearly 100 million homes.

-However, solar stocks have mostly been a sink-hole for investor wealth over the past decade. Plunging panel prices, especially from China, have caused severe pain and, even, bankruptcies for US solar companies.

-Evergreen believes it has identified a safe-harbor in this treacherous space. Solar “Yield Companies” are structured similar to MLPs (master limited partnerships) with extremely predictable long-term cash flows. Current prices seem unfairly depressed and present yields excessively elevated, considering what we believe to be modest risks.

THE US ECONOMY:

-Evergreen came close to making a recession call this fall, the first since the autumn of 2007. Since then, US (and worldwide) economic data has perked up.

-However, growth estimates for US GDP this quarter and the first quarter of 2017 have recently been reduced to sub-2%. So, although recession risks have receded for now, the economy remains quite sluggish.

-Between an elevated US dollar and rising interest rates, the total drag on America’s economy could approach 3% or around $550 billion. The downward pull from these factors are serving as offsets to the greater business and investor confidence in future growth seen since the election.

*The yield gap, or spread, between government and corporate bonds. When this widens significantly, private-sector bond prices typically decline, often precipitously

Gentlemen (and women) don’t prefer bonds. When the phones start ringing off the hooks around Evergreen, with clients calling in a mild state of alarm, we have found that we must be quite late in a particular panic cycle. That has certainly been the case lately regarding interest rates and their impact on bond portfolios.

While we do hold a large number of bonds for our clients, we’ve actually had it pretty easy considering that 10-year treasury rates have basically doubled in six months. For sure, the move from 1.3% to 2.6% isn’t as painful as going from, say, 3% to 6%. Regardless, it’s a stunningly rapid and significant increase.

What has made this just mildly uncomfortable for Evergreen is that we have substantial cash reserves for almost all clients. We also hold a number of floating rate bonds which have actually risen in value during the bond market rout. Additionally, most of our corporate debt securities are in the BB-rated category with relatively short-term maturities. These have maintained their values far better than have 10-year treasuries. Finally, we had substantially reduced our longer treasury holdings when yields were at lower levels.

Nonetheless, our income portfolios overall have seen a small erosion in value even as the stock market has been making new highs. This is always a tad discomfiting since clients tend to focus far more on the equity markets than they do on the debt markets—even if most of their investments are yield-oriented.

This is the fourth episode over the last five years or so in which bond investors have gotten their knickers in a twist. The first was in 2011 when America’s credit rating was downgraded and Europe looked set to implode. The next was in 2013 during the infamous “Taper Tantrum”. The third started in the fateful summer of 2014 and continued into February of this year, caused by a pronounced widening in credit spreads. The fourth panic period, of course, erupted after The Donald became the president-elect.

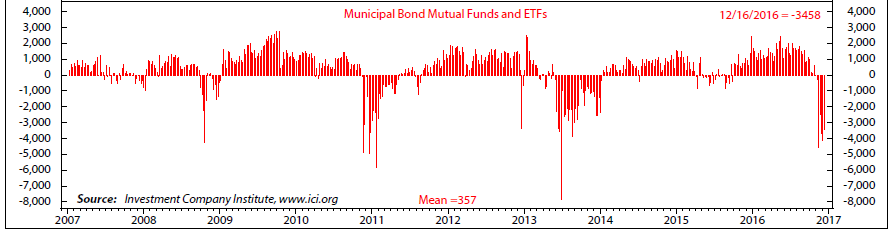

Market pros refer to dramatic and unexpected developments as Black Swans. For bond investors, what has happened since November 8th could be considered an Orange Swan, in honor of Mr. Trump’s nearly neon-hued flowing mane. Bond market participants have reacted by bailing out of debt funds and securities at a frenetic pace. Munis have been particularly pummeled due to the double whammy of higher interest rates and presumed lower tax rates. As you can see below, redemptions from tax-exempt funds are rapidly approaching the intensity seen during the taper tantrum. Interestingly, those outflows have been even more extreme than during the global financial crisis, when portions of the municipal bond market literally froze.

FIGURE 1: MUNICIPAL BOND FUNDS AND ETFS  Source: Ned Davis Research

Source: Ned Davis Research

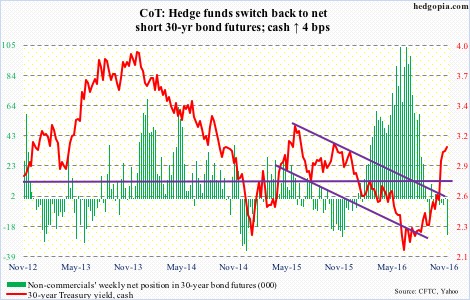

A discerning observer would quickly ascertain that each one of those bail-out moments was a stellar buying opportunity. The same has also been true with long-term treasuries whenever the hedge fund community has turned ultra-negative on them. As you can also see, “hedgies” are almost at a maximum bearish level. And the net speculative short position on the 10-year T-note is simply shocking.

FIGURE 2: LOVE ‘EM HIGH; HATE ‘EM LOW Source: Hedgopia

Source: Hedgopia

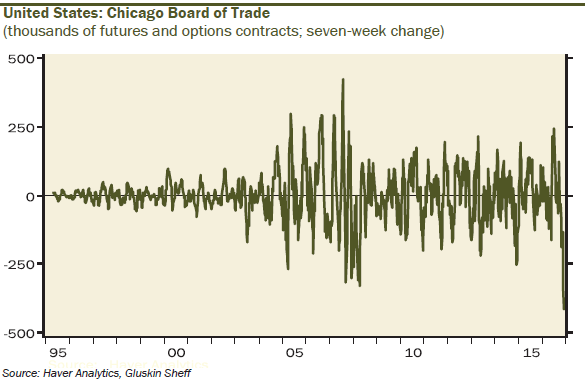

FIGURE 3: NET SPECULATIVE POSITION Source: Haver Analytics, Gluskin Sheff, Breakfast with Dave

Source: Haver Analytics, Gluskin Sheff, Breakfast with Dave

Moreover, David Rosenberg—Canada’s most influential economist and a card-carrying contrarian—recently pointed out that the Bloomberg Relative Strength Index on bonds is at 17.5, with anything below 30 being oversold. The sub-18 reading is the lowest this measure has been in over 40 years. And believe me, as one who has been involved in the bond market for about 38 of those 40 years, there have been some terrifying fixed-income sell-offs during that time-span.

Additionally, as David further observers, a mere 6% of portfolio managers see lower bond yields in 2017. Similarly, 58% of asset allocators are underweight fixed-income. Yet, net debt issuance in developed countries during 2017 may be the lowest in 25 years, as a result of on-going central bank bond buying.

My money, literally, is on a bond market bounce, likely a snazzy one. In the Evergreen view, the usual year-end “portfolio primping process”—whereby losers are belatedly jettisoned and in-vogue issues are hastily added—is aggravating the bond weakness. Tax-loss selling in the waning days of the year is undoubtedly a depressing factor as well.

Whether we are setting up for a short-term rally within the context of a new bear market in bonds or a more lasting recovery, such as we’ve repeatedly seen for the last 35 years, is unclear at this point. But a key factor in that decision-tree is likely to be a function of the next section.

Inflation obsession? Okay, this isn’t much of a random shift since it is such a crucial and related topic when it comes to bonds. But we haven’t written on inflation in quite awhile, mostly because it’s been such a non-event. Lately, though, there are mounting fears that it’s ready to rumble.

What’s fascinating about this anxiety is that only the bond market seems to be suffering from its effects. Yet, history is high-def clear that stocks also don’t like a major spike in consumer prices. At this point, as we have repeatedly noted when similar inflation-phobia has arisen in the past, we think it’s another case of much ado about very little.

Most of the inflation angst emanates from the aforementioned Orange Swan (by the way, I can’t take credit for that nifty term). Assumptions are rampant that fiscal profligacy caused by both “big-league” spending and radical tax cuts will cause inflation to do a ‘70s replay. Since we don’t know what future policies will look like, this is a tough one to handicap. But influential GOP members of Congress, like Mitch McConnell, are making it clear they won’t allow a red-ink blow-out.

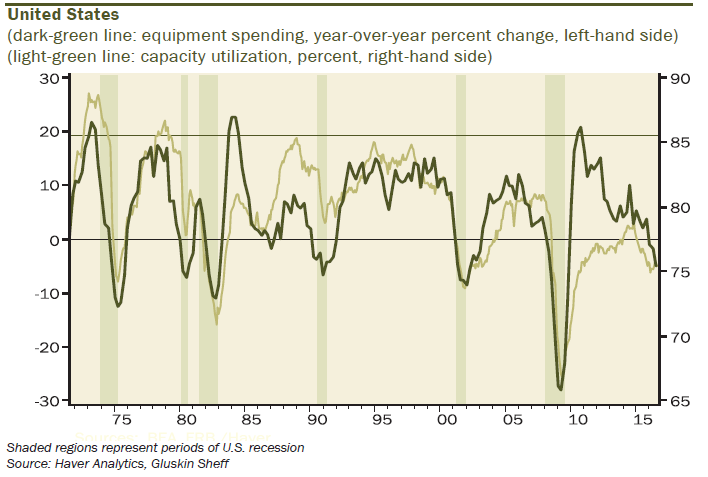

In the here and now, we have a situation where capacity utilization is around 75%, down from near 80% at the peak of this expansion. As Gavekal’s Steve Vanelli has pointed out, this level of factory usage was hit during the recessions of 1982 and 2002. In other words, it’s a very weak reading that is totally inconsistent with rising inflation.

Another reason to be less than frazzled about this threat is the continuing break-out by the US dollar. We highlighted the importance of the 100 level on the dollar index in the November 18th EVA. After decisively penetrating that resistance, the greenback has continued rising, recently hitting a 14-year high. This lowers the cost of imports and, hence, is most disinflationary.

A further rationale for why inflation is unlikely to erupt anytime soon is the labor market. It’s true that the unofficial unemployment rate is rock-bottom currently. However, as most of us know, that’s a direct result of so many Americans being out of the work force. Presently, there are around 95 million folks of an employable age who aren’t. This includes 23 million in the prime working age-bracket of 25 to 54.

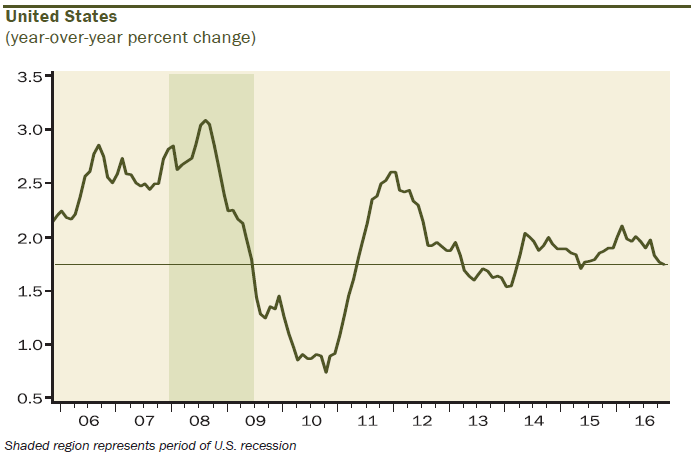

This soft under-belly of the labor market is showing up in less than roaring wage increases. While pay is rising, it’s doing so at a sedate—and recently easing—clip. In the most recent report, the year-over-year rate of increased faded from 2.8% to 2.5%.

FIGURE 4: TOO MUCH SPARE CAPACITY

Source: Haver Analytics, Gluskin Sheff, Breakfast with Dave

Additionally, if you look at the CPI excluding health care and shelter costs, an extraordinarily subdued picture emerges. Per figure 5 below, it is running below one percent. We are in the camp that believes medical and housing expenses are essential items and as these escalate they drain spending potential from more economically supportive purchases such as of appliances and cars.

FIGURE 5: US CPI LESS SHELTER & MEDICAL CARE Source: Gavekal Data/Macrobond

Source: Gavekal Data/Macrobond

Similarly, the CPI excluding energy is extremely subdued (oil prices are up dramatically from a year ago (fortunately!) distorting the official inflation number). As David Rosenberg further observes, both headline and core inflation will probably peak at their lowest points since the 1950s.

FIGURE 6: CPI EXCLUDING ENERGY

Source: Haver Analytics, Gluskin Sheff, Breakfast with Dave

US-based economist Gary Shilling—who has been much more accurate than nearly all of his peers for decades about inflation, or, rather, the lack of it—has an interesting view on the topic. He notes that throughout the history of the US, whenever we are at peace, inflation stays contained. One could argue that we’re in a constant state of low level war on terrorism but he believes we’ve ratcheted way down from when we were funding dual budget-busting wars in Iraq and Afghanistan.

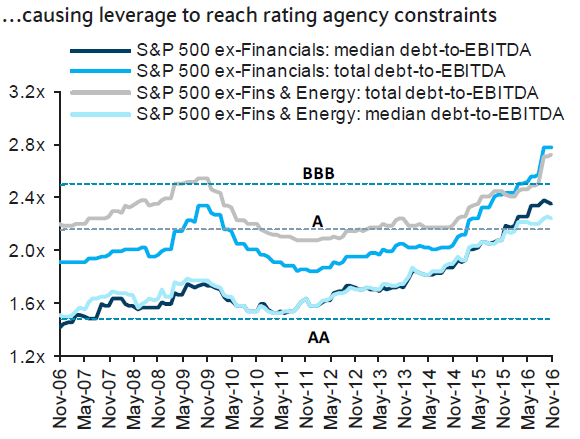

In addition to Gary Shilling remaining totally unconcerned about an inflation revival, my partner and mentor Charles Gave recently wrote: “Let me be clear: there is absolutely no inflation risk in the US economy.” Actually, he’s becoming increasingly apprehensive that rapidly rising interest rates could trigger a US recession next year (more on that in a bit). This is particularly a risk given how much Corporate America has leveraged up, mostly to buy back their own shares at higher and higher prices.

FIGURE 7: CORPORATE AMERICA: PUTTIN' ON THE DEBT! Source: S&P 500, FactSet, Barclays Research

Source: S&P 500, FactSet, Barclays Research

Ergo, for now, there are a lot of things to worry about in this day and age but inflation isn’t one of them.

Let it shine, let it shine, let it shine. Evergreen has long believed that solar will ultimately be the planet’s dominant energy source. However, for years, investing in solar stocks has been an exercise in frustration, if not impoverishment. Despite solar power’s exponential growth over the past decade, the Solar ETF has returned a shockingly negative 62% since 2005. It’s reminiscent of Warren Buffett’s comment about airlines stocks a number of years ago, pointing out the investment return on them since the invention of flight was roughly zero. The Oracle of Omaha quipped that based on how horribly they were destined to perform over many decades—despite equally exponential growth in air travel—airline investors would have been wise to shoot down Orville and Wilbur Wright’s first plane over Kitty Hawk.

Solar companies have also struggled to attain consistent profitability, much less reliable growth, for a number of reasons but we’d speculate to say that most of their travails come down to one word: China. Chinese solar companies became a global force in the production of solar equipment about a decade ago. After some stunning initial success, however, the sector has been far from a shining example of prosperity. This is despite the fact that China has installed 136 gigawatts of solar capacity—enough to power almost 100 million homes—over the last 10 years.

But what they have truly excelled at is crashing the price of solar equipment, notably of the increasingly ubiquitous panels that you see on roof-tops, particularly in the Southwestern US. This price cliff-dive forced some American solar manufacturers into bankruptcy including the now-infamous Solyndra, so heavily backed by the US government. (That disastrous investment cost US taxpayers a not-to-so cool $525 million, by the way.) Even the once-promising Sun Edison, had to seek refuge in Chapter 11 despite having a market value of $10 billion as recently as mid-2015!

The good news for this beleaguered sector is that panel prices have come down so far that solar is fast approaching the holy grail of “grid parity” in many regions. This means that solar is essentially cost-competitive with traditional sources of electricity production even without government subsidies. This is particularly true in developing countries that lack the sophisticated energy production and distribution infrastructure that the US and other developed nations possess. In Chile, for example, a deal was recently inked to provide solar-generated power for just $29 per megawatt hour (under 3 cents per kilowatt hour), about half what coal would have cost.

China, naturally, is one of the emerging world’s leaders in putting photovoltaic power, as solar is also known, into operation. The more panels are manufactured, the more the price tumbles, a truly virtuous circle—unless you’re a producer of this equipment. To say that it’s been hard to find a solar company with a defensible competitive “moat”, is like saying it’s a tad challenging to find affordable housing in the Seattle area these days. (Prices are now above their 2007 bubble peaks!)

Evergreen, though, believes there are winners in this brutally Darwinian process. It may come as no surprise to long-time clients and EVA readers that we have been moving into the MLP equivalent in the solar space. These are known as “Yield Cos” (i.e., Yield Companies) that own and operate renewable energy facilities. These are typically solar-powered but some involve wind-turbine “farms”. Undoubtedly, you’ve seen the huge windmills that operate in some of our country’s windier areas, such as in the mountain passes east of LA or in the deserts of West Texas.

Unlike MLPs, the Solar/Wind Yield Cos don’t generate K1s. On the other hand, their tax shields on payouts may not be as great, though distributions should be preferentially taxed. Cash flow returns are in the 5 ½% to 8% range, comparable to MLPs, and the Yield Cos have grown distributions respectably since they began to go public back in 2014. Part of the reason for the high current yields is that they are out of favor, partially due to the election of Donald Trump and his clear preference for fossil fuels, with share prices down 40% to 50% from their 2015 high points.

As we’ve previously written, we are grateful for the friendlier attitude toward domestic oil and gas production and transportation, given our extensive MLP exposure. However, we also believe the future is nearly certain to bring an increasingly electrified auto fleet. For the next few years, those vehicles will be largely charged off the existing grid, where natural gas is now the primary power source, having recently surpassed coal. But, longer-term, we believes millions of Americans will be using solar power to charge their electric cars, either from the local utility (which may receive the power from the aforementioned solar farms) or rooftop panels.

Admittedly, the Yieldcos are a bit of a chicken way to play the tremendous growth potential of solar. But we sure like the eggs they produce on a quarterly basis!

A close almost call. A few months back, Evergreen came close to calling that the odds favored a US recession in 2017 for the first time since the fall of 2007 when we went against the consensus to forecasts a downturn in 2008. Fortunately, recent economic data has been mostly on the bouncier side, leading us to downgrade the chances of a contraction next year.

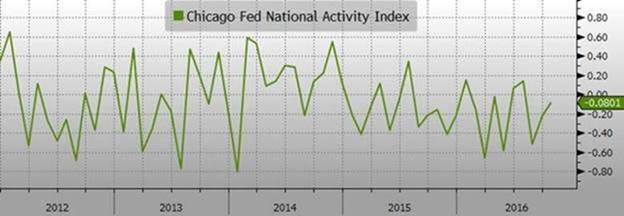

One of the most comprehensive measures of the health of the US economy is the Chicago Fed’s National Activity Index (NAI). The Chicago NAI is comprised of 85 high-frequency indicators, meaning the Index is sensitive to short-term shifts in economic activity. The most recent report perked up to a three-month high with 50 of the components showing improvement. This is consistent with various Purchasing Manager Index (PMI) releases—one of the most important trackers of economic vitality—that have also shown a better tone of late.

FIGURE 8: NAI: LATELY, MORE OF A YAY THAN A NAY Source: Evergreen Gavekal, Bloomberg

Source: Evergreen Gavekal, Bloomberg

FIGURE 9: US MANUFACTURING PMI

Source: Evergreen Gavekal, Bloomberg

FIGURE 10: US SERVICE-SECTOR PMI

Source: Evergreen Gavekal, Bloomberg

Globally, it’s the same message, with even long-comatose Europe showing signs of resurgence.

FIGURE 11: EUROPEAN MANUFACTURING PMI

Source: Evergreen Gavekal, Bloomberg

FIGURE 12: EUROPEAN SERVICE-SECTOR PMI

Source: Evergreen Gavekal, Bloomberg

This all encouraging to see but at the same time some influential sources are slashing GDP estimates for both this quarter and the start of next year. For example, the New York Fed has lowered its expectations to just 1.83% for this quarter (one simply has to chuckle about the pretension of precision shown by the second decimal point!). Perhaps even more surprising, it also slashed its first quarter 2017 GDP number to 1.7% from 2.4%. In other words, if the NY Fed is right, we’re back to the same snail’s pace we’ve been “running” at for most of this low-energy expansion, after a brief pop above 3% in Q3. (Though, as noted in prior EVAs, this was flattered by some unusual items, with the actual rate likely closer to 1 ½%.)

Of course, the post-election optimism about the future may render these forecasts obsolete. That’s certainly what the stock market is banking on with its charge toward 20,000 on the Dow. But let’s not overlook the negative impact from the higher dollar and the near doubling of the 10-year treasury rate.

Bloomberg Business Week estimates the rise in the dollar since the election represents almost a ½% GDP drag (about $75 billion). Also from David Rosenberg—citing an analysis by Peter Boockvar, the Lindsey Group’s Chief Market Analyst—a 100 basis points (1%) increase in market rates pushes up America’s interest costs by nearly $500 billion. This amounts to a whopping 2.5% drag on GDP. Now, this may be an over-estimation since not all rates are immediately re-set to reflect the 1.3% increase in the 10-year T-note. But if rates go higher and stay there for awhile, the impact may end up being that severe.

At this juncture, our view is that we are in a major tug-of-war between the downward pull from higher rates and an uncompetitive US dollar vs. the soaring “animal spirits” due to Mr. Trump’s election (as hard as the latter is to swallow for many Evergreen clients and EVA readers; but it is a reality). Time may be the deciding factor, as earlier EVAs have contended. The negative impacts from higher rates and the rising dollar hit almost immediately while the potential benefits from lower taxes, regulatory reform, and any infrastructure blitz will be realized over a multi-year period. Only time will tell which side will win this epic battle, but thinking realistically about the uncertainties involved is, in our view, not a matter of being chicken but, rather, appropriately prudent.

David Hay

Chief Investment Officer

To contact Dave, email:

dhay@evergreengavekal.com

OUR CURRENT LIKES AND DISLIKES

One change in bold below.

LIKE

NEUTRAL

DISLIKE

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness.