By David Hay

Don’t ask, don’t tell. Lately, I’ve begun to pose an uncomfortable question to both my investment professional friends (I still have a few) and to a handful of clients: What happens when the stock market quits going up? For now, let’s ignore the more unsettling notion of the impact of a deep correction and just focus on an extended sideways scenario. That wouldn’t be so bad, right? Unfortunately, for millions of Americans—and countless retirement plans—the reality is quite the opposite.

The dividend yield on the S&P 500 is currently around 2%. Ergo, if prices plateau, that will be the sum total of the return investors will receive. As frequently relayed in this newsletter, many experts with the best long-term forecasting records are predicting precisely this scenario for years to come, though they also suspect it will be a far more volatile future than my assumed extended flat-lining.

However, that’s only half the puzzle since most investors have some form of balanced portfolio. For argument’s sake, let’s assume a 50/50 mix between stocks and bonds (or other “high income” securities). The reason I put “high income” in quotes is that, these days, bonds are anything but. As for money market funds and CDs, they have been yield-free for years.

As a result, when the dreaded day of the S&P 500 topping out occurs—whenever that might be—investors will find themselves in one dicey dilemma. It’s interesting that, despite the fact the opening quarter of the year is almost always very strong (especially during bull markets), 2015 thus far has been oscillating between small gains and small losses. In other words, we are getting a taste of what it’s like when stocks stall out.

In this month’s Guest EVA, I am turning once again to one of my touchstones for coping with our increasingly surreal investment world, Charles Gave. Because Charles’ essay is fairly brief, I’ve created a longer than normal introduction to hone in on his main theme. I believe it is enormously important, particularly for all the baby boomers who are planning to live off their portfolio income for years to come.

In an essay Charles wrote last month, The Hidden Tax on Savings, he attacks the concept made famous by John Maynard Keynes commonly known as “the euthanasia of the rentier.” Rentier is just a fancy word for someone who lends money thereby deriving interest, a form of rent. By the way, for all you real estate “coupon clippers,” Keynes was clear that you were in his cross-hairs, too, when he wrote: “Interest today rewards no genuine sacrifice, any more than does the rent of land.”

Ironically, for a man who was by all accounts an extravagantly successful investor, he went on to write: “It will be, moreover, a great advantage to (what) I am advocating, that the euthanasia of the rentier, of the functionless investor, will be nothing sudden, merely a gradual but prolonged continuance of what we have seen recently…” (meaning a further collapse of returns on capital).

Although Keynes’ words were written in 1936, they are just as true now as they were then—perhaps more so. Those with capital to lend today have truly been rendered “functionless investors” or, certainly “return-less investors.”

And, as Keynes advocated, to avoid messy things like violent revolution, it’s far better to gradually euthanize the victims, kind of like a slow-motion Kevorkian procedure. Or, said differently, if you boil the frog slowly, he won’t figure out what’s happening to him until it’s too late.

Of course, some of the biggest beneficiaries of the euthanasia of the rentier are overly-indebted governments, which includes almost all of them in the developed world these days. Zero interest rates—or even negative rates as seen in 16% of sovereign bond markets currently—allow profligate fiscal authorities to put off addressing unaffordable entitlement programs.

Yet, there is an important element of the public sector that is also being slowly euthanized: state and local government retirement plans. These still assume 7% to 8% rates of return, which are almost certain to be proven ludicrously high in the years to come. Many corporations are in a similar bind though the private sector has been diligently striving to get out from under defined benefit obligations, putting the problem squarely on the shoulders of their eventually retiring employees.

Then there is the insurance industry, where non-existent interest rates make it nearly impossible to fund their guarantees to policyholders. Many will feel they have no option but to play dangerous games involving derivatives and/or leverage to goose returns. This runs the risk of insolvency if these tactics blow up, as they so often do. However, insurers may rationally conclude they are headed that direction anyway, so they might as well roll the dice.

As Charles points out, the euthanasia of the rentier amounts to a wealth transfer from the private to the public sector, essentially a stealth tax. He estimates this amounts to roughly 2% of GDP annually and is behind much of the highly heralded Federal budget deficit shrinkage.

He also asserts, with strong data to back it up, that these eras when interest rates are too low lead to poor economic performance. This is due to a shortage of investment in the productive parts of the economy. As Charles observes, low interest rates depress savings, which in turn reduces investment in capital assets, leading to poor productivity—the oxygen of economic growth. This is exactly what we’ve seen in the US for nearly fifteen years. In fact, we’ve just experienced the worst five-year growth in capital spending since WWII. And this was during an expansion!

Like the frog who initially enjoys the warming water, the process of destroying returns on capital is initially a pleasant experience. The collapse of interest rates drives up the value of stocks, bonds, real estate, collectibles—basically, almost everything—to unreasonable levels. This actually makes the “functionless investor” giddy as a result of her or his paper profits. But no real wealth, at least of an enduring nature, is created.

This eradication of interest rates’ does raise an interesting (sorry for the pun) question: What should an investor in need of livable cash flow do in this yield-gone-missing world? With central banks so intent on forcing investors out of cash, but with the incentive to extend maturities having been reduced to almost nothing, maybe resisting this temptation is advisable. Basically, much of the world is in a flat-yield curve, clustered around zero. The situation in North America is better, but not much—unless one is willing to buy the formerly exalted, now detested, MLP sector or venture up to Canada, the land of 7% yielding REITs. Other than that, and a few BB-rated US corporate bonds, the pickings are super-model thin. Thus, holding some cash seems appropriate.

Keynes seemed not to appreciate the lifetime of work behind the capital built up by most “functionless investors.” Consequently, he had little empathy for the plight of those who needed more than a miserly yield on which to live. Judging by prevailing conditions, neither does our current generation of monetary mandarins.

THE HIDDEN TAX ON SAVINGS

Charles Gave

Frederic Bastiat, the great 19th century French liberal thinker, observed that mediocre economists spend plenty of time talking up the immediate beneficial impact of their measures, but usually ignore the less obvious long term effects. He summarized this view with the pithy observation: “In economics, there is what you see and there is what you don’t.”

An excellent example of this dichotomy can be seen in responses to the monetary policy settings of the main central banks. By adopting negative real short rates policymakers are effectively enshrining a “false price”. You might expect trained economists to oppose such an abrogation of control. But then again, for those high priests of the Keynesian church, it is clear that both “capitalism” and “markets” are flawed beasts which need the assistance of an “anointed” class who know both what the public want and the level of interest rates at which an optimal outcome can be achieved.

The economists of the Keynesian church believe that every slow-down, each recession, and depressions of all varieties stem from an “excess of savings”, leading to an insufficient level of “final demand”, and from there to a sub-optimal employment level. To correct such a calamitous state of affairs, the solution is for the government to hire ever more people and for this “employment” to be financed by escalating state borrowing.

Needless to say, the government must borrow funds at a subsidized level against the interests of stodgy old bond investors—Keynes solution to the problem of “excess savings” was, of course, the “euthanasia of the rentier”, which can be simply thought of as policies that penalize savers. Unfortunately, every subsidy paid to somebody (what you see) is a tax on somebody else as a counterpart (what you do not see).

Of course, in the case of negative real rates, the subsidy is paid by the saver to the borrower, which more often than not means a transfer of wealth from the private to the public sector. As a matter of fact, negative real short rates is in fact a tax on savings—the very worst kind of tax.

The aim of this paper is to show the effects on an economy of such a move which is at the same time (i) an increase in taxes, (ii) a form of protectionism (the currency depreciation effect), (iii) an increase in regulation (controlling the price of money) and, of course, (iv) a massive monetary policy mistake since it leads to money flowing from the private sector to the government. Historically, such policies have led to wars (remember the 1930s). I’ll illustrate my argument using the US economy, but the results are generally applicable.

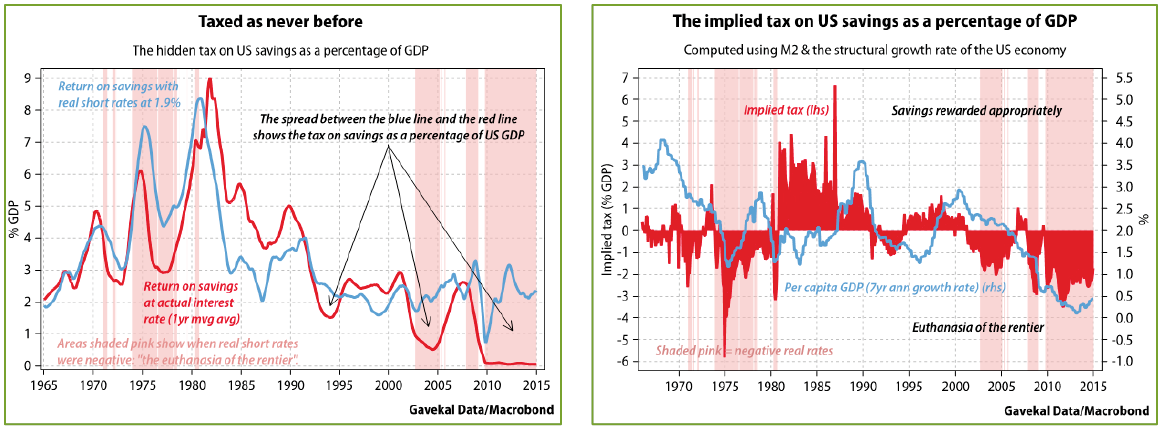

To start our analysis, consider the size of the transfer from US savers to US borrowers that results from this policy approach. The monetary aggregate M2* can be used as a proxy for the inventory of savings. In the chart below (left), the red line represents the return on savings using the market rate as imposed by the Federal Reserve while the blue line shows what returns would have been if real short rates been maintained at 1.9% which is their average since 1950. The pink shaded area shows periods of negative real rates or times when the rentier was put to the sword.

* M2 is a broad measure of money supply

Since 2002, the tax on savings (the difference between the blue and the red lines) has averaged roughly 2% of US GDP, as it did in the 1970s. Hence, it is clear that both the ‘70s and the last 13 years have been “Keynesian periods”. The two worst recessions since 1950 (1974, 2008-2009) occurred after such a policy was applied, which is not very surprising. Next, we need to compute the arithmetical difference between the blue and the red line in order to show the size of the hidden tax on savings as a proportion of the US GDP (see the chart above, right).

Since outstanding US government debt is about the same size as US GDP it is fair to assume that government spending as a share of domestic product would be at least 2% higher than officially announced in the event that the Federal Government had to pay a proper fee to borrow. Indeed, the much vaunted decrease in government spending as a proportion of the national economy is probably an accounting illusion.

Moreover, the transfer is from the saver to the government, which is seldom a recipe for improved economic growth. Indeed, each time there has been a big increase in the taxation borne by savings, the structural growth rate of the US economy (the seven year growth rate of GDP per capita) has fallen by at least half. In the 1970s the annual growth rate of GDP per capita fell from 3% to 1.5%; since 2002 this measure has declined from 2.25% to 0.5 %. Bravo Fed!

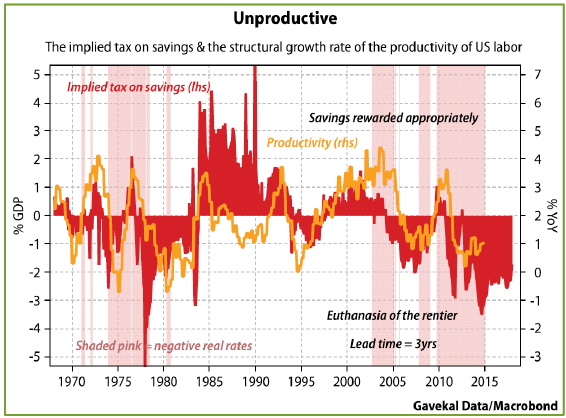

This fall in growth stems from the unavoidable decline (with a lag of a few years) in the growth rate of productivity stemming from the lower level of savings, which must result in lower capital spending. After all, investment (I) is ultimately a direct function of the savings (S) level (I=S). When “S” declines, so “I” must follow, and if “I” falls productivity is not far behind.

From 1917 to 1990, much of the world was in thrall to Marxism or Scientific Socialism which was nothing but a form of magical thinking. One would have expected the bankruptcy of Marxism to lead to the class of “anointed” policymakers being more modest in their ambition. Fat chance. Marxism has been replaced by Keynesianism, replacing Scientific Socialism with an equally false science in the shape of “Econometry” or the use of statistical techniques to validate all manner of nonsense. Personally, I cannot wait for the Berlin Wall to fall again.