“To buy when others are despondently selling and sell when others are greedily buying requires the greatest fortitude and pays the greatest reward.”

– Sir John Templeton, founder of the mutual fund group bearing his name

“Go out on a limb—that’s where the fruit is.”

– American humorist, Will Rogers

“There is no security on this earth; there is only opportunity.”

– General Douglas MacArthur

______________________________________________________________________________________________________

Over the last few years, the spectacular rise and subsequent fall in asset prices for Bitcoin, pot stocks, high-end real estate and cash-burning companies have proven that the line between “in-favor” and “out-of-favor” is very thin and can evaporate almost instantly. One currently “out-of-favor” asset class that we have been particularly fond of is Master Limited Partnerships (MLPs) – the tax-advantaged, high-yielding oil, natural gas, or refined product pipeline businesses.

The MLP industry—and investors in it—haven’t had much to be thankful for recently. In this week’s newsletter, David Hay provides an overview of why the asset class has largely underperformed lately, while making the case for the long-term outperformance of this group. We believe this is especially relevant in the current market environment, where many stocks have reached all-time highs while bonds are yielding near all-time lows.

We hope readers had a wonderful Thanksgiving with family, friends, and co-workers. Thank you to our clients and readers for your continued loyalty and Happy Thanksgiving from the Evergreen family to yours!

“Do you want to know a secret? Do you promise not to tell? Whoa, oh, oh, closer. Let me whisper in your ear…”

Like almost everyone who came of age in the 1960s, I was a Beatles fan and I still am. The satellite radio station dedicated to the Fab Four is one of my few go-to channels and listening to it blows me away with how many monster hits they created in eight short years. The lyrics above were from one of their earliest breakthrough albums, in 1963, “Please, Please Me”. But the next line of the song is about love, a very different emotion than the one that is the subject of this newsletter.

The secret I’m sharing is about something that has become virtually radioactive to most investors these days. In my mind, it’s no exaggeration to say that the energy infrastructure entities known as Master Limited Partnerships (MLPs) are among the most reviled asset classes on the Planet Earth right now. Actually, it’s hard to come up with one that is more hated currently other than, say, Argentinian government bonds or the once smoking-hot Canadian pot stocks.

Up until mid-summer, this extreme penalty-box status didn’t look remotely probable. The main MLP index was up roughly 20% for the year as of July. But, then, as has been the case so often in recent years, the tide went out. It started as a mild reversal but the ebbing intensified In October to pre-tsunami speed. This was likely caused by institutions, which had decided to exit this long-lagging sector, bailing before the end of their fiscal year, typically 10/31. Next, it was retail investors who have done what they usually do when MLPs are weak at year-end: tax-loss selling without regard to price, yield or intrinsic value. In an investment area where individuals still are a major force this creates huge waves, often swamping those willing to batten down their hatches until the selling storm passes.

Repeated victims of this process since oil prices crashed in 2015 have been the closed-end funds that specialize in what is also known as mid-stream energy (meaning pipelines, and other physical energy assets that are between the well-head and the end user, such as utilities and gas stations). These funds are often leveraged and whenever MLP prices fall hard, they appear to suffer forced selling, more commonly known as margin calls.

There were a variety of factors that triggered this sudden fall from grace. However, one that seemed to be the ultimate “perp” was the ascendance of Elizabeth Warren in the polls. You have likely read and/or heard that Ms. Warren, if elected president, has said one of her first acts would be to ban fracking. While this would certainly have a wide range of negative implications, including almost for sure sending oil and gas prices rocketing, the mid-stream industry would no doubt be a major casualty.

Related to this has been a general antipathy toward anything fossil fuel-related. As noted in our October 18th “Apocalypse Not Now” EVA, this hostility even extends to low-carbon natural gas, despite the key role it has played in lowering America’s carbon emissions by approximately 20% over the last 15 years. Accordingly, an increasing number of professional investors are concluding that energy has become uninvestable. (That should be music to the ears of true contrarian investors, by the way.)

Another serious downward force on the mid-stream/MLP space has been extremely weak natural gas prices. Earlier this fall, the 12-month “strip”, or average price, hit $2.30 per million British thermal units (MM btu), a price at which very few producers can make money or even survive. (Nat gas prices are highly seasonal which is why it is important to use a forward-year average.) This has caused many companies that explore for and produce natural gas to announce spending reductions, implying reduced production growth. This, in turn, means lower volumes, or, at least, reduced throughput growth for the pipelines.

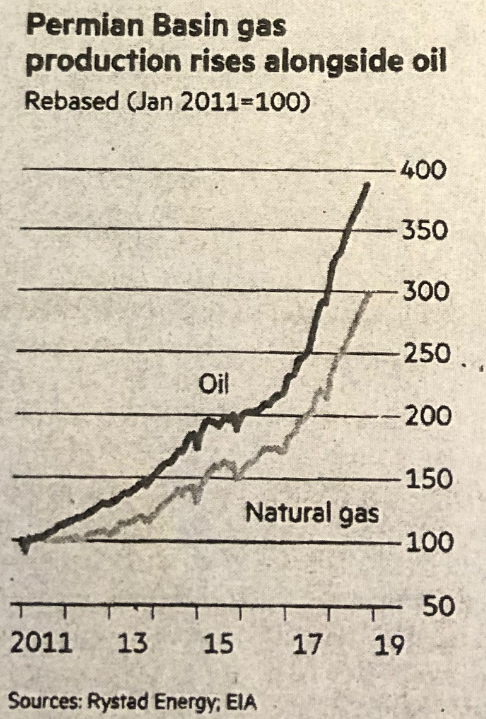

There are also escalating concerns about overcapacity in some of the most important producing areas, including the ultra-prolific Permian Basin. The Permian now puts out over 4 million barrels per day (bpd) of oil, about one-third of total US supply (excluding natural gas liquids or NGLs). Even though this is up from just 1 million bpd in 2010, enough new pipelines have been built over the last few years that what was, not long ago, a shortage of capacity has turned into an excess.

Pipeline safety concerns have been another worry for MLP investors. The Department of Transportation’s Pipeline Safety administration is rightly increasing scrutiny on the integrity of about 500,000 miles of “pipes” (out of roughly 2.8 million total miles of installed capacity), particularly those placed in service before 1970.

This confluence of negatives is likely to cause at least a few isolated distribution cuts, particularly for the more natural gas exposed entities. Retail investors are already burned out and turned off by another year-end swoon, especially with the S&P 500 at a record high. Consequently, they have adopted a “get me out” attitude, with the desire for year-end tax losses providing the catalyst to do so immediately – if not sooner.

Yet, even over the last punishing half-decade investors who have bought MLPs when they’ve been getting hammered near year-end have reaped significant rewards. 2015, 2017 and 2018 all fit the bill in that regard and in each case a 20% or greater rally ensued over the following three to six months. Evergreen anticipated a rough tax-selling season this year and thus is in a position to buy into the extreme weakness, something we’ve begun to do.

As most EVA readers know, I am in the midst of writing a book in real-time on what I believe to be the biggest investment bubble in history. It’s become apparent, as I’ve been doing so, that what we’ve seen is a series of bubbles, many of which have already popped. Bitcoin, the aforementioned pot stocks, high-end real estate in major cities (have you checked the tanking prices of luxury homes in LA lately?) and money-losing IPOs (initial public offerings) are just a few that have had a close encounter with a pin-prick. In fact, one could make the case that MLPs were in a bubble back in 2014, particularly in some of the sub-sectors. (This newsletter was warning that many were overvalued at that time.)

When a bubble implodes, what often happens in its wake is an anti-bubble. Instead of too much money chasing too few whatevers—be they tech stocks, crypto currencies, or tulip bulbs—the opposite happens. Instead of capital flooding in, it flows out in torrents. That’s exactly what is happening with energy in general right now and, in particular, MLPs.

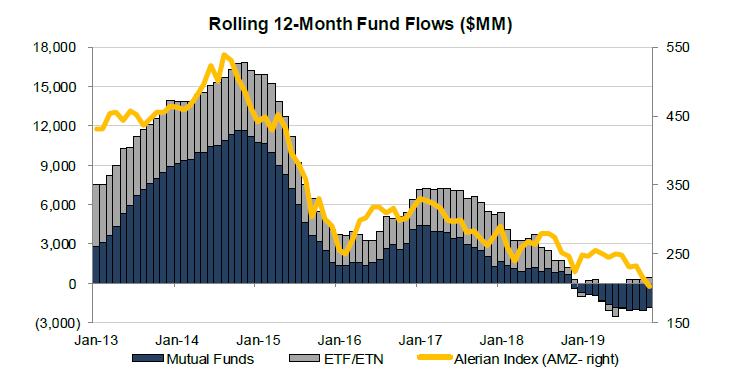

As you can see in the chart below, money has been exiting the MLP sector for the last two years at a rate that even exceeds the excruciating energy bear market of mid-2014 to early-2016. To that point, there already have been 219 days of outflows from MLP-dedicated mutual funds and ETFs this year, far eclipsing the 130 days of outflows in 2015 when oil price were in free-fall. Ironically, persistent outflows out of an investment sector or style are one of the best predictors of strong future returns.

Source: Bloomberg and Morningstar; Stifel presentation

In some cases, the abandonment of a specific asset class or an investment category can be rational. Tulip bulbs never did come back in favor and Japanese stocks—which, in the late 1980s, became the most spectacular equity bubble ever--are still only about half of their December, 1989, level. Undoubtedly, many feel that fossil fuel energy deserves similar disdain and long-term avoidance.

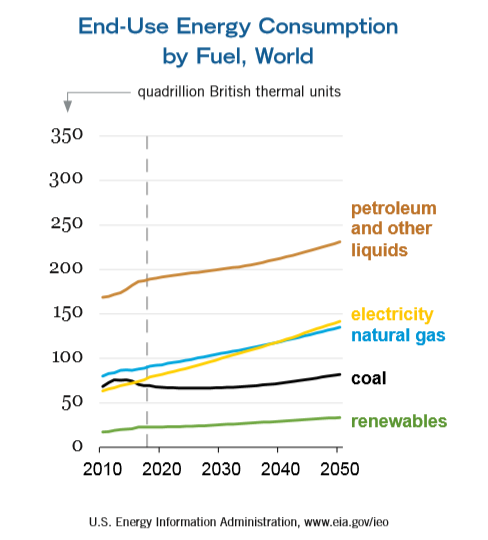

To be fair to the bear case on almost everything fossil fuel related, it’s probable that the fastest growth in energy demand is likely to be for renewables such as solar and wind power. However, that doesn’t mean that the need for oil and natural gas is going to ebb anytime soon (again, for more on this topic, please use this link). As the below chart from the US Energy Information Administration indicates, both are projected to see increasing demand for decades to come. Evergreen continues to believe that when it comes to natural gas in particular, there is an acute need for the blue fuel – even in an increasingly green energy world.

Additionally, the planet remains highly reliant on the US to meet the rising demand for oil and natural gas shown above. Conventional (i.e., non-shale) oil discoveries have been running at 70-year lows since 2015. Major energy companies are eschewing the long lead-time, high-risk, and exceedingly costly “elephant” projects. Instead, they are focusing more and more on fast pay-back US shale basins like the Permian. There are almost never the dreaded “dry holes” and the project cycles are in years, not decades. As the independent oil and gas companies retrench somewhat under intense pressure from disgruntled shareholders to produce free cash flow (i.e., cash flow in excess of capital spending), firms like Exxon, Chevron, Shell and BP have made the Permian their future resource growth vehicle of choice.

Another extraordinarily positive development for the US energy industry is the voracious demand for oil and gas exports to the rest of the world, especially developing countries. For most of them (and realize these include billions of consumers), oil and natural gas are far cleaner energy sources than they currently utilize. Reinforcing a crucial point made in the October 18th EVA, last week The Financial Times ran a front-page article pointing out that China is building more new coal plants than Europe’s entire installed base of coal generation.

Source: Financial Times

The opportunity for US LNG (liquified natural gas) to displace the highly toxic pollutants caused by burning coal to generate electricity, including for industrial uses, is immense. This creates another growth area for MLPs which, in some cases, have already built-out considerable infrastructure for LNG exports.

Incredibly, oil is another export success story. The US is now exporting around 3 million bpd to the rest of the world, a remarkable achievement for a country that was supposed to be a continual net crude importer (and, consequently, at the mercy of frequently hostile nations).

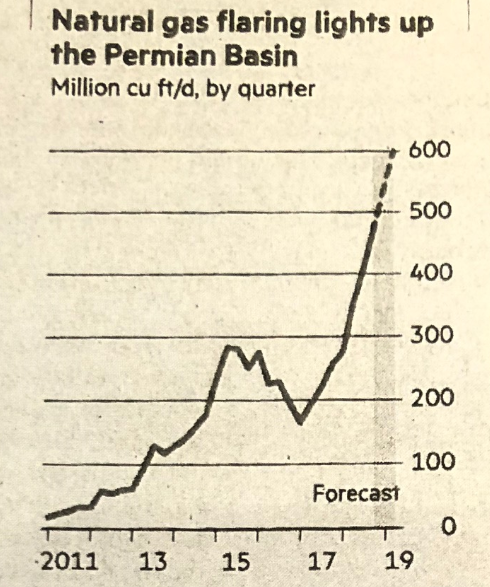

The MLP industry is also playing a key role in reducing the flaring of natural gas in areas such as the Permian. Vast amounts of the blue fuel are incidentally produced when oil is extracted from shale formations (this is known as associated gas). Due to a lack of pipeline takeaway capacity, billions of cubic feet of gas per day are simply burned off, a tremendous waste and not great for the environment. (Estimates are that there is a need for an additional 15 billion cubic feet per day of such capacity, equivalent to about 15% of all US natural gas output.) Several leading MLPs are alleviating this grave problem by building a series of new pipelines, some of which have already gone into service.

Source: Wall Street Journal

Therefore, it’s highly unlikely that there won’t be enough hydrocarbons to utilize most US pipelines and other infrastructure assets. And, as far as Ms. Warren’s frac ban is concerned, the worst case is probably a prohibition on federal lands (the good news is that, if we’re right, oil and gas prices won’t do a moon-shot). Most MLPs have modest exposure to production from US government land.

Every industry has its risks, including high-tech which is also in Ms. Warren’s cross-hairs. The difference is that MLPs are pricing in all of the downsides (and then some, in our view) whereas most US stocks are back up to prices that assume we live in a highly certain, low-risk world. You don’t have to be an economic or geopolitical expert to realize that’s definitely not reality. Actually, one could argue it’s the polar opposite with the world about as polarized as it has ever been, short of global military conflict.

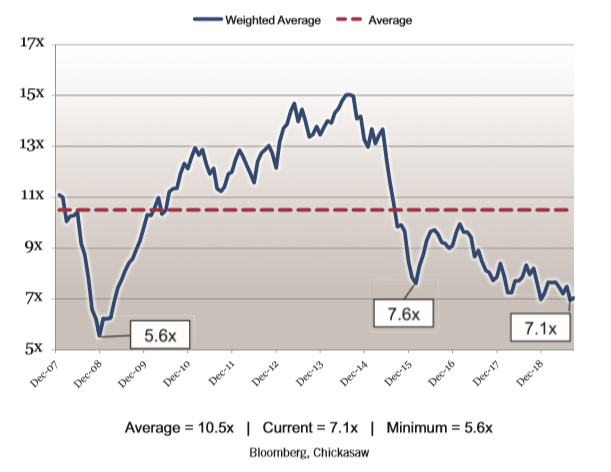

Presently, the top 20 MLPs sell at an average of 13 times earnings vs the S&P at 17 and most big utilities at 20 times or more. Moreover, the MLP index has a cash flow yield of almost 10% versus only 2% for the S&P 500 and around 3% for the utility index. Such yields imply payout cuts yet estimates are for the mid-stream sector overall to raise distributions about 7% this year and to continue to increase them (albeit probably at a slower rate) going forward.

Encouragingly, fundamentals are much healthier in most cases than they were in 2016 when oil was under $30 per barrel and MLP prices were similarly bombed-out. Coverage ratios (a measure of excess distributable cash flows versus their payouts) are far stronger and debt is materially lower for most of them. Many have also eliminated the splits to general partners so that all future cash flow growth goes exclusively to the limited partners (i.e., MLP investors). The majority have also been meeting or exceeding Wall Street earnings estimates lately, as well. Further, because of their excess cash flow, MLPs are largely able to “self-fund” their capital spending needs. Thus, they are able to avoid the dilutive aspect of raising equity when their market values are at fire-sale levels.

Alerian MLP Index Price-to-Distributable Cash Flow

Typically in the past, insider buying and share buy-backs were as rare in the MLP world as accurate facts are in a political debate. Now, however, both are becoming increasingly common. In fact, the CEO and founder of one of the largest MLPs recently made a $45 million purchase. Among a wide array of MLPs, senior managers are persistent buyers, at a time when insider selling on the S&P itself is running at one of the highest rates ever.

Another once infrequent event in the MLP world that has become more commonplace relates to takeovers. There have been three MLP acquisitions, at substantial premiums to where they were trading prior to the buy-outs, since last spring. We expect more before year-end, possibly several. Even private equity firms (those that typically use leverage to acquire their targets and take them private), are coming after MLPs. These buyers are flush with cash and very attracted to the lofty, mostly reliable yields energy infrastructure generates. One of the biggest MLPs is rumored to be considering going private at a 70% premium over its current depressed price.

It strikes this author as incredibly ironic that during a decade when yields on other income vehicles have collapsed and US energy production has more than doubled, mid-stream energy infrastructure should be one of the most reviled asset classes on the face of the Earth. Undoubtedly, the industry has experienced some self-inflicted wounds but, in my opinion, they have been far from fatal. One of those involves accidental environmental incidents. There have been spills, explosions and other environmental problems. One of the few guarantees I’ll make is that there will be more. But it’s essential to realize that pipelines are the safest way to deliver hydrocarbons over long distances. The industry has a 99.999% safe delivery rate based on US Dept. of Transportation findings.

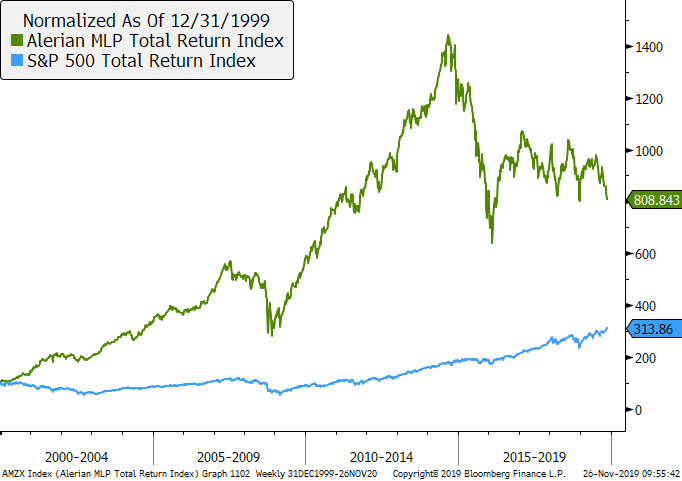

Another surprising reality is that despite a horrific performance streak since mid-2014, MLPs have materially out-performed the S&P 500 since the late 1990s. You can almost certainly win a lot of money betting your brother-in-law about this factoid—particularly if he’s been invested in mid-stream over the last five years!

Source: Bloomberg, Evergreen Gavekal

The MLP industry—and investors in it—are learning a hard lesson about the fickleness of popularity in the investment world. Even for the premier company in the sector, one that has raised its distribution for 53 quarters in a row, the market has rewarded it with a 36% price decline since September, 2014. Talk about giving no quarter—even when every three months has brought its owners higher cash flow!

Maybe it’s a classic case of another Beatles song from their early era, the 1964 mega-hit, “Can’t Buy Me Love”. Over my career I’ve learned that when prices are falling, love is almost impossible to come by and the opposite emotion nearly always dominates. Let me tell you another secret: in the next bear market for the S&P 500, a lot of companies are going to feel the hate. And they won’t have 10% yields to ease the pain.

David Hay

Chief Investment Officer

To contact Dave, email:

dhay@evergreengavekal.com

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.