"You can check out any time you like, but you can never leave."

-The Eagles, from their classic song, "Hotel California"

The Immaculate correction. Maybe it really is that painless. Perhaps it is possible that US stocks can go through a series of rolling, sector-specific corrections that eliminate the need for a broad market sell-off. If so, it’s potentially feasible that the long-lagging high-quality issues might actually go sideways, or even rise a bit, as the speculative mania fades in areas like biotech, fuel cell, social media, and cloud computing.

Actually, the results so far this year are encouraging in that regard. In a dramatic reversal from last year (as so often happens), safer and better-yielding stocks, like utilities, have shellacked the high-flyers—the darlings of 2013. Additionally, one of the most influential men in the world of finance today has publicly endorsed this idea of an immaculate correction.

If you think I am referring to Warren Buffett or Kyle Bass, you are a bit off the mark. Rather, the investment thought-leader I have in mind is none other than CNBC’s ever-effervescent Jim Cramer. Earlier this month, he assured his viewers that there was no reason to be concerned about a bursting bubble in tech and other go-go/mo-mo issues. Naturally, this caused me to turn up the volume and listen closely to his rationale, which was essentially as follows: Don’t worry about that bubble because IT HAS ALREADY POPPED!

Considering that the group of tech stocks trading at over 10 times annual sales—an accepted indication of true bubble status—had recently declined by nearly 40%, this was a reasonable point for him to make. However, what struck me as more than a touch disingenuous is that he never, at least to my knowledge, admitted there was any bubble as it was in inflation mode. (If any readers know otherwise, don’t hesitate to correct me.)

Rather, what I remember him saying is that investors shouldn’t be concerned about valuations on companies like Tesla, Amazon, and Netflix. Cramer claimed their products and services were so great that price really didn’t matter. In his view, they were going higher regardless of 100 plus P/Es, and, to Jim’s credit, for awhile, they did exactly that.

Ever since I promised not to ridicule Seattle sports teams in the wake of the Seahawks’ slaughtering of a certain team whose mascot is a horse, I’ve been in search of a new piñata, and, for now, Jim is my paper-mache pony. It’s not that I don’t like him. How could you not?

He’s fun, he’s witty, and he’s got more energy than Hoover Dam. But, what bugs me is that so many viewers treat him as a serious investor versus the highly entertaining showman he is. Moreover, I am chagrined by his tendency to fuel the speculative fires that have engulfed countless smaller investors as this bull market moved into its incendiary phase.

Also, in his defense, Jim is not alone in his bubble blindness (notwithstanding his recent epiphany). Numerous strategists from the major Wall Street firms are continually opining that they don’t see the excesses that typically mark a market top. Some have gone so far as to say that this is the most hated bull market they’ve ever seen.

To which I say: Really?

Make that eight out of nine. A specific example of this sanguine attitude is a piece I came across back in early March. At that time, the nifty-fifty were ironically on the verge of becoming a lot less nifty and a lot more thrifty. This report showed nine indicators as part of its "Bull Market Top Checklist." In 2000 and 2007, all of the boxes were checked (at least in hindsight), such as rising real interest rates and deteriorating earnings revisions, two elements it conceded are now warning of a "Bull Top." However, in this firm’s soothing opinion, none of the other seven had been triggered. These were: "Blow off top," "Heavy inflows into equity mutual funds," "Big Pick-Up in M&A" (takeovers), "IPO Activity," "Erosion of stocks making new highs," "Shift towards defensive leadership," "Credit spreads moving in the wrong direction."

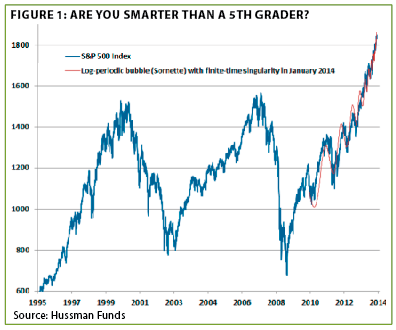

Maybe I’m just too critical, but, in my ever-more humble opinion, I believe all of the above, save credit spreads moving in the wrong direction, now deserve a big, red check next to them. In fairness to this firm, some of these have changed since they published their checklist, but a number of them were already flashing scarlet three months ago. Past EVAs have shown the below chart on the stock market, but it continues to be one of my favorites, and it sure looks like a blow-off top to my eyes. (See Figure 1)

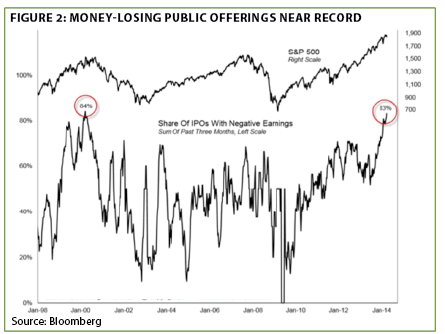

Additionally, last year saw the highest in-flows into US stock funds since 2000, M&A has done a moon-shot, IPO activity has been blistering (with 83% of recent issues proudly spewing red ink, per Figure 2 below), the number of stocks making new highs has plunged since a year ago, and, in 2014, utilities are killing growth issues.

Yet there’s more…

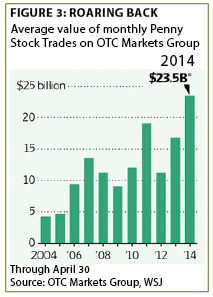

As EVAs this year have repeatedly shown, margin debt has done its own version of a blow-off top, as has retail trading at firms like TD Ameritrade and E-Trade. To underscore how rabid small investor risk appetites are presently, the Wall Street Journal just ran an article,"Penny Stocks Fuel Big-Dollar Dreams." It goes on to point out the frenzy that is occurring in this most speculative of all stock market spaces, as illustrated by the following chart from this piece. (See Figure 3 on the next page)

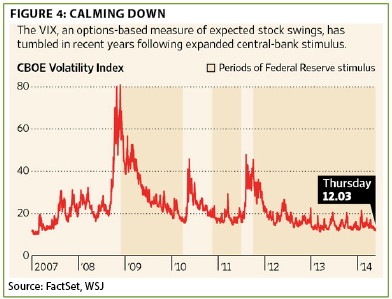

The same Journal edition had an article right above the one on penny stocks with this headline: "Investors Show Little Fear." It also featured a rather telling graphic. (See Figure 4)

As my Singapore-based chum, Grant Williams, said so eloquently at this year's Mauldin/Altegris Strategic Investment Conference (SIC), "The ultimate bubble is in complacency." (Coincidentally, Grant's latest newsletter is a fun and lively expose of the zany valuations in tech, what he calls Eyeballs 2.0; to access it, please click here.)

Now, wait a second! This is starting to sound a lot like my typical EVAs over the last year and a half, quibbling with this bull market. Let's get back to the immaculate correction concept, shall we?

A Tale of Two Conferences. Candidly, the last couple of weeks have been a bit rough on my aging body. Right after the SIC, I headed to Jacksonville for the National Association of Publicly Traded Partnerships* (NAPTP) confab. Fortunately, Memorial Day weekend allowed me a change to regroup and assemble my overflowing thoughts from the past fourteen days. One memory, that has come back to me upon reflection, was a polite opinion exchange I had at the SIC. It's one thing if you disagree with another firm, but when you dissent with one of your own partners, especially in a high-profile setting, it's a bit more serious.

*Popularly known as MLPs or Master Limited Partnerships.

Anatole Kaletsky is the "Kal" in GaveKal and, in case you haven’t noticed, Evergreen’s full name is Evergreen GaveKal. Anatole is arguably the most influential financial journalist in Europe, and after seeing his presentation at the SIC, I fully understand why. Frankly, his delivery of the bull case he supports was remarkably articulate. He spoke for almost an hour, while every other speaker held their prepared remarks to just thirty minutes. Yet, as I looked around while he was talking, I noticed the audience was completely captivated.

His message was resoundingly upbeat: Fed policies are working, the economy is set to accelerate, valuations are reasonable (if a bit stretched in some of the more dice-rolling market niches), and corporate profits are basically hovering on a permanently elevated plateau (at least given the attention span of most investors these days). Essentially, his talk was a tour-de-force of the bull argument, though he did admit toward the end that US and eurozone stocks weren’t as attractive as emerging markets, a point that resonated with me.

Gadfly that I am, I raised my hand to ask him—in front of several hundred listeners—about margin and margins. I wanted to get his take on the exceedingly stretched current status of both margin debt and corporate profit margins. He blew off the former and explained that he believed sales were poised to bust out on the upside, which would keep profits at their present vertigo-inducing levels, even if margins came under some downward pressure. (Interestingly, Will Denyer, one of GaveKal’s rising stars, just wrote an essay stating margins would stay elevated due to weak sales caused by an aging population. It’s safe to say, opinion-conflict is alive and well at GaveKal.)

The second part of my question pertained to my concern that if the economy was as hunky-dory as he believed, present Fed policies, which are more stimulative than at any time in US history, are totally inappropriate. My follow-on point was that if he was right, the Fed would need to go, in the inimitable words of Dick Fisher, one of the newest Fed policy setters, from

Wild Turkey to cold turkey. His reply was that the Fed could gradually reduce their multi-trillion dollar liquidity infusion with no ill effects on the economy or financial markets.

If you sense that I’m a Doubting Dave, you’ve got excellent instincts. Yet, the fact of the matter is that Anatole’s stock market views have been more accurate than mine over the last eighteen months (though the reverse is true when it comes to bonds). Thus, perhaps events will unfold as Anatole sees them, with an ongoing shakeout in the nutty sectors, while the blue chip stocks do just fine—pretty much along the lines of what we’ve seen this year.

All that sounds idyllic to me, given how overweight Evergreen clients’ equity portfolios are in the Rodney Dangerfield "Get No Respect" variety of high-quality stocks. But somehow, it doesn’t quite ring true…

Tepper Tantrum? David Tepper has become one of the most celebrated hedge fund managers in recent years because of his prescient recognition that QEs 2 and 3 were going to provide rocket fuel to US stocks. Lately, though, he has caused some consternation among market bulls by shifting to a much more guarded tone. While insisting he’s only neutral and not bearish (almost no one is willing to wear that label, except perhaps me and a few other crazies!), Mr. Tepper uttered a sound bite remarkably similar to Grant Williams’, by referring to what he called "coordinated complacency." Perhaps that seems like a benign state of affairs, but when investors are complacent, volatility fades into tranquility. And, as the now iconic economist Hyman Minsky, frequently quoted by Paul "The Dude" McCulley, so concisely observed: "Stability breeds instability." (Please click here to read Tyler’s humorous take on Mr. McCulley, who Pimco just re-hired with copious fanfare.)

Reinforcing Minsky’s point, the Financial Times’ James Mackintosh, author of its must-read daily column, "The Short View," ran this factoid last week: "Only twice since 1990 have volatility in US bonds and equities both been so low at the same time: in 2006-07 and in 1998. Both presaged market disasters, with the stability of bonds encouraging Long-Term Capital Management to take on massive leverage in 1998, and a full credit bubble developing before the subprime crash."

Now, you don’t associate the word "crash" with MLPs, but I have to say that the near-euphoria I witnessed at the Jacksonville conference was disconcerting to me. As nearly all veteran EVA readers are aware, I’ve been a long-time fan of these reliable income vehicles (including back when they were almost universally neglected), and they’ve delivered extraordinary returns to our clients for many years. But those exceptional gains over such an extended period are precisely what make me nervous as does an emotion I picked up on in Florida that is even worse than complacency: greed.

IPO mania has hit the once-staid world of MLPs. There was excited chatter in Jacksonville about how much money had been made on deals that have come out over the last couple of years, with one issue having risen over 400% in less than a year. Evergreen clients have enjoyed some of this windfall but, beyond the almost too-easy gains, I worry about how much these have been a

function of the Fed’s even easier monetary policies. There is so much cheap money floating around that there is no doubt in my mind even MLPs are being levitated by those borrowing at 1% short-term rates to "invest" at higher yields in this sector. As with US common stocks, it’s the sexier names that look at greatest risk; most of the older, more traditional, issues are not nearly as stretched—which leads me back to this EVA’s main theme of an immaculate correction.

Is it possible for some of the high-flying MLPs to get slammed while the far more reasonably priced, and higher yielding, issues resist the eventual shakeout? Possible? Yes. Probable? Probably not—as much as I would like that to be the case. Similarly, I would love to see our fairly-valued blue chip stocks not suffer once the air begins to rush out of the Fed’s overt stock price inflation but that also seems improbable. (If you think I’m too cynical, Ben Bernanke announced kiting equities as an express goal in a Wall Street Journal Op-Ed piece back in 2010!)

My opinion jousting has involved many more individuals than my talented partner, Anatole. I have also crossed verbal lances with professional investor friends of mine, who believe I’ve become a perma-bear. To them I say: Au contraire, mon ami. I’m simply perma-realistic and, right now, realism bites.

Here Lie the Real Dragons. Even though Jeff Gundlach is a bond guy, he did make an incisive stock market observation during his presentation at the SIC. Loosely quoting, he believes it’s morally offensive that insiders are selling at nearly a record-breading pace while, simultaneously, their companies are buying back massive sums of stock, using shareholder money. You’ve got to admit, he’s got a point there.

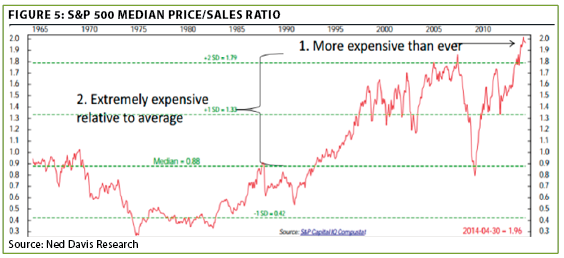

Further, I believe the chart below makes an even more powerful statement, one that overrides the usually airy comments from most market strategists, that stocks aren’t currently overvalued. The prestigious Ned Davis Research recently published a chart based on Evergreen’s favorite price-to-sales metric revealing the median stock to be more expensive than at any time since 1965. (See Figure 5)

Okay, but let’s attribute this very worrisome valuation measure to the fact that medium-sized companies are much pricier today than they were back in the dotcom days, pulling the median up to this record-breaking level. Therefore, the type of elite companies we primarily own for our clients are not where the serious vulnerability lies. This is an argument that I totally concede (though I continue to worry about collateral damage from blow-ups in other areas).

Yet, it’s dawned on me that with all the focus on stocks, we might be missing the true powder keg: the bond market. As with stocks, it’s essential to make a distinction between high-grade and low-grade bonds. Unlike most of Wall Street, I’m not particularly worried about US Treasury bonds, at least anytime soon. But I am becoming increasingly concerned about riskier debt, which has been the best place to be in the bond market for years—at least until lately.

Marty Fridson is one of the sharpest operators in this segment of the debt world, and he describes junk bonds as having gone from "way overvalued to way, way overvalued." Somehow, that doesn’t sound encouraging.

Spreads, or the difference in yield between corporate and government bonds, are exceedingly compressed currently. As noted in the May 9th EVA, based on the ground-breaking studies of Jeremy Stein (who just left his senior position at the Fed), when credit spreads widen, it sets off a nasty chain reaction. A mere ½% increase in spreads over a few months time has historically caused a 2% contraction in economic activity. That’s a very big deal in our Lilliputian-growth world.

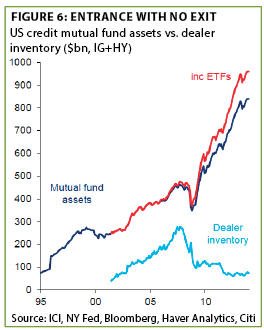

Making this situation even more fraught, fixed-income ETFs have gone viral, including those involved in many of the most illiquid and volatile niches of the bond market. Meanwhile, banks and brokers have drastically reduced their inventories of the underlying debt instruments. This has created what I believe is a highly dangerous situation once spreads begin to widen out, as they always do (which would be the ninth "Bull Top" warning to fall into place, per the earlier check-list). Who is going to be on the buy-side when overleveraged "investors" are forced to liquidate as prices fall? (See Figure 6)

To reiterate, based on how Evergreen client portfolios, and my own, are positioned, I love the idea of an immaculate correction. I’ll even admit it’s possible in the stock market. But when it comes to the type of excesses I see in the credit markets (not to mention luxury real estate, rare books, vintage wines, and high-end art), I’m not going to mince words: This is one bodacious bubble.

Accordingly, I thought I’d conclude this week’s EVA with a quote from one of the most hallowed economists of all-time, Friedrich Hayek, co-winner of the 1974 Nobel Prize in Economics (courtesy of John Hussman): "To combat depression by a forced credit expansion is to attempt to cure the evil by the very means which brought it about; because we are suffering from a misdirection or production, we want to create further misdirection—a procedure which can only lead to a much more severe crisis as soon as the credit expansion comes to an end."

But what the Hayek! As Jim Cramer said last year, in the meantime we can make some money…at least until we all try to leave the Hotel California.

Important Disclosures

This report is for informational purposes only and does not constitute a solicitation or an offer to buy or sell any securities mentioned herein. This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. All of the recommendations and assumptions included in this presentation are based upon current market conditions as of the date of this presentation and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. Information contained in this report has been obtained from sources believed to be reliable, Evergreen Capital Management LLC makes no representation as to its accuracy or completeness, except with respect to the Disclosure Section of the report. Any opinions expressed herein reflect our judgment as of the date of the materials and are subject to change without notice. The securities discussed in this report may not be suitable for all investors and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. Investors must make their own investment decisions based on their financial situations and investment objectives.