Click here to view EVA in PDF form.

“There’s no harm in hoping for the best as long as you’re prepared for the worst.”

- STEPHEN KING, author of The Shining and The Shawshank Redemption

Evergreen initiated a slightly modified version of its annual forecast EVA just over a year ago. We shifted from specific predictions to attempting to identify developments that could catch the investment community off-guard. As we noted at the time, this was an unabashed imitation of what Blackstone’s Byron Wien has done for years (including when he was Chief US Investment Strategist for Morgan Stanley). However, we also did this because it is the most unanticipated events that have the greatest market impact.

Whenever this type of approach is used, there are going to be a number of misses, as Mr. Wien himself has long acknowledged. The positive aspect, though, is that because unexpected outcomes are, by definition, contrary to what most investors are positioned for, the damage is typically minimal if you are wrong. Conversely, if you are right, the rewards are typically significant.

Last year, a good example of that latter point was energy-related. Evergreen was one of the lonely bulls on oil and, particularly, master limited partnerships (MLPs, those entities that operate mid-stream energy assets such as pipelines and storage facilities). Due to a disastrous 2015, nearly all things connected to energy had experienced devastating declines, including the normally defensive MLPs. Yet, as we thought might occur, MLPs and the energy sector in general was among the best performing asset classes of 2016. Frankly, MLPs did even better than we had hoped (and prayed!), but we definitely got the direction right.

On the other hand, one of our worst “unexpected outcomes” was that the US stock market might rise or fall more than the 10% to 15% expected by the consensus of Wall Street strategists. It was our suspicion that if this was the case, a big decline was more likely than a 20%-plus type rally. But the Street seers pretty much nailed it, as the S&P finished up 12%. However, by being overweight out-of-favor securities like energy, Evergreen portfolios had a strong year.

Certainly, one of the biggest shockers of 2016—if not THE biggest—was Donald Trump’s election. We didn’t venture into the political realm a year ago but, if we had, it’s unlikely we would have brought that up even as an extreme long shot. At this stage, though, his impending presidency has set the stage for what could be another year that turns out as improbable as a Netflix political thriller. (To review last year’s potential Surprise EVA, please click here.)

Unexpected Outcomes summary:

1. The Fed actually raises rates three times, hitting their forecasted hike target for the first time since the Jurassic Era. There is even a decent chance they exceed three bumps.

2. If the Fed does surprise on the upside, the stock market is likely to struggle--maybe a little, maybe a lot. But with valuations among the highest of all time, it’s wise to consider the “a lot” scenario, even though Wall Street accords that nearly a zero probability.

3. The most comprehensive tax reform since the mid-1980s actually happens. This provides a long-term boost to US economic growth. However, some aspects have negative repercussions initially, particularly with regard to stock buy- backs.

4. After a boffo 2016, despite suffering mightily in the wake of Trump’s triumph, gold mining stocks enjoy another surge. This is likely to be delayed until later in the year, when the US dollar might be forced down by global central banks (see item 9 below).

5. Oil, so detested a year ago, is now much too popular, at least on a near-term basis and taking into account still enormous inventory overhangs. Consequently, crude sells off 15% to 20% early in the year, flummoxing the bullish consensus, before stabilizing as sentiment turns against it once more. Later in 2017, it stages another surprising rally, wrong-footing those who buy into (or should I say, “sell into”) the never-ending-glut scenario yet again.

6. Assuming the Fed tightens repeatedly, a serious shocker could be the bond market. Most investors seem to believe rising short-term rates will lower longer-term bond prices, raising yields. Thus, the majority could be caught off-guard if the 10-year T-note trades in a yield range of 2% to 2.7% even as the Fed hikes multiple times, flattening the yield curve.

7. Based on the stock market’s celebration of Trump’s election, it’s clear it believes his policies will be extremely equity-friendly. But what could throw the consensus for a loop would be if the Trump-related surge in “animal spirits”, benefits the real economy while creating problems for the financial markets. If so, it would be the inverse of what we’ve seen for most of this anemic economic expansion.

8. Hopes are high that Mr. Trump is the next Ronald Reagan. A most unexpected outcome would be if, instead, he comes to increasingly resemble Italy’s former Prime Minister Silvio Berlusconi. The parallels between the two tycoons are striking but, hopefully, for the good of the country, this potential surprise doesn’t materialize.

9. Our penultimate possible curveball would be if the dollar strengthens enough that it causes global central banks to weaken it in concerted fashion via another Plaza Accord. (This was the agreement in the mid-1980s that brought the soaring Reagan dollar back down to earth.) It will likely take an upside burst by the dollar greater than what market participants are currently expecting in order to trigger such a reaction. If so, emerging markets could surprise the investment community by being star performers in the second half of 2017.

10. In France, soaring confidence, after decades of relentlessly rising socialism, unleashes an economic renaissance thanks to a Reaganesque political figure. The French stock market stuns investors by being one of the best performers of 2017.

1. One of our better unexpected outcome calls from last year was that the Fed might fall woefully short of its self-proclaimed goal of four rate hikes in 2016. In reality, they managed just one, right at year-end. In fairness, we had speculated our cherished central bank might actually do a “volte face” and join its fellow monetary mandarins—as Jim Grant refers to them—in moving toward negative rates, if the economy tumbled into an actual recession. Fortunately, the US economy continued to limp along and, to its credit, overcame some serious shock waves, particularly early in the year when oil prices were tanking and credit spreads were spiking.

But now we are taking the diametrically opposed view and hypothesizing that the Fed may actually not only fulfill its stated objective of hiking three times this year but might even exceed that goal. We haven’t felt this way in about twelve years; ergo, we don’t float this notion out there lightly. But due to the election of Donald “The Twitter-meister” Trump, it’s a whole new ball game.

Janet Yellen realizes she’s a lame duck Fed chairwoman and, as a result, she’s got very little to lose in erring on the aggressive side. If she does, she can somewhat justifiably point out that she found monetary rectitude before her term expired, giving her successor plenty of latitude to cut rates in the next crisis/recession. (A caveat here is that, should something truly bad happen, the tightening cycle will almost certainly be aborted, if not permanently halted.)

Ms. Yellen can also cite the surge of confidence that Mr. Trump’s election has produced in the financial markets and the real economy (CEO and consumer surveys are both revealing an undeniable outbreak of optimism).

Additionally, she can most legitimately point out that, based on the $3 trillion or so of high-powered money the Fed has dumped into the financial system since 2008, if this new-found confidence leads to an upturn in the long-falling velocity of money, "Katie bar the door". That would be the door possibly leading to a 1970s-type inflation outbreak. And that’s definitely not something Ms. Yellen would want to see in her biography when people google her on Wikipedia ten years from now.

Therefore, potential shocker numero uno is that the Fed actually raises rates as much as they have said they will—possibly even more—for the first time in the post-crisis era.

2. Our worst suggested surprise from last year may have been, as acknowledged in the introduction, that the stock market would either exceed the consensus view of a 10% to 15% gain or, more plausibly, do worse than that, possibly much worse. Instead, in a rare occurrence, the Wall Street strategist community was essentially dead on the mark.

Once again, they are forecasting solid, though more muted returns, in the 5% to 10% range. And, also once again, we take issue with that sanguine outlook. (As a reminder, they had a healthy market view for 2015 as well when the market was basically flat, with serious below-the-surface damage. Bonds outperformed stocks that year, as we had forecast, contrary to the majority view.) Thus to qualify as a true surprise, stocks will need to do much better or materially worse than plus 5% to 10%.

Considering Wall Street’s new-found love of Trumponomics, one needs to give the upside scenario a decent weight. Working against this outcome are exceedingly elevated valuations. As most EVA readers know, stocks are about as pricey as they have ever been, in some cases—such as based on the median price-to-sales ratio—the highest in history. But could they continue higher, despite this reality? Of course! Is that the most prudent way to invest? Of course not!

If we are right about the first potential shocker—multiple Fed rate hikes—that might be enough to bring this seemingly eternal bull run to a screeching halt. One of the more tried and true market axioms is “three steps and a stumble”. This means that once the Fed has raised rates three time, stocks tend to do a face-plant.

However, it could be that when the tightening process starts at such a low level, it might take five or six hikes before they provide the pin prick. Naturally, that’s impossible to know for sure. This is another example of how the old rules may not work like they have in the past in this bizarre new world of extreme central bank policies.

It’s possible, though, that higher rates could combine with our next potential surprise to create a double-whammy for those that believe bear markets have become extinct.

3. It’s been 30 years since the US has had truly meaningful tax reform. After such a long period of stasis, it’s understandable if Americans are doubtful 2017 will bring dramatic changes to the tax code. But there does seem to be bipartisan support for major revisions. Moreover, the House/GOP version for corporate tax reform has gained President Trump’s endorsement.

Considering the strong stock market action of companies perceived to be winners under the proposed changes—and the lagging action of those thought to be losers—it wouldn’t be a total surprise if the legislation passes. But what does seem to be materially under-appreciated is the potential for debt to lose its tax-preferred status.

As alluded to in the January 6th EVA, the corporate tax reform package would eliminate the deduction for debt issued after a certain date and, possibly, for all debt outstanding. Personally, I doubt it will be the latter but, even if not, making new debt non-deductible has the potential to cause share buy-backs to look much less appealing to senior management. This is despite the benefits to their stock options! Since companies repurchasing their own shares has been the main driver of stock prices in recent years, this has the potential to be a rude awakening for all those assuming it’s business as usual for buy-backs.

As you may be aware, even cash-rich companies have resorted to debt issuance in order to finance share repurchases. In many cases, this is because their cash is trapped overseas due to the high tax cost of bringing it home. The January 6th EVA also addressed why Corporate America may prefer to pay down debt with most of the money that may be repatriated from overseas should tax-reform provide a lower rate to do so, as is widely assumed.

If interest rates are also rising, at least on shorter term debt, that would be another reason companies might be much less active on the buy side. This is something very few are commenting on in their year-ahead forecasts—which is why we believe it is a potential unexpected development worth pondering.

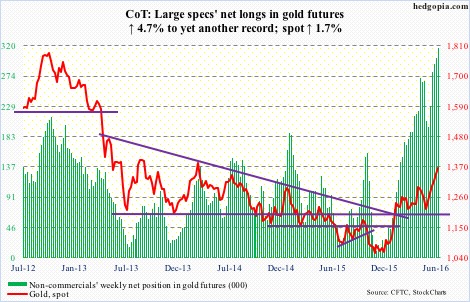

4. Surprises tend to have a negative skew to them when prices are stretched. Call it the curse of Great Expectations. But not all realms of the financial markets are overvalued and in-vogue. Probably our best against-the-grain anticipation a year ago was for commodities to rally hard after a likely rocky start. We particularly thought the long-suffering gold miners might catch the markets off-guard by surging far more than the metal itself, which we also felt was due to outperform.

After falling 9% to start the year, the ETF of senior gold-producers mounted a rally for the ages, rising 145% by July. The junior miners ETF did even better, exploding 186% from its January low point. The move was so powerful that we suggested taking profits, despite our belief that ultimately gold will trade much higher than its summer apex of $1350 an ounce.

Leading us to additionally believe it was time for profit-taking was the fact that speculative bullish sentiment on gold last summer became feverish. Such lopsided optimism is almost always a serious red flag and this time was no exception.

FIGURE 1: source: CFTC

source: CFTC

Now, however, sentiment has gone full circle, back to the despondency of a year ago. Consequently, we believe another rally may be in the offing for gold as well, as those that find and produce it. Based on how out-of-favor bullion and the miners are presently, that certainly would qualify as a major surprise.

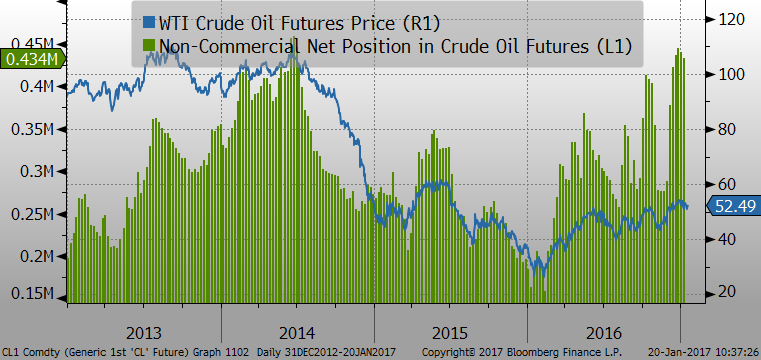

5. The next one is a toughie for us based on our long-term expectation that oil might hit $100 by 2020. A year ago, as also noted in our intro, another of our other best surprise candidates was energy. It was thoroughly detested after having gone through one of its worst bear markets starting in the summer of 2014. During this sickening slide, crude prices were slammed by 75% by the time they bottomed in February of last year.

As was the case with gold, speculative sentiment was ragingly bearish as reflected by almost non-existent bullish position in oil futures at the time.

FIGURE 2: source: Evergreen Gavekal, Bloomberg

source: Evergreen Gavekal, Bloomberg

And, as also happened with the yellow metal, this highly negative positioning was dead wrong, as were all the calls for oil to trade to $10. (Remember those? For some strange reason, these voices have all gone silent.)

The problem is, now the tables have turned completely. The speculative open interest is just as ragingly bullish, as you can see in Figure 2 to the far right. There is also widespread confidence in OPEC’s ability to cut production in a meaningful way. Our view is that the Saudis will give it their best shot, but we’ve got much less confidence in the rest of OPEC’s members adhering to the agreed upon reductions. Russia, not part of OPEC, has also pledged to curtail output. Yet, as Churchill once said, that country is a riddle wrapped in a mystery inside an enigma. Not much has changed since Sir Winston uttered those words. Consequently, we don’t have high hopes the Russians will stay true to their word.

Additionally, the crude market remains very oversupplied. Therefore, we believe the extremely bullish consensus on oil is in for an unpleasant surprise. Later in the year, though, should prices retreat a bit—likely to the mid-40s from the current low 50s level—and bearishness once again reigns supreme, we may see another spirited rally. The good news is that we don’t believe the price decline will cause more than a mild correction in the master limited partnership (MLP) space, similar to what we saw in the fall of 2016 when oil tumbled 20% and MLPs dipped 10%.

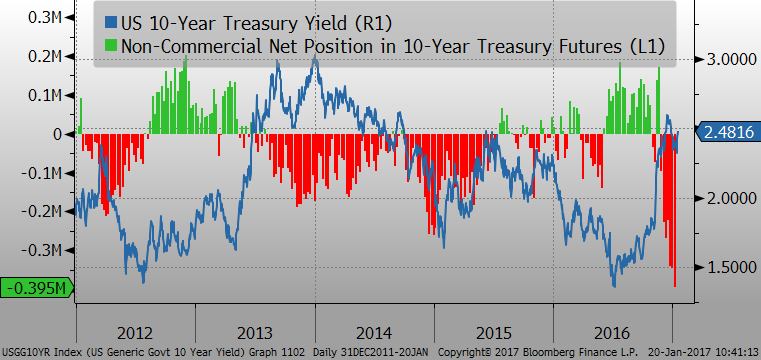

6. Another unexpected event that could wrong-foot the majority of investors is the bond market, particularly if the Fed does raise rates as much and as often as we think they will. The common-knowledge reaction is that bonds perform very poorly during a tightening campaign; thus, most expect high-grade debt to perform poorly should the Fed actually deliver on rate hikes (junk bonds are presumed to do better, benefiting from what is expected to be an accelerating economy).

Per section 1 above, the consensus seems to be doubtful about the resolve on the part of Yellen & Co. but the group-think also appears to be that if they do it will be another dagger in the heart of the bond market (along with the purported inflationary nature of Trumponomics). Certainly, the current positioning of the more aggressive participants in the bond market reveals severe negativity.

FIGURE 3: source: Evergreen Gavekal, Bloomberg

source: Evergreen Gavekal, Bloomberg

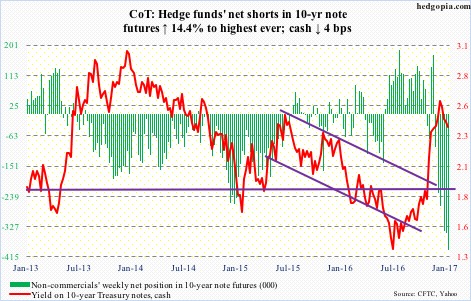

FIGURE 4:

source: CFTC

Yet, the Fed has already hiked twice and the tendency in recent tightening episodes is for most, if not all, of the bond market pain to occur early in the rate-raising cycle. In fact, when the Fed jacked its overnight rate up from 1% in 2004 to 5¼% in 2007, nearly all of the damage to bonds was done before it even raised once!

It’s this tendency for bond yields to surge early on and then stabilize—or even fall—as the Fed tightening process intensifies that creates the ultimate recession alert: an inverted yield curve (where short rates go above longer rates). Frankly, we had our doubts we’d see this before the next economic contraction. We thought we’d see a situation more like Japan and Europe over the last decade where recessions happen without the yield curve inverting.

It may still turn out that way because, as we speculated in section 1, the Fed is likely to stop hiking as soon as something really bad occurs, like a crisis in emerging markets or a US market crash a la 1987. But, barring a shock, the Fed will probably keep pushing rates up trying to get as close to 2% as they can. This would at least bring their overnight rate to around the inflation rate. It would also give them some room to cut when a truly nasty surprise comes out of left field, as they typically do.

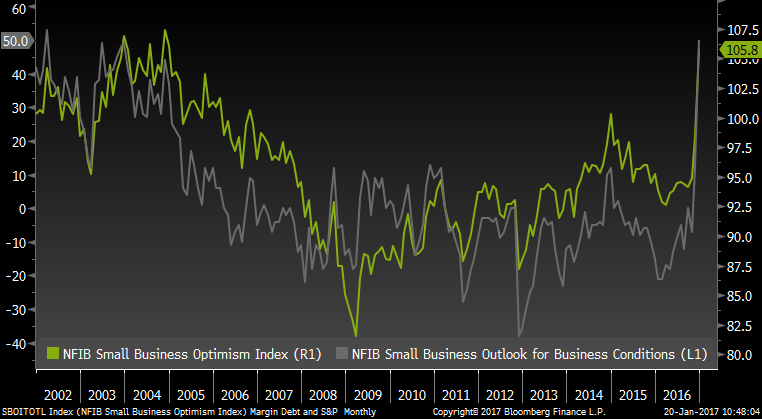

7. One of the questions we get most often from clients since the election is: Why has the stock market done as well as it has since Trump won? Unsurprisingly, these tend to come more from clients who are not fans of The Donald than those who are but many have emanated from longtime GOPers.

The main answer I give is confidence. Rightly or wrongly, both CEOs of large companies and small business owners are reporting a remarkable surge in their future outlooks.

FIGURE 5: source: Evergreen Gavekal, Bloomberg

source: Evergreen Gavekal, Bloomberg

FIGURE 6: source: Things That Make You Go Hmmm...

source: Things That Make You Go Hmmm...

As we’ve noted in prior EVAs, some of his proposed policies are similar to what we’ve been long advocating. Accordingly, we get that part and do believe these changes, like comprehensive tax reform, could have a very positive impact on the economy.

But what could be a shocker for the rampaging bulls right now is that what’s good for the economy isn’t necessarily good for the stock market. If that sounds implausible, consider that the worst economic expansion since WWII has been associated with one of the most virile and long-lasting bull markets. So it wouldn’t be outlandish to postulate that a better economy could be problematic for stock prices, particularly if it takes away the dual (and related) crutches of near-zero short-term rates and stock buy-backs. After all, nothing lasts forever—though this market has given it its best shot.

8. With each passing day, this possible surprise may not be all that surprising. However, given that the financial markets are our main focus at Evergreen and they continue to be head-over-heels infatuated with President Trump, this potentiality could still be considered a wicked knuckleball for the consensus: His administration ends up looking much more like Silvio Berlusconi than Ronald Reagan.

This is a topic I covered in a recent interview with Macro Voices’ Erik Townsend, which we plan to soon run as an audio EVA. But for those who are unfamiliar with Mr. Berlusconi, he is a flamboyant and womanizing billionaire who became prime minister of Italy back in the mid-1990s. His election on a platform built around his extravagant personality fostered extreme initial optimism, in no small part based on his proven business acumen. (Is this sounding eerily familiar?)

Early on, his Teflon-like persona was able to sluff-off a flurry of scandals. But, eventually, they became so repetitive that his administration was rendered ineffective. The final straw was a tax-scandal that effectively ended his political career (not that The Donald would EVER have tax controversies, si?).

When Barack Obama was first elected president, I was rooting hard for the success of his administration, despite my trepidations about his utter lack of experience (that hopeful viewpoint angered many an EVA reader back in 2008). Similarly, I sincerely hope Mr. Trump is a bundle of political upside surprises. However, I do believe comparisons with the jovial and avuncular Ronald Reagan are poorly drawn. Let’s just say that there is a decent case to be made that the ghosts of Mr. Trump’s past will haunt his presidency. And that’s definitely not what Wall Street is pricing in presently.

9. The first half of the year may well see continued underperformance by emerging stock and bond markets relative to the US. If so, this would not constitute a surprise or a shock to the consensus view, which is decidedly negative as a result of many years of poor results versus the S&P 500 and US treasuries. However, we suspect that should the Fed hike rates repeatedly and a new “destination-based” corporate tax system be put into place—and further assuming these cause the dollar to have a “blow-off top”—there may well be another version of the famous Plaza Accord.

This agreement occurred back in 1985 and was implemented to bring down the “Reagan dollar”. As older EVA readers may recall—and I certainly do—confidence in Reaganomics caused the buck to go vertical in the mid-1980s, putting the US manufacturing sector in dire straits. The situation became so severe that the major nations of the free world at the time got together at NYC’s Plaza Hotel and agreed to coordinate central bank policies to cheapen the dollar (something the Fed has been highly proficient at over its 100-year history!). It worked. The dollar fell by 50% against currencies like the old German deutschmark and the Japanese yen. In the latter’s case, the yen rose from 242 to the dollar in 1985 to 120 by 1988 (ironically, that’s very close to the dollar/yen relationship today, despite almost 30 years of huge trade surpluses in favor of Japan).

Once again the dollar is extremely overvalued on a purchasing-power-parity basis (for example, I’m told that downtown hotel prices in Tokyo are amazingly affordable in US dollars). Based on the factors described above, it is poised to become even more so, once a correction of its current overbought condition is rectified. If it does rocket another 20% or so from here, the odds of a Plaza Accord 2.0 go up dramatically. A weakening dollar is almost always jet fuel for emerging markets. Accordingly, it’s at that point emerging market stocks and bonds should go from the doghouse to the penthouse.

10. The US stock market has been outperforming its global peers for such a long time that it’s as hard to find bulls on foreign equities as it is to find Trump supporters in downtown Seattle. As a result, it almost goes without saying that should overseas markets beat the S&P this year that would be a seismic shock.

Taking this one step further, there are few markets and/or economies held in as low esteem as is France’s. Yet, that long moribund nation could be on the cusp of its own Trump moment…but minus all the—shall we say—“flamboyance” (a lovely French/English word).

Few Americans are aware of the shifting political winds in France where the front-runner in next year’s presidential race is a much more similar echo of Ronald Reagan based on the likeability factor, Francois Fillon. (However, Barron’s readers may have noticed a supportive article on this topic in last week’s Issue.) France is also home to a long list of world-class companies. Its economy has, of course, been smothered for decades by an encroaching socialism which has drained it of its inherent vitality. Thus, should policies be put in place to remove those shackles, France could experience the same business and investor confidence surge that Trump has delivered in the US.

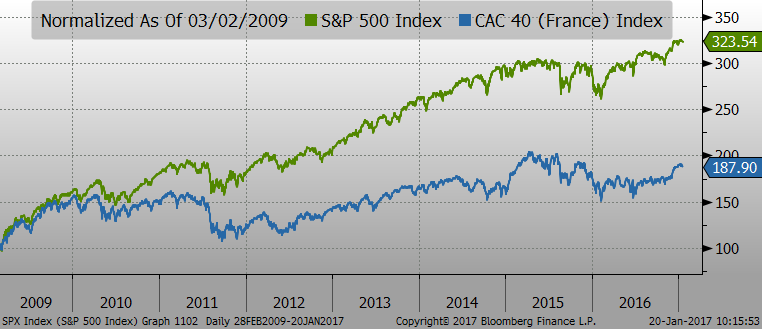

Additionally, the French stock market sells at about a one-third discount to the US on a cyclically-adjusted P/E basis (CAPE). And, as you can see below, it has hugely lagged the S&P 500 since the Great Recession.

FIGURE 7:

I can hear your skepticism from here—which is why this one might be the biggest surprise of all, should it play out this way over the course of 2017. By the way, 2017 is the Year of the Rooster on the Chinese calendar. And the rooster just happens to be the national bird of France.

______________________________________________________________________

OUR CURRENT LIKES AND DISLIKES

Changes in bold.

LIKE

NEUTRAL

DISLIKE

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness.