This week’s guest EVA comes from one of our favorite contributing authors, Gerard Minack, and his highly regarded publication: Down Under Daily. Whenever someone we hold in high esteem comments on an area we like too, we are eager to share it with our readers (yes, that could be called confirmation bias!). In this piece, he homes in on how Japan’s equity market continues to experience significant growth after range trading for the last six years. For Evergreen clients invested in our strategies that have an international element, we have been starting to position portfolios toward markets like Japan; accordingly we hope you find this missive especially interesting.

As many EVA readers know, we are big believers in multi-year breakouts – especially when they happen to be of the 30-year variety. As you’ll see in the chart below, Japan has achieved that rare feat with very little fanfare (a positive from a contrarian standpoint).

Many opine that the US stock market is cheap due to low interest rates, and if you’re in that camp, you’re going to love Japan: current interest rates there are hovering around zero. For years, the allure of this favorable investment environment was dismissed by US investors because of Japan’s poor corporate profitability. But now, as Gerard highlights, that’s no longer the case (see his second-to-last chart). Further magnifying the opportunity in the Land of the Rising Sun (and now rising stock market), its equity market trades at just 15 times estimated 2022 earnings, compared to 20 times in the US.

We think there’s a good chance that Japan will also see capital flowing in from investors looking for Asian exposure but seeking to avoid countries under siege from their own government (see: China). We tend to believe that several overseas markets have the potential to make up considerable ground on the US after it’s dominated global equity returns over the last dozen years. Such a change could be on the horizon. That being said, the US market has many pockets of value that we’ll continue to seek out for our more domestic-focused portfolios.

Japanese equities, like Japan’s economy, lagged in the initial recovery from the Covid pandemic. Both should do better, at least in a relative sense, in 2022. The outlook would brighten further if the new Prime Minister, Fumio Kishida, delivers on plans for fiscal stimulus and policies to reduce inequality.

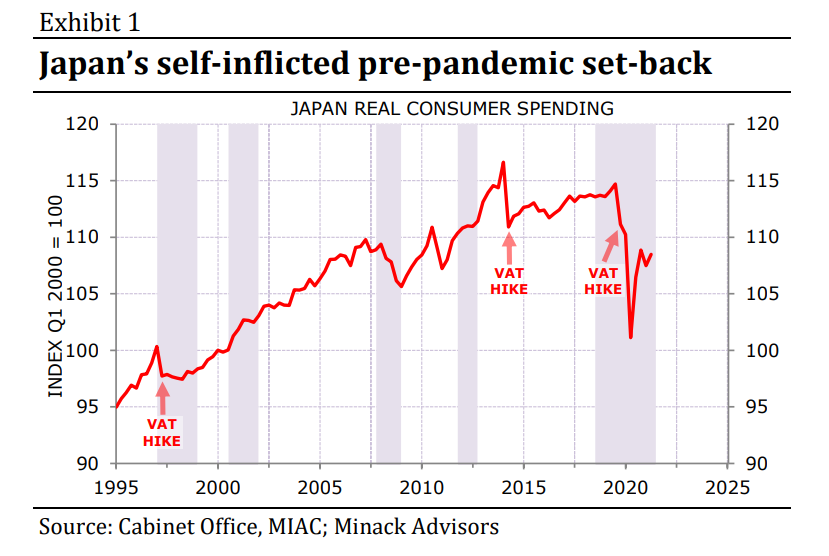

Japan has struggled through the past two years. Problems pre-dated the pandemic: growth weakened after the VAT rate increased from 8% to 10% in October 2019. For the third time fiscal tightening had nobbled an expansion (Exhibit 1).

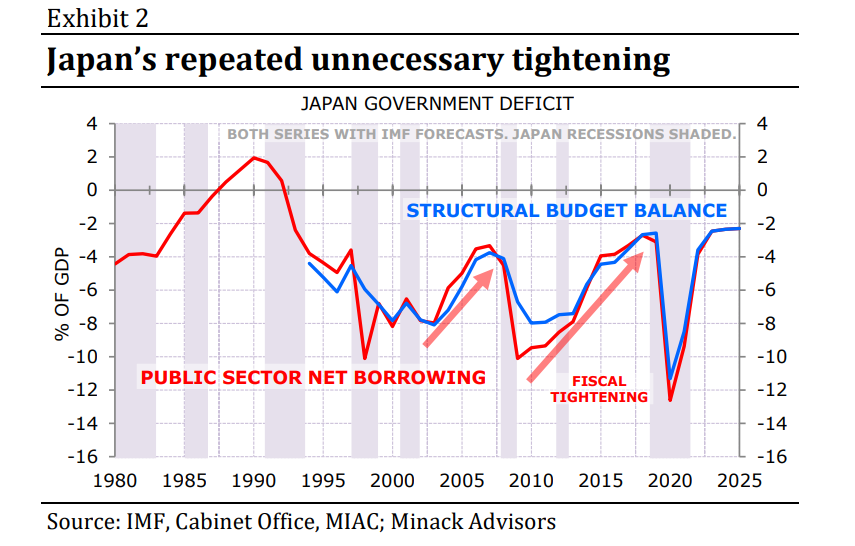

As an aside, some see Japan as proof that fiscal stimulus doesn’t work. I see it as proof that fiscal does work: when fiscal policy is tightened – and reducing deficits is tightening – growth slows. Japan specialises in ill-timed austerity (Exhibit 2).

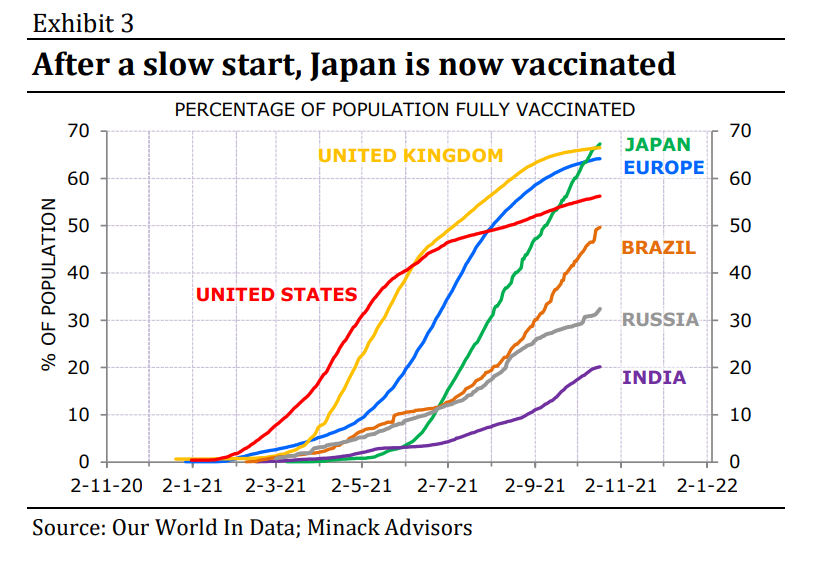

Consequently, the pandemic hit an economy already in recession. Japan, like most other developed economies, responded with aggressive fiscal stimulus. However, Japan’s recovery lagged other developed economies’ in part because of the initial slow vaccine rollout. One factor pointing to better prospects ahead is that Japan’s vaccine rollout now exceeds other G7 countries’ (Exhibit 3).

Partly as a result of these problems, Japan’s equity market – one of the most cyclical in the world – lagged through last year’s initial pandemic recovery.

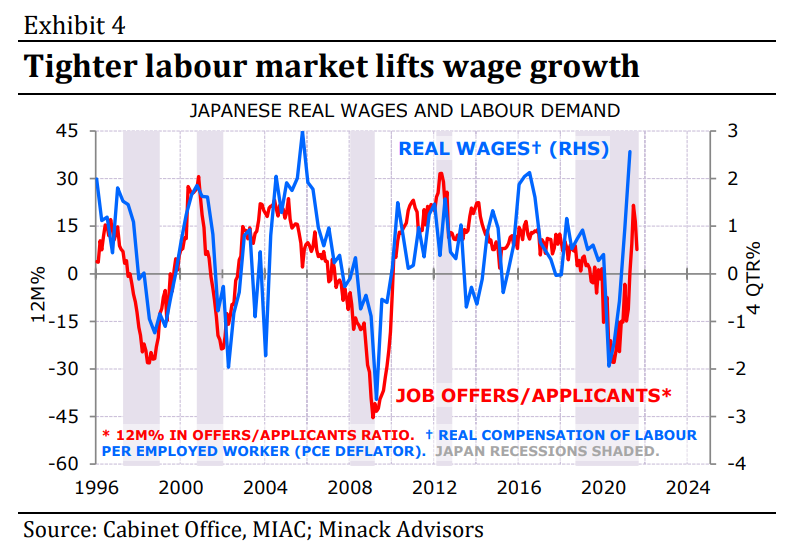

I expect Japan will be better placed in 2022 to take advantage of what is likely to be a year of above-trend growth in the developed economies. The vaccine catch-up is one positive factor. Another is that Japan is following the pattern in other developed economies of tightening labour markets and faster wage growth (Exhibit 4). Japan would also benefit from unblocking supply chains and increased auto production. Finally, it would be helpful if the LDP administration – presuming it gets re-elected on 31 October – delivers on a promise to increase stimulus.

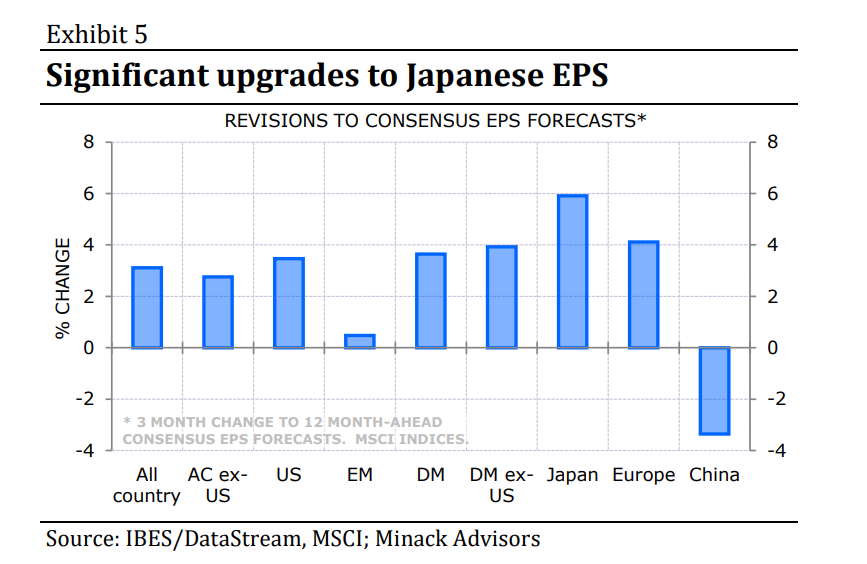

Japan’s equity market is now seeing faster EPS upgrades than other major markets (Exhibit 5).

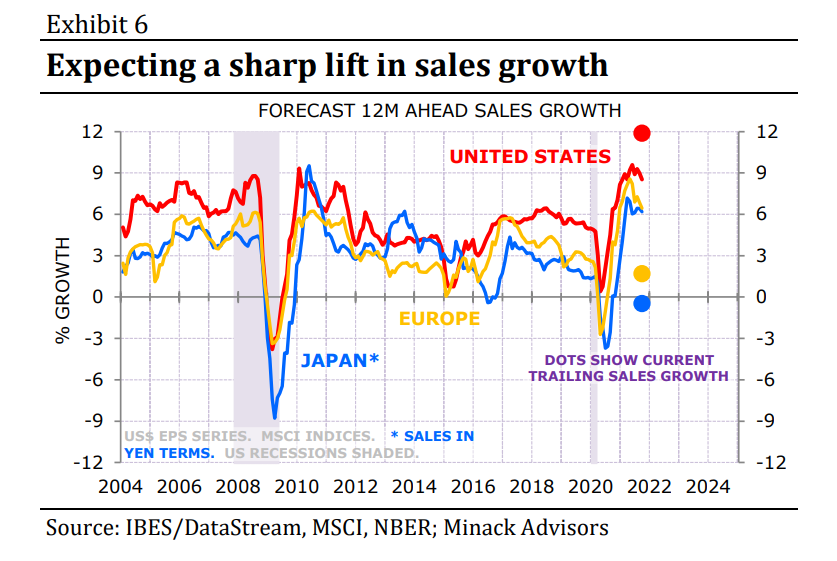

Sales growth, which has been flat lining, is expected to accelerate in the next 12 months. To be fair, consensus also expects fast sales growth elsewhere, although for US companies forecasts imply a deceleration from current growth (Exhibit 6).

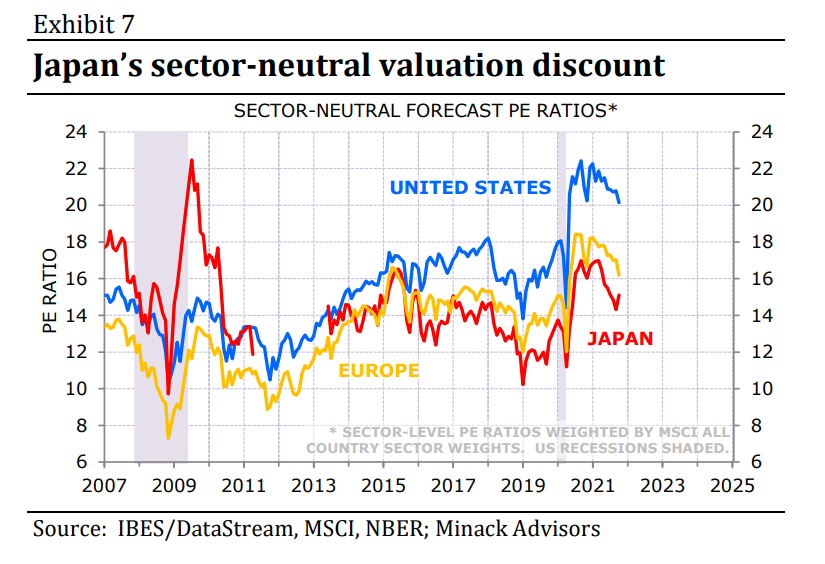

Japanese equities also are relatively cheap. This is not just a reflection of the market’s composition: Japan trades at a discount to Europe and the US on a sector-neutral basis (Exhibit 7).

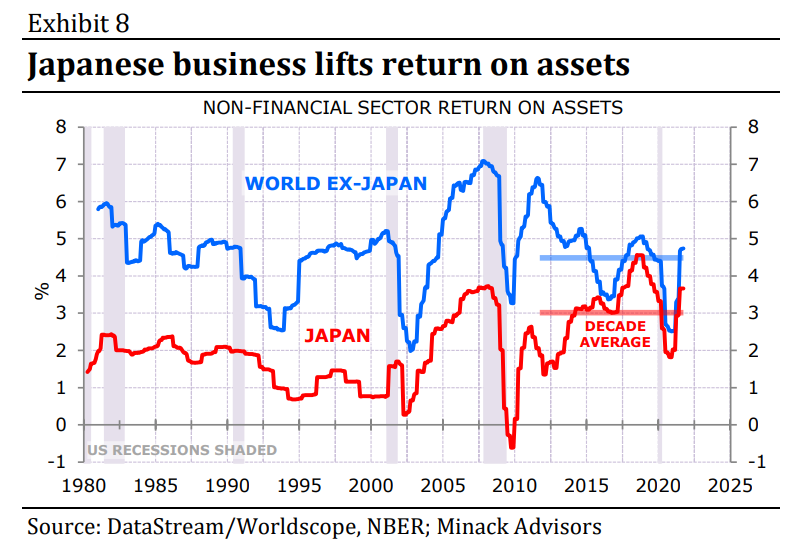

This is a cyclical story. But I continue to believe that there is also a structural bull story for Japan. Corporate Japan was terrible at capital allocation through the bubble period. However, return on assets has improved steadily over the past two decades (Exhibit 8). Free cash flow is now high, and the non-financial sector has dramatically reduced leverage since the early 1990s.

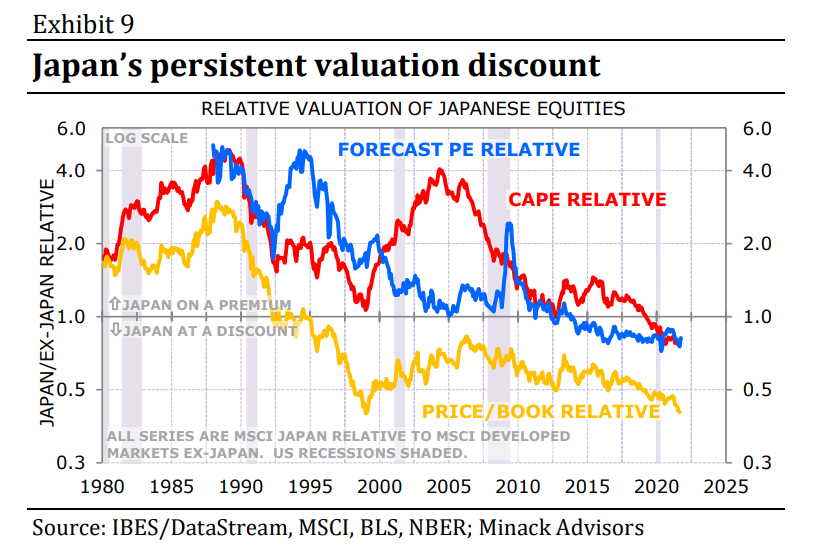

These structural trends have gone unrewarded. The Japanese market has steadily de-rated relative to other developed markets through the low growth, low rate post-GFC environment (Exhibit 9). The prospect of above-trend economic growth, and rising long-end rates, may be the catalyst for a period of sustained out-performance.

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.