"There are times when it’s easier to fool yourself than swallow some jagged piece of reality."

- John Rogers Searle

On January 23rd, over 400 friends, clients, and other interested parties attended our Annual Outlook event at the Meydenbauer Center in Bellevue, Washington. At the event, we were fortunate enough to have been joined by our newest colleague, Grant Williams. To say Grant is a man of many talents is far too modest. He writes one of the world’s most popular newsletters (www.ttmygh.com), is a coveted public speaker, and is the co-founder of Real Vision TV (realvisiontv.com). It’s also an understatement to call him a man on the move; since the start of this year, he’s already been to 10 different countries!

As a strategic advisor to Evergreen, Grant will function in a few different capacities. First, he’ll be making periodic contributions throughout the year to our newsletter, the Evergreen Virtual Advisor (EVA). In the past, we have occasionally run condensed versions of his acclaimed newsletter, Things That Make You Go Hmmm… Now, however, he will be writing an abridged newsletter tailored specifically for our readers. In addition, Grant will have a seat on our investment committee, offering his keen insight into shaping our firm’s views on the macroeconomic landscape. Lastly, when appropriate, Grant will participate in engaging clients or prospective clients in face-to-face meetings.

This edition of our newsletter is the inaugural edition of Grant’s direct authorship to EVA readers. In it, he tackles the seemingly limitless amount of trust afforded to monetary easing tactics, and the frightening reversals of opinion by retired central bankers. It’s an insightful piece that helps crystallize our thoughts on what may be the most serious risk currently facing investors. The central banking experiments happening around the world are unprecedented, untested, and unlimited. If anyone can tell you they know what happens next, they are likely fooling themselves. The reality is that no one knows how this ends, because we’ve never been here before. As Grant points out, this includes the world’s currently idolized central bankers. We feel privileged to be adding someone of his caliber to Evergreen GaveKal and we hope you enjoy his first contribution as a member of our team.

THE REDISCOVERY OF THE MIND

Grant Williams

"Bank of England governor Sir Mervyn King backed more action to boost the economy earlier this month, but was outvoted by his colleagues on the Monetary Policy Committee (MPC).

Minutes of the MPC’s meeting show it voted 6-3 against expanding the quantitative easing (QE) programme from its current level of £375bn." - BBC News, 20 February, 2013

"[Greenspan] said the bond-buying program was ultimately a mixed bag. He said that the purchases of Treasury and mortgage-backed securities did help lift asset prices and lower borrowing costs. But it didn’t do much for the real economy.

"Effective demand is dead in the water" and the effort to boost it via bond buying "has not worked," said Mr. Greenspan. Boosting asset prices, however, has been "a terrific success." - Wall Street Journal

“I propose to consider the question, ‘Can machines think?” With those nine words, Professor Alan Turing (played brilliantly in the current Oscar-nominated movie The Imitation Game, by the wonderfully-named Benedict Cumberbatch) began his 1950 paper “Computing Machinery and Intelligence” in which he set out to find if it were possible for a machine to exhibit intelligent behavior indistinguishable to that of a human.

In order to achieve his aim, Turing (the man who famously broke the code of the Nazis’ Enigma Machine—an action estimated to have shortened WWII by at least two years) devised a simple test by which he would be able to establish beyond any reasonable doubt whether a machine could actually “think.”

In the Turing Test, the interrogator (C) is tasked with trying to establish which of players (A & B) is human and which is a machine based solely on written answers to written questions.

If the interrogator is unable to determine whether he is talking to the man or the machine, the latter is deemed to have passed the test and can therefore be said to have artificial intelligence.

Simple.

In 1980, John Rogers Searle, Professor of Philosophy at the University of California, Berkeley, published a paper entitled "Minds, Brains and Programs" in which he introduced an argument called "The Chinese Room" which, according to David Cole, writing in 2002 was "…probably…the most widely discussed philosophical argument in cognitive science to appear in the past 25 years."

Searle’s argument sparked enormous discussion (with most commentary aimed at proving it fallacious), but what he suggested—like the suggestions of Turing before him—was simple, clean, and stimulating.

(Wikipedia): "Assume you do not speak Chinese and imagine yourself in a room with two slits, a book, and some scratch paper. Someone slides you some Chinese characters through the first slit, you follow the instructions in the book, transcribing characters as instructed onto the scratch paper, and slide the resulting sheet out the second slit. To people on the outside world, it appears the room speaks Chinese—they slide Chinese statements in one slit and get valid responses in return—yet you do not understand a word of Chinese."

Now, with that as background, let’s move forward in time to November of 2014, when former Chairman of the Federal Reserve, Alan Greenspan, spoke at the Council on Foreign Relations.

After his speech, in a subsequent discussion with Gillian Tett of the London Financial Times, the following exchange took place:

TETT: Do you think that gold is currently a good investment?

GREENSPAN: Yes... Remember what we’re looking at. Gold is a currency. It is still, by all evidence, a premier currency. No fiat currency, including the dollar, can match it.

Now, contrary to your initial fears, this is not going to be a piece espousing the benefits of owning gold (“thank Heavens!” I hear you cry), but Greenspan’s comments were—to those of us who watch such things closely—both extraordinary and symptomatic.

Having decried gold relentlessly during his time as Fed Chair, Greenspan reverted to his core beliefs once relieved of that burden, and announced (I am told, with a straight face) that no fiat currency, including the dollar, was its equal.

Hot on the heels of Greenspan’s volte face, former Bank of England (BoE) governor Melvyn King recently gave his first public speech since leaving office almost two years ago. Interestingly, his reappearance in the spotlight happened just a handful of days before Mario Draghi finally unveiled the much-

anticipated European Central Bank (ECB) Quantitative Easing (QE) program and what King had to say was, once again, highly educational:

(Reuters): King said he was concerned about a persistent weakness in global economic demand, six years on from the depths of the financial crisis.

“We should worry about that,” King told an audience at the London School of Economics, where he was once a professor.

“We have had the biggest monetary stimulus that the world must have ever seen, and we still have not solved the problem of weak demand. The idea that monetary stimulus after six years ... is the answer doesn’t seem (right) to me,” he added…

“There are quite serious disequilibria both between and within economies that, for good economic reasons, are depressing demand. Simply lowering rates even further or adding more monetary stimulus is unlikely to solve that problem,” he said.

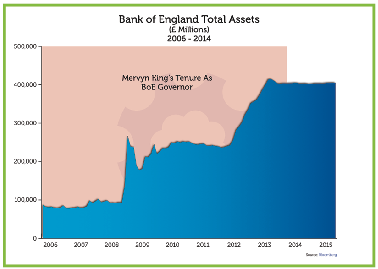

During King’s tenure as Governor, the Bank of England bought £375 billion of government bonds between 2009 and 2011 to take the BoE’s total assets from a little under £100 billion to today’s £405 billion in its own QE program, aimed at restoring the UK economy to growth in the wake of the Great Recession of 2008.

King was an ardent supporter of the QE program and, in fact, he was still lobbying for an increase in its size a mere four months prior to his departure, stage left, but—and here’s where we finally get to the point of this week’s EVA—once his job was no longer predicated on toeing the company line, King seems to have made what Searle called in his 1992 book a Rediscovery of the Mind, just as Greenspan did before him.

The policy of Quantitative Easing has been around for over two decades now and was begun by the Bank of Japan, who are currently in the midst of QE10. Each of their iterations of Quantitative Easing has been greater than the last and the current "plan" of doubling the monetary base and buying up to 90% of JGB issuance is nothing short of the total debauchery of the yen—debauchery which has been cheered to the echo around the globe as if the destruction of the currency of the world’s second third largest economy is something worth celebrating.

The basic defence of QE (and Keynesian economics in general) has been a simple one throughout the years: It would have worked—they just didn’t print enough. That mentality has been evident across global monetary policy since 2008 as central bank after central bank has capitulated (some more willingly than others) and joined the rush to create currency out of thin air in an attempt to forestall the forces of deflation and generate the level of inflation required to stop the enormous debt load under which the world is struggling from overwhelming the financial system and causing a complete collapse.

Each of them has assured the pubic that such action was both completely necessary and absolutely temporary.

The US Federal Reserve has now finished its (third) taper and, the general narrative is that the operation has been a success and has, in fact, passed without any major problems occurring. That sound you can hear if you listen carefully outside the Marriner S. Eccles building is an outbreak of back-slapping.

However, to accept this as gospel is an incredibly dangerous thing to do. Attention must be paid to the underlying reality if one is to avoid the pitfalls which are all too prevalent in listening to the words of public figures whose very existence currently hinges on conveying a set of beliefs to a particular populace with the singular aim of instilling within that populace a level of confidence sufficient to render their economic malfeasance successful.

Without that confidence, they are dead in the water.

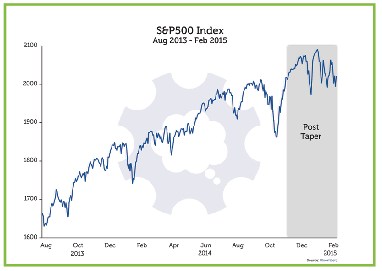

The chart on the next page shows the gyrations of the S&P 500 since August 2013 when the Fed’s QE3 program was in full swing. It’s been a long time since "gyrations" was an appropriate noun to use in relation to the S&P 500 but, almost imperceptibly, it has become entirely apropos.

As you can see, the chart is characterized by long periods of steady appreciation followed by reasonably sharp corrections, after which the rise has resumed.

However, as the end of the Taper drew near, the dips became more pronounced as investors feared the uncertainty of a world without central bank support.

After one more in a long series of "V-bottoms" in October—right before the scheduled end of the Taper—the market climbed back to yet another all-time high and all was seemingly right in the world—the Taper had been executed flawlessly and a sigh of relief could be heard.

Only, as you can see from the chart, in the post-Taper world, we have seen the return of volatility to markets (a return that can be seen more clearly in the chart below which shows three-month S&P volatility).

After a long (three-year) period of steadily declining volatility, the post-taper environment has seen the first trend-change to the upside and this heralds the return of volatility to a market in which suppression has been the name of the game in order to generate that confidence about which we spoke a few paragraphs ago.

Because of the importance of confidence, central bankers have, as GaveKal’s renowned Anatole Kaletsky recently pointed out, been granted a "license to lie"—and lie they have. Do they believe they are lying? Possibly not, but I feel certain they will have already justified in their own minds the reasons why they might have to do so well in advance of any possible mendacity and so, when the time comes, the transition is a seamless one.

Jean-Claude Juncker—one-time Prime Minister of Luxembourg and the longest serving head of government in the European Union as well as one of the longest-serving democratically-elected leaders in the world when he left office in 2013—gave us a peek behind the veil when he famously said, at the height of the eurozone crisis after being caught red-handed blurring the line between truth and fiction, that "when it gets serious, you have to lie."

Juncker was one of the architects of the Maastricht Treaty and largely responsible for the construction of clauses on Economic and Monetary Union within that hallowed document and so, as interests go, it is safe to call his "vested" when it comes to preserving a legacy.

Juncker was also voted European Banker of the Year in 2008. Just sayin’…

Anyway, whatever the reasons behind Messrs. Greenspan and King’s sudden reversal in tone, they are irrelevant. It is clear that the world’s central bankers leave their beliefs and principles at the door when they take office, only to pick them up again on the way out in the interests of protecting their legacy. What they do in between those two short journeys is dictated by the position and not what they, in their heart of hearts, know to be in the best interests of the citizens under their auspices.

In mid-January, we had another central banker demonstrate the danger of becoming too aligned with promises emanating from those august institutions when the Swiss National Bank governor, Thomas B. Jordan removed the Swiss Franc’s peg to the euro with this short statement:

"The Swiss National Bank (SNB) is discontinuing the minimum exchange rate of CHF 1.20 per euro."

No fanfare, no apology (though one was most certainly warranted as a matter of three days prior, a high-ranking official reaffirmed that the peg was "a pillar of Swiss monetary policy"). Clearly, when the earlier statement was made, it was a bare-faced lie and, in his press conference, Jordan explained (though not in direct relation to his colleague’s statement) why such mendacity was not only warranted, but required:

"If you decide to exit such a policy, you have to take the markets by surprise,"

The game has shifted in the last several weeks and central bankers are now not only fighting a rearguard action but each other in an attempt to protect their own economies from the ravages of a debt deleveraging.

Once they have left office, there will be plenty of time to try and rewrite history through autobiographies, tell-all accounts (yes, Timothy Geithner, I’m looking at you - and you, Hank Paulson) and after-dinner speeches in which they explain that they did what they had to do to "save the system"—even though it went against their core principles—but for now, for investors lulled to sleep by six years of whispered promises, it is time to wake up and understand that the only time we will find out what those in control of the world’s monetary rudder really think is the appropriate action will be after they have handed the baton to the next poor unfortunate soul.

With this shift will come increased volatility, harsher focus on valuations, creditworthiness and economic numbers and a reduction in the willingness to blindly believe in the narrative being disseminated from seats of power around the world. The landscape has changed.

Turing once wrote "If a machine is expected to be infallible, it cannot also be intelligent." But today, the world is seemingly pinning all its hopes for economic and monetary stability on the twin machines of government and central banking being both.

Meanwhile, during their time in office at least, politicians and central bankers put aside their real feelings about what must be done in favor of expediency and then pretend to the world that the actions taken, whilst dictated by circumstance, were in everybody’s best interests.

That, ladies and gentlemen, is the real Imitation Game.

IMPORTANT DISCLOSURES

This report is for informational purposes only and does not constitute a solicitation or an offer to buy or sell any securities mentioned herein. This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. All of the recommendations and assumptions included in this presentation are based upon current market conditions as of the date of this presentation and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. Information contained in this report has been obtained from sources believed to be reliable, Evergreen Capital Management LLC makes no representation as to its accuracy or completeness, except with respect to the Disclosure Section of the report. Any opinions expressed herein reflect our judgment as of the date of the materials and are subject to change without notice. The securities discussed in this report may not be suitable for all investors and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. Investors must make their own investment decisions based on their financial situations and investment objectives.