“Our task now is to implement intelligent policies to contain future bubbles and credit binges, and to make sure that those that do occur inflict a lot less damage on the economy. Next time I hope we can say, we did see it coming, and we did something about it.”

-JANET YELLEN, Federal Reserve Chair, from a 2010 speech

Picking up millions in front of a steamroller. Warren Buffett is famous for his disdain of “investment strategies” that involve making small gains while taking big risks, even if those risks rarely erupt. He has described this approach using the above analogy, although he has said “pennies” instead of “millions”. In today’s $28 trillion US stock market, however, “millions” is a much more appropriate word.

The classic case of this is one of the most in-vogue tactics for churning out profits in a market environment where central banks have convinced investors that downside risk has been made an artifact of history. It involves selling volatility. Many EVA readers might not realize that even the average Joe or Jane can play this game thanks to—naturally—exchange-traded funds (ETFs).

There are several short volatility ETFs and these have become some of America’s most actively traded “securities”. At one point this summer, the short VIX ETFs, as they are known, were up 100% on the year. These vehicles profited from the “roll” on the volatility futures contracts. In layman’s terms, this means that to sell, for example, the September VIX contract in order to buy the December contract, you have to pay a materially higher price to maintain the position out another three months. In this case, the insurance pays off should the market crash. But for someone seeking to protect their stock portfolio by purchasing the “VIX”, and rolling it quarter after quarter, it is very expensive risk mitigation.

On the other hand, for those brave souls betting that the Fed and its overseas counterparts will continue to levitate stock prices, this is money from heaven. Instead of paying out expensive premiums, they are on the collecting side of the deal. And, as indicated by the above 100% gain number, collect they have.

The New York Times recently ran a story on page one of its business section recounting the tale of a former Target middle manager who quit his day job to focus on selling volatility (VIX) insurance full-time. According to the article, this intrepid individual has parlayed $500,000 into $12 million in a few short years. (Like I said, millions not pennies.)

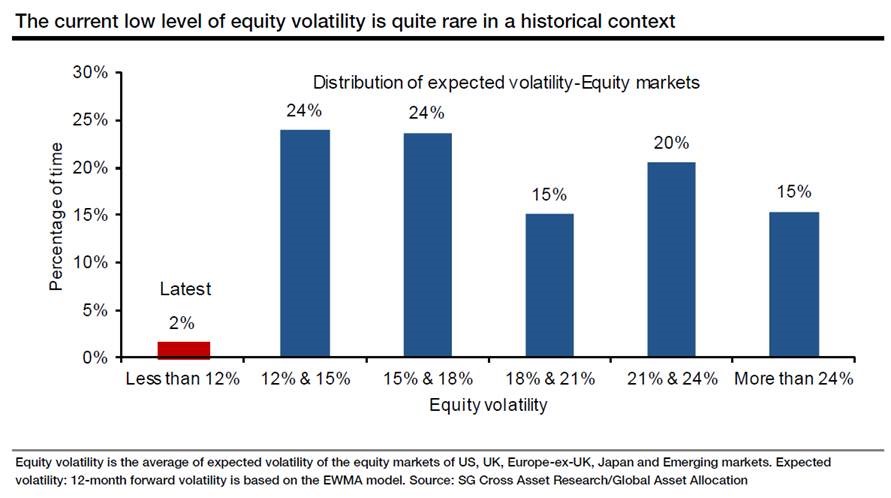

Needless to say, this central bank-anesthetized environment has been nirvana for sellers of volatility. The below chart drives this home with LED clarity (actually, these days that should be OLED clarity, as in Organic Light Emitting Diodes, the sexy new technology behind Apple’s iPhone X). In fact, since the end of 2010, the “long” VIX has vaporized by 99.6% (thank goodness for that last 0.4%!) while the short VIX has returned a fortune-making 681%! Also, unsurprisingly, short interest on the VIX has gone ballistic.

If you think this is all just a bit too easy, and a potentially highly destabilizing phenomenon, Evergreen couldn’t agree more emphatically. At some point—and we have no idea when—something is going to shatter the current paradigm of exceptionally suppressed volatility. When it does, those such as the erstwhile Target manager and, particularly, legions of hedge funds who have been trying to prop up their lagging performance by playing this game, are going to suddenly have to cover their shorts.

Maybe the short volatility trade can unwind without systemic reverberations but there is a closely-related concept that is unlikely to go quietly into the night. This is the similarly obscure Value-at-Risk (VAR) formula that many mega-financial firms use to determine how much exposure they have in their own portfolios to market fluctuations. The lower volatility goes, the more risk their computers tell them they can incur. But when volatility surges, their systems force them to sell stocks. Consequently, this has the potential to be highly reminiscent of the portfolio insurance debacle that greatly accentuated the market crash thirty years ago next month.

As John Maynard Keynes noted some 70 years ago, “When the capital development of a country becomes the by-product of the activities of a casino, the job is likely to be ill done.” It’s not a leap of faith to believe that if Mr. Keynes were alive today, he would be feeling very ill indeed.

Rotation, rotation, rotation. One of the ultimate real estate axioms is “location, location, location”. These days, in the US stock market, if you replace the “l’s” with “r’s” and the “c’s” with “t’s,” you’ve nailed what has been going on lately.

For those of us who remain convinced it’s just a matter of time until the folly of the world’s central bankers is exposed, with US equities being a probable victim, there is a tendency to want to sit back and not touch stocks. But that’s been a mistake as the market has done its slow-motion melt-up in recent years. The reality is that below the surface calm and superficially steadily rising prices, there has been enormous damage done to many industry groups and stocks during 2017. In some cases, the plunges have been 50% or more.

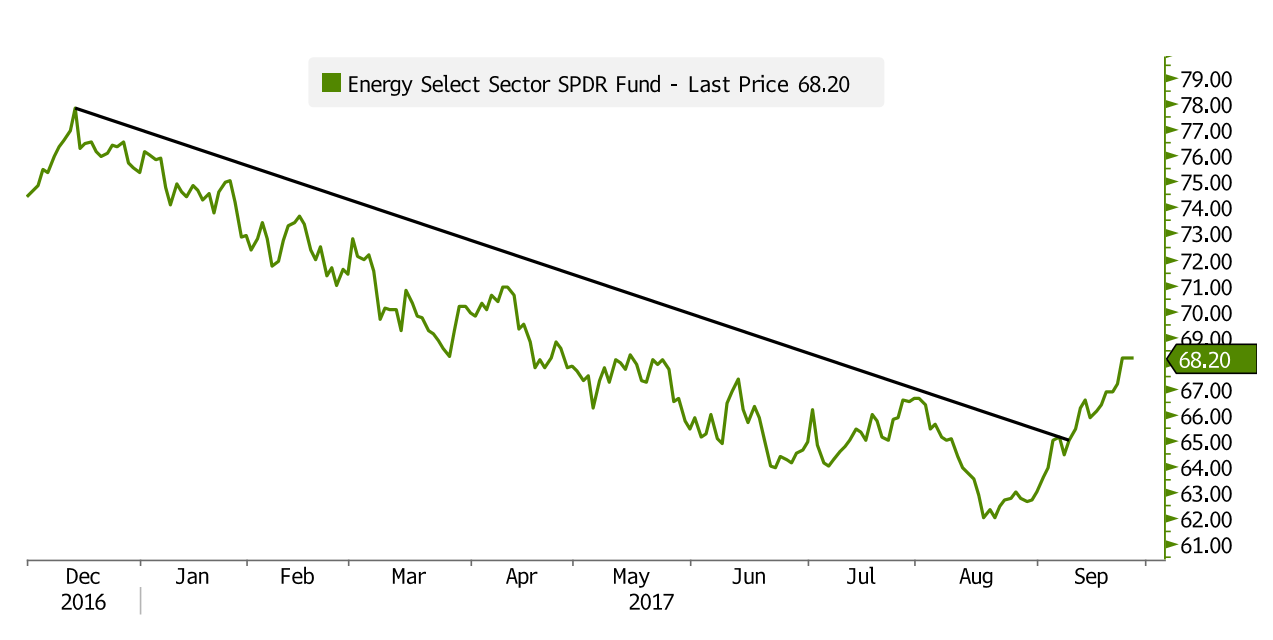

Consequently, this year has been one of the best profit-making environments we’ve seen since the market dislocations during the summer of 2015. As these pages have often noted in recent months, energy has been a prime example. The sector got slammed starting in February, after its snappy rally that followed the 2014/2015 bloodbath. Predictably, once energy stocks were on their heels this summer, the nattering nabobs of negativity seemed to be everywhere.

Also, as usual, Jim Cramer jumped on the bandwagon, warning one caller on his Mad Money show not to touch even the strongest master limited partnership, despite its high and rising yield and depressed price. Yet, per the below chart, you can see there is something up—literally—with energy lately, even though that revival hasn’t helped MLPs much so far.

The opportunities, however, have extended well beyond energy. Unsurprisingly, retailers of all stripes have been taken to the wood shed—and then back again…and again…and again. The prevailing attitude, of course, is that Amazon will take over every nook and cranny of the consumer-facing space—or at least destroy profitability for all brick and mortar retailers as it encroaches on their turf. As with all popular market “memes”, there is logic in this mindset. Yet, as also is often the case, the belief has been taken to such an extreme that it has created some exceptional profit-generating situations. One of the retail names that we recently acquired has a strong online presence and a resurgent product line.

Restaurants, while they are a form of retailing, are obviously not stores and their travails are hard to blame on Amazon. Yet, even many of the strongest dining-out brands have been poleaxed. This seems at odds with the widespread view that the US consumer is in husky shape. Since Evergreen disagrees with the cheery consensus—and, in fact, believes American households are increasingly stressed—we’ve only kicked some tires in the space. But it is undeniably cheap.

Then, there are the media stocks which haven’t been cut in half but have been under significant downward pressure, nonetheless. For example, The House of the Mouse, arguably the finest franchise in media, has been languishing down 20% from its 2015 high, and is trading at a P/E ratio below the overall market. Other blue-chip content names are down as much as the bombed-out retailers.

But there are several other “nichey” areas like maritime and metallurgic coal stocks that recently traded so cheap that they were irresistible despite our overall market concerns. Some of these have already staged comebacks worthy of the New England Patriots in last year’s Super Bowl.

The common theme among these companies is that they are very seldom represented in the most heavily-owned exchange traded funds (ETFs). For those hardy contrarians, willing to venture into the ETF-neglected wilderness, the bargains are aplenty.

The Year of Living Undangerously, Redux. REALLY long-time EVA readers will hopefully forgive me for re-using this section title but it seems appropriate as we begin to anticipate the market atmospherics in 2018.

After the seeming eternity of this bull cycle, it’s reasonable to wonder what could possibly go wrong next year. In our view, it comes down to money, or, more precisely, the impending absence of trillions of monetary amphetamines. As noted in some recent EVAs, the litany of excuses for why this bull market should continue indefinitely is a long one. But, to cut to the chase, we believe those are mostly flimsy save for the intersection of a shrinking number of shares outstanding—due to both buy-backs and take-over activities—and over $10 trillion of high-powered money injected by central banks.

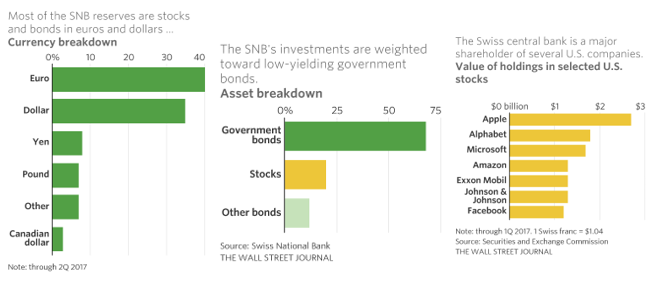

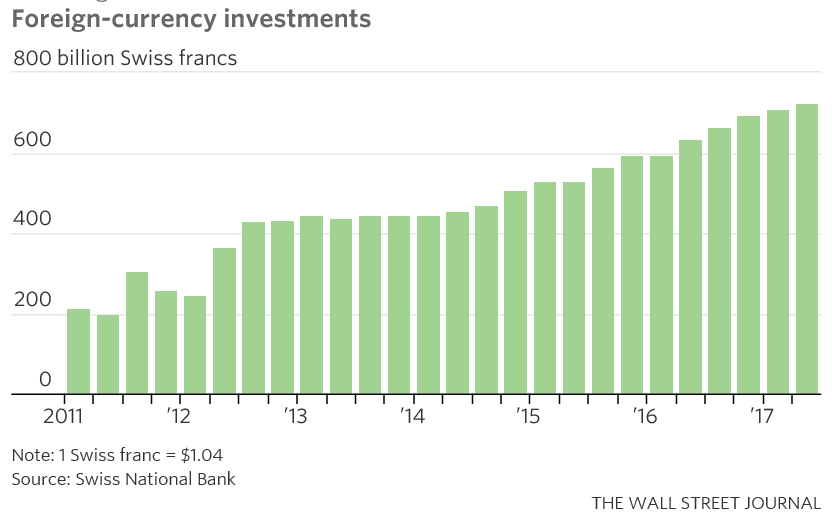

We doubt most ordinary, non-market minutiae obsessed folks (i.e., as opposed to those of us at Evergreen) realize how much “QE”—formally known as Quantitative Easing—has been injected into the global financial system this year. But, in case you are in the sane majority, through the first half of this year that sum broke all prior records (at least on an annualized basis). And, as we have pointed out before in these pages, what the once circumspect Swiss National Bank (SNB) has done is truly staggering. (Note that the “foreign currency investments” shown below have been totally funded by digital money the Swiss have created out of Alpine-thin air.)

At the start of 2017, Evergreen was among the few research/money management entities to be forecasting that the Fed would not only hike rates multiple times but that it would also begin to unwind its three rounds of QE. It was, as usual, a most renegade viewpoint but it’s now considered to be a given. Lately, the once low odds of a December rate hike, which would be the third of the year, have zoomed to 70%.

As is typical of this timid Fed’s modus operandi, the balance sheet shrinkage has been well telegraphed and it will begin at a modest pace of just $10 billion per month. Out of the Fed’s $4.5 trillion treasure trove of government bonds and mortgages (all acquired with money it created from its computers, just like the Swiss) that is truly a pittance. But if they stay true to their plan, by next year this will be running at a $50 billion monthly rate, or $600 billion annualized. In other words, by then we’ll be talking some serious dough.

Concurrently, other central banks are moving the Fed’s direction. The Bank of Canada has raised rates twice already with more looking almost certain. The Bank of Australia is rumored to be considering rate hikes as is the once devoted QE-practitioner over in London, the Bank of England.

As you will hear in next week’s EVA, my partner and great friend Louis Gave makes a persuasive case that as 2018 matures, it will only be the Bank of Japan that is still QEing. And to the extent they are, that is likely to be offset by the Fed’s QTing (as in, Quantitative Tightening).

In other words, ladies and gentlemen, the financial markets are likely going to have to go cold turkey in the not-too-distant future. If so, leveraged investors—and all of those volatility sellers—might need to have on hand a healthy supply of Wild Turkey.

Thrown for a curve? Forecasting a rise in treasury bond yields at the start of each year has become as much of an annual ritual as post-holiday weight-loss resolutions. And, for years now, they have had just about as much staying power. 2017 has been no exception.

As outlined in our January 20th EVA, Wall Street strategists and money managers were nearly unanimous in their belief that longer-term treasury rates would rise this year. Since Evergreen was among the more aggressive Fed rate-hike forecasters, it would have been logical to assume we would be in the higher bond yield camp, too.

Yet, as we described in our March 17th “Fed Storm Rising” EVA, we felt we were looking at a classic Fed tightening cycle that would likely begin to flatten the yield curve and, eventually, invert it (in simpler terms, this means that short-term interest rates would begin converging with longer rates and possibly rise above them, creating a so-called yield curve inversion).

Part of our rationale for this oddity of rising short rates and stable-to-falling longer yields was based on the last Fed tightening campaign from 2004 – 2007 when nearly all the yield increase happened before our central bank had raised its overnight rate even once. However, our contention was also derived by observing that Treasury yields had essentially doubled from their Brexit lows in the summer of 2016 (around 1.35%) before the Fed implemented its second rate hike last December. Whatever the reasons, the reality is that going back to last December we’ve had three rate increases and yet yields on the 10-year T-note have declined.

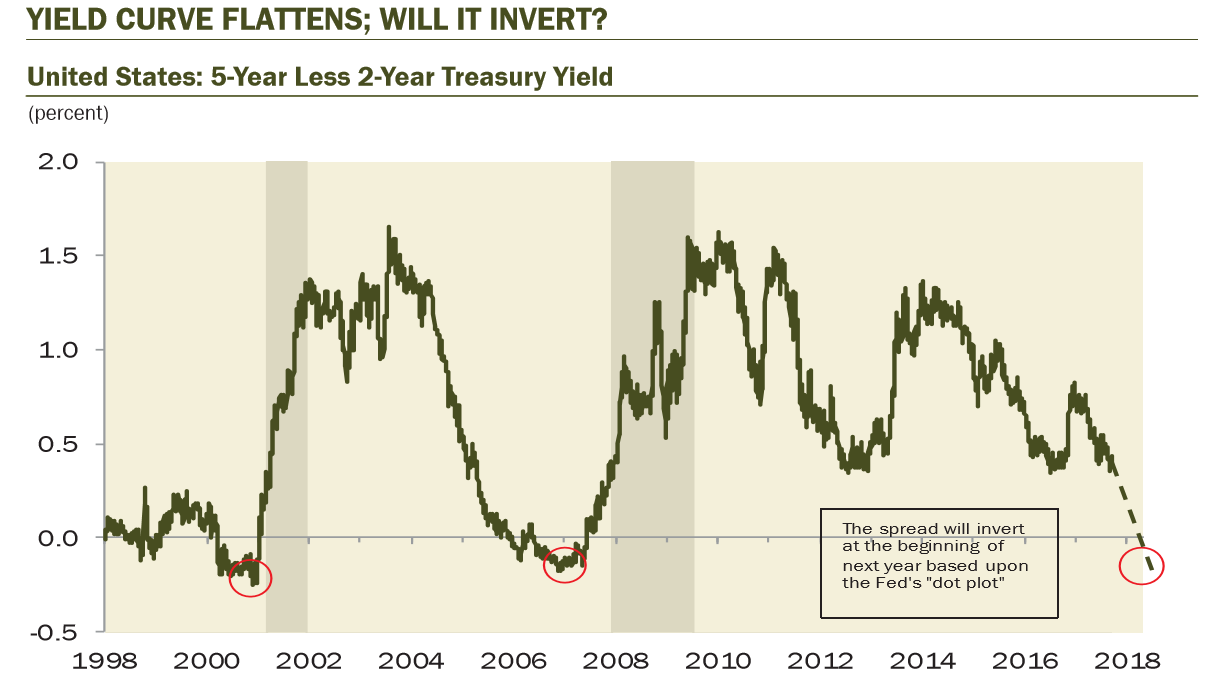

Since the last hike in June, we haven’t had any further rate bumps but, as noted in the previous section, another looks extremely likely in December. Moreover, the Fed is indicating a total of four more hikes over the next fifteen months. Therefore, unless 10-year treasury note yields rise a decent amount, we will be looking at a very flat yield curve. If they decline, as they often do late in a Fed tightening cycle, we could actually see the dreaded inversion. (The reason this development is so unwelcome is that the anomaly of short rates above long yields consistently leads to recessions.)

On Monday, one of the few economists who anticipated both the housing bust and the severe recession of 2008, David Rosenberg, wrote these words: “With the two-year T-note testing 1.45% last week, a cycle high, we may be on the precipice of the Fed starting to invert parts of the Treasury yield curve, with obvious economic implications.” David also created the below chart showing how much the rate differential between the 2-year and the 5-year T-note has already come in, with his projections of an actual inversion occurring early next year based on the Fed’s “dot plot” (its projection of future rate increases).

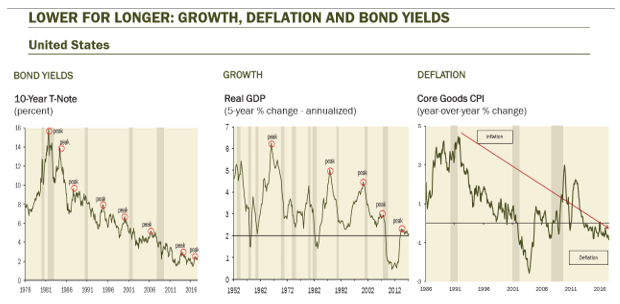

If longer treasury yields don’t go much higher than where they are now, it would mean that for this cycle they topped out at 2.6% on the 10-year note. This would maintain the pattern we’ve seen for over thirty-five years of successively lower peaks by long-term treasury rates (starting at 15.84% in 1981, then 13.84% in 1984, 8% in 1990, 6.8% in 2000; and 5.2% at the apex in 2007).

The following charts, also from David Rosenberg, give you a very concise illustration of this downwardly sloping yield peak pattern, as well as why it has played out this way thanks to the persistent downtrends by both real GDP and inflation.

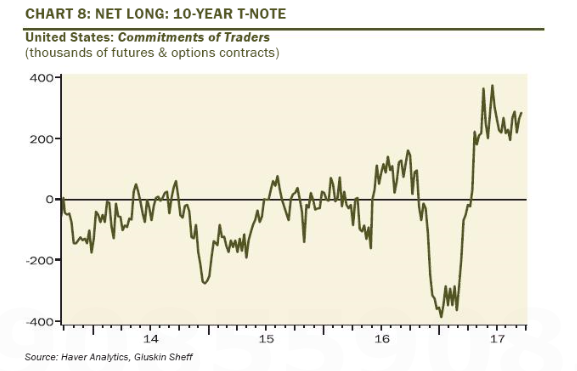

It’s certainly possible that the yield curve won’t invert, particularly if longer rates take flight. Frankly, we think in the very near-term we could see some temporary steepening with the 10-year T-note moving back up to 2.5% to 2.6%. It’s unquestionable that speculative positioning on treasuries became too bullish right around the time yield bottomed close to 2% in the late summer, per the following chart (and note what a great buy signal was produced early in the year when speculators were the most bearish they had been in years).

But, if so, we think that level will be tough to sustain and we seriously doubt we will see yields on the 10-year rise as high as 3%. The reason is that the US economy already looks shaky and higher rates will only further inhibit growth.

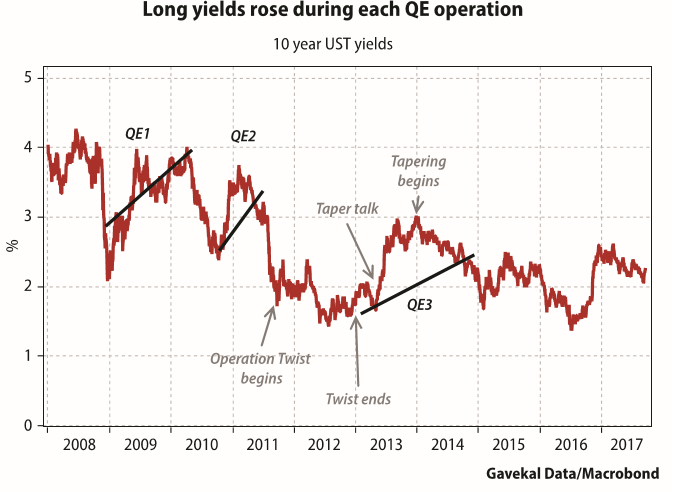

For those who doubt this relatively limited rate upside scenario, particularly with the Fed preparing to launch Quantitative Tightening (QT), please realize that during each of its earlier QEs I, II, and III, interest rates actually rose. In other words, they did the opposite of what the Fed was trying to achieve. Then, once our central bank’s buying binge was over, yields declined again.

So, good reader, should bonds sell off in the weeks and months ahead, creating widespread bearishness such as we saw early this year, be prepared to do some serious buying of high-grade long-term bonds. The likelihood is that yields will plunge again during 2018 at the same time that the Fed has jacked up short rates even further. That’s exactly how we have wound up with inverted yield curves in the past...and, no, we don’t think this time is different.

David Hay

Chief Investment Officer

To contact Dave, email:

dhay@evergreengavekal.com

OUR CURRENT LIKES AND DISLIKES

Changes highlighted in bold.

LIKE

NEUTRAL

DISLIKE

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.