“There is a meaningful risk that, come November, one of the people currently running for president will win.”

- Barron’s Jack Hough.

“If God had wanted us to vote, he’d have given us candidates.”

- Jay Leno

HUNT FOR THE TRUTH

By David Hay, Chief Investment Officer

Almost every golfer has heard of Harvey Penick and his classic golf instruction manual, The Little Red Book. One of the most memorable stories he tells in it details how he decided he had no future on the PGA golf tour despite being an accomplished player. What disabused Harvey of the notion of “joining the circuit” was when an up-and-coming golfer came into Harvey’s hometown of Austin, Texas, back in the 1920s. The prodigy’s name was Sam Snead.

Harvey wrote that once he merely heard one of Snead’s tee shots, he realized he had no chance to ever be truly competitive with Slammin’ Sammy. That sound, which he had never heard before, convinced him in an instant that he was a mere mortal in the presence of a golfing god.

That’s a bit how I feel when I read certain other financial writers. Having composed a few hundred newsletters over the last decade or so, I’ve developed an appreciation for a few of my “peers” (really, my superiors) who are truly gifted when it comes to shaping the English language around their ideas and themes. Jim Grant is one of those. Another is Ben Hunt.

Ben writes a free weekly piece called Epsilon Theory (please see the end of this message for subscription instructions). He is also a PhD and chief risk officer for the $18 billion money management firm, Salient Partners. Late last month, he wrote the piece which is this month’s Guest EVA, “The Silver Age of the Central Banker”.

Like yours truly, Ben has long believed that the dominant force for financial markets in recent years has been central bank intervention. As entities like the Fed, the Bank of Japan, and the European Central Bank have taken ever more aggressive actions to inflate asset prices in order to fight the twin enemies of excessive debt and stalling growth, they have attained god-like status (even if none of their leaders can hit a golf ball like Sam Snead). Ben has dubbed this period the era of Central Bank Omnipotence.

In this phase, bad economic news has been treated as good. This is because it has consistently meant more monetary narcotics from the Fed, et al., something markets have consistently celebrated. That is, until lately, when, like a needle-scarred junkie, the fixes need to be stronger and stronger to create an increasingly fleeting sense of euphoria.

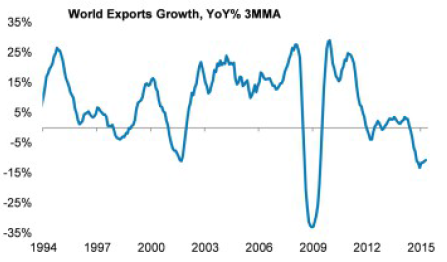

Also very much in synch with my view, Ben is alarmed by how little attention is being paid to currency wars (i.e., Japan driving down the yen and Europe cheapening the euro in order to gain competitive advantages). This vestige of the 1930s has already produced a worrisome decline in world trade, to a level that typically only occurs during recession. It is also shrinking for the first time since 2009.

A SUBDUED GLOBAL TRADE ENVIRONMENT

Source: International Monetary Fund, Morgan Stanley Research

Further aggravating this dangerous scenario, the leading US presidential candidates are spewing copious amounts of anti-free trade rhetoric. America is not alone in its new-found hostility to free-trade. As Ben notes, when the global export pie is shrinking it becomes a case of every country—and central bank—for itself. He even provides a brief tutorial on John Nash’s (“A Beautiful Mind”) game theory in this regard.

As I listen to CNBC, I hear a steady stream of commentary that the US economy is doing fine and almost nothing about how profoundly weak global trade activity is currently. (Check out the recent reports from Moeller/Maersk, the planet’s leading container shipping company; they are reporting their business is a bad as it was during the Great Recession.)

Neither Ben nor I are of an apocalyptic persuasion. However, when almost 40% of the developed world is operating under the influence of negative interest rates, you don’t have to be Milton Friedman or Charles Gave to realize something is very rotten in Denmark (which is among those countries where you have to pay to deposit your money).

It’s time to hand the baton to Ben. This is a bit longer Guest EVA issue than we normally run but I think it will be worth every moment you invest in it.

THE SILVER AGE OF THE CENTRAL BANKER

By Ben Hunt, Epsilon Theory

For the past six plus years, ever since the Fed launched QE1 in March 2009, we have lived in an era I’ve described as the Golden Age of the Central Banker, where the dominant explanation for why market events occur as they do has been the Narrative of Central Bank Omnipotence. By that I don’t mean that central bankers are actually omnipotent in their ability to control real economic outcomes (far from it), but that most market participants have internalized a faith that central bankers are responsible for all market outcomes.

As a result, an entire generation of investors (we investors live in dog years) has come of age in a market where fundamental down is up and fundamental up is down. What’s the inevitable market reaction to real world bad news – any bad news, regardless of geography? Why, additional accommodation by the monetary Powers That Be, united in their common cause to inflate financial asset prices through large scale asset purchases, must surely be on the way. Buy, Mortimer, buy! During the Golden Age of the Central Banker, monetary policy is truly a movable feast for investors.

But the Golden Age of the Central Banker has now devolved into the Silver Age of the Central Banker, and monetary policy is no longer the surefire tonic for investors it was even a few months ago. In less poetic terms, the Coordination game that dominated the strategic interactions of central banks from March 2009 to June 2014 is now well and fully replaced by a Prisoner’s Dilemma game in the long run and a game of Chicken in the short run. As a result, monetary policy is now firmly a creature of each nation’s domestic politics, and the Narrative of Central Bank Omnipotence is in turn devolving into a Narrative of Central Bank Competition.

Why the structural change in the Great Game of the 21st century? Because this is what ALWAYS happens during periods of massive global debt, as the existential imperatives of domestic politics eventually come to dominate the logic of international economic cooperation. Because this is what ALWAYS happens when global trade volumes roll over and global growth becomes structurally challenged.

Yes, that’s right, global trade volumes – not just values, but volumes, not just in one geography, but everywhere – peaked in Q3 or Q4 2014 and have been in decline since. That’s pretty much the most important fact I could tell you about this or any other period in global economic history, and yet it’s a fact that I’ve never seen in a Wall Street Journal or Financial Times article, never heard mentioned on CNBC.

Using World Trade Organization (WTO) data on seasonally-adjusted quarterly merchandise export volume indices, as of Q3 2015 (the last data point from the WTO), the US is off 1% from peak export volumes, the EU is off 2% (this is EU exports to rest of world, not intra-EU), Japan is off 3%, and China + Hong Kong is off 5%. That’s through Q3. Working from global trade value data, converting to local currencies, and making some educated guesses about price elasticity to estimate Q4 2015 volumes, I’m thinking that the US is now off 3% from peak volumes, the European Union (EU) is off 2.5%, Japan is off 5%, and China + Hong Kong is off 7%.

Now those numbers probably don’t seem very large to you, and certainly in the Great Recession those numbers got a lot larger (about an 18% peak-to-trough decline in worldwide export volumes from Q2 2008 to Q2 2009). But it’s incredibly rare to see any sort of decline in export volumes, particularly a decline that’s shared by every major economy on Earth. In fact, you don’t get numbers like this unless you’re already in a recession.

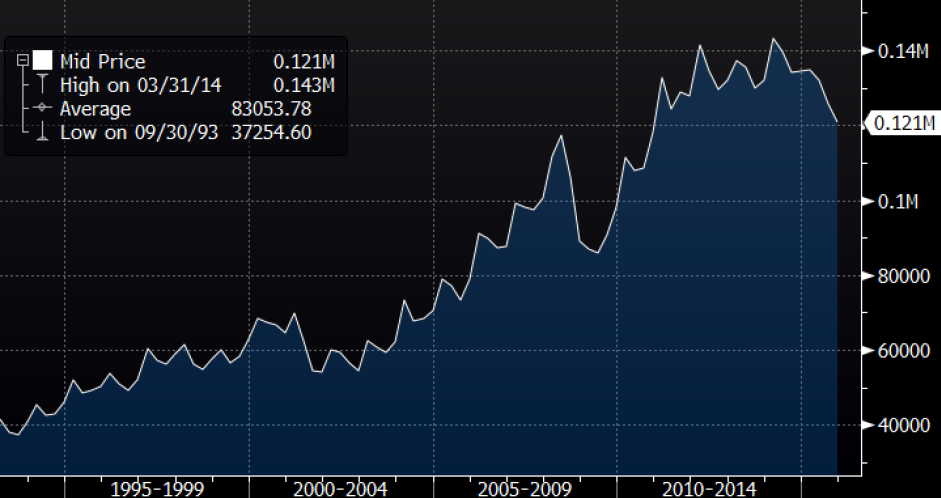

For example, here’s a chart of quarterly US export data since 1993. Now this chart is showing total value of US exports, not volumes of US exports, but you get the idea. Over the past 20+ years, we’ve never had a peak-to-trough decline in exports like we’re seeing today that wasn’t part of a full-blown recession, and we’re getting close to a decline in values (but not in volumes) that rivals what we saw in the Great Recession. The next time someone tells you that there’s a 10% or 20% chance of a recession in the US in 2016, show them this chart. Export growth is THE swing factor in GDP calculations. I don’t care how consumer-driven your economy might be, it is next to impossible for a real economy to expand when your exports are contracting like this. The truth is that we are already in a recession in the US, and this notion that you can somehow divorce the overall US economy from the obvious recession that’s happening in anything related to global trade (industrials, energy, manufacturing, transportation, etc.) just drives me nuts. Yes, it’s a “mild recession” or an “earnings recession” (choose your own qualifier) because the decline in export values (i.e., profits and margins) has only started to show up as a decline in export volumes (i.e., economic activity and jobs). But it’s here. And it’s getting worse.

This is the root of pretty much all macroeconomic evils. If global trade volumes in Asia, the US, and Europe are contracting simultaneously, then global growth is contracting on a structural basis. Global contraction in trade volumes everywhere is exactly as rare as a nationwide decline in US home prices, and it’s exactly as mispriced from a risk perspective. The 2007-2009 nationwide decline in US home prices blew up trillions of dollars in AAA-rated residential mortgage-backed securities (RMBS). A continued contraction in Asian, US, and European trade volumes will blow up whatever vestiges of monetary policy cooperation remain, and that’s a far bigger deal than US RMBS.

When global trade volumes contract, the domestic political pressure to raise protectionist barriers and seize a larger slice of a smaller trade pie becomes unbearable. That was true in the 1930s when protectionist policies took the form of tariffs and quotas, and it’s true today as protectionist policies take the form of currency devaluation and negative interest rates.

Here’s why. In Q4 of 2015, the value of German exports as measured in euros was actually up 0.5% over Q4 of 2014. But over the same time span the euro depreciated versus the dollar by more than 10%. As a result, the value of German exports as measured in dollars from Q4 2014 to Q4 2015 was also down more than 10%. But domestic German economic activity doesn’t take place in dollars, of course, it takes place in euros. In other words, the export-oriented sectors of the German economy felt okay in 2015, at least from a domestic political perspective. But if you had not enjoyed that euro depreciation against the dollar, German exports would have felt terrible, and there would have been significant domestic political consequences. We would all be reading today about “the industrial slowdown in Germany”, with scads of articles in the Financial Times about how Merkel’s regime was losing popular support.

To be sure, the depreciation of the euro versus the dollar made everything that Germany imported that much more expensive. So this isn’t necessarily some profits windfall for German exporters, and if you’re the German equivalent of Walmart it’s a big problem. I’ve read a number of economists and analysts (not so much in regards to Germany but definitely in regards to China) say that this economic downside serves as an effective deterrent against rampant and competitive devaluations. Unfortunately, that’s pure nonsense.

Thinking of national governments as just another big company (or, in slightly more academic terms, conflating national competitiveness with private sector profit margins) is a classic mistake that investors and economists make when they analyze politics. Neither the German government nor the Bundesbank care about corporate profit margins! They care about economic activity. They care about keeping the factories running, with real people making real things that can be sold in the real world. A depreciating currency is, by an order of magnitude, the most effective weapon in any modern government’s arsenal for keeping the factories running, and when global trade starts to contract this weapon will be employed by any means necessary, regardless of the P&L consequences for the private sector. That includes the P&L consequences for the banks, by the way.

Now everything I just wrote about the domestic political dynamics of Germany, multiply it by 10 for Japan. Multiply it by 100 for China. Both China’s export volumes and export values are declining, and no matter how much domestic credit and currency they pump in (and god knows they’ve tried), there is no possible way to stimulate the domestic economy enough to pick up the slack from a declining export sector. This is a domestic political disaster, and getting those factories humming again is a domestic political imperative. At least if there’s a regime change in Germany, Merkel and Schäuble and Weidmann can all retire to their respective comfy chalets and pick up however many millions they like by hitting the speaker circuit. Somehow I doubt that those retirement options are available for senior Politburo members rousted in the middle of the night by a new Chinese regime. To get the factories hiring you need to sell more stuff. To sell more stuff you need to cut your prices. To cut your prices you need to devalue your currency. This is why China is going to float the yuan. Not because George Soros or Kyle Bass said they have to. Not even because their foreign reserves are by no means the fortress balance sheet they’re made out to be. No, China is going to float the yuan because they want to, because it’s clearly the winning move from a domestic political perspective.

Just like the Smoot-Hawley Tariff Act was clearly the winning move from a domestic political perspective in 1930. Just like the anti-free trade diatribes by both the Republican and Democratic presidential frontrunners are clearly the winning moves from a domestic political perspective in 2016. This is … ummm … not good.

It’s not good because these winning moves from a domestic political perspective do not occur in an international vacuum. To the degree that these monetary policy decisions impact other countries – and when global trade volumes are shrinking these decisions impact other countries a lot – other countries are going to respond with their own “winning” moves from a domestic political perspective, and before long you have a competitive death spiral of monetary policy decisions that sound good when you’re making the decisions, but end up putting everyone in a worse position and shrinking the global trade pie even further.

But, Ben, our monetary policy leaders aren’t stupid. They know what happened in the 1930s just as well as you do. Don’t they see that there is a strategic interaction at work here – a game, in the formal sense of the word – that requires them to take into account other leaders’ decision-making within their own decision-making process, understanding (and this is the crucial bit for game theory) that the other leaders are making exactly the same sort of contingent policy evaluations?

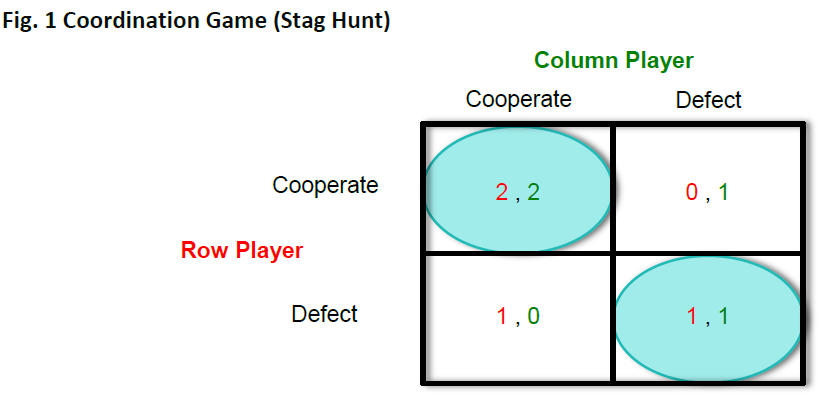

Yes, of course the Fed can see that there’s a strategic interaction here, and of course they’re playing the game as best as they can. But they’re playing the wrong game. They’re still playing a Coordination Game, which is ALWAYS the game that’s played in the immediate aftermath of a global crisis like a Great War or a Great Recession. They have yet to adopt the strategies necessary for a Competition Game, which is ALWAYS the game that’s played after you survive the post-apocalyptic period.

Here’s what a Coordination Game looks like in the typical game theoretic 2x2 matrix framework. If you want to read more about this look up the “Stag Hunt” game on Wikipedia or the like. It’s an old concept, first written about by Rousseau and Hume, and more recently explored (brilliantly, I think) by Brian Skyrms.

The basic idea here is that each player can choose to either cooperate (hunt together for a stag, in Rousseau’s example) or defect (hunt independently for a rabbit, in Rousseau’s example), but neither player knows what the other player is going to choose. If you defect, you’re guaranteed to bag a rabbit (so, for example, if the Row Player chooses Defect, he gets 1 point regardless of Column Player’s choice), but if you cooperate, you get a big deer if the other player also cooperates (worth 2 points to both players) and nothing if the other player defects. There are two Nash equilibria for the Coordination Game, marked by the blue ovals in the figure above. A Nash equilibrium is a stable equilibrium because once both players get to that outcome, neither player has any incentive to change his strategy. If both players are defecting, both will get rabbits (bottom right quadrant), and neither player will change to a Cooperate strategy. But if both players are cooperating, both will share a stag (top left quadrant), and neither player will change to a Defect strategy, as you’d be worse off by only getting a rabbit instead of sharing a stag (the other player would be even more worse off if you switched to Defect, but you don’t care about that).

The point of the Coordination Game is that mutual cooperation is a stable outcome, so long as the payoffs from defecting are always less than the payoff of mutual cooperation. This is exactly the payoff structure we got in the aftermath of a Great Recession, as global trade volumes increased across the board, and every country could enjoy greater benefits from monetary policy coordination than by going it alone. As a result we got every politician and every central banker in the world – Missionaries, in game theory parlance – wagging their fingers at us and telling us how to think about the truly extraordinary monetary policies all countries adopted in unison.

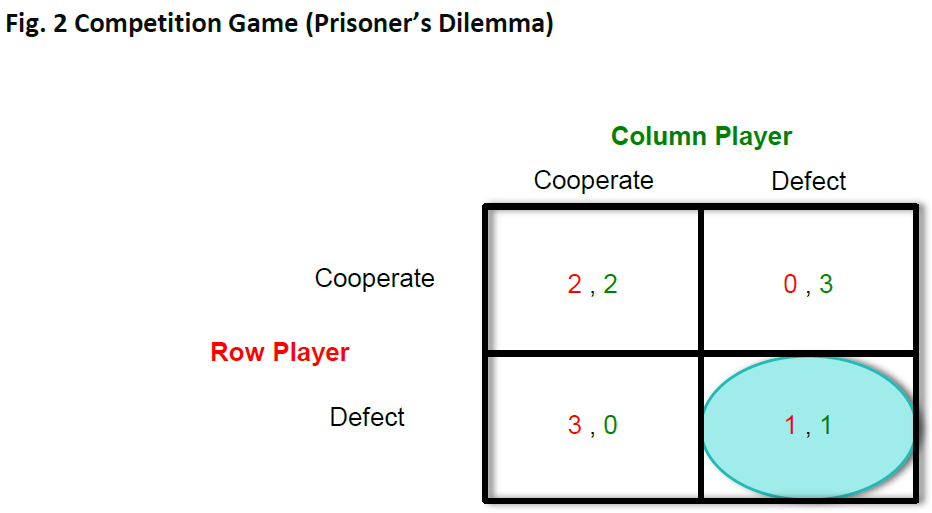

But when global trade volumes begin to shrink, the payoffs from monetary policy defection are no longer always less than the payoff of monetary policy cooperation, and we get a game like this.

Here, the payoff from defecting while everyone else continues to cooperate is no longer a mere 1 point rabbit, but is a truly extraordinary payoff where you get the “free rider” benefits of everyone else’s cooperation AND you go out to get a rabbit on your own. It’s essentially the payoff that Europe and Japan got in 2015 by seeing the euro and the yen depreciate against the dollar, and it’s the payoff that China hopes it can get through yuan devaluation in 2016. Ultimately, every country sees where this is going, and so every country stops cooperating and starts defecting, even though every country is worse off in the end, as no one gets the +3 payoff once everyone starts defecting. To make matters worse, the “everyone defect” outcome of the bottom right quadrant is a Nash equilibrium – the only Nash equilibrium in a Competition Game like the Prisoner’s Dilemma – meaning that once you get to this point you are well and truly stuck until you have another crisis that forces you back into the survival mode of a Coordination Game. Sigh.

Look, I understand why the Fed (and for that matter, important constituencies in the PBOC* and ECB*) want to keep playing the Coordination Game even when the writing is on the wall for a change in the game payoffs. It’s a much “nicer” game, where you’re baking a larger economic pie and everyone can be better off than they were before. Also (not to get too tinfoil hat-ish about all this), it’s the sort of game that academics and the Davos crowd love to play, as it allows them to gather in tony enclaves, congratulate each other on their intellectual prowess and service to mankind, and tut-tut about those pesky elections and benighted masses. Put in a less snarky way, the IMF and similar entities have an existential stake in promoting the Coordination Game. Not that there’s anything wrong with that.

But it’s no accident that everything, from exchange rates to commodity prices to global trade volumes, started to go off the rails in Q3 of 2014. That was the start of monetary policy divergence – a $10 word that means competition – as Yellen’s Fed announced an outright tightening bias and Draghi’s ECB went in the polar opposite direction with balance sheet expansion and negative rates. And I’m sorry to say it, but once you leave the cozy confines of the mutual coordination Nash equilibrium, you can never go back. Instead, it’s an inexorable one-way street to the other Nash equilibrium, mutual defection. It’s just math. And human nature. I wouldn’t want to bet against that combination.

The Golden Age, per the original Greek myth, was an era of unblemished cooperation and great deeds. The Silver Age, on the other hand, was a pretty miserable time to be alive. Not as warlike as the Bronze Age, and not the war of all against all as in the Iron Age, but the spirit of the age was one of strife and competition. It ends badly. But it’s not a hopeless time. It’s a time to protect oneself and one’s family for the harder times to come, and it’s also a time to plant the seeds that will flourish when this cycle ends. What’s required is seeing the world for what it is, not what we might wish it to be. That’s not easy, whether you’re a central banker or a small investor, but it’s never been more important.

*People's Bank of China and European Central Bank

To subscribe to Epsilon Theory:

Sign up here: www.salientpartners.com/epsilontheory/subscribe

OR send an email to bhunt@salientpartners.com with your name, email address, and company affiliation (optional).

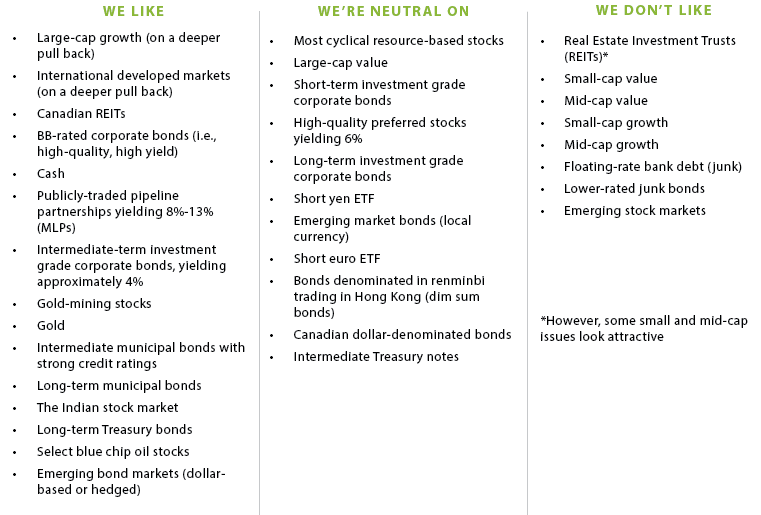

OUR LIKES AND DISLIKES.

No changes this week.

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness.