“The most reliable way to anticipate the future is by understanding the past.”

-JOHN NAISBITT, Megatrends Author

Special message: First, Happy New Year to all! Based on our clients’ investment results for 2010, it was certainly a happy old year. We’d be thrilled to see anything approaching those returns in 2011.

Second, because this is our annual forecast issue, which necessarily runs a bit longer than normal, I’ve decided to skip our usual Points to Ponder section this week.

EVAluating the Environment

Forecast for show, manage for dough. Steven Leuthold is one of those rare newsletter writers who, like yours truly, actually manages money at his day job. For nearly 50 years—a duration that makes me feel like a newbie—he has produced outstanding investment results in addition to penning (or, I guess, keystroking) a steady stream of witty and generally accurate market outlooks.

In another parallel with your humble EVA author (recently made more humble, as you will soon

read), Steve also publishes his annual forecasts. And in his recent installment on this score, he

articulated a point that all of us who engage in this somewhat foolhardy pursuit should acknowledge: What really counts is our client returns. In other words, the forecasts provide entertainment value while returns are where the radials meet the road.

If you think this sounds like a bit of a whitewash for a less than stellar forecasting year, you’re not

too far off the mark. To cut to the credits, my 2010 hit rate was 65%. For those of you with exceptional memories, you might recall that in 2009 my on-target number was 90%―in other words, quite a comedown (or, as some less charitably inclined might say, comeuppance).

Yet, in a way, this actualized my ultimate prediction for last year―that, for me, 2010 was “likely to

be rich in embarrassment and generous helpings of humble pie.” As I also noted at the time, when

you play the guru-game you better be satisfied with a 60% to 70% success rate. Otherwise, you

will eventually need to be fitted with one of those sports coats that button in the back.

Therefore, when you consider that I was due for some serious payback, coming in around the average wasn’t too shabby even though it felt like little better than an exercise in dart throwing.

Now, without further rationalization, let’s see what I hit and what I missed as well as what my team and I see coming at us in 2011.

1. The economy. This one I pretty well nailed: a strong start followed by a deceleration as the year progressed. My expectation that fears of a double dip would flare up but be proven wrong was essentially how it played out.

2. Stocks. This is where I need to explain my self-scoring system. Often, as in this case, I get part of the prediction right and part wrong. Accordingly, I give myself 1/2 of a point. Thus, I saw the stock market, like the economy, quick out of the blocks and then experiencing the seasonal weakness often seen in the spring and summer months (particularly in the second year of a presidential term). Then I anticipated a year-end rally. So far, so good...

However, I went on to say that stocks would finish roughly flat, possibly slightly on the upside. Through October this looked spot on, bu the power of the year-ending rally pushed the S&P 500 up 15% including dividends, hence, my half-right outcome. This is one on which I'm happy I didn't earn a full score.

3. Bonds. Another kiss-your-sister result: Unlike most pundits, who were very bearish on US government bonds, I thought the 10-year Treasury was a decent value at 4%. As it turned out, the value was a bit more decent than I thought. My projection was for Treasuries to produce flat to slightly positive returns when it fact the ten year T-note generated a husky 8.%.

On the accurate side, I did see corporate bonds and preferred stocks doing better with returns in the 5% to 10% range. In reality, the corporate index produced a 9.4% total return while preferred stocks gained 13.7% including their always generous dividends.

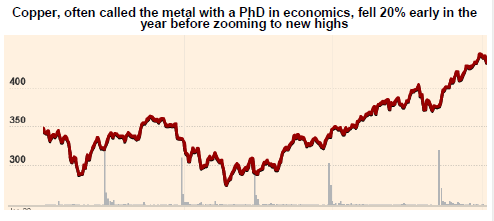

4. Risky investments before zooming to record highs. No gray area here—I totally blew it at least on a full year basis which is how this game is scored, notwithstanding real-world actions we took along the way. After an initial shellacking, high-risk asset classes—such as commodities, junk bonds, smaller stocks, and emerging stock markets—all had banner years.

Fortunately for our clients, we did use the spring-time downdraft in almost all risk assets to increase our exposure to junk bonds (particularly of the higher quality variety) as well as some commodity-related stocks, especially in the energy space. However, we "coulda, shoulda" been more aggressive buyers during the May "Flash Crash" and the summer double-dip scare.

5. The credit crunch. An outright hit on this one: My view was that its tentacles would stretch into 2010 and they did, particularly related to a few countries on the other side of the Atlantic. The best part of my call on this theme was that there was "an untenable situation in Europe where the PIGS (Portugal, Italy, Greece, and Spain) are caught between an overvalued euro and exploding debt levels."

Moreover, I warned about China noting officials were increasingly alarmed about a potential real estate bubble. In fact, they tightened money in a number of ways causing the Chinese market to be a stark underperformed.

6. The Fed. This was almost a good call. Unlike most commentators, I felt the Fed would be very reluctant to raise rates and might not do so at all for the entire year. If I'd left it at that, I would have aced this one.

Unfortunately for my track record, I went on to say that Mr. Bernanke was likely to sell his vast holdings of government debt, bought with printed money, before he would start jacking up the cost of money. This may still be true, but the fact is that I totally underestimated the Fed's angst over economic weakness, which caused it to do even more quantitative easing (the now infamous QEII). Thus, another partial hit.

7. Inflation. At the time, as is the case now, there was widespread hand-wringing over an impeding inflation eruption which I dismissed as "paranoia." Further, I noted justifiable inflation fears were more likely to occur on the other side of the Pacific. Both subdued US cost pressures and rising prices in Asia turned out to be the case. Therefore, this was one of my better calls.

8. Overseas markets. Once again, close to being on the money but, alas, no Cohiba. My view was that the emerging inflation issue in China and measures to rein in its property market would lead to underperformance versus the US. In the case of China, this was most definitely true. I doubt most Americans realize the Chinese stock market fell 14% in 2010. Additionally, the most venerable of all the international indexes, the Morgan Stanley EAFE (Europe, Asia, Far East) was up just 7.7%, held back, as I speculated, by weakness in the eurozone.

Remarkably, the vaunted BRIC (Brazil, Russia, India, and China) markets returned a mere 6.5% on an equally weighted basis. In reality, however, I believe most investors bet more heavily on the darlings going into 2010, China and Brazil. The latter rose a barely perceptible 1%; therefore, those two booming economies managed to produce a combined return of minus 6.5%. In reality, it was the more obscure emerging markets that delivered last year, driving the index up nearly 19%.

Therefore, one could make the case that I pretty much had this one down, but given that the emerging markets in aggregate were up more than the US market, despite the drag from the BRICs, I’m putting it down as a partial.

9. The dollar. Another almost—I was mostly bullish on the dollar though I felt it would weaken versus the Chinese yuan. In fact, the dollar index eked out a 1.5% gain and it did lose measured ground against the yuan. Also, my expectation that the dollar would rise against the euro played out (reversing my one miss from 2009), but I also saw it increasing versus the yen when in reality it fell. As Bette Davis once said about old age, this forecasting game ain’t for wimps.

10. Politics. This was my most controversial forecast and due to that I’m putting it down (at least in my own mind, as if anyone cares) as my best call. First, I projected a major shift to the GOP in Congress. Further, I wrote: “…the pendulum swung too far to the left for most voters…It is likely to move back toward the center, as is our president.”

Maybe I should consider writing a political newsletter…

Now on to what 2011 might have in store.

First of all, I’m going to invoke predictor’s privilege by switching out some of my usual themes and replacing them with a few others that I believe are more meaningful. The new ones are also topics I feel more strongly about (meaning, I’ve got a better chance of being right, something to which I’m kind of partial).

1. Stocks. Despite the notorious difficulty of divining the stock market, I know this is the one almost everyone cares about the most. Therefore, in a nod to the entertainment nature of this exercise, here I go again: Stocks will replay their volatile act from last year but I suspect the rhythm will be different.

In my view, the sequence will be down, up, down, and then back up, ending slightly on the positive side. However, I do think we could get some surprisingly good news on the budget front (more to follow in that section) that might produce another double-digit year. My range for stock returns: +5% to +10%.

The biggest threat to an up year is the current euphoric sentiment and the unanimity with which leading strategists see stocks rising in 2011.

But I believe an early-year correction triggered by more bad news out of Europe and rising distress with a few important municipal credits will shake up the complacency, trigger a sharp sell-off, and thereby set the stage for another up-leg. We shall see…

2. Bonds. How soon they forget! After having delivered boffo returns over the last decade, investors have turned a cold shoulder toward bonds, especially of the municipal persuasion. Treasuries have also been the victim of investor wrath of late, enduring one of their worst quarters in decades.

As astute EVA readers know, my attitude toward bonds and other income investments cooled appreciably as the year progressed and prices levitated up to levels that seemed frothy. That caution turned out to be well placed, but a lot of damage was done in a hurry. In 2011, we see the best gains coming from the battered muni market, followed by mid-single-digit returns on corporate debt and around break-even to a slightly negative total return on the 10 year T-note. Expect plenty of volatility from these normally tranquil investments, however.

3. The economy. This theme was moved down from the top of the list partially to reflect its altered status versus the stock market. In the past, I’ve argued that the economy drives stocks, but lately that dynamic has been changing. How wealthy people feel increasingly impacts consumer spending given that richer folks represent a disproportionate amount of overall household expenditures. With stocks having recovered and likely to stay in a jagged upward trend, the surprisingly strong holiday spending we just saw (topping even the most optimistic expectations) might portend more of the same for next year.

Moreover, the biggest positive I see bubbling up throughout 2011 is a steady increase in confidence. In my opinion, businesses will also get caught up in this better karma, leading them to at long last go on a hiring binge, further uplifting consumer spirits and, therefore, causing yet stronger activity and more job growth. Net/net, I’m looking for a scenario where rising optimism about the future catalyzes a positive feedback loop, wrongfooting those expecting the new normal of a perennially growth-challenged US economy.

4. Junk bonds and risky investments. In the second half of last year, I attempted to draw a distinction between high-grade junk (BB-rated) and truly junky junk. It continues to be my view that the better junk (forgive the oxymoron) will produce decent returns while at some point during 2011 the weakest slices are likely to get seriously lacerated.

As far as other aggressive asset classes like small stocks and commodities, I believe they will be relative underperformers. In English, this means that I feel the odds favor them lagging blue chip stocks though they may show positive returns for the year overall.

At some point, however, I believe a major day of reckoning is coming for these overly popular and pricy areas. Dislocations in China due to various excesses, notably in real estate, could cause things like copper to come a cropper. It just might not happen in 2011 given a generally improving economic backdrop. But even over the next year, expect to see a roller coaster ride worthy of Magic Mountain.

5. The Fed. Unless Ben Bernanke was trying to drive longer term rates up, it’s hard not to consider his unprecedented accumulation of government bonds (using printed money) a backfire. My view is that he will need to halt or reverse QEII at some point during the year as it becomes clear that job growth is resuming, confidence is returning, and the all-important velocity of money accelerates.

However, it’s improbable the Fed will actually raise rates, though I think that’s somewhat of a possibility late in the year.

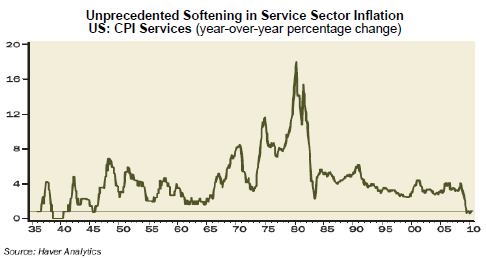

6. Inflation. Basically, fears of its rise are likely to be greatly exaggerated. This isn’t to say that there won’t be some bounce-back off of levels that are dangerously close to deflation. But this is an area where I depart from the most strident Fed-bashers—I don’t believe Bernanke and Co. will fall asleep at this particular switch (after all, they got plenty of snooze time in when the housing bubble was inflating, then imploding).

While their bag of tricks is getting pretty lean when it comes to fighting deflation, they’ve got ample weapons to stop any serious inflationary forces dead in their tracks. In fact, the Fed is likely to tolerate some upward CPI pressure to put to final rest any concerns about a deflationary spiral.

However, by selling a portion of their $2 trillion government bond and mortgage hoard, they can nip any budding inflation well before they even need to think about raising the fed funds rate. The trick will be to not torpedo the economy in the process. That part won’t be easy but I think measured dispositions will actually be an overall confidence booster.

7. Overseas markets. Put me down as mixed in this regard. My belief is that Europe will face a moment of truth in the near future and be forced to solve some of the core problems that it has been sweeping under the antique rugs in Brussels ever since the European Union was formed. Thus, a serious sell-off impacting global markets is a distinct possibility.

However, I do believe Europeans will finally figure it out, particularly the acute need for recapitalizing their banking system. Consequently, any panic resulting from events like Ireland voting in an anti-EU party, or a taxpayer revolt in Germany, should be a superb buying opportunity.

As for everybody’s favorite foreign investment, emerging markets, I believe we’ll see pretty much a replay of 2010—some up a lot, some hit hard, many in the middle, but overall you should make as much through blue chip US stocks with a lot less heartburn.

8. Currencies. This is an area where I think there is good money to be made and we have been positioning accordingly for our clients via securities that appreciate should the yen and euro decline. Further weakness in the euro is highly probable as it’s an absolutely essential element in preventing the weaker countries from devolving into chaos.

Long-time readers may be aware that my worst calls from the prior year often are the best going forward. In my opinion, that will be the case with the yen, especially now that yields have moved up sharply on US bonds, rendering Japanese debt securities, with their miniscule returns, much less appealing. Should the Fed do an about face on QEII, as I think likely, the odds are high the yen will very quickly give up its 2010 gains and then some.

9. Unemployment. At long last, hiring! There are already signs a major turn is at hand but a variety of factors has inhibited the normal employment cycle. This week, however, the closely followed ADP payroll survey revealed almost 300,000 new jobs, the best in its ten year history. Also indicating a major turn, first-time unemployment applications have fallen below the critical 400,000 level.

Moreover, corporate profits have opened up their biggest spread versus employment in 30 years, strongly suggesting that a hiring binge lies ahead (though this will be partially offset by widespread municipal layoffs).

The Obama administration has definitely dusted off the old Clinton playbook from the 1990s. Its much more conciliatory attitude toward the business community is already manifest and that is bound to make companies feel much better about adding workers. Additional olive branches such as providing firms with reduced taxation on repatriating overseas cash or, most importantly, a major Tax Code revision lowering the corporate tax rate, as proposed by the president’s budget commission, could really catalyze hiring.

Oh, yes, the budget―everyone’s worst nightmare. But what if even that horror begins to fade away in the light of a new dawn?

10. The budget deficit. States do it, cities do it, even European elites do it, let’s fall in love—with spending cuts, that is. Some might savor the irony in seeing those traditionally left of center, such as New York’s Mario Cuomo and California’s new/old governor, Jerry Brown, being forced to radically reduce spending in their states.

Yet, as I’ve often noted, there is extensive precedence for this. It’s frequently the more liberal party that takes the ax to sacred cow programs such as public employees being able to retire at 50 at nearly 100% of their prior compensation.

At the federal level, the president’s upcoming budget proposal might be surprising in its fiscal toughness, possibly embracing key elements of the Simpson-Bowles plan that realistically can bend the otherwise terrifying budgetary cost curve (as seen in the chart below). A convincing bipartisan effort to rekindle the fiscal magic of the 1990s would definitely take a lot of folks by surprise, giving the stock market rally further impetus.

If so, 2011 might not be as happy as 2010, but it should still be another healing year as the terrifying trauma of 2008 fades further into the rear view mirror.

IMPORTANT DISCLOSURES

This report is for informational purposes only and does not constitute a solicitation or an offer to buy or sell any securities mentioned herein. This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. All of the recommendations and assumptions included in this presentation are based upon current market conditions as of the date of this presentation and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. Information contained in this report has been obtained from sources believed to be reliable, Evergreen Capital Management LLC makes no representation as to its accuracy or completeness, except with respect to the Disclosure Section of the report. Any opinions expressed herein reflect our judgment as of the date of the materials and are subject to change without notice. The securities discussed in this report may not be suitable for all investors and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. Investors must make their own investment decisions based on their financial situations and investment objectives.