"Sir: The next financial apocalypse is imminent. I know this to be true because the House and Home section is now assuming the epic proportions last seen before the great crash. 24 pages chock full of adverts for mansions and wicker tea trays for $1,000. You’re all mad. Sell everything and run for your lives."

- Anonymous reader in a letter to The Financial Times last fall.

"Why not go out on a limb. That’s where the fruit is."

- Will Rogers

POINTS TO PONDER

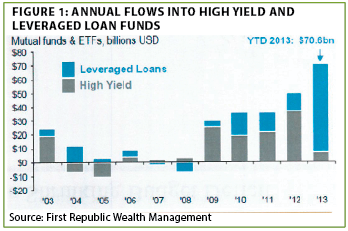

1. It’s fair to say that repeated warnings in this newsletter about the overvaluation of the US stock market have been, to say the least, "premature." However, our cautions about the junkier reaches of the high yield market, as well as leveraged bank loans, were quite timely. As is so often the case, extreme inflows into these asset classes in recent years provided an excellent heads-up. (See Figure 1.)

2. Stock market bulls—who might be feeling their oats a bit less these days—may also want to be aware that two of America’s billionaire investors believe there are bubbles in various portions of the US stock market. Both real estate tycoon Sam Zell and financier extraordinaire Carl Icahn have noted the extreme overvaluation of certain sectors and stocks with exciting stories.

3. According to the elite research firm, Capital Economics, the implosion by oil prices should add between 40 and 80 basis points (0.4% - 0.8%) to US GDP growth. This is significant considering the US economy has been growing at an average rate of less than 2% over the last fifteen years.

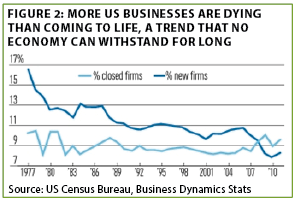

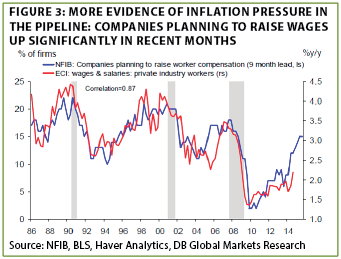

4. There is little doubt that the jobs market has improved dramatically for the most employable workers. Even long-beleaguered small businesses are reporting that they are paying out higher wages. On the downside, the trend toward more business failing than being established is a long-term concern. (See Figure 2 and Figure 3.)

5 Our current economic expansion has lasted 67 months versus an average lifecycle of 58 months since WWII. This validates a long-term EVA thesis that this upturn’s sluggishness would likely allow it to last longer. Barring some kind of external or financial market shock, the US economy looks poised to continue growing, aided by lower oil prices, as noted above. The odds of a "profits recession" (two quarters of falling earnings) are rising, however. This is due to the soaring dollar and, ironically, imploding oil prices which are nuking profits in the energy sector.

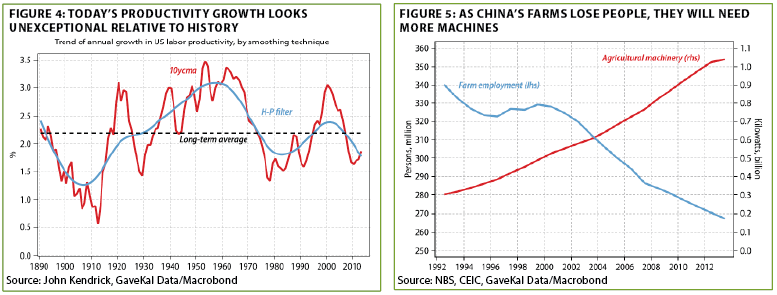

6. It is merely stating reality to observe that the ultra-important factor of productivity is in a long-term downtrend, recently nearing a post-war low. There could be multiple causes for this situation, such as ill-advised Fed policies that have lead to poor capital allocation (i.e., condo-flipping over infrastructure investing). Yet, the reality is sluggish productivity combined with an aging population is a major problem that is certainly not being discounted by one of the most expensive US stock markets of all time. (See Figure 4 below, left.)

7. Not all parts of the American stock market are richly valued. In addition to energy stocks, shares in agriculture companies remain intensely out-of-favor despite the mega-trend in China where rural works continue to migrate to cities by the tens of millions. Consequently, the demand for US farm machinery, as well as fertilizers, should continue to increase at a healthy clip over time. (See Figure 5 above, right.)

8. There’s little doubt that the biggest shock this week was the Swiss National Bank’s (SNB) decision to let its currency rise or, more accurately, explode to the upside. Incredibly, the Swiss franc gained 30% against the euro at one point on Thursday alone, triggering a nearly 9% plunge in Swiss stocks. This dramatic action came despite repeated and recent assurances "the Swissie" would continue to be pegged to the euro. Stay tuned for considerable fall-out from this development.

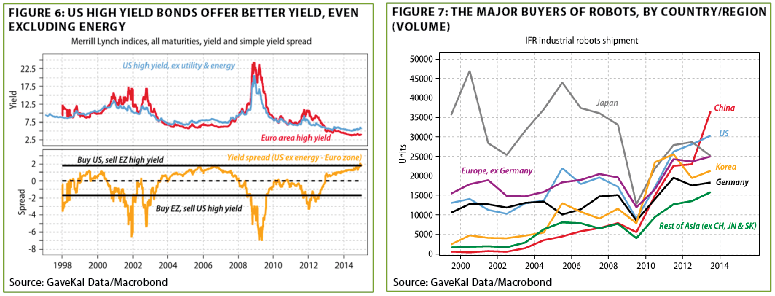

9. In addition to US treasuries yielding more than most European sovereign debt, domestic high-yield bonds also offer considerably loftier rates than are available on the Continent. As with government issues, this anomaly seems unlikely to persist long-term.

10. Japan was once by far the dominant buyer and user of industrial robots. Lately, though, China and the US have both eclipsed the "land of the setting yen," dramatically in the former’s case. (See Figure 7 above, right.)

THE EVERGREEN EXCHANGE

By David Hay, Jeff Eulberg, and Tyler Hay

Shooting fish in a barrel? As often happens, shortly after hitting send on last week’s Annual Outlook EVA, I began to have writer’s remorse. This particular attack was due to the realization that many readers would think my extra credit forecast—which is also my highest conviction prediction—was about as bold and insightful as saying that Greece would soon default—again—on its debt. (To read last week’s 2015 forecast, please click here.)

Accordingly, I thought that I should go out on the limb quite a bit more (hat tip to Will Rogers) and say that if it merely increases somewhat I will count that as a miss. In other words, unless, at some point during this year, US stock market volatility has a major surge—beyond what it experienced last October—I will eat more of my favorite fowl, as in crow (and that certainly has had a foul taste!).

As you will soon read in this week’s Evergreen Exchange edition, Tyler is once again taking the more sanguine view. His belief (though certainly not his strongest conviction) is that volatility is likely to return to a more typical range. Further up the scale, Jeff Eulberg is making the argument that the world is much too unstable—geopolitically, economically, and financially—for such a tapioca-like outcome. And, of course, I get the thankless job of pointing out how perhaps the Financial Times letter-writer quoted above may not be one sandwich short of a picnic, as the English are wont to say.

First of all, I thought a basic explanation may be in order. Many EVA readers might wonder how come increased volatility is a bad thing. After all, why can’t wild price moves be mostly on the upside? It’s a reasonable musing but the reality is that all prior periods of major volatility spikes have corresponded with corrections or bear markets. Certainly, the experience with commodities lately validates that view. This reality may be a function of the old market axiom that stocks go up on an escalator and down on an elevator. In fact, I believe that is true of almost every asset class, not just equities.

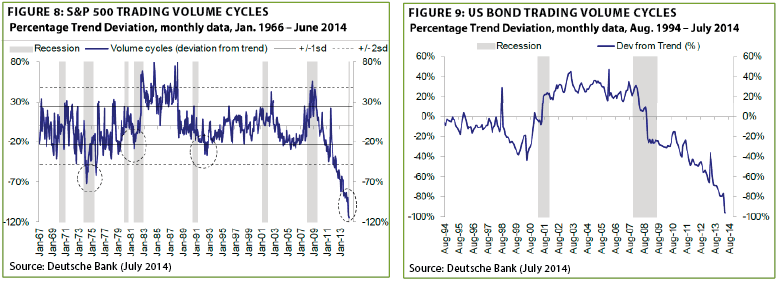

One fairly obscure factoid that I believe may lead to a fluctuation explosion—in the usual adverse direction—is trading volume. As you can see on the next page, courtesy of the cerebrally-gifted Ben Hunt, volume has gone the same way as risk-free interest rates—as in, adios muchachos. (See Figures 8 and 9 below.)

Clearly, volume has not just gone missing for stocks. The even larger bond market has seen an equally stunning drop off. This was driven home to Evergreen’s investment team when we went to sell a large block of a high-grade bond in mid-October and couldn’t locate a single buyer. And that was in a mini-, not maxi-, panic.

Thin volume is not an issue in a rising market. Actually, it’s kind of fun if you’re long the asset in question as it usually goes up far more than it would—or should—if liquidity was deeper. But in a falling market, the reverse plays out—most painfully for those still holding the bag security.

Besides thin markets, exaggerated price swings also typically require overvaluation brought about by years of rising prices and a pervasive confidence that any declines will be mild and fleeting. The leading Wall Street strategists remain utterly unperturbed by today’s market valuation as, once again, they are unanimous in their belief stocks are heading higher in 2015 ("Sunny Jim" Paulsen is an intriguing exception to that consensus view). In fairness, this same group was right about stocks in 2014, though they were just as uniformly wrong about bonds, especially treasuries, last year.

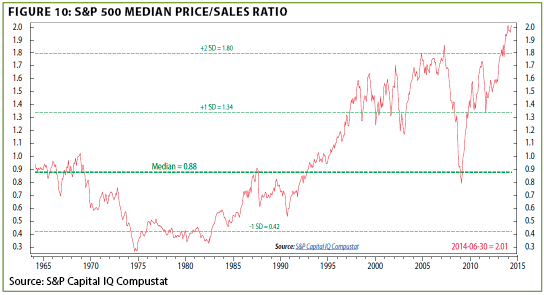

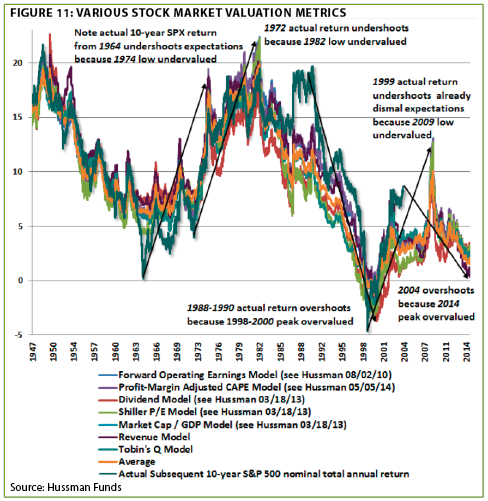

Arguing about the fair value for stocks is right up there with debating how many angels are doing the salsa on the head of a pin. But, to reiterate one of our old refrains, focusing on the price-to-sales ratio removes a lot of the confusion. This is because it defuses so many complicating aspects like the impact of share buy-backs, as well as profit margins and, similarly, peak (or trough) earnings. Last week, we mentioned that on this basis the median stock is above the super-bubble peak in early 2000 but a visual is always more powerful.

Lest you think I have early onset dementia (which, actually, a number of clients have been wondering about lately), I do realize I’ve run this one previously. Yet, I believe it and the following also-ran-before chart are really all you need to know about whether this stock market is over- or under-priced. The proceeding graphic not only includes price-to-sales (revenues) but various other yardsticks that have been proven over time to reveal whether the market is cheap or dear (and there’s no doubt, my dear, that it ain’t cheap!).

Interestingly, the still-bullish Ned Davis himself, one of the investment industry’s living legends, has pointed out that while the highly controversial Shiller P/E has done poorly as a "short-term timing device," it has been most effective at projecting returns over the next decade—at least since 1881. But, heck, that’s only 134 years so maybe we need to wait until there’s a larger sample set!

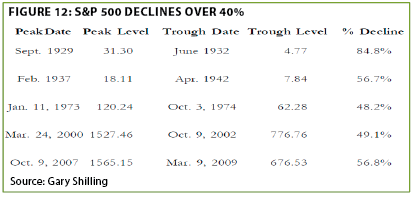

Now I’m going to close my section of this EVA with a chart I haven’t run before (please, no fainting), thanks to that graph-machine (note, I didn’t say "graft-machine"—that would be Washington, D.C.), Gary Shilling.

What caught my eye about this one is that since the late 1930s, there have only been three 50% type declines. Yet, two of them have happened in the last 14 years. Am I being fooled by randomness or could there be valuable information in this? Could it be that over the last 20 years when the Fed has sought to micro-manage the economy, and even asset prices they’ve created the ideal conditions for hyper-volatility?

The jury is still out on this but when you ruminate on the two prior charts it’s hard to dismiss the possibility there could be another 2:1 stock split, without any additional shares in the mail, coming. In other words, what if we see the third 50% off-sale in the not too distant future?

Trust me, I don’t want to see this happen because, as I’ve written before, I’m certain Evergreen will be guilty of "premature accumulation syndrome" on the way down. But, also trust me, it’s not the remote possibility most of Wall Street would like you to believe.

![]()

The European roller coaster. Over the past eight years, European markets and global investors have experienced a rather tumultuous relationship. In 2007, the euro was so popular rapper Jay-Z made headlines when in a music video he famously flaunted a briefcase overflowing with euros, rather than the typical US dollar-filled attaché. Then in 2011, European peripheral debt concerns led global investors running for safety—nearly causing a bear market in the US. In 2012, after peaking at $1.60 versus. the dollar, the euro traded all the way down to $1.22 on fears that the crumbling Greek economy might lead to a potential eurozone breakup. As government bond yields soared, European Central Bank (ECB) Chief Mario Draghi famously proclaimed to be willing to do whatever it took to preserve the euro, immediately sparking an immense turnaround for European asset prices. The euro regained its footing versus dollar and peaked at $1.44 in 2014. European equities rallied over 61% since 2012 and government bond yields went from the high single digits down to levels never seen before in many European countries.

As we start 2015, the euro is crashing, trading at $1.16 versus the dollar. Market volatility is back, and in a déjà vu like event, eurozone membership concerns are flaring up throughout the union. As with any relationship, you can only pretend that problems are solved for so long. While we’d agree that it’s unlikely a divorce will happen anytime soon, a drawn out fight within the eurozone could very well dictate the direction of global markets in 2015.

In the second half of last year, hopes of a broad eurozone recovery evaporated. GDP hovered just above 1%, and deflation concerns were heightened as the fourth quarter inflation rate was just 0.44%. Forecasts for 2015 aren’t much better; the ECB expects inflation to barely stay positive and GDP growth to limp along at 0.8%. Due to these dreary expectations, the central bank is now being asked to do more. On January 22nd, the ECB is expected to announce a large-scale quantitative easing (QE) program in an effort to ward off deflation and revitalize growth in the lifeless economy. While we think an announcement will be made, the efficacy of such a program, and the magnitude, may leave many investors disappointed.

Begrudgingly, Germany appears to be going along with the plan, but with interest rates at or close to all-time lows, and the currency already depreciated significantly, the results are unlikely to provide the catalyst necessary for the European economy to stabilize. In the US, where some have anointed QE as the saving grace for the economy, GDP averaged less than 2% growth after nearly $4 trillion was infused into the financial system. And as I’ve written in the past, Germany won’t be willing to keep the figurative printing presses going with such lackluster results. Structural reforms are the true solution needed to get the European economy on the right track, and unfortunately, not one politician has the backbone or support needed to force these changes through reluctant bureaucratic and vested-interest channels.

Beyond just the German hesitation to go along with such programs, Greece again has become an unwanted distraction for the ECB. On January 25th the Grecians will be heading back to the voting booth in a snap national election. Recent polls have the leftist Syriza party, headed by 40-year-old Alex Tspiras, comfortably in the lead. In 2012, Tspiras made a name for himself as the young and brash leader of the then anti-European party. Since, Tspiras has softened his anti-euro stance and now intends to remain in the euro (as 74% of Greeks would prefer), but promises to re-negotiate the austerity programs agreed to during prior bail-out negotiations with the ECB and the International Monetary Fund. While it appears that Syriza will win the general election, it’s likely that they’ll lack the votes necessary to form a controlling government, forcing the winning party to establish a coalition government with smaller centrist parties. Thus, Syriza’s hard-line negotiations will likely soften, or a resolution in Greece is unlikely anytime soon. The voting process can be dragged out over three separate elections if necessary, and could potentially delay the desired QE longer.

The initial reaction for many observers is to downplay Greece because the economy is so small it doesn’t really move the economic needle. However, the precedent of a Greek exit could lead other more important nations to consider making the same move. It was recently reported by German newspaper Der Spiegel, that German Chancellor, Angela Merkel, now believes that the economic bloc could handle an exit. While this may be the case, the unknown ramifications of such an event would add quite a bit of volatility throughout global markets.

For investors who downplay Greece, they should realize that the small coastal country is not alone in questioning the benefits of using the euro as its currency. Nationalistic parties are gaining steam throughout the EU. France’s National Front party is believed to be the front-runner for the 2017 national election with over 25% of support. The Euro-Hostel Alternative for Germany party has grown from a small fringe group to gaining legitimate credibility as a threat to the establishment. Spain’s anti-austerity party, Podemos, is currently the leader in recent electoral polls. Further, the tragic events at the Charlie Hebdo offices in Paris, along with other terrorist attacks throughout Europe, are only strengthening these xenophobic voices.

In the US, the actions of the Federal Reserve appear to have the grabbed the sole attention for most market participants. Yet, the most concerning element today amongst governors who sit on the Federal Reserve board is likely the malaise that is spreading around the world. The last thing the Fed wants to do is raise rates in the midst of a global recession, and while a recovery in Europe is possible, the political maneuvering required from the ECB, and local politicians, would require a heroic feat. This year is setting up for many disappointments throughout Europe, and while talk was enough to appease investors in the past, this time investors are likely to demand action—if it’s not already too late. Thus, I believe financial market volatility is poised to surge to levels not seen since 2012.

On Thursday, the Swiss National Bank (SNB) stunned global markets by removing the ceiling placed on its currency, allowing the Swiss Franc to appreciate nearly 30% versus the euro at one point in the trading day. The move caught traders off-guard because just Monday of this week the SNB said that it remained committed to the ceiling. This may be the first signal that we’re nearing the end of the "era of central bank omnipotence," and they will no longer be able to dictate market prices based on the fact this was such a credibility-shattering "180." Hopefully, we’re heading back to an era where fundamentals and true market forces determine values. This sea change will be good for markets in the long run, but will likely cause painful re-pricing for global assets. Over the last two years, central banks have done a fantastic job keeping volatility subdued, but once the manipulators lose control of the markets, as seemed to happen yesterday, who knows where the floor is? Maybe now we’ll see what the price tag is for all of that suppressed volatility. My guess is it won’t be like filling up your gas tank these days.

Can stocks keep defying gravity? While I concede 2015 could certainly be a volatile year for the reasons Jeff Eulberg and David Hay have outlined in their respective sections above, I want to propose an alternate viewpoint for the markets that is hopefully worthy of some consideration.

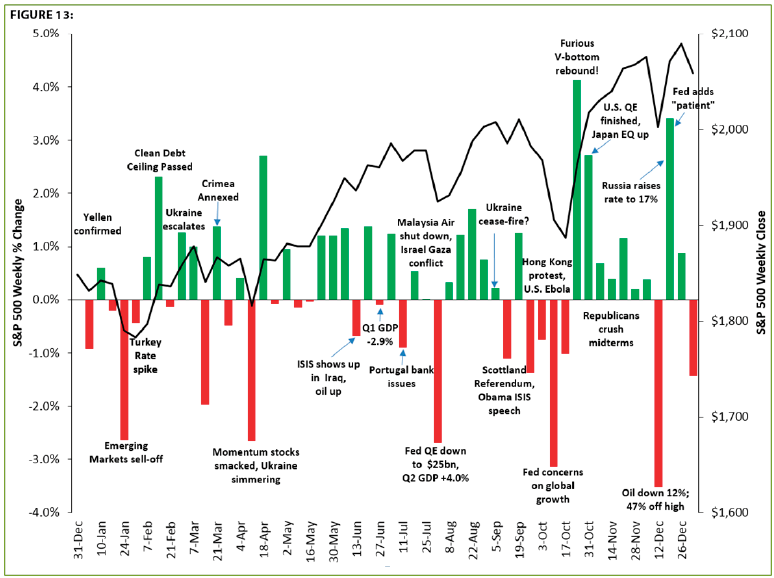

If you recall, going into 2014, expectations for stocks were still surprisingly high, even after the S&P 500 had returned a scorching 32% the year prior. A "Round Table" in Barron’s surveyed 10 of Wall Street’s "smartest" strategists, and all were expecting another positive year for stocks for 2014. (It’s worth noting that not a single strategist has forecasted equity prices to decline since 2012.) As the year begun, lingering concerns of a slowdown in China, Fed uncertainty, and lackluster economic growth had all the makings of delivering a return to more normal levels of volatility. Yet, despite a surge toward the end of 2014, volatility remained near decade lows, with most fluctuations skewed clearly to the upside.

Perhaps this was because, as "they" say, a bull market climbs a wall of worry and, beyond those issues cited above, it was one towering wall! Russia—or, should I say, Putin—signaled to the world that he does not respect Ukraine’s sovereignty, nor does he fear related consequences for his incursion. The markets barely stumbled in April as a result of the conflict and bounced back with great resiliency. Next, investors shrugged, after some initial spasms, as Ebola made its way to American soil for the first time. In Asia, the eyes of the world watched closely as the Chinese government averted a repeat of Tiananmen Square as protests flared in Hong Kong, but, once again, the stock market hardly flinched. Perhaps unsurprisingly, the two largest weekly drops for the S&P 500 came on the backs of Federal Reserve concerns over slowing global growth and the shocking collapse in oil, but even those two declines saw their losses nearly recouped only one week later. (See Figure 13 below.)

Now, it’s possible that a larger scale exogenous shock to the financial system occurs in 2015 and leads to a major market shakeout. It’s also possible that an overextended equity market simply doesn’t digest any negative surprises quite so easily as we saw last year. However, I believe that the same conditions that were in place in 2014—and allowed the US stock market to remain unflinching in the face of uncertainty—remain at work in the coming year. A strengthening American economy and a Fed eager to rescue the financial markets have given investors tremendous confidence in equities and that’s not likely to change in the near future.

The recent upward revision to GDP, along with low unemployment and a massive de facto tax cut due to lower gasoline prices, seem to confirm that the economy is in fact on stronger footing. The US economy has long been called (perhaps way too often, including by us) the cleanest shirt in a pile of dirty laundry but that may no longer be a fair analogy. Maybe now the shirt is actually clean. If this is true and the economy is really stronger we should turn our attention to the Fed.

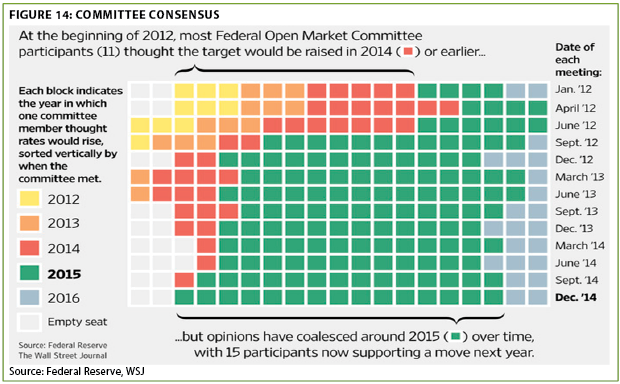

For those who think that tough talk from the Fed about raising rates make that scenario a virtual certainty, a quick refresher of their historical behavior may be useful. (See Figure 14 below.)

Since January of 2012, the Fed has been saying that it is targeting a rate hike in 12-24 months. Yet, we haven’t seen a single raise. If it finally does follow through, this would mean two things: First, it would signal the Fed believes the US economy is indeed strong and can sustain an increase in the cost of capital. After all, since the financial crisis, even the smallest blip in economic data has sent it running to the rescue with monetary "tools" and calming words. Second, and possibly most important, it means the Fed will be taking the risk of its rate hikes serving as the pinprick that bursts the equity market bubble (particularly in small- and mid-caps as well as the "cult" stocks, i.e. TWTR). The Fed seems very reluctant to take that chance. Back in December plummeting oil prices began to seriously worry investors and quickly Fed Chair Yellen calmed fears by saying the Fed "can be patient." The market responded by posting its largest one-day gain in three years.

In a lot of ways, no matter how I begin my writings lately, I find myself landing back in the same spot. The Federal Reserve has built a floor for the markets over the last seven years. At some point it will stop working (note: I didn’t say the Fed would stop trying). Even if it raises rates this year, that alone is not all that interesting. What’s interesting is what the Fed will do when the markets begin to wonder if its crutch is gone for good. Remember that many investors have become equity market participants through coercion not choice. Retirees who have long been able to generate modest "cost of living" type returns with relatively little risk have had to buy equities. This could make for a very painful adjustment as these investors flee to where they belong. It’s a question of when—not if—this happens, but I’m just not as convinced as some (first name is David!) it will be this year.

![]()

IMPORTANT DISCLOSURES

This report is for informational purposes only and does not constitute a solicitation or an offer to buy or sell any securities mentioned herein. This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. All of the recommendations and assumptions included in this presentation are based upon current market conditions as of the date of this presentation and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. Information contained in this report has been obtained from sources believed to be reliable, Evergreen Capital Management LLC makes no representation as to its accuracy or completeness, except with respect to the Disclosure Section of the report. Any opinions expressed herein reflect our judgment as of the date of the materials and are subject to change without notice. The securities discussed in this report may not be suitable for all investors and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. Investors must make their own investment decisions based on their financial situations and investment objectives.