“Stock market bubbles don’t grow out of thin air. They have a solid basis in reality, but reality as distorted by a misconception.” -GEORGE SOROS, billionaire investor

“The problem with bubbles is that they force one to decide whether to look like an idiot before the peak, or an idiot after the peak.” -JOHN HUSSMAN, famed money manager

“If you have 10,000 regulations, you destroy all respect for the law.”

-WINSTON CHURCHILL

POINTS TO PONDER

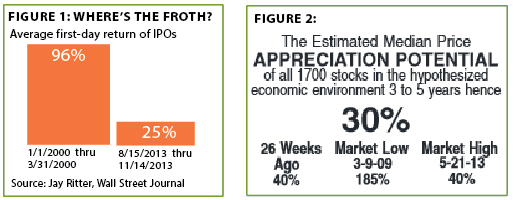

1. In another sign of escalating speculation, the initial public offering (IPO) market has heated up considerably of late. However, average first-day trading gains of 25% on today’s crop of new issues remain well below the one-day near doubling seen back in early 2000. Of course, comparing against the wildest stock market mania in history may not be an exercise in rationality or prudence. (See Figure 1, left)

2. One of the more reliable long-term indicators of an overvalued or undervalued broad market is Value Line’s estimated median return potential on its 1700 stock universe. It recently hit 30%, among the lowest readings on record. (See Figure 2 above, right)

3. 2007 was considered the high-water mark for frenzied and reckless lending practices, with an explosion in the issuance of “cov-lite” loans being one of its signature events. Yet these loans, characterized by extremely lax covenants (i.e., little lender protection and/or recourse), are now being issued at twice the rate of six years ago.

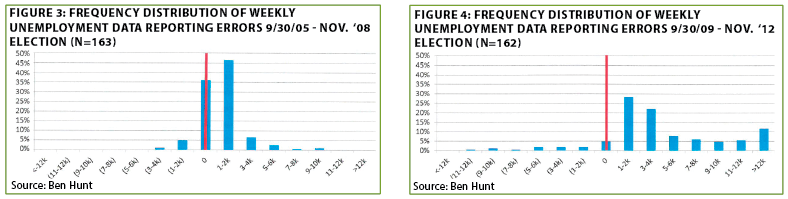

4. It may be sheer coincidence but there was a dramatic deterioration in the accuracy of the Department of Labor’s jobs data from 2009 to 2012. There are those who believe the current unemployment numbers continue to be manipulated in such a way as to understate the actual jobless rate. (See Figures 3 and 4)

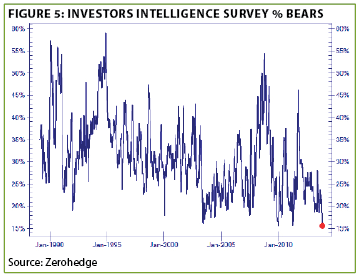

5. Once more underscoring how extreme bullish sentiment has become, a recent Investors Intelligence survey found that participants expecting the rally to persist surged from 42% to 49%, while those anticipating a decline fell from 22% to a mere 16%. Similarly, net speculative long positions in the S&P 500 futures contract have risen by almost 400% since mid-September. (See Figure 5 below, left)

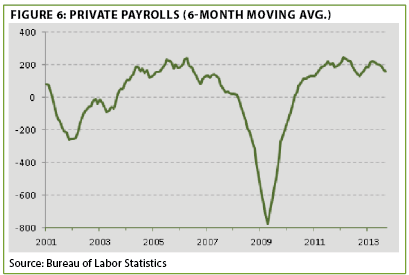

6. The Fed has fabricated nearly $2.5 trillion in a frantic attempt to stimulate payroll growth. Yet, looking at just the private sector, where job creation has been more robust than in the public realm, the six-month moving average has plateaued, albeit at a respectable level. (See Figure 6)

7. Previous EVAs have commented that a US recession is unlikely in the near future because the yield curve is not inverted. However, as Charles Gave from GaveKal research points out, numerous past US downturns have occurred without short-term interest rates being above long-term rates, the 1930s being one example. Moreover, he cites the fact that Japan has had multiple recessions without an inverted yield curve and that this was also the case in Europe over the past two years.

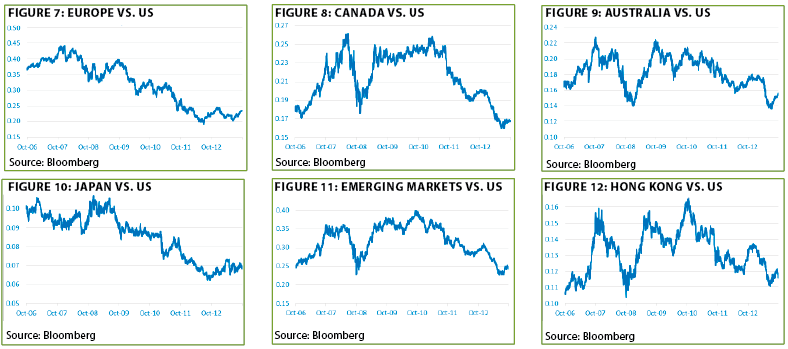

8. After years of lagging the US, foreign stock markets are beginning to display improving relative strength. However, at this point it is premature to say this is a sustainable trend as opposed to another head-fake, as seen intermittently over the last year. (See Figures 7 thru 12).

9. There's much to like about Canada's economic outlook, including far lower government debt than in the US, one of the developed world's few remaining AAA ratings, a nearly balanced federal budget, and materially lower unemployment than in America or Europe. However, housing prices 60% above their long-term mean and household debt at 163% of GDP definitely counterbalance some of the allure.

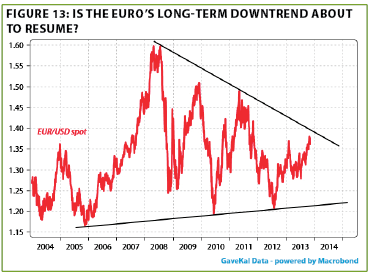

10. Although the euro has enjoyed a spirited rally relative to the dollar over the past few months, notwithstanding a mild correction lately, it remains locked within a long-term downtrend. (See Figure 13)

11. Optimism was running high this summer that Europe was finally emerging from its double-dip recession. Unfortunately, third quarter releases were notably anemic, with both France and Italy contracting once again. Even mighty Germany saw a deceleration to just a 1.3% annualized growth rate.

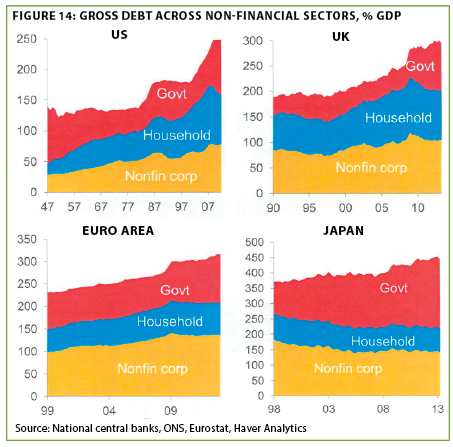

12. Despite the fact that there has been some deleveraging in the private sectors in the US, the UK, Europe, and Japan, the explosion in government debt in all four has more than offset this healthy trend. (See Figure 14)

13. Prior EVAs have observed the rabid buying of gold in China after prices crashed last spring. To put this surge in perspective, physical bullion deliveries in Shanghai since that time have nearly equaled total global mine output. (See Figure 15)

14. China has managed to avoid a housing market meltdown like the one that broadsided many rich countries five years ago. However, given that property prices in major Chinese cities have quintupled in the last 10 years, it is unlikely China will escape unscathed from the excesses in its property market.

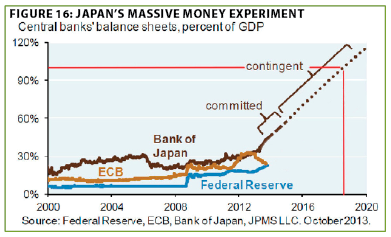

15. The Bank of Japan (BOJ) is dramatically upping the ante in the global central bank arms race. Based on current money creation trends, the BOJ will own assets equivalent to the total size of Japan’s economy by 2018, all purchased, of course, with alchemic funds.

Estate planning for dummies. Who knew it could be so easy? After spending years doing complex planning, laying out tens of thousands of dollars in legal fees, and even more in life insurance premiums, I found a dummy-proof way to minimize my estate tax liability. All it took was a two-week trip for my wife’s major milestone birthday to Spendy Sandy Lane in Barbados! (If you think I’m kidding, what we owed at check-out was more than the down payment on our first house.) And, in keeping with a theme of this week’s EVA, it was an exercise in simplicity.

Despite the major hit to my net worth, one of the advantages of being in such a remote spot is that it’s very hard to receive FedEx packages (and it would probably have cost the equivalent of a first class airline ticket to get one there). So, I didn’t receive my usual every other day 10-pound research packet, allowing me, as I wrote in last week’s EVA, to catch up on long-deferred reading. It also gave me the chance to do some serious contemplating about where we are heading in our country, both economically and politically.

Most of what I want to convey from my latest “tropical musings” will be forthcoming in the weeks ahead (some of you may recall the EVA I wrote more than six years ago from Hawaii in which I outlined my case for serious problems looming at that time). However, I do want to relay some preliminary thoughts, especially on the Fed chairwoman nominee, Janet Yellen.

During her testimony to the Senate banking committee last week, I was literally riding the exercise bike in the fitness center at Sandy Lane (yes, I realize that it’s a bit deranged to be watching Bloomberg TV while working out on vacation). Nevertheless, several things struck me about her comments, which were reinforced by a summary I read the next day from Jones Trading’s diamond-cutter-sharp Mike O’Rourke. One was her naiveté, intentional or unintentional, about the financial markets. For starters, she referred to stocks as being reasonably valued based on their “price-to-equity ratios.” It’s possible that’s what she meant, but it is a much less widely used metric than price-to-earnings ratios.

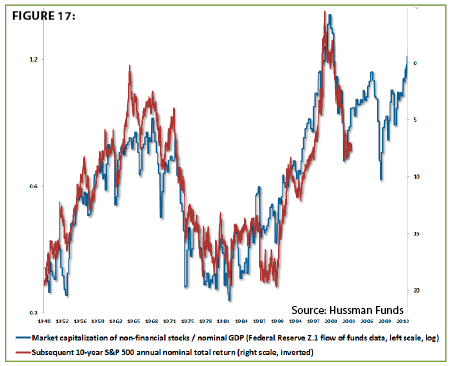

Even chalking that one up to a verbal fumble, what is more concerning is that she made no attempt to discuss peak profit margins, or any kind of adjustment for their cyclicality, in justifying her belief that stocks are not overpriced. There was also no mention of comparing total market value to the size of the economy, which, as you can see below, has had a remarkably accurate linkage to future returns (logically, high value-to-GDP ratios have preceded low returns and vice versa; note that the right-hand return scale is inverted). Obviously, this measure is currently soaring into the danger zone.

Instead, Ms. Yellen relied on the Fed’s tried but not very true “equity risk premium,” which compares unadjusted P/E ratios (not price-equity ratios) to interest rates. In addition to the just mentioned flaw in using peak earnings in this calculation, it is also flattered by interest rates being unusually low, a direct consequence of Fed actions. Beyond that deficiency, the reality is that the equity risk premium has had very little predictive value when it comes to future market returns.

Of course, that hasn’t prevented the Fed from sticking with it anyway. Just like with QE, the Fed won’t let something trivial, such as overwhelming evidence of ineffectiveness, get in the way of its game plan.

See no bubble, hear no bubble, take two. Ms. Yellen’s remarks caused me to peddle even more furiously when she omitted any mention of what’s been going on with the latest “Nifty Fifty” stocks, i.e., Amazon, LinkedIn, Facebook, Tesla, Netflix, and the rest of that high-gloss collection. Apparently, 100 plus P/Es on companies with massive market capitalizations doesn’t pop up on the Fed’s radar as a speculative warning flag, in an eerie echo of its obliviousness to the tech bubble 13 years ago. Moreover, 1999-type valuations are also popping up in the biotech space, where the Bloomberg index for this sector is trading at a rather generous 174 times earnings. At least the Financial Times is taking note, per the following recent headline.

![]()

She also made nary a mention of what’s transpiring in credit markets, which are looking, at least to me, in ever greater need of a rabies vaccine. For example, so far this year, nearly $500 billion dollars in loans have been extended to highly leveraged companies (aka, junk credits), with over half of these being the loosey-goosey “cov-lite” variety, per Point to Ponder #2.

Nor did she touch on the fact that CCC-rated bonds, definitely among the junkiest of junk, are yielding a mere 7.75%. Lest you think that sounds pretty good in an era of yields gone missing, please be aware that, historically, 50% of bonds with such a lowly rating default within three years—about a 17% annual bust rate. Even allowing for a 50% recovery through bankruptcy, a downward adjustment of roughly 8.50% should be made to the superficial yield to approximate the true return. In other words, this is a classic example of investors accepting return-free risk. Yet, in today’s wonderfully risk-tolerant world, the money keeps rushing toward the dodgiest credits.

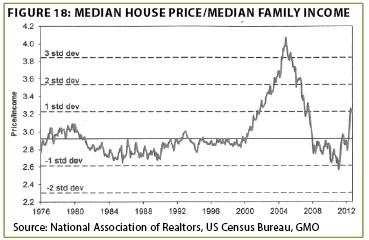

She also neglected to mention that even housing might be overheating again after years of exceptionally lax monetary policies. As you can see, relative to median family income, home prices have rarely been so spendy (though certainly not on the same exorbitant plane as property values on that lovely West Indies isle we just returned from, where multi-million dollar homes are a Barbadian dime a dozen).

Further, Ms. Yellen did not bring up, nor did I hear or read of a senator asking her about, the Wall Street Journal op-ed article that ran just the day before her congressional appearance. It was authored by the individual once in charge of investing the Fed’s fabricated trillions, and was provocatively titled “Confessions of a Quantitative Easer.” In case you missed it, his “confession” was a searing indictment of the impotency of QE to help the real economy.

On that score, given that the explicit intention of the $2.5 trillion (and counting) QEs was to elevate asset prices to boost spending and, eventually, employment, the facts strongly suggest mission unaccomplished. (At least the failure on the labor front was conceded by Ms. Yellen when she admitted the real unemployment rate is 10% or higher.)

As I’ve expressed in the past, there is no doubt Janet Yellen is one smart lady. Similarly, Ben Bernanke, her soon to be former boss, has a Mensa-like IQ, as does his predecessor Alan Greenspan. And, just maybe, that’s a big part of the problem.

Strangling the golden goose. Returning to the opening theme on simplicity, it doesn’t take someone with the brilliance of the aforementioned trio to realize there’s not much simplification going on these days, and that includes Fed policies. While I haven’t read them personally, I have perused summaries from trusted sources, including from my good friend and Fed-watcher extraordinaire, Grant Williams, of two new exhaustive (and exhausting) Fed studies that were unveiled earlier this month at the IMF’s annual research conference.

These treatises, from senior Fed staff members, are replete with mind-bending syntax such as this gem: “Optimal policy should become even more accommodative if the central bank did not target the unemployment gap but instead aimed at keeping the employment-to-population ratio near the trend level that would prevail in the absence of hysteresis effects and exogenous (but ultimately transitory) shocks to the natural rate.” Surely, you get that? More likely you’re thinking, surely you jest!

Yet, buried within the inscrutable Fed-speak is one phrase that jumps out with clarity: “…even more accommodative.” But, what seems to be different about these studies, which, apparently, are receiving thumbs-up from the current Fed Caesar and his successor-in-waiting, is the admission that a taper does need to occur soon. Yet, the authors are acutely aware of the threat to the economy posed by the rate run-up since taper talk first surfaced last May. Thus, they are proposing new drugs to keep at least the bond market anesthetized once the withdrawal process begins, such as keeping short-term rates close to zero late into this decade.

Essentially, these are exceedingly complex documents, drafted by folks who have spent their lives cloistered in the rarefied world of academia, and comprehensible almost exclusively to them. Sadly, what seems to be consistently lacking at the upper levels of the Fed, with a few exceptions, is private sector experience and that most precious of all policymaking attributes—common sense.

Perhaps an even more pressing illustration of excessive complexity, and its deleterious implications, is Obamacare. Like many others, I’ve previously warned of the threat it poses to business confidence and full-time hiring despite my personal preference to see universal healthcare. It’s been my view that Obamacare is almost certain to be a disaster in no small part due to its bloated and confusing design. The legislative document is 2000 pages filled with techno-jargon and, from the numerous articles I’ve read, an utterly baffling array of rules and regulations. (Any guesses on how many of the senators and representatives who voted for the ACA actually read it? Zero strikes me as a reasonable answer.)

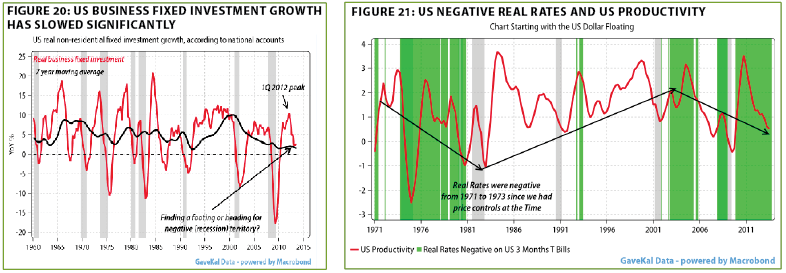

Unfortunately, the seemingly endless QEs and Obamacare are just two of the more salient examples of governmental overreach. The reality is that hyper-interventionism and bureaucratic proliferation are crushing the private sector. To back this statement up, over the past seven years, the US has fallen from 23rd in the world to 80th in terms of regulatory burden according to The Economist. Is it any wonder the largest companies are electing financial engineering over real engineering? As a result, capital spending is in a long-term downtrend, as is productivity, both of which portend very poorly for returning to our normal growth rate, regardless of the Fed’s vain—and even counterproductive—attempts to print our way to prosperity.

This is a theme I’d like to develop more fully in the weeks ahead, but one of my uber-worries is that while the Fed has created a raging bull market in stocks, with very little positive benefit to the real economy, there has been a concurrent, hyperventilating bull market in complexity. It’s my fear that the latter will overwhelm the former at some not-too-distant future date. A highly complex system is a highly fragile system. And that is a total disconnect with a stock market that is as pricey as a two-week vacation at Sandy Lane.

IMPORTANT DISCLOSURES

This report is for informational purposes only and does not constitute a solicitation or an offer to buy or sell any securities mentioned herein. This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. All of the recommendations and assumptions included in this presentation are based upon current market conditions as of the date of this presentation and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. Information contained in this report has been obtained from sources believed to be reliable, Evergreen Capital Management LLC makes no representation as to its accuracy or completeness, except with respect to the Disclosure Section of the report. Any opinions expressed herein reflect our judgment as of the date of the materials and are subject to change without notice. The securities discussed in this report may not be suitable for all investors and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. Investors must make their own investment decisions based on their financial situations and investment objectives.