"No persons are more frequently wrong than those who will not admit they are wrong."

-Author FRANCOIS DUC DE LA ROCHEFOUCAULD

POINTS TO PONDER

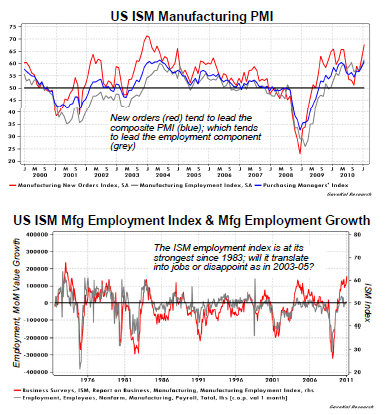

1. The Fed’s ultra-easy monetary policy is looking increasingly out-of-phase with the mounting evidence of a healing US economy. The manufacturing version of the Institute of Supply Management (ISM) Purchasing Managers’ Index (PMI) and its employment index have surged while ISM’s service sector index is also showing strong expansion.

2. Today’s official unemployment report contains enough crosscurrents to be called schizophrenic by Pimco’s Bill Gross. Yet for

the second month in a row the jobless rate fell by 0.4% one of only 9 monthly declines of that magnitude in the last 45 years. Without extreme winter weather, job growth would likely have been far more robust.

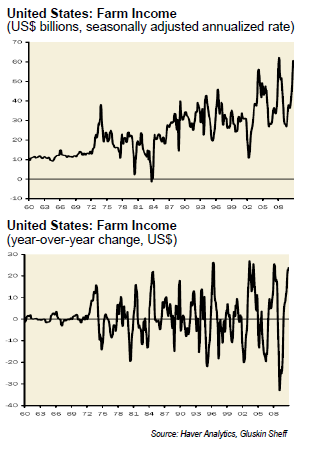

3. The US is often referred to as the Saudi Arabia of food. Rapidly increasing demand for agricultural products from the developing world is driving up prices and causing boom times down on the American farm.

4. Despite a strong start to the year by US stocks, the Indian market is off 10%, and China’s Shanghai exchange recently entered official bear market territory, falling 21% from its peak in August 2009.

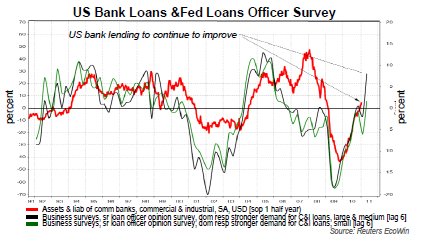

5. As more evidence that the Fed may be falling behind the curve by staying too easy, too long, US lending activity is clearly on the upswing. This improvement is almost certain to lead to a revival of the long dormant money multiplier.

EVAluating the Environment

Where did all the press coverage go? Two years ago, one theme seemed to dominate all forms of media: the unconscionable bail-out of Wall Street. This enraging and energizing emotion spanned the political spectrum, involving those on the left as well as the founding fathers (and mothers) of the Tea Party movement.

Nothing seemed to fan the flames of outrage more than financial system triage efforts like the TARP (Troubled Asset Relief Program) and the PPIP (Public Private Investment Program). It didn’t help that both the outgoing and incoming Treasury Secretaries, Hank Paulson and Tim Geithner, displayed about as much marketing panache as the typical telephone solicitation call.

As is so often the case when passions run high, logic fell by the wayside. So intense was the vitriol against the TARP that its original mission—buying deeply discounted mortgage securities—had to be scrapped.

One of the enduring images I have of that calamitous time is of then-Treasury Secretary Paulson haplessly attempting to explain to Congress why he needed to be given hundreds of billions of dollars to buy what were routinely labeled “toxic” assets. The furious blow-back he received from representatives of both parties sent him packing and in desperate need of Plan B. In the meantime, the stock market cratered, major financial institutions were on the brink of extinction and confidence around the world was vaporizing.

Fortunately, for him and our nation, the Brits had just unveiled a stratagem to inject government capital in the form of preferred stock into their leading banks. Encouraged by some kind of decisive stabilization action, global financial markets rallied, and Mr. Paulson took that as his cue to copy the British model. Soon thereafter he was back before Congress, which reluctantly gave him the $700 billion credit line he needed to shore up the US banking system.

At the time, a series of EVAs tried to explain that the original TARP, designed to buy mortgages that in many cases were trading at 30 cents on the dollar, was almost certain to be a windfall, not sinkhole, for taxpayers. In fact, I went even further and repeatedly suggested that the Fed reinforce the Treasury’s efforts by acquiring massive amounts of severely discounted, high-grade corporate debt which, in those days, was trading like junk bonds.

Despite the fact that true masters of the financial cosmos such as Warren Buffett and Bill Gross were also defending the original TARP (Mr. Gross even offered to manage the government’s buying program for free), their voices of reason were drowned out in the hysteria.

In my own case, I received numerous emails asserting that I was—among other uplifting observations—a socialist, a dreamer, an idiot and a nutcase (I hadn’t been called the last two names since my sons were teenagers). One particularly scathing missive came from a colleague in the investment industry who told me there was “zero” chance the government would ever see its money returned. The intensity of his scorn caused me to wager that US taxpayers would actually make a profit on this undertaking.

Yet, here we are a mere two years and a few months later, and nearly all the TARP funds have been repaid. Even the sickest of the major banks, Citigroup, has paid in full with the Treasury netting a cool $12 billion profit.

Additionally, the PPIP-squeak of the alphabet soup of rescue efforts, the Public Private Investment Program, is also rewarding taxpayers, and dismaying naysayers, by generating husky profits. The Treasury recently reported that it is already ahead 27% on the PPIP since the spring of 2009, but the sad fact is that only $6.3 billion was committed to this effort.

The strong opposition to the idea from many political quarters led to such a lengthy delay that by the time it was activated, the formerly devastated mortgage market was already soaring. Additionally, several key institutions backed away due to the controversy and confusion. (Evergreen was a victim of this as our plans to participate through a major Wall Street firm were derailed by infighting between the SEC and the Treasury.)

Despite considerable opportunity mostly lost, the overall results of both the TARP and the PPIP were exceedingly positive, particularly given that their main mission was to save the financial system, with profit generation a distant second.

Yet, as is often the case with good news, you have to look hard to find articles that talk about this remarkable turn of events. When you do find them, they often include quotes from grumpy “experts” that the returns weren’t commensurate with the risks and/or that the bank shareholders got too good a deal (don’t tell that to the poor souls who rode Citigroup down from 50 to 5).

The biggest coup, though, is still unfolding.

Anything but a give-away. The bail-out that seemed to generate the greatest indignation involved not a bank, but an insurance company with the deceptively simple acronym of AIG (and whose business model was about as far removed from simple as the Egyptian government is from democracy). At the time, I posed the question as to whether AIG should stand for “Another Infuriating Giveaway,” but I had the temerity to contend that it, too, would produce profits for US taxpayers.

This position once again triggered some highly critical feedback, which was understandable given the enormity of the cost to the TARP, potentially as much as $170 billion. In fact, this number continues to be bandied about even though nowhere near that amount was ever actually drawn down by AIG.

It was just a few months ago that certain elements of the government itself were still warning that US taxpayers would lose money on AIG. However, the recent success of initial public offerings of several of its key subsidiaries has served to stifle those dire views.

Flummoxing the carping critics and vindicating Bruce Berkowitz, Morningstar’s equity fund manager from 2000 – 2010 who has touted AIG for months, the Treasury’s 93% stake is now worth $70 billion versus a $48 billion cost. Of course, there is a loser in all this, and that would be AIG’s shareholders who saw their ownership stake almost completely obliterated. All’s fair in love and the stock market, you might say (particularly if you weren’t an AIG owner), but the fact of the matter is that it was one of the crown jewels of corporate America. Moreover, AIG’s basic insurance businesses remained consistently profitable, which is why it has been able to attract top-dollar prices for the businesses they are selling despite the lingering taint of its highly public near-death experience.

For those who don’t recall, it was a small division, located in London, that nearly whacked the firm. This unit sold credit default insurance on hundreds of billions of dollars of ostensibly AAA-rated securities which possessed the unfortunate characteristic of being backed by sub-prime mortgages.

Ironically, though, as mentioned in EVAs back in 2008, these securities had enough safeguards in place that it seemed highly unlikely they would produce much in the way of actual credit losses (versus the massive hits indicated by market prices at the time).

This leads to how the Fed played its hand at the great AIG Texas Hold ‘em game.

Riverboat Ben. The rescue of AIG involved such large sums (potentially 25% of the entire $700 billion TARP) that it required a joint effort by the Treasury and the Fed. Most of the attention since then has been focused on the Treasury’s role and its de facto nationalization of AIG, at least from a shareholder standpoint. As seen above, that looks set to be a tidy gain for taxpayers. However, the Fed also appears poised to win a big pot, and they have pulled this off with the subtlety of the slyest card shark.

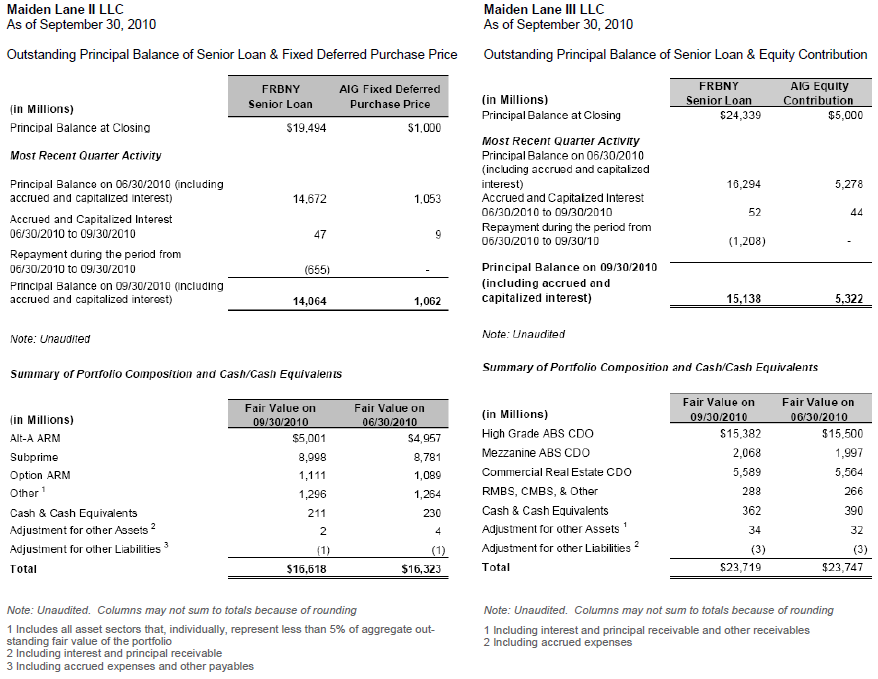

Perhaps Ben Bernanke is a better poker player than I give him credit for, because he appears to be keeping a pair of aces up his pin-striped sleeve—in this case, a couple of the Fed’s investment vehicles with the innocuous names of Maiden Lane II and III.

(For the curious, the name Maiden Lane comes from the Manhattan street on which the New York Federal Reserve is located. Maiden Lane I is the entity established to own and guarantee the illiquid securities held by Bear Stearns prior to its shotgun marriage to JP Morgan.)

There has been negligible coverage in the US media of the results of Maiden Lane II and III, possibly because they both appear to be heading toward profitability in the extreme, thus posing quite an embarrassment for the many strident media critics of the AIG rescue. The only news article I have come across on this topic (as discussed in an EVA last year) was from the London-based Financial Times in January of 2010, which disclosed a $15 billion gain.

However, if you go to the Federal Reserve website on these two vehicles (just Google Maiden Lane II), you will find the tables shown below which, with a little number crunching, come close to the Financial Times’ $15 billion profit estimate. This site shows Maiden Lane II with a market value $2.6 billion higher than cost as of September 30, 2010, while ML III has an embedded gain of nearly $9 billion. Therefore, by the Fed’s reckoning, they’re ahead almost $12 billion.

In reality, the Fed’s windfall could be much larger given that in the case of Maiden Lane III, they’ve received $8 billion of the $24 billion they put up due to the return of principal on the original asset pool. Because the Fed paid roughly 50% on the dollar to buy the assets AIG held (in this case, credit default swaps), it’s probable that they’ve already booked $4 billion in gains (the official annual report for 2010 has not been released).

Pretty much the same math applies to ML II, where the Fed also bought the assets for 50 cents on the dollar. In this case, around $5 billion appears to have been repaid at par, implying another $2 ½ billion in gains.

Additionally, there has been substantial interest earned on these securities, so it’s possible the Fed’s earnings on the two Maiden Lane deals will be in the vicinity of $20 billion, if not more. Consequently, despite the fact that AIG will receive a small portion of the profits, it appears highly likely that the government will earn a substantial amount on the AIG rescue, particularly given the high prices being realized in the public offerings of the various subsidiaries.

Combining a potential $20 billion Fed gain on its AIG financing efforts with the $22 billion the Treasury is positioned to net and you’re talking $42 billion in gains accruing to the US government. As taxpayers, I thought you might want to know about this little factoid that has been conveniently ignored by the mainstream media.

For those taxpayers who are also Evergreen clients, the most relevant aspect is that we sold our AIG equity position in the $50 to $70 price range, but kept our debt holdings. Though the latter fell down as low as 10 cents on the dollar, we hung in there and, over time, added to our stake.

Even today, AIG preferred, backed by subordinated debt, selling at a 12% discount from par and yielding 7.3%, remains one of our favorite income vehicles.

It was a rough voyage, no question about it, and in many ways it was a microcosm of the overall credit cataclysm. However, a happy ending, at least for taxpayers and bondholders, seems in the offing. Just don’t expect to read about it in the popular press!

A note of clarification: Last week’s EVA included a Point to Ponder on Google. It noted that the company’s cash costs per employee have risen to $500,000 but this does not mean that the average Google worker is realizing that level of earnings. Rather, this is the average amount of operating expense per employee exclusive of equity based compensation (mostly stock options).

IMPORTANT DISCLOSURES

This report is for informational purposes only and does not constitute a solicitation or an offer to buy or sell any securities mentioned herein. This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. All of the recommendations and assumptions included in this presentation are based upon current market conditions as of the date of this presentation and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. Information contained in this report has been obtained from sources believed to be reliable, Evergreen Capital Management LLC makes no representation as to its accuracy or completeness, except with respect to the Disclosure Section of the report. Any opinions expressed herein reflect our judgment as of the date of the materials and are subject to change without notice. The securities discussed in this report may not be suitable for all investors and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. Investors must make their own investment decisions based on their financial situations and investment objectives.