“Evergrande has been called a cat with nine lives. They’ve had a liquidity crisis for years…But, using the cat analogy, this cat got too fat.”

– Shuli Ren, Bloomberg Opinion columnist

______________________________________________________________________________________________________

China’s official debt-to-GDP ratio has surged by 45 percentage points since 2016, leaving it with one of the highest debt ratios for any developing country in the history of mankind. The Chinese property sector is particularly notorious for its addiction to debt and Evergrande, the most-indebted property developer in the world, has on-balance-sheet liabilities that amount to nearly 2% of China’s annual GDP.

As one of the main engines of economic activity for the Chinese economy, this borrowing spree has elevated Chinese real estate prices into bubble territory – several times higher, relative to household income, than the US and other major economies. As alluded to in this week’s quote, Evergrande – one of the country’s largest property developers – has had a debt problem for years and short sellers have been taking short positions for nearly a decade. In the past, it was widely assumed that they were too big and integral to the Chinese economy that they would never be allowed to default on their debt obligations.

However, in an effort to transform the country’s financial system by encouraging “genuine growth” rather than “fictional growth,” Chinese regulators have decided to engage in a showdown with creditors over Evergrande.

On Monday, the showdown hit a crescendo, at least for now, as markets across the world were jolted by the possibility that Evergrande would default on its $300 billion of debt obligations. As we’re writing these words (Friday morning during Asia hours), the company had not made any announcement that it has paid its $83 million interest payment due Thursday, leaving investors in limbo.

The question becomes, is there a broad implication for markets if Evergrande does in fact default on its debt obligation in the coming days? Could this be, as some have speculated, China’s “Lehman Moment”? This week, we are presenting an opinion on the subject from one of our Gavekal colleagues, Wei He. Wei does not believe a systemic crisis is in the cards for the country’s financial sector but does concede that the default of such a large and financially connected company will cause serious short-term pain for the financial system and economy – with the potential for ripple effects beyond Beijing.

Fears about the potential systemic risks posed by troubled property developer China Evergrande Group reverberated through global financial markets on Monday. The company has already begun defaulting on some of its debt obligations, and it appears unable to pay interest or principal on loans due this week. However, unless China’s regulators seriously mismanage the situation, a systemic crisis in the country’s financial sector is not on the cards.

Nevertheless, the default of a company as large and financially connected as Evergrande is still going to cause visible short-term pain for both the financial system and the economy. Growth momentum has already slowed more than expected under the impact of multiple tightening policies. Evergrande’s troubles further raise the probability of early action to continue easing monetary policy.

The strains on Evergrande’s highly levered business model became more obvious around 12 months ago, as financial regulators resumed their years long effort to control financial risk and speculation in housing markets, imposing strict new limits on the leverage of major property developers. A further tightening of housing policies in recent months has led to a sharp weakening in sales momentum, with national property sales volume falling -8.5% YoY in July, making it even more difficult for Evergrande to keep generating cash.

The fate of Evergrande is therefore closely tied to the government’s tough real estate policies. Those would be politically difficult to reverse, so the preferred outcome is likely to be combining a solution for its individual problems with continued overall restrictions. There are precedents for such a nuanced approach. The recent drama around Huarong, another troubled Chinese borrower in offshore bond markets, was resolved fairly smoothly when the central government arranged a recapitalization led by other state-owned enterprises.

That decision showed the government was not wedded to its rhetoric about removing implicit guarantees, and is sensitive to the need to avoid wider financial risks. Yet as a financial institution directly owned by the Ministry of Finance, Huarong is not a simple parallel to mostly private Evergrande.

The central government is certainly not trying to engineer the collapse of Evergrande just to demonstrate its toughness on real estate. But its hands-off stance—the central bank said it is the company’s responsibility to deal with its financial problems—has created uncertainty and delayed resolution. So far, the provincial government of Guangdong, where Evergrande is based, appears to be taking the lead, having hired advisors and started negotiations.

It’s not too difficult to sketch the outline of an eventual solution. The political priority is going to be to protect the homebuyers who have paid Evergrande for housing but have not yet received completed units. The simplest way to do that is for other developers to take over the projects and finish construction, and use the proceeds of further apartment sales to cover debts.

But such transfers have not happened yet, suggesting Evergrande’s projects are not attractive, and that its assets are not as valuable as previously thought. Evergrande said last week that it had made “no material progress” in its efforts to sell assets to raise cash. With Evergrande’s US dollar-denominated bonds now trading around 20-30% of par, the gap between the market value of Evergrande’s assets and its liabilities could easily be in the hundreds of billions of renminbi (and more if off-balance-sheet liabilities are included). If the households which bought the properties and the companies building them are protected, it is financial institutions which will have to absorb losses.

That process will create financial risks—most obviously for lenders. Thanks to conservative regulation, China’s large banks have substantial provisions against bad debts and can probably ride out defaults. But many smaller banks have higher levels of exposure to real estate and weaker finances. Banks with concentrated exposure could have more trouble financing themselves in the interbank market, and some could be dragged down by losses on Evergrande-related loans. Evergrande is the largest shareholder of Shengjing Bank, a local bank in Shenyang with which it has numerous transactions.

The bigger worry is probably nonbank financial institutions such as trusts, which as of 1H20 reportedly accounted for about 45% of Evergrande’s interest-bearing liabilities, compared with just 25% for bank loans. Some trust companies could fail, and wealthy investors in trust products will be forced to take losses. In addition, liquidity risks for weaker property developers are rising as bond investors fly to quality. With investors pricing in higher odds of default, it will get harder for some developers to refinance themselves.

None of these channels of financial risk will inevitably spiral out of control, as long as China’s regulators step in to break self-reinforcing feedback loops. The good news is that after a series of failures and near-failures including HNA Group and Baoshang Bank, regulators have plenty of experience in containing risks posed by troubled institutions. Still, the difficulty of managing the fallout from Evergrande is greater, given the number of institutions involved and the large role of nonbank lenders. One consequence is likely to be a wider spread of funding costs between banks and nonbanks.

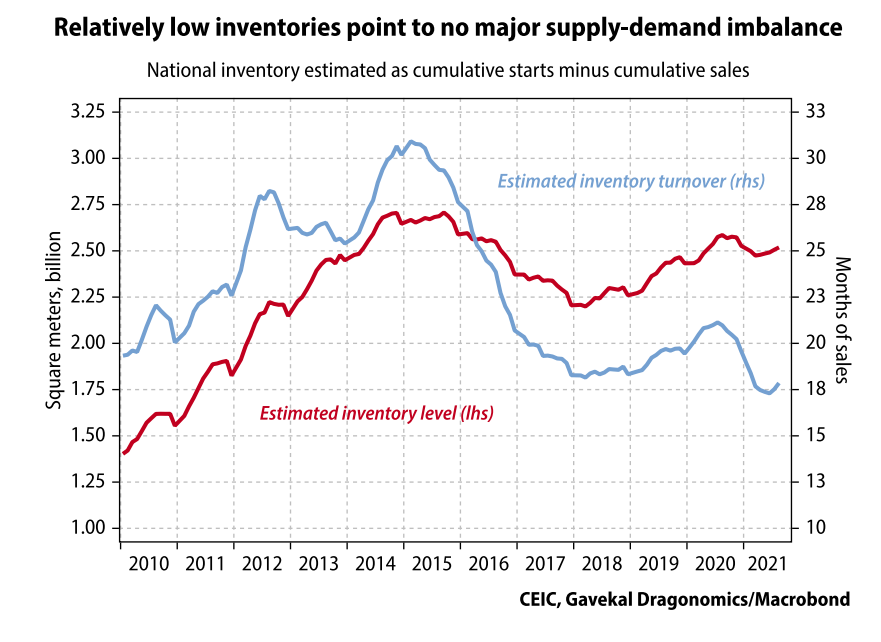

The true systemic risk to the financial system would be large and sustained declines in housing prices and sales. Such an eventuality would be the most likely trigger for a major change in China’s tough real-estate policies, but is not imminent. In aggregate terms, the balance between housing supply and demand is not out of whack, in part because tight financial policies have prevented developers from overbuilding. Nonetheless, defaults are a deflationary impulse and will dampen the economic outlook. A tighter funding environment for developers will reduce land sales and new starts, further dampening construction activity and materials demand.

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.