“There’s clearly a buyers strike in the market for state and local government debt that

is largely based on fear and misperception. The mass selling of munis, which represent

the bedrock of the US economy, is incredible.”

- Influential strategist and economist DAVID ROSENBERG

POINTS TO PONDER

1. The powerful 20-month rally in real estate investment trusts, combined with the recent pummeling of tax-free bonds, has put munis in the very strange position of yielding more than REITs. In the last ten years, this happened just once, at the peak of the real estate bubble.

2. Underscoring once again how divergent the economic performance is between northern and southern Europe (as well as Ireland), in 2010, Germany reported its strongest GDP growth in a generation.

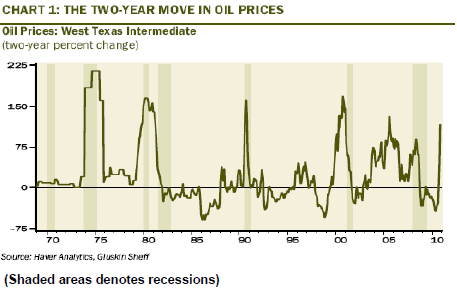

3. Another unintended―and undesirable― consequence of the Fed’s QEII program has been the spike in oil prices. These are now up 130% in the last two years and rarely in the past has such an increase not led to an economic slowdown or recession.

4. Even as billions of dollars flow out of battered municipal bonds funds, net speculative long positions are at or near record highs on the Kansas City Board of Trade and the Minneapolis Grain Exchange. Specific commodities at multi-year peaks of open interest include crude oil, platinum, palladium, corn, soybeans, cattle, and copper.

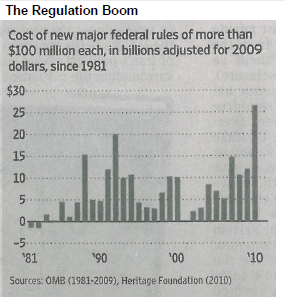

5. One reason that business confidence has been slow to recover, despite exceedingly robust profits, may be the unparalleled increase in regulations. This has likely inhibited both capital expenditures and hiring. Recently, however, the Obama administration has indicated a willingness to roll back some of the more onerous rules.

Correction: Last week’s issue contained a statistic about California’s population change that was erroneous. My source on this was a recent Wall Street Journal article stating that 2,000,000 California residents left the state over the past two decades. Due to a questioning EVA reader, we looked into this statistic further and found that it ignored organic population growth (births over deaths) as well as immigration. In reality, California’s population rose by roughly 7,500,000 since 1990 despite the 2,000,000 exodus referenced in the Journal article. I apologize for the error.

EVAluating the Environment

And the beat(ing) goes on. It’s not hyperbole to say that when it comes to tax-free investing these days it’s not your father’s municipal bond market. In my own case, that’s more than a sound bite as I vividly remember the elation my dad felt back in 1975 when he finally sold his company after 30 years of hard labor.

Interest rates in the mid-1970s were on the rise and he was able to get around 7% on his modest buy-out sum. Of course, for those of you old enough to remember, rates were in the early stages of the most radical increase in US history. It wouldn’t be that many more years before he could have gotten 14% on high-grade municipal bonds and he did live long enough to see those previously inconceivable yields. In fact, bonds in general did so poorly for so long that they became known as “certificates of confiscation.”

Dad never complained, however; he was always thrilled with the monthly check he got and seemed continually amazed that it was truly tax-free. He also never worried whether it would show up in the mailbox in the same steady amount (even if inflation was eroding much of its value and would often even exceed his yield). After all, everyone knew that municipal bonds were unquestionably safe.

Like so many aspects of life today, things have changed in a big way. To be fair, even back then, New York City was on the edge of solvency but there was never a sense of widespread defaults. Presently, however, fears of a wave of municipal bankruptcies are going viral.

Meredith Whitney achieved much deserved acclaim for her timely warnings about the volcano of bad loans the banks were sitting on a few years ago. Lately, she has turned her skeptical eye toward the municipal bond market. In a December 19th 60 Minutes interview, Ms. Whitney threw the tax-free world into a tizzy by predicting 50 to 100 “sizable” defaults that would collectively run into the hundreds of billions.

Her comments came only nine days after muni bonds had been favorably commented on in the December 10th EVA. So, is it crow-eating time for yours truly?

2009 all over again? A little chronological recap is in order to understand why I’m not nearly as bearish as Ms. Whitney is right now. First, by the time her interview appeared on the tube, tax-free bonds had already been thumped. As a result, they were offering yields exceeding lower rated (i.e., riskier) taxable bonds. Thus, it seemed to me that many of the fears she articulated were already discounted.

Second, a belief had descended on the market that credit problems were endemic throughout the municipal complex. The evidence of this was that even pristine borrowers had seen their borrowing costs spike. It was clear that despite the normally jovial spirits prevalent during the holiday season a bit of selling hysteria was in the air.

Finally, due to the year-end expiration of the Build America Bond (BAB) program there was a rush to market by municipal issuers (even though these are taxable bonds that receive a federal subsidy, they created competitive supply). In essence, there were a lot of sellers at year-end while normal buyers were both seasonally distracted and at least partially paralyzed by abundant scare talk even before Ms. Whitney’s broadsides.

Perhaps unsurprisingly, her bleak views generated a powerful backlash from bond market heavyweights who took exception to an erstwhile bank analyst belittling one of their brood. Most notable was the ever ubiquitous “Bond King,” Pimco’s Bill Gross, who has been repeatedly in the press defending tax-free bonds. Mr. Gross put an exclamation mark on his endorsement by announcing that he was putting millions of his own money into munis to capitalize on the selling spasm.

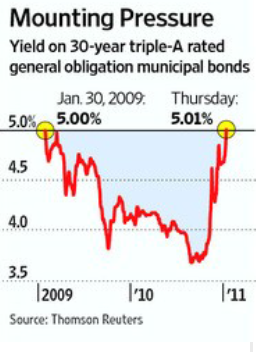

For a time, the tax-exempt debt market appeared to be stabilizing, but last week saw another bout of weakness as a New Jersey agency was forced to reduce a capital raise by 40%. Meanwhile, fund giant Vanguard opted to shelve three pending muni fund offerings. This latest turmoil has now pushed the yields on long-term tax-free bonds back to where they were in early 2009, when the credit crisis was at its most terrifying.

These latest developments are actually consistent with my views in the December 10th EVA when I warned of a very real chance of a “mini-panic…escalating into the maxi-variety.” With yields threatening to break above their 2009 peak, it does seem like we are entering true panic territory.

Having survived―by my hangnails―the unparalleled collapse in high-grade cor-porate bonds during the Great Recession/Credit Cataclysm, I have tremendous respect for how far markets can overshoot. Therefore, I will readily concede that 5% may not be the zenith in rates. But that does not mean AAA tax-exempt bonds bought at today’s prices won’t turn out to be very good investments over the next few years.

In fact, it’s hard for me to believe that times are worse now for municipal credits than they were in early 2009 when the economy was doing a cliff dive and the global financial system was in cardiac arrest. Certainly, the US stock market presently isn’t signaling that kind of trauma.

So what’s an investor to do? In that regard, it might be helpful to consider that Ms. Whitney and Mr. Gross’ views aren’t as diametrically opposed as they appear at first blush.

And the panic thickens. Interestingly, despite her Cassandra-like outlook on munis, Ms. Whitney also admitted she doesn’t see a single state reneging on its debt. Her negativity, quite appropriately in my opinion, is focused on US cities where numerous defaults are as certain as exorbitant Wall Street bonuses in December.

This means that she doesn’t believe even the fiscally precarious state of Illinois will default, an opinion that Mr. Gross also shares (though he said he wouldn’t buy its debt at prevailing rates). Nonetheless, yields on debt from all states and particularly the bad boys of the muni market—Illinois, California, and New Jersey—continue to charge higher.

In California’s case, it now yields more than taxable debt from its southern neighbor with a long history of debt restructuring and US-orchestrated bailouts (Mexico was saved from a catastrophic default in the 1980s by former Treasury Secretary Nicholas Brady).

Another reason why it appears to me that we are fast approaching a selling climax is the huge volumes of bonds being offered for sale. My team and I have been inundated with offerings in the last week, including one particularly large “bid-wanted” list from a major bank. Vanguard was reported to have $200 million of muni bonds for sale and several other fund groups were said to be seeking accelerated settlement dates, indicative of urgent needs for cash (likely to fund mass redemptions).

One offering shown to us was City of Chicago general obligations (GOs) with an intermediate maturity length, an A+ rating, and a yield of nearly 6%. Now this isn’t quite the 7% my dad was able to lock down in the 1970s, but given that the CPI increased by more than 8% in 1975, his real return was actually negative. With the CPI around 1% today, the net of inflation return is extremely high on a historical basis even at 5%, much less 6%.

In the case of the Chicago bonds, however, we passed. The Windy City, besides domiciling the team that unceremoniously ended the Seahawks improbable playoff run, has a staggering $12 billion unfunded pension obligation. To put that in perspective, the state of Washington’s retirement fund shortfall is $7 billion, or at least it was, and this leads me to a key point of why we want to be buyers into this selling frenzy.

The unlikely budget hawks. An oft-repeated theme in numerous EVAs is that the unavoidable return to fiscal integrity at all levels of government will in many, if not most, cases be driven by Democrats. As others have noted, and I have copied, it’s the Nixon-going-to-China concept.

In the state of Washington, for example, Democratic governor Christine Gregoire recently proposed halting automatic wage increases, which would cut the state’s unfunded retirement plan status in half. If approved, as expected, the shortfall would be $3.5 billion, still a large number but one that is easily manageable by the state of Washington.

Illinois appears to be taking a different route through a 60% increase in its state income tax. While this may re-turn the state to solvency, tax hikes of that magnitude are dangerous, as New Jersey, New York, and California can attest. Additionally, though, Illinois is also taking the pruning shears to its bloated budget.

In the not-so-Golden State, newly re-elected Governor Jerry Brown is putting through a series of massive spending cuts while extending the “temporary” tax increases that were set to expire. Yet, it’s highly probable he will also have to go after his longtime allies in the public employee union world, to whom he injudiciously gave collective bargaining status in the 1970s (something Franklin Roosevelt refused to do in the 1930s).

As long-time Democrat and former San Francisco Mayor Willie Brown pointed out in an editorial last year, 80% of every state revenue dollar collected in California now goes toward public employee compensation and benefits. Thus, Governor-elect Brown has no choice but to do a “Left Coast” imitation of New Jersey Governor Chris Christie (a Republican who has taken on the union powers that have crippled the Garden State with a staggering $240 billion unfunded pension and retiree health care deficit).

In New York, Democratic Governor Andrew Cuomo is also promising major expenditure reductions, admitting that continuing to squeeze state taxpayers is no longer feasible (New York state property taxes rose by a confiscatory 73% from 1998 through 2008).

My point is that the states are now vigorously responding to their financial difficulties leading me to agree with Meredith Whitney and Bill Gross that none of them will default. Few investors seem to realize that in California bond holders get paid right after teachers and in all other states debt service comes off the top. With munis now yielding 110% as much as taxable Treasuries, versus a long-term average of 82%, there’s no doubt an extraordinary clearance sale is underway.

The trick is trying to judge how high the yields will go before they finally hit their apex. It could be that we are very close, which is why it makes sense to be a buyer. But it would be imprudent to go “all-in” when there is as much negative momentum driving the market as there is today.

Therefore, we’re dusting off our playbook from 2008 and 2009 when we systematically bought into the meltdown that hit all non-government bond markets (including munis). We definitely suffered for awhile but buying into that panic turned out enormously lucrative for our clients.

At this point, despite the recent free fall, municipals bonds haven’t been driven down as brutally as corporates were two years ago and we don’t expect they will be. Consequently, they won’t produce anything close to the 100%-type returns seen by so many corporate bonds and preferred stocks since the trough of the crisis. But they can still be very lucrative investments for those willing to dollar cost average into the storm. As usual, that includes us.

IMPORTANT DISCLOSURES

This report is for informational purposes only and does not constitute a solicitation or an offer to buy or sell any securities mentioned herein. This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. All of the recommendations and assumptions included in this presentation are based upon current market conditions as of the date of this presentation and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. Information contained in this report has been obtained from sources believed to be reliable, Evergreen Capital Management LLC makes no representation as to its accuracy or completeness, except with respect to the Disclosure Section of the report. Any opinions expressed herein reflect our judgment as of the date of the materials and are subject to change without notice. The securities discussed in this report may not be suitable for all investors and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. Investors must make their own investment decisions based on their financial situations and investment objectives.