Below are Evergreen Gavekal's Likes/Dislikes for October 29th, 2021.

OUR CURRENT LIKES AND DISLIKES

Changes highlighted in bold.

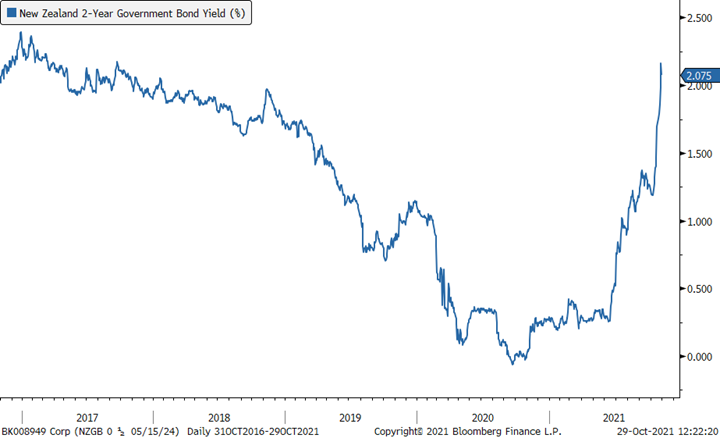

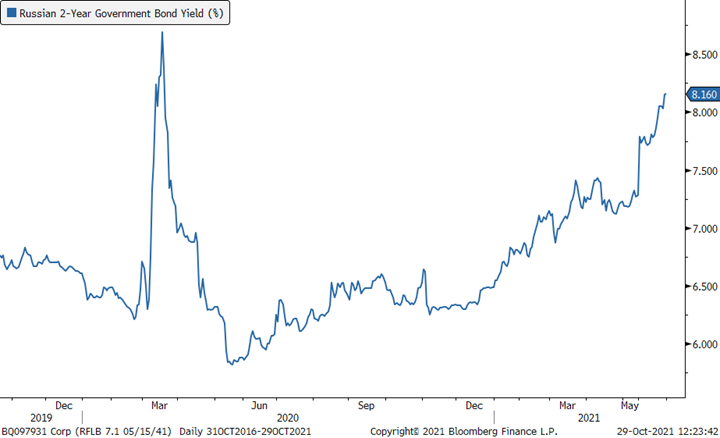

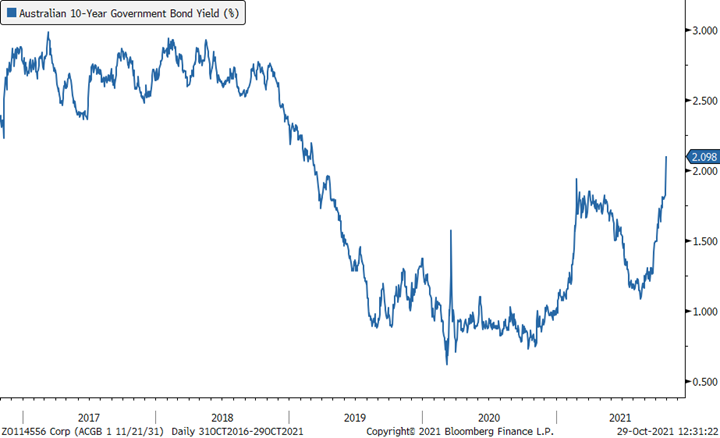

The main market story of this week has nothing to do with stocks though the S&P did hit a minor new high. Rather, the really big news is what’s happening to bond markets around the world. Putting it bluntly, they are getting pounded. This is particularly true on the short end of the yield curve (i.e., shorter maturity bonds) with some of the rate jumps truly eyebrow-raising, particularly on a percentage increase basis. (Please see the charts below and if they don’t shock you, you’ve probably been watching too many Halloween horror films!) If this type of carnage spreads to the US bond market, it will quickly become headline news.

Absolute yields levels remain, of course, miniscule and in most countries well below their inflation rates. Thus, most bond markets still “offer” negative yields, a most unappealing situation for fixed-income investors. Perhaps the term “fixed income” should be replaced with “nixed-income”.

While Delta fears in the US have largely evaporated, the rise in Covid cases in the UK continues to be worrisome. Moreover, it’s possible those infections are due to a more virulent variant than even Delta. Perhaps this is why economically-sensitive market sectors have been somewhat soft this week; however, this could also be a function of the aforementioned bond market convulsions, as well as China slowdown concerns.

Gold and silver miners have been beat up a bit this week, likely for similar reasons. Copper miners have held up better but still gave up some ground. Evergreens’ long-term bullish outlook on them has not diminished, however. Additionally, they remain up from their late September lows.

Despite the S&P 500 moving to a slightly higher high, the sub-surface market action continues to be less-than-inspiring. The divergence between the broader NYSE Composite Index and the S&P is one example. The NYSE Comp often weakens before S&P 500 corrections. The key to whether stocks experience a hiccup or something more serious may well lie with global bond markets. A true rout in the fixed-income world would be seriously bad news for almost every asset class. Hopefully, it will not get that disorderly but with such deeply negative real yields in most countries it is a non-trivial risk.

One of our favorite markets continues to be Japan. For those that missed it in prior EVAs, the Japanese market has broken out to a 28-year high. This is an extremely bullish development in Evergreen’s view.

Another long-favored area by our firm has been energy. It’s been on fire this year but it has also eased for the week. As usual, the high-yielding midstream infrastructure sub-sector has been weaker than the broader energy sector even though these utility-like entities have much less volatile business models than, say, oil and gas producers. It doesn’t really make sense but, as they say, it is what it is. Oil prices themselves have stayed resilient despite the growth and bond market worries described above.

2-Year Government Bonds

10-Year Government Bonds

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.