"That is going to be a huge challenge, to which I don’t have a great answer."

- Janet Yellen, referring this week to risks from the Shadow Banking System

Fireworks in our future? As perceptive EVA readers realize, today we should be running our Evergreen Exchange edition co-written by Jeff, Tyler, and me. However, as this is a holiday-shortened week, with all three of the aforementioned authors on vacation, we need to alter our sequence a bit, yours truly gets the privilege of producing this issue while allegedly on "vacay."

Actually, it isn’t as onerous as it sounds, due to the fact that last Friday, at about 4 a.m., it hit me that I needed to bring out the editing scissors and trim last week’s EVA to avoid overwhelming readers even more than I did. As a result, I’m going to run some text that wound up on the cutting room floor a week ago, as well as some new, but related, material.

A reality (some might say "psychosis," in my case) of summer road vacations in our family is that my supportive wife drives to our destinations while I read. This will afford me about 32 total hours of mobile research reading time on our current two-week trip, not counting considerable time spent perusing newspapers and company reports by the pool (I know, tough duty!). The last few days have been particularly intensive in that regard, providing me with further insights into a couple of the main themes from last week.

One of them is the uber-vital topic, in my opinion, of the Shadow Banking System (SBS). In the May 23rd EVA, Tyler wrote about "The Homeless Man" from an investment conference several of us attended a few years ago. Many of you may recall this was a somewhat facetious (but only somewhat) vignette concerning Paul McCulley who, at the time, did bear a striking resemblance to the title character from Down and Out in Beverly Hills. (Click here to read the May 23rd EVA.)

As Tyler correctly speculated at the time, Mr. McCulley’s dramatic make-over—from scruffy vagrant to neatly-groomed intellectual—at this year’s version of that conference was a prelude to his return to the financial world’s limelight. Soon thereafter, he was made Pimco’s Chief Economist, where he will report directly to his long-time pal Bill Gross, the illustrious and controversial "Bond King" (who seems to like to have his picture taken with his tie undone).

Ironically, it was the sound-bite fluent Mr. McCulley who first coined the term Shadow Banking System. Moreover, he accurately warned prior to the financial crisis that the SBS was likely to magnify—again, presciently—the disaster he saw coming from the housing bubble’s collapse.

Returning to top dog status at Pimco has made the always-quotable Mr. McCulley a media darling again. Accordingly, on June 17th, the Financial Times published an Op-Ed he authored titled, "Make shadow banks safe and private money sound." His opening paragraph got right to the heart of the matter: "The rise of the shadow bank—a kind of intermediary that lies outside the range of much banking regulation—carries a subtler corollary. It has created a kind of money that is likewise beyond reach of central bankers’ traditional instruments of oversight and control." He begins his final paragraph with this sentence: "The crisis of the past decade was a reminder of the instability inherent in private money [the SBS]."

If you read both the article’s title and the above excerpts closely, you realize that Mr. McCulley is saying that, as the SBS stands today, it is not safe and it is also largely outside the Fed’s regulatory powers (my, how our central bank’s mission statement has expanded!). Mr. McCulley proposes several ways in which the Fed could make the SBS sounder but the key word is "proposes." In other words, his suggestions are a long way from implementation despite his new and influential position.

Speaking of proposals, you may have seen a flurry of articles lately about the Fed’s alleged consideration of exit fees on bond funds, which are definitely a part of the SBS. This speaks to their fears that a run on bond funds is possible, perhaps even probable.

It was my contention in last week’s EVA that ETFs have, in many cases, become an extension of the SBS. To further buttress this claim, beyond the example of the Bank Loan ETF (BKLN) I gave in that EVA, there is another ETF, which I believe has already given us an advance look at what could happen on a much broader scale.

All that glitters isn’t gold—especially GLD. Some of you may know the name Fred Hickey, long-time author of The High-Tech Strategist. Additionally, he is a member of the prestigious Barron’s "Roundtable." Last Saturday, somewhere on the road between Sun Valley and Reno, I read his June monthly, issue #317 (yes, he’s been at the newsletter game for over 25 years), "Running Out of Time."

It was so good I’m going to seek his permission to run it as a guest EVA later this month. In the meantime, though, I thought I’d share some of his primary points, especially a few that overlap with the "ETFization of the US financial system" theory that I discussed a week ago. In that issue, we ran what I believe is a profound quote by former Fed governor Jeremy Stein: "The essence of shadow banking is to give a liquid claim on illiquid assets."

To see how this dynamic can play out most tumultuously, Fred highlights the experience of what was, three years ago, one of the most popular ETFs on the planet. In 2011, as the Fed was admist QE2 and stocks worldwide were struggling, the gold ETF (ticker symbol GLD) was soaring in both price and popularity. Precious metals in general seemed to be the ideal antidote to profligate Fed policies. For a brief period during the spring of that year, GLD’s close cousin, the silver ETF (SLV), actually traded with heavier volume than did the S&P 500 ETF, SPY. (Don’t you just love all these acronyms?)

In fact, the speculative forces engulfing the SLV became so intense that in May of 2011 I was preparing an EVA calling the silver blow-off the latest bubble. Unfortunately for my "I told you so" record, it explosively popped before I could send that edition out (though I did issue a number of warnings about the commodity mania around that time). After reaching the upper 40s during that frenzy, SLV has plunged by 60% and has been bouncing around $20 for the last 15 months or so.

Gold initially held up much better, pulling back in controlled fashion from a peak of just over $1900 an ounce to around $1600. However, in April of last year, a truly extraordinary event occurred. Massive selling of gold futures contracts occurred while the US markets were closed. This triggered what Fred rightly calls a "flash crash" in bullion, with the price cliff-diving almost 14% in two days. Predictably, this caused retail investors, who had previously piled into GLD, to liquidate en masse.

Thus, what started out as a mysterious "bear raid" on gold derivatives (futures contracts) turned into frantic liquidation of the gold ETF. This in turn forced the sponsors of the ETF to liquidate the underlying bullion. And, as things so often go, this selling paroxysm fed on itself. Consequently, as Fred points out, there is now 42% less gold in the ETF than there was before its "flash crash."

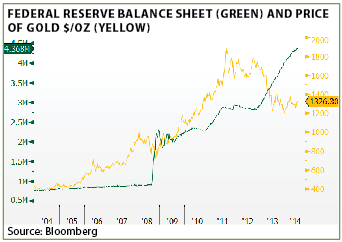

This has created another one of the many "great disconnects" abounding today. As you can see below, the gold price had fairly closely tracked the unprecedented inflation in the Fed’s balance sheet over the years—with an euphoria-driven overshoot in 2010 and 2011—until the spring of last year.

Fred admits, despite his network of "plugged-in ‘Swiss gnomes’ in the gold market," that he can’t ascertain who or what caused bullion to meltdown despite super-supportive fundamentals, including nearly nil short-term interest rates. Conspiracy theories abound, but what we do know is that, as western investors stampeded away, Asian investors enthusiastically stepped in to accumulate thousands of tons of the physical gold that GLD and the other precious metal ETFs were forced to liquidate.

If you’re wondering what all this has to do with bonds and the shadow banking system, I’m going to do my best to make what I think is a highly relevant connection.

The dangers of fairy dust. Gold is not your typical asset that trades "by appointment only," unlike many parts of the bond market. It has been the ultimate unit of exchange for thousands of years and is still coveted by central banks. In fact, even in this era of "fiat" money, a classic sign of a country’s distress is when its version of the Fed runs short of the yellow metal.

Therefore, if an enigmatic midnight raid, greatly facilitated by a rush of retail redemptions, could crush this essential market, what would happen to bond ETFs, involving assets that are much less fungible, should selling go viral? Given the inherent illiquidity of many of the underlying assets, and the illusion of instantaneous liquidity, the only element that can square the circle is price. In other words, prices will need to come down, likely by a lot, to entice buyers to risk their capital when an initial trickle of selling turns into a torrent. Shocking price declines are almost certain to create even more frenzied liquidation.

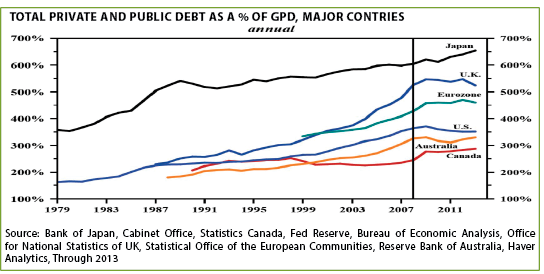

As I’ve said and written before, if it can happen to gold, it can most definitely happen to the riskier niches of the financial markets. But wait, you say—the bond markets are much safer than they were before the Great Recession led to the Great Deleveraging. To which I reply, what deleveraging?

Despite a minor—emphasis on minor—reduction in US debt relative to the total size of our economy (mostly due to mortgage defaults), debt-to-GDP ratios in nearly all major countries are higher than they were pre-crash.

It hasn’t escaped me that many EVA readers feel that I’m being too negative about issues like debt, the shadow banking system, and the extreme overreliance on central bank printing presses to solve the world’s economic problems. Consequently, I would like to close this week’s EVA with a few snippets from a New York Times article that ran a few days ago.

It discusses a report that was issued last Sunday by the Bank for International Settlements (BIS). Several past EVAs have pointed out that the BIS is often referred to as the "central bank of central banks" and also that it was one of the precious few official organizations to anticipate the global financial crisis. Therefore, I would strongly suggest all investors seriously consider what the BIS is saying now.

The author of the aforementioned article, Jack Ewing, summarizes this study as follows: "The overall, somewhat gloomy message from the (BIS) was that the world is drunk on easy money and has already forgotten the lessons of recent years." He then quotes several sections of this report, including: "The signs of financial imbalances are there…Despite the euphoria in financial markets, investment remains weak. Instead of adding to the productive capacity, large firms prefer to buy back shares or engage in mergers and acquisitions."

Mr. Ewing concludes his article with this final direct quote from the BIS: "The temptation to postpone adjustment can prove irresistible, especially when times are good and financial booms sprinkle the fairy dust of illusory riches. The consequence is a growth model that relies too much on debt, both private and public, and which over time sows the seeds of its own demise."

And you thought I was worried! Maybe holding some insurance against the consequences of this grand exercise in central bank fairy dust sprinkling isn’t a bad idea. We continue to think that an important part of that protection is spelled GOLD even though—or, actually, because—so many others have cancelled their policies.

Important Disclosures

This report is for informational purposes only and does not constitute a solicitation or an offer to buy or sell any securities mentioned herein. This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. All of the recommendations and assumptions included in this presentation are based upon current market conditions as of the date of this presentation and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. Information contained in this report has been obtained from sources believed to be reliable, Evergreen Capital Management LLC makes no representation as to its accuracy or completeness, except with respect to the Disclosure Section of the report. Any opinions expressed herein reflect our judgment as of the date of the materials and are subject to change without notice. The securities discussed in this report may not be suitable for all investors and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. Investors must make their own investment decisions based on their financial situations and investment objectives.