"Retail is not dead; it is changing."

-MATT FASSLER, Managing Director, Goldman Sachs

Please see important disclosures following the piece. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.

In one of the most surprising plot twists in e-commerce history, technology giant Amazon.com piloted a physical bookstore concept in late-2015. Dubbed Amazon Books, the retailer, which started as an online store to compete against the likes of Barnes & Noble and now-defunct Borders, entered the same brick-and-mortar space that many argue they are helping destroy.

More recently, Amazon surprised with their purchase of grocery-chain staple Whole Foods. While we won’t spend much time detailing the implications of the purchase, the undeniable fact is that the line between physical and digital retail is more blurry than ever. As traditional retailers are attempting to make an e-commerce push and e-commerce players are opening (or buying) brick-and-mortar stores, it begs the question: what are we to make of all this as consumers and investors?

Last week, we heard from Erik Nordstrom on the future of retail in Retail Realities (Part I). In Part II of this two-week series on the topic, Evergreen will take a closer look at the evolution of retail up to this point, before examining what retail might look like in ten years and summarizing some of the potential winners and losers in the space.

As noted last week, the reality facing the retail industry is that it has and will continue to evolve. Acclaimed investor Warren Buffett even spent his precious time weighing in on the topic at Berkshire Hathaway’s annual meeting earlier this year, stating, “The department store is online now… I have no illusion that 10 years from now will look the same as today, and there will be a few things along the way that surprise us. The world has evolved, and it’s going to keep evolving.”

This evolution has given many retailers a tremendous opportunity to rethink how they engage with their customers in a hyper-connected, digital world, while leaving others that are slower to adapt in the dust.

Some companies that we believe have been successful at developing new strategies to reach their customers so far are Wal-Mart, Home Depot, Costco, T.J. Maxx, Nordstrom, and Best Buy. These businesses have reimagined their physical stores while also establishing robust e-commerce platforms to engage with consumers online. As a result, their market performance has remained (mostly) positive during a time where several other retailers are languishing near multi-year lows.

NORMALIZED RETAIL STOCK PRICE RETURNS (JANUARY 2012 – JUNE 2017)

Source: Bloomberg Finance, Evergreen Gavekal

Source: Bloomberg Finance, Evergreen Gavekal

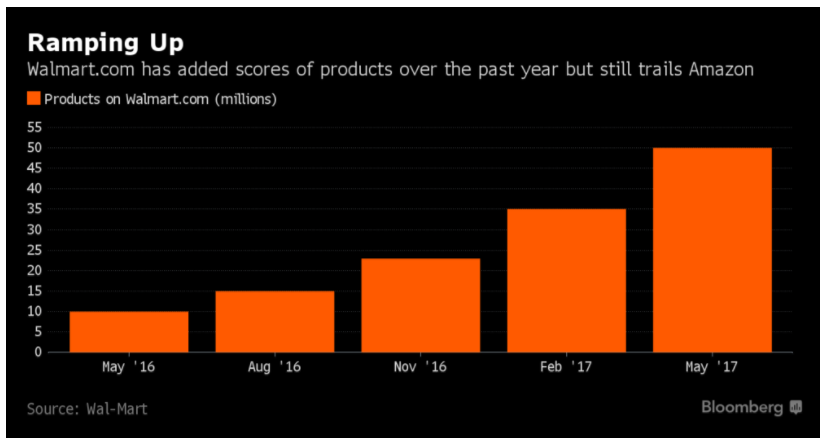

Wal-Mart, as an example, bought startup Jet.com for $3 billion last year and put its co-founder in charge of their e-commerce business in an effort to boost digital sales. The result? U.S. online sales rose a staggering 63% in the first quarter of 2017. Much of this is attributed to Walmart.com adding nearly 40 million products to their digital marketplace over the past year – on top of the 10 million products they already offered in May 2016. While this still trails Amazon’s impressive catalogue of 350 million product offerings, the gap has narrowed substantially. Additionally, unlike Amazon, which allows almost all sellers onto their platform after going through an online registration process, Wal-Mart’s marketplace is invitation-only which keeps its product offerings lower, but higher-quality, than competitors.

Source: Wal-Mart, Bloomberg

Source: Wal-Mart, Bloomberg

Alternatively, those suffering most are retailers that have not changed as quickly as technology or consumer behavior. In early May, S&P Global Market Intelligence had already tallied a record 18 retail bankruptcies, matching the total for all of 2016.

What’s equally alarming is the rate at which some retailers are closing stores nationwide. As shown in the chart below, once-proud-and-profitable brands are being forced to downsize their physical presence.

Source: Business Insider

Source: Business Insider

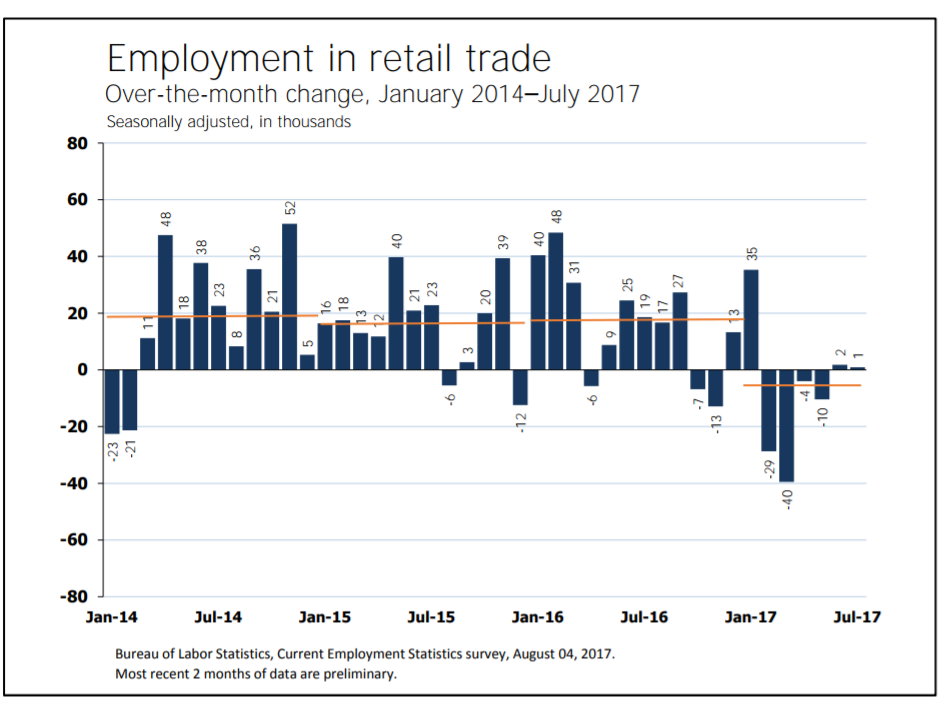

These bankruptcies and store closures have obvious read-through implications for American workers. While overall job growth remains positive, and unemployment is at its lowest since 2001, retail employees have felt the effects of this seismic shift. For example, in March of this year, the industry lost 40,000 jobs in a retail retrenchment, while most other industries (all except wholesale trade, utilities, and information) added jobs.

Altogether, the industry has lost an average of 13,000 jobs per month so far in 2017 (updated from 9,000 in the most recent Bureau of Labor Statistics publication) compared to 2016, when monthly job gains averaged 17,000. This could very well be a foreshadowing of what’s to come (and a continuation of what’s already begun): a retail revolution evolution.

Source: Bureau of Labor Statistics

Source: Bureau of Labor Statistics

As Warren Buffett alluded to, the evolution that’s underway will undoubtedly challenge the norm. While it’s impossible to forecast exactly what the world will look like in ten years, some trends in their infancy today could gain widespread adoption by 2027. Here are some conceivable developments:

In-Store Fittings, Online Delivery

The price of physical space is a significant cost to brick-and-mortar stores. Not only do businesses pay for consumer-facing storefronts, but also for the space to stock inventory. Bonobos, an e-commerce-driven apparel company that sells men’s clothing and was purchased by Wal-Mart last month for $310 million, has challenged conventional orthodoxy for both e-commerce and physical retailers.

Rather than building out large, costly storefronts, they have opened several “fitting room stores” that allow customers to try on clothes they wish to purchase online. The advantage for Bonobos is that they don’t have to worry about holding massive amounts of inventory at each storefront – they only pay for enough space to stock a select amount of clothing. The benefit for the consumer is that they can physically try on “online” apparel before making their purchase. The unfortunate kicker is that once in the physical storefront, customers cannot leave with their purchased merchandise –it still must be delivered to them.

While this model doesn’t work for every consumer, Bonobos has been successful in adapting to an online vs. offline shopping experience. In the future, retailers (specifically department stores) would be wise to consider a similar model to reduce steep overhead costs. The major roadblock for this kind of operation becoming more widely adopted is perception of the process – not many consumers want to try something on, buy it, and then wait two or more days before receiving it. But, as delivery speeds become quicker, this concern could be muted over time.

For example, take a minute to imagine a world where you go shopping, find something that you like, and purchase it in the store. However, instead of carrying around shopping bags from store-to-store, the merchandise is shipped directly to your home and arrives by the time you get there. Seems far-fetched? Maybe in today’s reality, but not in the not-too-distant future.

Lightspeed Distribution

Two-day shipping has become the standard for what consumers consider “fast delivery.” But many companies are challenging this benchmark by offering same-day (or in some cases two-hour) distribution. Amazon’s Prime Now service is an obvious example of this ultra-fast service. Another company that’s working feverishly to meet the demands of today’s consumer is Macy’s. While they have closed nearly 150 stores and seen several straight quarters of lower revenues, their partnership with Deliv, a same-day delivery company, highlights the commitment they (and many other businesses) are making to pivot towards faster standards.

One technological advancement that could change the economics of the “last mile” dilemma is drone delivery. Both Amazon (Prime Air) and Google (Project Wing) have launched test concepts to make the space-age delivery method a reality. In fact, late last year, Amazon released a video demo of Prime Air, which is designed to “get packages to customers in 30 minutes or less using unmanned aerial vehicles.” Larry Page, cofounder and CEO of Google’s parent company Alphabet, promised in his annual shareholder letter that Google’s Project Wing would make big strides this year.

Decisions by the FAA and other regulatory bodies will ultimately dictate the future of this hi-tech delivery method. However, regardless of what regulations are imposed, we should expect super-fast (at the very least same-day) delivery to become the new standard.

Mixed Reality Shopping Experience

Circling back around to Bonobos, one issue that their model seeks to address is the ability for consumers to test products before making an online purchase. But imagine a world where you could virtually assess products directly from your phone, tablet or TV.

At the Consumer Electronics Show in Las Vegas, Gap unveiled “DressingRoom”, an application that allows consumers to try on clothes virtually. Sephora has also launched an application called “Virtual Artist” that gives users a virtual, 3D experience to trying on makeup. Both examples emphasize a push towards mixed reality, or technology that blends the virtual and physical worlds.

The “limits” of this mixed reality experience are literally limitless and, like many technologies, still in their infancy. As companies push the constraints of what’s possible, and bring new experiences to consumers, the status quo will continue to be challenged. As previously stressed, this will have read-through implications for the physical retail store. While virtual or mixed reality experiences cannot completely replicate real-world experiences today, the verdict is still out on what will be possible tomorrow (let alone in ten years).

Easy, Instant Purchasing Power

One of the main value propositions for online shopping is its relative ease compared to in-store shopping. There’s no need to get in a car, walk through a mall, or put on shoes when items can be purchased with the click of a button from literally anywhere an internet connection exists. What’s scary (at least to pure-play physical retailers) is the ability to purchase anything and everything from anywhere is only growing in ease.

With the rise of voice assistants such as Google Home, Amazon Echo, Apple HomePod, Microsoft Invoke, and Alibaba Tmall Genie, consumers must only begin a phrase with “Google”, “Alexa”, “Siri”, “Cortana”, or “AliGenie” to be connected to an online wonderland full of endless, easy, and instant buying opportunities.

Greg Yevich, co-founder and technology director of e-commerce marketing firm OperationROI, recently stated, “With the proliferation of mobile devices, smart glass and smart appliances, e-commerce will become more intertwined to our future instant gratification lifestyles. Every touchpoint — from digital to TV, radio and social networks — will let shoppers complete immediate purchases on the spot.”

What’s even more mindboggling is that the rise of IoT (Internet of Things), AI (Artificial Intelligence), and the connected world could replace active shopping altogether. In other words, things would just show up when and where you want them without having to physically order a product. Seems crazy? Well, Amazon’s Dash Buttons (and more recently Dash Wand) is a step in that direction. While their product still requires an element of human touch, it brings the process of replacing everyday items easily and instantly to the forefront of the human experience.

In any industry facing this much change, there are sure to be winners and losers. The evolution that’s underway has and will likely continue to separate the two. As Erik highlighted in last week’s EVA, agility, speed, being customer-centric, increasing digital and physical capabilities, and picking the right partners will all influence this outcome. In addition to Erik’s insights, here are some potential winners and losers Evergreen sees.

Winners

Class A Malls

Class A malls, which tend to be higher-quality and more profitable than their Class B and Class C counterparts, should have an easier time retaining and attracting new tenants, leading to a decent outlook over a sustained period. Although they will still suffer traffic concerns, Class A malls are less likely to face the same mounting pressures of malls in less densely populated metropolises. While classifying Class A malls as true “winners” might be overly optimistic, the reality is that they have a greater likelihood of surviving and thriving in this evolving retail environment than other classes of malls. REITs who have concentrated investments in this class of malls look undervalued and provide a decent forward outlook.

Retailers Who Reimagine their Physical Stores and Invest in Emerging Technologies

As Goldman Sachs highlighted in a recent research paper titled The Store of the Future: Reimagining Retail in the E-Commerce Era, 85% of retail sales are still transacted in stores. In five years, at an online growth rate of 15%, this number could be closer to 70%. While the trend is significant and should not be overlooked, the reality is that the majority of commerce still happens in physical locations.

Matt Fassler, author of the aforementioned paper, summarized the importance of reimagining the physical store, stating, “those that take their fate into their own hands and play to the acknowledged strengths of the physical store by enhancing their stores should outperform those who choose to lean on legacy business practices.” One way retailers can be successful in this area is by leveraging emerging technologies and Big Data.

The reason this has become increasingly important is because we live in an information age. Consumers and online retailers have the advantage of leveraging real-time technology and data to make decisions. Winners in this space will be those who advance with emerging technologies and reimagine how to reach consumers in physical stores, in a highly data-driven world.

Trusted, Established Brands

Many trusted and established brands have experienced declining performance over the past several years. One advantage brands have against traditional physical retailers and department stores is their ability to move product without making heavy investments in physical space. Brands that form partnerships with both physical and online retailers could experience a turnaround. Winners will be brands that are trusted and established in the United States, but also appeal to international and emerging markets such as China and India.

Losers

REITs with concentrated investments in regional malls and shopping centers

Retailers have closed over 3,200 stores so far in 2017. As store closures have mounted, increased vacancy rates have led to rising costs for both redeveloping and re-tenanting properties. The implications are declining performance among REITs with concentrated investments in regional malls and shopping centers. In fact, a recent report from Cohen & Steers, a global investment manager specializing in liquid real assets, stated that REITs with investments in these areas have seen “declines of 14.6% and 11.5% respectively in the 12 months ended March 31, 2017.” Conversely, REITs that do not hold investments in these sectors have returned a positive 8.2% throughout the same period.

In their report, Cohen & Steers state that they “expect the paradigm shift taking place to dramatically alter the retail landscape, with potentially significant implications for real estate investors.” We agree with this thesis, and REITs that are highly concentrated in malls and shopping centers (specifically “Class B” and “Class C” malls) will likely continue to feel the downward effects of this trend.

Class B and Class C Malls

Class B and C malls (which represents most malls in America) will have the most trouble retaining and attracting new tenants. These malls have experienced a negative annual average growth of -3% and rental rate decline of approximately -19% since 2011. Additionally, they are facing a decrease in the average square footage being leased, from approximately 17,000 square feet to 11,000 square feet per lessee between 2010 and 2015.

Another sobering statistic is that one-fifth of all U.S. malls have vacancy rates above 10%. This is increasingly due to a department store retrenchment, which is a trend we expect to continue. As such, the outlook for Class B and C malls is grim as pressures mount from multiple angles. We believe investors should generally avoid investing in REITs that have highly concentrated positions in these classes of malls. Having said that, it is worth noting how depressed these REITs are currently and, unlike with the overall stock market, some REITs look deeply undervalued.

The future for retailers leaning on legacy business practices in an evolving environment is likely grim. However, those willing to adapt to shifting consumer behaviors, reimagine physical storefronts, and adopt new technologies is bright. Many developments that we highlighted above (and some that we didn’t) will dictate the future of retail and separate the winners from losers.

The declaration that physical retail is dead is exaggerated. The reality is not that it’s dead, but that it’s undoubtedly (and very quickly) changing.

Michael Johnston

Marketing & Communications Manager

OUR CURRENT LIKES AND DISLIKES

Changes highlighted in BOLD.

LIKE

NEUTRAL

DISLIKE

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.