"In their efforts to promote growth and jobs, central banks are trading the possibility of immediate economic gains for a growing risk of financial instability later."

- Mohamed El-Erian, former Pimco CEO

POINTS TO PONDER

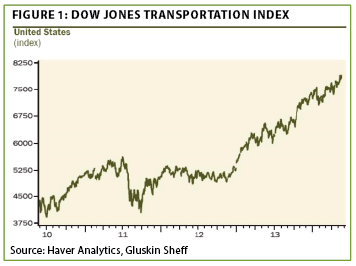

1, Although the US bond market is indicating economic softness, as are most major global debt markets, the relentless rise by the Dow Jones Transportation Index is sending a much different message. (See Figure 1)

2. Unquestionably, US companies, especially of the tech variety, are extremely cash rich, despite the fact that much of it is held overseas for tax considerations. Yet, in recent years, corporate America has been frantically incurring debt, mostly for share buy-backs, dividends, and takeovers. Meanwhile, capital spending, the lifeblood of future growth, remains depressed, even as overall corporate leverage has hit a new post-WWII peak relative to the size of the economy.

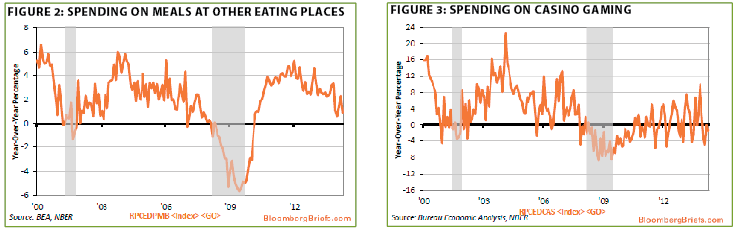

3. Bloomberg Chief Economist Rich Yamarone believes that spending on eating out and gambling are revealing indicators of the economy’s health. Presently, neither is very robust. (See Figures 2 and 3)

4. According to the prestigious economic analytics firm ISI, there is now $700 trillion in global derivatives. The complexity and interlocking nature of these instruments raises legitimate concerns about the financial system’s ability to withstand future shocks, which, despite unusual market tranquility presently, are virtually certain to continue occurring.

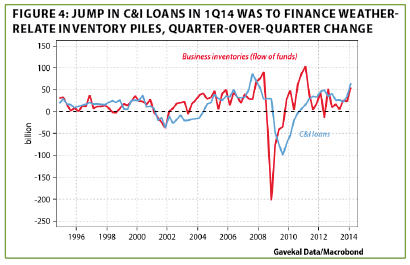

5. Evergreen has been keeping a laser focus on lending activity. This is due to our belief that a definitive up-turn is likely to be an advance indicator of a reversal in money velocity’s long downtrend. As prior EVAs have relayed, commercial and industrial loans (C&I) have rocketed this year. However, GaveKal’s astute economic analyst Will Denyer believes this is due to involuntary inventory accumulation during the unusually harsh winter. (See Figure 4)

6. In another example of America’s "Tale of Two Economies," sales of the 1% most expensive US homes (roughly $1.7 million and up) have risen by 21% during the first four months of this year. Meanwhile, the other 99% have fallen by 7.6%. In a similar vein, luxury goods retailers Tiffany and Louis Vuitton Moet Hennessy (LVMH) reported a 9% jump in first quarter sales, while Walmart experienced a 5% contraction.

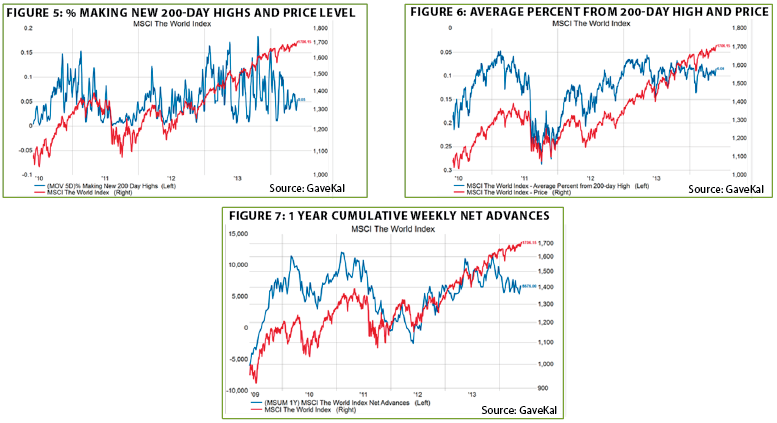

7. Deteriorating breadth isn’t just a US market phenomenon. Globally, the percentage of stocks making new highs, as well as the erosion in the measure of advancing vs. declining issues, are not confirming new closing peaks by the MSCI World Index. (See Figures 5-7)

8. Italy has never been known for its pristine bookkeeping, but it is elevating "creative" accounting to a new level. In a desperate attempt to make its budget deficit as a percentage of GDP appear lower, it will now include estimated transactions in illicit drugs, prostitution, and smuggling as part of national economic activity. Not to be outdone in the "Vice Race," the UK is opting to include these activities as well.

9. China’s glutted real estate market needs more supply like the VA needs more bad press, but there is now 5.7 billion square meters (equivalent to over 61 billion square feet) of urban housing under construction. This is roughly five times the current annual sales rate.

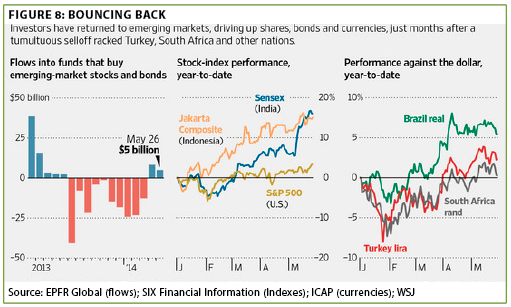

10. Like municipal bonds last year, emerging market stocks and bonds were investment pariahs in the second half of 2013 and into 2014. Funds dedicated to the developing world saw severe out-flows, as did those focused on US tax-exempt debt. And, as so frequently happens when mutual fund investors take flight, emerging market equities and debt have generated some of 2014’s best returns so far. (See Figure 8)

THE EVERGREEN EXCHANGE

By David Hay, Jeff Eulberg, and Tyler Hay

The beauty of bubbles. Considerable digital ink has been expended in these pages on the immense inflation of asset prices in recent years. Understandably, given our reader base and our firm’s focus, most of this attention been centered on the financial markets. But thanks in no small part to a recent trip I took with several Evergreen colleagues, it dawned on us that we should be broadening the message, including highlighting a new service we are offering.

We traveled last week to one of America’s most scenic venues: The Colorado Rockies, about two and a half hours northwest of Denver. Our purpose was to visit a ranch that is in the process of being sold. Its owners graciously invited us out to view it and to discuss reinvestment options.

Suffice to say it isn’t your normal gentleman-rancher spread. It covers roughly 10,000 acres, and it took us four hours to tour the perimeter, even in a Polaris 4-wheeler. Some of the streams we ploughed through looked more like rivers to us. At times, we weren’t sure we were going to make it to the other side without doing the breast stroke! The scenery was spectacular and the views from their mountain top home, at about 10,000 feet looking out at the surrounding Rockies, are impossible to do justice to with words. Therefore, I thought we should just show you a few photos.

Despite their understandable love for this extraordinary property, our clients sense this is the time to sell. They previously witnessed a 30% to 40% evaporation in its value and are shrewd enough to realize that some of the same preconditions that existed prior to the Great Recession are present once again. Prominent among these are the return of lax lending standards and monetary policies that encourage the elevation of asset values to levels that defy economic logic; in other words, the emergence of new bubbles.

This savvy couple realizes that the easy money won’t flow forever, leading them to conclude now is the time to "monetize" their incredible holding. When they see Long Island estates selling for $147 million, shattering previous records, and paintings going for nearly as much (not to mention Balloon Dog from last week’s EVA being sold for 58 million smackers), they wisely perceive the froth to be nearing a head.

Admittedly, not many EVA readers have 10,000-acre ranches in their portfolios, but many of you own expensive homes and valuable businesses. In fact, a member of my own nuclear family, whose home value suffered severe fallout as a result of the financial crisis, is in exactly this situation. The earlier meltdown in what is by far his most valuable asset shattered his retirement dreams. Now, however, its value supposedly exceeds what it was before the helium rushed out of the Seattle housing market back in 2007. Thus, he has another chance to secure his financial future. Who said bubbles are all bad?

For those entrepreneurial EVA readers, now might also be a propitious time to "hit the bid," as we say in our business. Obviously, there are many considerations, and we would never want to give blanket advice in that regard. But if you have been thinking of cashing in (or out), the present time is likely to go down as one of those ideal moments in which to attain top dollar (some Evergreen clients have already done just that, to which we say: well done!).

Evergreen has recently established a family office group led by Mark Nicoletti, a veteran of the multi-billion dollar Getty family investment entity. One of the services we offer, free of charge, is consultation on potential business transitions (sale, partial sale, debt restructure, ownership transitions). Given that we have analyzed countless businesses over the years, mostly public but some private, we have considerable experience when it comes to determining value and evaluating strategies. Additionally, we utilize a network of outside professionals with specialized skills needed to augment our role alongside the client. Business owners often have a very in-depth understanding of their company but find themselves intimidated by the complexities involved in such an

event. Being able to use Evergreen’s investment team as a collaborative partner during a transition of such magnitude can make a daunting task more manageable and likely more profitable.

As with the stock market, prices for small (and not-so-small) businesses can always rise further. However, even the Fed—which did a persuasive imitation of Sergeant Schultz from Hogan’s Heroes ("I know nothing! I see nothing! NOTHING!"), as home prices went hyperbolic a decade ago—is now warning of investor complacency and deteriorating lending standards. As a result, we can’t help but wonder if the little hand has moved very close to midnight for just about everything in this latest bull market run. For those wise enough to sell while the selling is good, or at least good enough, bubbles can be a beautiful thing indeed.

![]()

Market mysticism. Magic: The power of apparently influencing the course of events by using mysterious or supernatural forces. For several years now, I’ve watched earnings disappoint prior years’ estimates, and lower GDP revision after lower GDP revision. Yet, the S&P 500 continues to reach higher highs. Have I been poorly tracking these releases, or is something strange going on in the market?

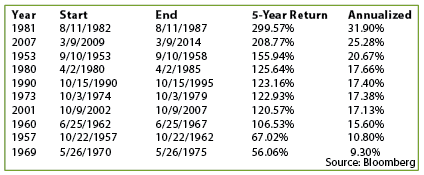

In my quest to determine if some magic is at play, I wanted to see if this truly has been a stronger market recovery than after previous recessions. Therefore, I called on Jeff Dicks, Evergreen’s in-house data guru, and asked him where this bull run ranks compared to other post-recession market rallies. Here is what he found:

Since 1950, this has been the second strongest post-recession bull market. Ominously, the only stronger market return ended in 1987. Now, in order to determine if this is magic or reality, we need to double-check the supporting data.

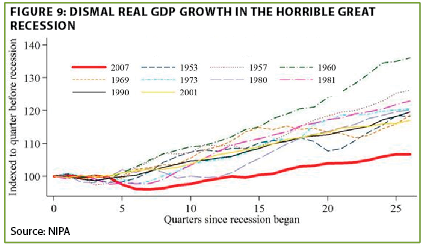

To me, it would make sense that if we had the strongest market recovery, the economy would also be growing at a comparable rate. Below is a chart that compares this GDP recovery to all of the other post-1950 recoveries.

Clearly, the overall US economy did not grow at a pace to justify the strongest market recovery. And, while we do have peak profit margins, is it possible that corporations have decoupled and the private sector has experienced a record expansion?

The highly sophisticated answer is: not so much. As mentioned in previous EVAs, Jeff Kleintop, Chief Market Strategist of LPL Financial, says, "This earnings cycle is the weakest in 55 years with annualized growth of 2.8% from the previous cycle peak in the second quarter of 2007 through the first quarter of 2014."

So, compared to all post-1950 recoveries, this economic and profits expansion has been the least vigorous, and yet the market recovery has been one of the strongest. That sounds like one heck of a magic trick to me.

The magician in this case is obviously the Federal Reserve Board. The Fed has used its massive balance sheet to keep rates low and make stocks truly levitate. They call this trick the "Wealth Effect." And, the best magicians are the ones who can trick you into thinking their illusions are real for the longest period of time.

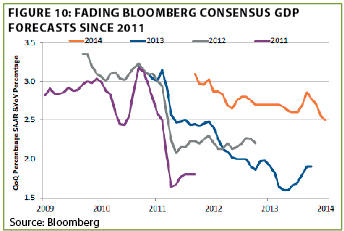

Over the last five years, the spring season has brought more than blossoming flowers. It’s also been the season for Wall Street analysts and economists to prune their prior growth forecasts. This week, the IMF trimmed its 2014 GDP expectations to 2% from a previous prediction of over 3%. Furthermore, Goldman Sachs believes after all revisions are said and done, first quarter GDP may come in around minus 1.9%. Regardless of the negative effects of a harsh winter, that is a pathetic quarter for an economy supposedly on the verge of booming. Below is a chart that shows how this recovery has consistently failed to meet expectations. However, don’t worry—there is always next year!

With so much optimism built into this market, I don’t see a tremendous amount of upside at these levels. However, unlike a magic show in Vegas, if the economy reaches the elusive escape velocity that the "great and powerful" Fed talks about, there’s a chance this trick can turn into reality. On the other hand, If the economy and profits continue to sputter, this market is setting up to disappoint a lot of magic fans. Even worse, many of these onlookers don’t even realize they are witnessing the most elaborate monetary sleight of hand ever seen. Let’s hope the final act doesn’t involve turning a raging bull into a roaring bear!

You’re better than that! In order to stave off the effects of an aging metabolism and a mediocre diet, I routinely play basketball at a local athletic club. One of the regular players there has become a good friend of mine. In the late 1990s, he sold his tech company for a small fortune. Since then, he has dabbled in different types of investments ranging from exotic start-ups to real estate to traditional stocks and bonds. We occasionally discuss the latter. The other day, I teased him and said that he’d make a terrible, micro-managing, second-guessing, control freak, of a client, to which he replied: "You probably pick stocks by throwing darts at a board!" After I insisted that my aim with a dart is quite good, we shifted the conversation to the essence of his comment: Are markets too efficient? Is it impossible to add value through active management of one’s portfolio? We think there are two fundamental problems with the belief that investors cannot do better than the market itself.

The first reason is quite elementary: For markets to be efficient, those who participate in them must be efficient. Efficient market theorist Eugene Fama won a Nobel Prize for his work in this field in the 1960s. Though much of his thinking was taken as gospel for decades, it is no longer held with the same piety. Even arm-chair

market historians have noted that, in the wake of bubbles and subsequent disasters, the notion that investors behave rationally choices seems obviously inaccurate. As most readers are aware, a field known as Behavioral Finance has emerged as the primary adversary of efficient market advocates. In past writings, I have cited many psychological imperfections that are hard-wired into our DNA. This limits the effectiveness of our decision-making with respect to financial matters. While it seems painfully obvious to us that there are holes in the efficient market argument, many still refuse to acknowledge its shortcomings.

A recent study I came across in the Wall Street Journal provides furthers evidence of these deficiencies. At Rutgers University, a neuroscientist immersed a participant’s dominant arm in ice water (39 degrees farenheit). This released a stress hormone called cortisol. Participants were then asked to evaluate a number of gambles with varying odds. The effect of the stress caused two interesting reactions. First, it led the participants to gravitate to less risky, safer bets. Second, brain scans showed that when these bets in fact paid off, the part of the brain that processes rewards showed a more muted reaction. In short, when we are stressed, we become exceedingly cautious, and our brains don’t properly process successful events both seemingly obvious hurdle to rational investing. Countless other studies like this show our predisposition to behaviors that undermine good investing practices, but it’s a hard reality to face as an investor. (Click here to see the study from WSJ.)

Occasionally, I run into people who believe that simply buying an S&P 500 ETF is the best way to invest in the stock market. I’ve tried to challenge this by saying that market participants aren’t efficient actors because we have behavioral biases that limit our ability to act rationally. Therefore, the markets at times move out of equilibrium and thus a more tactical approach is needed. Efficient market advocates would say that even if that’s true, it’s impossible to determine when prices are distorted by basic human emotions such as fear and greed. Consequently, they are convinced it’s best to simply buy an index ETF on the broad market. I concede that if you asked me every day whether the market is going to go up or down I would say, "Flip a coin." Simply put: Most of the time markets are efficient and random; thus, it’s hard to ascertain their relative attractiveness or unattractiveness. That said, I believe there are certain times when it’s blatantly obvious that the market, or a sub-segment of the market, are mispriced. Further, it doesn’t take a degree in applied mathematics and sophisticated computer algorithms to determine these episodes. This leads me to my second reason why I feel it is possible to achieve better than market returns…

In 1999, technology stocks were skyrocketing in value far faster than any other part of the stock market. If you were indexing using the S&P 500 ETF, this meant the technology sector was becoming a larger and larger part of your portfolio. At its peak, technology made up 35% of the S&P 500’s total weight. Combined with telecom, these two sectors, which were the epicenter of the biggest US stock market bubble of all time, made up nearly half of the S&P’s total market value. Putting that in perspective, the average technology weight in the S&P 500 since 1990 has been 14%. Ergo, it was 250% larger than its average weighting during the heat of the dotcom frenzy. Then in 2006-2007, during the real estate bubble, the financial sector would have been roughly a quarter of your portfolio if you were indexing to the market. We all know what happened post-1999 to technology stocks and after 2007 to financial issues: They were obliterated, and therein lies the problem. Indexing means that your portfolio will have the highest allocation to the most overheated parts of the market at exactly the wrong times. Similarly, it also means an index investor is consistently underweight the most out-of-favor market segments.

So, what do you do if indexed ETFs have inherent flaws? We think that "intelligent indexing" is the superior methodology. In essence, you use sub-indexes to build portfolios that represent different areas of the market. Then, when you have extreme upward deviations from historical precedent, you reduce your portfolio’s exposure to that sector, becoming increasingly underweight the farther it rises above its historical average (think reducing tech exposure in the late 1990s). This works the other way, too. You should increase your exposure to segments of the market that have materially shrunk. Historical back tests we’ve performed show that this type of reversion to the mean analysis on styles, like large cap growth and small cap value, is extremely predictive of future performance.

Over the last few years those who’ve simply bought S&P 500 ETF indexes have looked borderline brilliant. This will always be the case in a bull market. Stock picking or asset allocation becomes marginalized as a rising tide lifts almost all boats. I tell people that indexing is like cruise control: It works when the road is straight, traffic is absent, and your speed is constant. But the stock market isn’t always a California freeway with no traffic (I suppose that’s an oxymoron). It can be an icy and winding mountain road with no guardrails. I don’t know about you, but I wouldn’t rely on cruise control for that drive.

Important Disclosures

This report is for informational purposes only and does not constitute a solicitation or an offer to buy or sell any securities mentioned herein. This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. All of the recommendations and assumptions included in this presentation are based upon current market conditions as of the date of this presentation and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. Information contained in this report has been obtained from sources believed to be reliable, Evergreen Capital Management LLC makes no representation as to its accuracy or completeness, except with respect to the Disclosure Section of the report. Any opinions expressed herein reflect our judgment as of the date of the materials and are subject to change without notice. The securities discussed in this report may not be suitable for all investors and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. Investors must make their own investment decisions based on their financial situations and investment objectives.