"Forget whether one is bullish or bearish, hawkish or dovish, a Central Bank with no credibility is dangerous."

-MIKE O’ROURKE, author of The Closing Print

POINTS TO PONDER

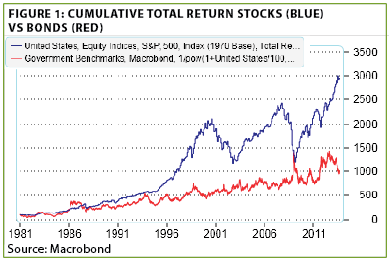

1. Four and a half years ago, during the worst bear market since the 1930s, a vocal chorus of chronically gloomy gurus was gleefully pointing out that bonds had beaten stocks over the prior 30 years. They further asserted that this disproved the theory that stocks produce superior long-term returns versus fixed income. Since then, stock values have gone vertical, creating an even greater return gap vis-à-vis bonds than in 2000. However, this should raise concerns about stocks being able to sustain this outperformance in the years ahead. (See Figure 1)

2. Gold stocks have been a wasteland for investors over the last two years. Unquestionably, a significant factor in this has been out-of-control production costs. The industry, though, is working hard to reduce expenses. Consequently, given scorched-earth valuations, if bullion prices rise, profits—and stock performance—might surprise on the upside.

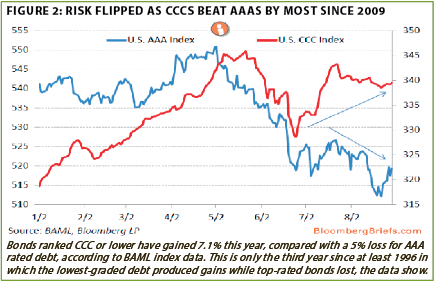

3. Demonstrating an abiding conviction in both "the riskier the better" investment thesis and that the US economy is poised to accelerate (making lower quality debt safer), the CCC tier of junk debt has bested AAA-rated debt by the largest margin since 2009. The earlier period was characterized by one of the most powerful rallies ever in the lowest rated corporate debt. (See Figure 2)

4. According to Simon Lack, author of The Hedge Fund Miracle, if all the money ever invested in hedge funds (roughly $1.8 trillion) had merely been parked in T-bills, investors would have, in the aggregate, realized returns double their gains from these costly and opaque vehicles.

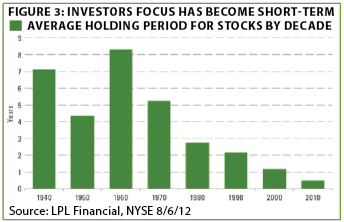

5. Long-term investors are increasingly becoming endangered species. Yet, with so many in the investment community short-term obsessed, it is logical that there are considerable opportunities for those with the discipline and courage to focus on a multi-year time horizon. (See Figure 3)

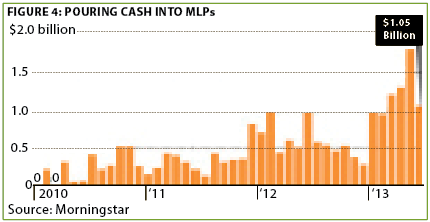

6. Master limited partnerships (MLPs) have been stellar performers this year after a lackluster 2012, generating a total return in excess of 20% so far in 2013. As usual, outsized returns are motivating Wall Street to bring out a flurry of MLP funds, producing an unsustainable buying spree. (See Figure 4)

7. One of the more sobering aspects of our so-called economic expansion is that since the Great Recession ended no year has seen US GDP exceed 2.4%. By contrast, from 1929 through 1941 (i.e., including the Great Depression), US GDP growth averaged 2.8%.

8. According to the Employee Benefit Research Institute, 57% of American workers have $25,000 or less in financial assets. This compares to 49% five years ago.

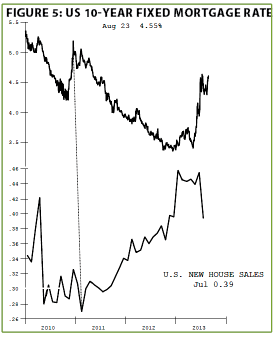

9. Those who believe that sharply higher long-term interest rates are having no impact on the real economy should analyze what is occurring with new home sales. (See Figures 5)

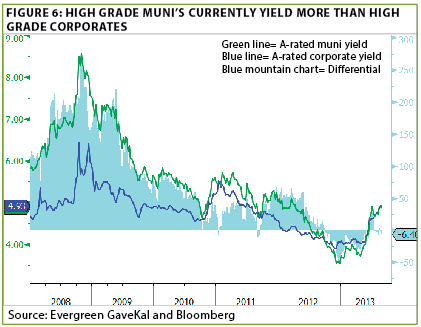

10. Corporate bond yields have risen materially since taper talk started in May. Even more depressed, and consequently more attractive on a return basis, are municipal bonds. Remarkably, A-rated intermediate-maturity munis now yield more than similarly rated and duration corporate. (See Figure 6)

11. Economic news out of Europe has been noticeably improved of late. Yet, the Continent has an enormous hole to dig itself out of, as underscored by the IMF’s forecast that Spain’s jobless rate won’t fall below 25% until 2018.

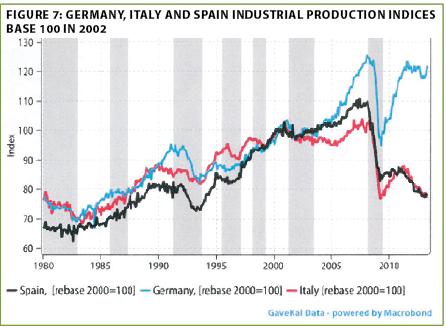

12. Most investors are aware that the performance of Italy’s and Spain’s manufacturing sectors has lagged Germany’s. Nonetheless, the magnitude of that deficiency is truly stunning. (See Figure 7)

13. According to the Financial Times, BRIC (Brazil, Russia, India, and China) bond funds have lost a breathtaking one-third of their asset bases to outflows since late May, highlighting the intense negativity toward developing country debt.

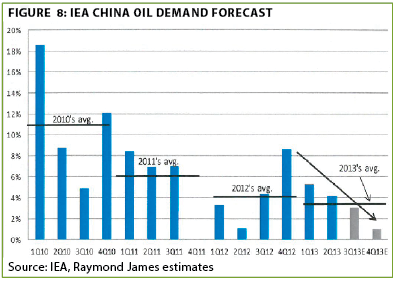

14. The latest spate of unrest in the Middle East has pushed oil prices well into the triple digits. A long-term "cooler" on crude prices, though, is the secular reduction in Chinese demand. (See Figure 8)

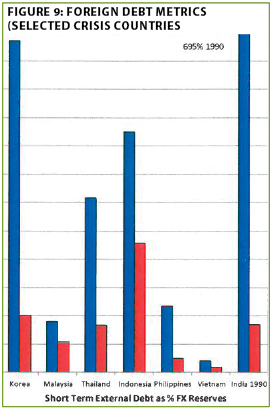

15. Emerging markets are enduring another of their regularly occurring crises. However, they have made enormous strides from their perilous condition in 1997, when the Asian crisis erupted. Short-term external debt as a percentage of foreign exchange reserves is much lower, while reserves relative to imports are also significantly improved. (See Figure 9)

Taper vapor. Baseball pundits are known to say that the defining difference between a major and minor league hitter is the ability to hit a curve ball. Yet, the toughest pitch to hit, the one that makes even the best big leaguer look foolish, is that fluttering phantom: the knuckleball. Appropriately, it is also one of the most difficult to throw, but on Wednesday, Ben Bernanke threw a perfect knuckleball at the financial markets, leaving them baffled and totally off balance.

Of slightly less significance, Mr. Bernanke's wicked pitch also caught me off guard. Like most observers, I did feel that a mild tapering would occur. Thus, I feel compelled to replace the EVA I had ready to go out today with this somewhat on-the-fly summary sent out, and I apologize in advance for any rough spots.

First of all, one recurring EVA theme this about-face seems to validate is that the US economy doesn’t have much ability to withstand the impact of higher interest rates. Among the reasons the Fed gave for deferring the taper, for which it had appeared to go out of its way since late May to prepare the markets, was: "the tightening of financial conditions observed in recent months, if sustained could slow the pace of improvement in the economy and the labor market."

What’s fascinating about this is that "the tightening of financial conditions" occurred at a time when the Fed has continued to inject roughly $300 billion into the system—not exactly your textbook tightening. But where the screws were being turned was in the longer term interest rate market. It appears clear now that the impact of 3% 10-year treasury yields, particularly on housing, alarmed the Fed.

Another major implication of this shocker, in my view, is that it further damages the credibility of the world’s most powerful central bank. Despite the initial stock market cheers when the Fed tapered not, the reality is that investors dislike uncertainty, including the kind that occurs when the Fed moves the goalposts. The Fed had also conditioned the investment community to focus on a falling unemployment rate as a lead indicator of when they would dial back their printing presses. On Wednesday, however, Mr. Bernanke said "There’s not any magic number we’re shooting for."

Wow! What happened to a 7% unemployment rate as Mr. Bernanke’s red line? Quite obviously, red lines don’t mean what they used to in Washington, D.C., these days.

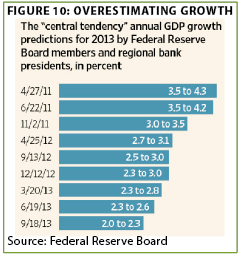

A third ramification of this change-of-heart is that, yet again, the long anticipated upside break-out by the US economy isn’t materializing. In fact, notwithstanding some encouraging economic data, especially the key Institute of Supply Managers’ (ISM) surveys, the Fed is once more cutting its growth forecast. For this year, it now sees GDP expansion of 2.2% versus 2.5% expected as recently as June. For 2014, its new forecast is for 3% growth versus 3.3% in June. This continues a discouraging pattern that has persisted in recent years. (See Figure 10)

Remarkably, there seems to be almost no acknowledgment at the highest levels of the Fed, at least as presently constituted, that binge-printing simply is self-defeating. Yet, the more time that elapses, and the more trillions that are whipped up out of the thinnest of air, with little to show for it, the more credulity accrues to those who have been warning of its impotence.

Speaking of which...or should it be whom?

Three wise men. Among the people I respect most when it comes to connecting the correct dots on the Fed’s unparalleled stimulus program are Charles Gave, Mike O’Rourke, and Grant Williams. Actually, there are several members of Team GaveKal, including Louis Gave, who have been warning that this grand experiment was destined to have a not-so-grand ending. But Charles is certainly the most prolific—and vitriolic—when it comes to his criticism of the latest central bank economic and market manipulation.

Charles has written repeatedly that the totally unintended consequence of the Fed’s addiction to QEs is that it actually lowers both growth and inflation; the exact opposite of what it has been striving to achieve. He notes that since last December, the Fed’s preferred inflation measure has been halved, with real interest rates (i.e., yields net of inflation) having soared. This in turn has pressured the economy, a reality the Fed is now clearly recognizing. In fact, Charles believes there is a whiff of panic emerging from the Fed of late (click here for Charles’ essay, A Panicked Fed Doubles Down).

Mike O’Rourke, who writes The Closing Print, absolutely one of the best daily recaps I receive, had a number of extremely trenchant comments on the Fed’s latest wimp-out (or, as characterized by both the Financial Times and the Wall Street Journal, its "blink"):

> "…the Fed has ‘a tiger by its tail’—it has lost control of monetary policy. It can’t stop buying assets because interest rates will rise and choke the recovery."

> "If the economy cannot handle a 3% yield on the 10 year (treasury), then the S&P 500 should not be north of 1700. It is remarkable that the equity market continued to buy into easy money over economic growth."

> "If the Fed has not already created an equity bubble (pushing asset prices well beyond where they would be otherwise be), then we would not be surprised if the Central Bank winds up doing so."

> "Thus, the question is—when will the market finally recognize that perpetual easy policy is a sign of weakness, not strength?"

> "It is hard not to think the Fed is doing the same thing over and over and expecting a different result."

> "He (Mr. Bernanke) has continually talked about a taper and eventual exit, but cannot even take a baby step forward."

As mentioned in last week’s EVA, one of the true shining stars in the financial newsletter firmament, Grant Williams, is in town. Wednesday night, over an adult beverage, I asked Grant what his take was on the Fed’s Big Blink. His response was almost a clone of Charles’ view, that the Fed is becoming panicky as their last perceived magic elixir of endless money manufacturing fails to do the trick.

Grant has long believed that the Fed, and other central banks following similar policies, will lose control of the bond market and eventually the overall financial markets. The wild rout in the fixed income world this summer would seem to validate his thesis.

He was also struck by the chutzpah of Mr. Bernanke, in his press conference after the official Fed conclave, who declared that there would be no rise in short-term interest rates until 2015 or 2016, at the earliest. Putting aside his rapidly diminishing credibility, it’s unprecedented for a "Fed head" almost certainly on his way out to essentially set monetary policy for his successor.

This morning, Grant was kind enough to relay some additional thoughts to me on the Taper Vapor even though he’s supposedly on holiday:

"The Fed has more information at their disposal than anybody and so their decisions are, quite literally, the best-informed of all. What does it say when the body in possession of the clearest data set feels it cannot withdraw even a paltry $10bn per month in stimulus after having done all the hard work in preparing markets for such an eventuality?

The cry of the skeptics (me amongst them) since the Taper Tantrum has been ‘...but they’re only going to taper by a small amount. That STILL leaves ~$70bn every month in asset purchases’. However, after this week’s ‘Bernanke Blink’ a rather more troubling question has emerged:

With everything they know, and understanding fully the damage to their credibility that NOT tapering would (and does entail, what is it the Fed sees in their data that means they feel they can’t even throw in a notional taper to preserve their credibility?"

That should frighten the most hardened equity bull....

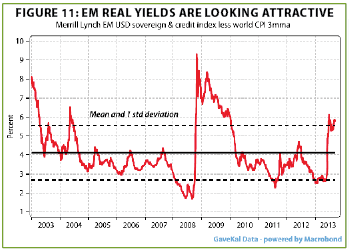

Don’t get mad, get global. So, what’s an investor to do based on this crazy pitch from the Fed? While the Evergreen GaveKal investment team is still evaluating this urgent question, we do think it’s logical that those asset classes most impaired by the "taper tantrum" might have the best snap-back potential. Emerging market debt, which EVA readers know we’ve been gradually accumulating over the summer, is a prime example. (See Figure 11)

The nuked wasteland known as municipal bonds is another. Per recent EVAs, when you can get tax-free yields above those of similar quality and maturity corporate bonds, you need to be extremely negative on the overall muni credit outlook not to be at least nibbling.

We also believe that overseas markets in general are the place to be for those seeking equity exposure and the higher return that should come with the increased risk (with the caveat that they’ve popped recently and are due for some consolidation). We continue to feel the US stock market, aside from a few pockets of value, like tech, offers an unattractive risk/reward ratio over the next five years (at least until the next market rout resets the calculus).

To end this week’s EVA, I thought I would include a flurry of charts from Mike O’Rourke that make it "high-def" clear just how much of an outlier the US stock market has been. Hmmm… in the entertainment world, "has-been" is a label nobody wants to have attached to them. But far worse than that is being labeled a "never-was."

Based on the Fed’s lack of action this week, perhaps there never was an intention to taper but simply a plan to take some steam out of equity and bond markets. Perhaps there never was any real proof of a truly strengthening economy. Or maybe, just maybe, there never was a plan at all and the Fed is simply being led by the nose through the turbulence surrounding them. Given how many times the Fed’s nose has led them in the wrong direction, the future could be downright smelly.

![]()

IMPORTANT DISCLOSURES

This report is for informational purposes only and does not constitute a solicitation or an offer to buy or sell any securities mentioned herein. This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. All of the recommendations and assumptions included in this presentation are based upon current market conditions as of the date of this presentation and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. Information contained in this report has been obtained from sources believed to be reliable, Evergreen Capital Management LLC makes no representation as to its accuracy or completeness, except with respect to the Disclosure Section of the report. Any opinions expressed herein reflect our judgment as of the date of the materials and are subject to change without notice. The securities discussed in this report may not be suitable for all investors and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. Investors must make their own investment decisions based on their financial situations and investment objectives.