As I hope all EVA Positioning Recommendation (PR) recipients are aware, our normal Evergreen Virtual Advisor newsletters are being switched out for the publication of my book “Bubble 3.0” via the increasingly popular financial social media service, Substack. If for some reason you are not getting the email links to it, please let us know right away.

Because of our “Bubble 3.0” series, we haven’t been publishing our monthly Guest EVAs. Accordingly, I thought it would be a good idea to run one in lieu of my normal EVA PR commentary.

One of my favorite Guest EVA sources is the author of the Downunder Daily, Gerard Minack. In this missive, he’s making the case that the recent market weakness is a correction not the start of a bear market. It’s a view with which I totally concur though I would make the distinction between my long-belittled COPS (Crazy Over-Priced Stocks) and those that are reasonably valued relative to their potential growth rate. Per numerous past EVAs, the COPS have been absolutely crushed in recent months. Unfortunately, many of them still have considerable downside.

As you will soon read, Gerard’s caveat about this being a correction and not the start of something far more ominous relates to the twin geopolitical risks of Russia/Ukraine and China/Taiwan. Based on the news on the former crisis, this risk may be in the process of being actualized. However, another emerging risk is an increasingly cracking long-term treasury bond market. As of yesterday, the 10-year T-note broke above 2%. Should this rate rise continue, and particularly if the 10-year treasury sprints toward 3%, the stock market is likely to come under some serious pressure. Hopefully, you are aware that long-term treasuries have been consistent cellar-dwellers in our Likes/Neutrals/Dislikes section, a stance that continues to be validated by market action.

The bottom-line: there are some intriguing bargains out there in the US stock market but keep some buying power in reserve based on what could turn into a bond market riot.

Assume it’s a correction, unless geopolitics blow - Gerard Minack

My base case is that we are in a vanilla market correction. It’s difficult to play because everything – even ‘safe’ assets – are expensive, so there are few refuges. However, broad-based equity bear markets normally don’t happen until investors sniff recession. I don’t think that that is the case now. However, the fact that bond yields are now starting to fall suggests something has changed. My hunch is that geopolitical risks are driving a safe haven bid. If – and it is an ‘if’ because I have no edge on politics – these concerns fade, upward pressure on rates will return while equities should be able to start an uneven recovery and out-perform bonds.

A few thoughts:

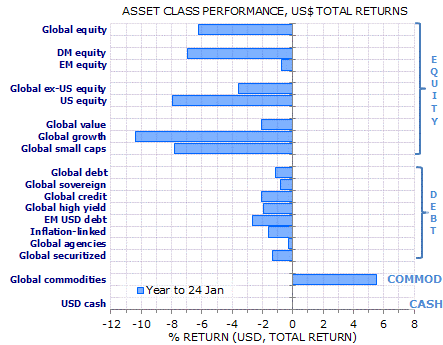

It’s hard to find somewhere to hide in a correction when everything looks expensive. Every major asset class is down year to date, commodities excepted (Exhibit 1).

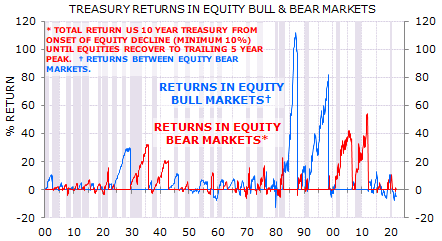

This is a problem that won’t go away. Through the long bond bull market Treasuries offered great protection when equities weakened and generated reasonable returns when equities were rallying. This has now changed. Treasuries now tend to lose money when equities are rallying, while the returns in corrections are modest (Exhibit 2). In short, Treasuries were a highly effective insurance policy that used to pay the policy holder, but now are a less effective insurance that cost the policy holder.

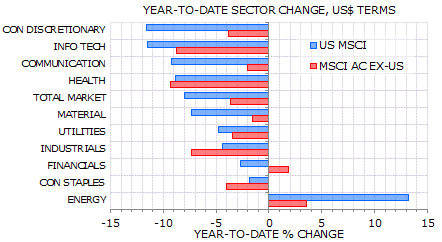

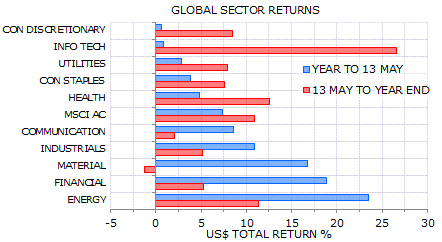

Even though there’s a broad-based equity correction underway, relative performance reflects a reflation bias, both at the regional level and the sector level. Exhibit 3 shows year-to-date sector performance. Cyclical sectors may be falling, but they’re falling less than the overall market. This is circumstantial evidence that concerns about the economic outlook are not driving the equity sell-off.

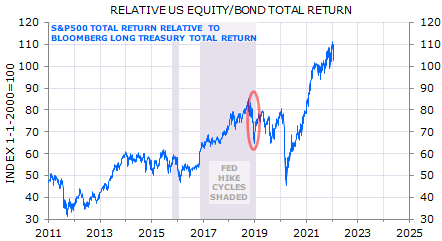

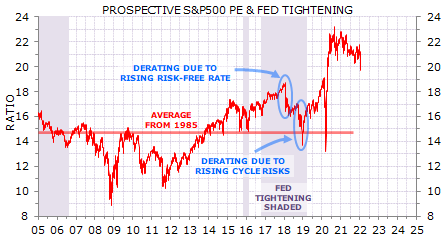

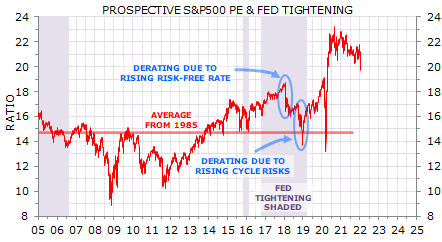

If this is a vanilla correction, then I think it’s right to expect that equities will out-perform bonds once markets settle. This is the typical pattern through Fed tightening cycles (Exhibit 4).

It is when bonds start to rally that the market is signaling a deeper distress. As an example, the last tightening cycle in the US went through two distinct phases. Initially equities de-rated while bond yields increased – a standard response to tightening. But a second derating occurred as bond yields started to fall, signaling market concerns about recession risk (Exhibit 5). That coincided with a sharp fall in equity returns versus bonds (circled in Exhibit 4). Next was the Powell pivot, which averted recession.

Even a less dramatic change in long end yields can be important for equities. The rise in long yields in the first third of last year coincided with strong out-performance by reflation beneficiaries. Once yields started to soften, the pattern of relative performance reversed (Exhibit 6).

As I’ve noted before, I will be watching the direction of long-end yields this year to ensure that the structural reflation trade remains intact. With central banks starting to tighten, I don’t expect yields to switch direction as they did last year.

However, it is noteworthy that long-end yields have fallen over the past four sessions, the US 10 year by almost 20 basis points. I don’t think that that decline reflects rising recession concerns. Markets look ahead, but it would be remarkably farsighted – implausibly farsighted – for bonds to be rallying now on the prospect of a downturn caused by a Fed tightening cycle that is yet to commence. My hunch is that the safe haven bid is due to rising geopolitical concerns. If – and it is an ‘if’ – those concerns blow over, then I would expect upward pressure on long-end rates to resume.

On the other hand, if the situation in eastern Europe deteriorates then this could be a deeper correction, particularly if there was a major energy supply shock. The silver lining would probably be a delay in planned monetary policy tightening.

One final point: while I expect moderate equity gains this year – despite the prospect of Fed tightening – the big story in equities will likely be a change in leadership. The stocks or sectors investors are rotating away from may face significant losses. In the TMT boom and bust the S&P500 was near its highs just before the recession started, while the NASDAQ had experienced a severe de-rating bear market. Meanwhile the rest of the market eked out reasonable gains (Exhibit 7).

Positioning Recommendations

Once again, it’s the bond market that was the big news this week. As I have been anticipating, the 10-year T-note yield has risen to 2%, even breaking slightly above that level. This is putting downward pressure on the interest rate sensitive segments of the stock market such as REITs, homebuilders and utilities. For months, speculative sentiment (basically, hedge funds) has been extremely negative on bonds. Additionally, retail investor exposure to bonds is very low. Generally, this type of broad bearishness typically leads to consensus-surprising rallies. However, in my experience when a particular asset class—like bonds, in this case—continues to sell off in the face of such bearishness it’s a sign of significant underlying weakness. As I’ve repeatedly pointed out, even as longer- term treasuries have been pounded over the last year and a half—with 10-year yields rising from 0.50% to over 2%--they still “offer” a deeply negative yield after inflation. Jeffrey Gundlach, the King of Bonds, was on CNBC today saying that he believes the 10-year will “take a peek” at 3% at some point this year. (He also believes inflation will remain over 5% this year, much higher than the “Street” is forecasting.) If he’s right, that has ominous implications for those stocks still trading at lofty valuations. Once again, if you’re a growth investor, I’d strongly recommend sticking with the GARP (Growth At a Reasonable Price) names. Many of these have become even more reasonably priced lately.

LIKE

When resource-related stocks have been spanked recently, I’ve suggested taking advantage of the softness. Specifically, I called out the sharp sell-offs in America’s largest copper producer and, more recently, in the largest publicly-traded uranium producer. Based on healthy bounce-backs over the last couple of weeks, being less bullish is appropriate.

NEUTRAL

Yields have also surged on short-term treasuries. As a result, these have become more attractive though not enough to justify an upgrade to buy status.

DISLIKE

As I write these words, stocks are falling sharply and oil prices have vaulted on media reports that Russia is preparing to invade Ukraine. Further, a White House press conference is warning that an invasion may be imminent. If that happens, the US dollar is likely to shoot up. However, I continue to feel the odds strongly favor it will be, over time, a victim of the absurdly over-stimulative US policies of the last 18 months. In other words, diversify out of US dollar-based assets on any price spikes caused by geopolitical crises.

DISCLOSURE: This material has been distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, are subject to change, and reflect the personal opinions of David Hay (an employee of Evergreen Gavekal) as of the date of this publication. This publication does not necessarily reflect the views of Evergreen’s Investment Committee as a whole. All investment decisions for Evergreen clients are made by the Evergreen Investment Committee. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed, and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this letter have been selected to illustrate the author’s investment approach and/or market outlook and are not intended to represent Evergreen’s performance or be an indicator for how Evergreen or its clients have performed or may perform in the future. Each security discussed in this letter has been selected solely for this purpose and has not been selected on the basis of performance or any performance-related criteria. The securities discussed herein do not represent an entire portfolio and, in the aggregate, may only represent a small percentage of a Evergreen’s client holdings. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time. Before making an investment decision, the reader should do their own research and/or consult with their financial advisor. Past performance is no guarantee of future results. All investments involve risk, including the loss of principal.