"I don’t think the words ‘dual mandate’ crossed my lips in eight years. If prices are stable, that (is) good for employment."

- Paul Volcker, referring to his time as Fed chairman, in a speech this week to the Economic Club of NY

POINTS TO PONDER

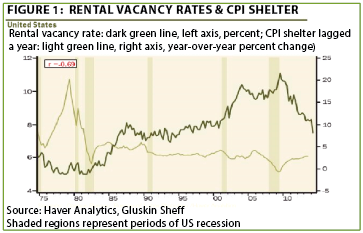

1. Inflation has moderated in the US recently, but one area that is likely to be a source of upward pressure is the cost of renting. With vacancy rates approaching 25-year lows, shelter costs have increased faster than the overall CPI. Rents may further accelerate based on the magnitude of the decline in vacancies. (See Figure 1.)

2. The Fed is maintaining one of the easiest monetary policies in American history, even though QE3 is nearly certain to end next month. This dovish stance is irrespective of dramatically improved employment conditions. Through the first eight months of this year, 2014 is second only to 2005 in terms of total job creation over the past 15 years.

3. There is no question that the labor market is robust for skilled workers. Unfortunately, however, disability seems to be highly contagious in America these days. The percentage of those who are not in the labor force between the ages of 25 and 54, due to illness or being disabled, has vaulted 30% from a year ago.

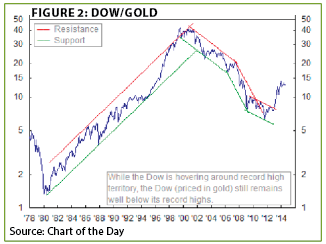

4. The Dow and the S&P 500 continue to attain new all-time highs almost daily, at least in US dollars. Interestingly, though, in gold terms, the Dow remains far lower than where it was trading fifteen years ago (as does the S&P). This is despite the extreme weakness in gold and the equally extreme strength in stocks over the last two and a half years. (See Figure 2.)

5. Reinforcing a key tenet from last week’s EVA about the heavy drag on economic growth as a result of a suffocating regulatory burden, think tank US Academics released a study estimating what America’s GDP would be if federal regulations had remained at 1949 levels. The total size of the US economy would be $56 trillion today, according to their estimates, versus the actual $17 trillion.

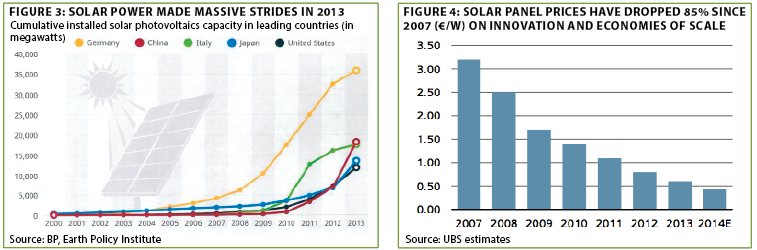

6. An EVA theme from 2008, when oil prices were nearing $150, and many pundits projected a run to $200, was that both new energy production techniques, such as horizontal drilling and fracking, would bring crude back down to double digits. We also opined that solar power was ready for prime time as panel prices were poised to see material declines. Based on total installed solar capacity in leading countries today versus then, that was a respectable forecast. (See Figures 3 and 4.)

7. Most economists and Wall Street strategists believe the global economy is "gaining traction." Yet, the International Energy Agency (IEA) just slashed its worldwide oil demand forecast by 900,000 barrels per day (bpd) for 2014 and 1,200,000 bpd for 2015. The IES characterized this consumption shortfall as "remarkable."

8. Numerous past EVAs have discussed Canada’s much stronger fiscal condition versus the US. In fairness, though, several important Canadian provinces, like Ontario, carry far higher debt levels than do US states. On the other hand, pension liability accounting in Canada appears considerably more conservative.

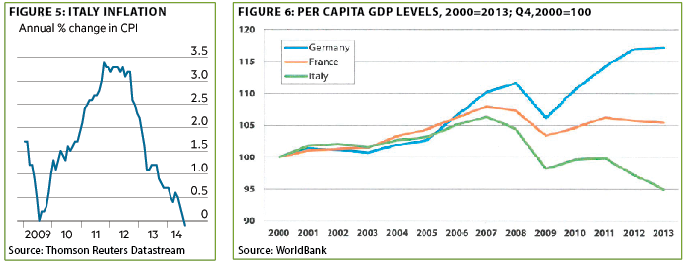

9. While there are myriad gloomy European data points to choose from, Italy is now facing deflation for the first time since 1959. This is in addition to a shocking plunge in GDP per capita relative to Germany (and even ossified France). (See Figures 5 and 6.)

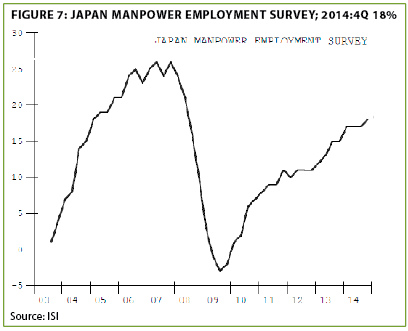

10. After a string of negative economic releases in the wake of its whopping sales tax increase, Japan has begun to report some better numbers. The recent weakness in its currency, at least versus the US dollar and the Korean won, may put a little more spring in the step of the "Land of the Setting Yen." (See Figure 7 below.)

THE EVERGREEN EXCHANGE

By David Hay, Tyler Hay, and Jeff Eulberg

The Great (Debt) Wall of China. One of the more amazing factoids I’ve come across recently pertains to China and its notoriously noxious air-quality. A seemingly logical partial solution to the problem is the Chinese government’s initiative to have 5,000,000 electric vehicles on the road by 2020. Yet, as pointed out in the September 14th Evergreen GaveKal Daily (click here to read), this effort has a slight problem. Due to the "tri-facta" that electric cars are 50% heavier than traditional vehicles, China’s power plants are 80% coal-fired, and its mostly primitive coal-based generation is exceedingly effluent-rich, an electric auto in Shanghai produces 19 times as much lethal PM2.5 pollution as a late-model gasoline powered vehicle! Accordingly, even if Teslas become the new go-to cars in China, the table to the right might look even worse.

But it’s not just the ubiquitous clouds of smog in its largest cities that smell in China these days. The Middle Kingdom’s property market, long a concern of this author, is also giving off an increasingly unpleasant stench. China bears (not to be confused with their beloved pandas) have been predicting a disaster in real estate for years, but the Evergreen view has been somewhat less apocalyptic.

It has been our belief that China’s immense foreign currency reserves and iron-fisted control over its banking system would prevent a US-style real estate cliff-dive. This stands in contrast to our extremely bearish view of Chinese stocks back in 2007, just before they crashed and burned in a financial market equivalent of the Hindenburg Disaster (and, in fact, they remain 60% below that level even today).

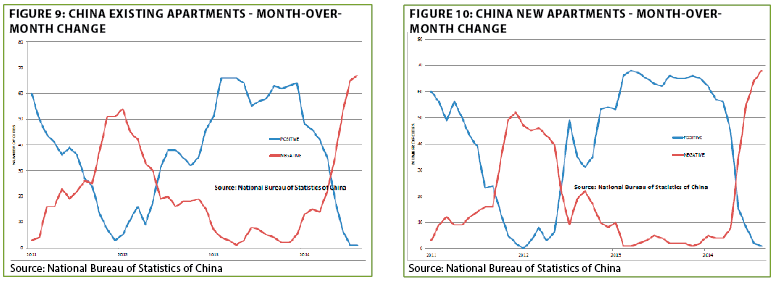

The reality is that, while there have been some tremors, China’s property market has held up reasonably well. But the facts on the ground do appear to be changing—and clearly not for the better. New condo prices are now falling in 68 out of 70 cities with existing units almost identically weak, down in 67 out of 70 markets.

This is likely why Chinese authorities have announced an $81 billion capital infusion into the top five banks. Interestingly, though, this is a loan, not actual equity—meaning leverage is not reduced. Considering that China has seen its overall debt-to-GDP ratio spike from 147% at the end of 2008 to 251% today, excessive debt is becoming a major issue.

Over this same timeframe, credit extensions by Chinese banks have gone viral with assets (typically loans) having swelled by a mammoth $14 trillion, roughly the size of the total US commercial banking sector, per Forbes.com columnist and the author of "The Coming Collapse of China," Gordon Chang. Yet, the additional debt is producing much more heat than light. According to China expert extraordinaire Simon Hunt, $1 of incremental debt in 2007 generated 83 cents of GDP. In 2013, though, the GDP gain was just 17 cents per $1 of added debt, with a mere 10 cents estimated for 2014. Consequently, it appears China may be hitting the same debt wall that most of the developed world did years ago.

According to Standard and Poor’s analysts Paul Gruenwald and Vincent Conti, this borrowing binge has "moved China from a position before the crisis where the financial sector was deemed to be reasonably sound to one where the fragility of the financial sector (as well as the sectors it has been financing, such as property) is seen as the biggest macro risk to China, if not the global economy."

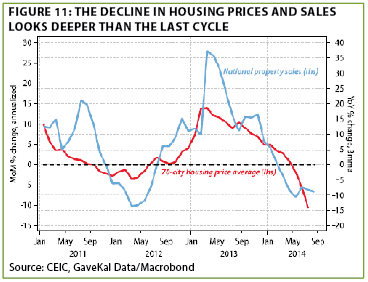

As with the overall economy, China’s property market is looking less and less responsive to larger doses of debt. Home sales and prices both peaked in early 2013 and, since then, they have been plunging at a rate akin to the popularity of NFL commissioner Roger Goodell (I’d sure like to be paid $44 million a year to make questionable decisions!). Both actually went negative at the start of this year with prices showing no signs of bottoming out.

Rumors are rife of desperate price stabilization measures by local governments in China, which have become highly reliant on fees and taxes on property development to fund their budget needs. Further, the publicly-traded real estate developers are feeling the strain. While their aggregate net worth is up a bouncy 250% since 2007, their debts have vaulted even more at 360%. And I suspect a lot of that equity increase is in the form of land that might not be worth what it’s being carried at on the books. Justifying my skepticism, three listed developers have recently done fire-sale capital raises (rights offerings) at 15% to 30% below their already depressed open market values.

Accordingly, time may be running out on China’s Herculean attempts to gently deflate its monstrously bloated real estate bubble. Don’t get me wrong—I’m not predicting a collapse of its economy or extreme social upheaval (certain countries in Europe would rank higher on my list in that regard!). Yet, if the property market in China has truly hit the bang point, that’s big news and it’s almost certain to ricochet around the world, as the S&P analysts quoted above suggest. You may have noticed the planet already has a few things out of kilter these days, even more than usual.

A huge advantage of command-control economies like China’s is that they are able to implement programs such as multi-trillion dollar stimulus initiatives with remarkable speed. The world should be grateful for China’s unparalleled splurge, which helped bring the global financial crisis to a quick conclusion. But, sometimes these fixes have serious unintended consequences—kind of like trying to reduce air pollution with electric vehicles. When the dust settles on China’s $14 trillion lending spree, and the related construction frenzy, we’ll likely see some bank balance sheets that are as toxic as Beijing’s air quality during a temperature inversion. And, if so, the odds are extremely high that it will make the $81 billion the Chinese government just injected into its banking system look like a modest down payment—with many more capital calls on the hazy horizon.

Federal Reserve mythology. There are two notions that seem to have become accepted Wall Street axioms regarding the Federal Reserve. First, is the seemingly inarguable phrase: "Don’t fight the Fed." The second is the belief that it effectively executes on its dual mandate of controlled inflation and maximum employment.

For as long as I can remember, our family road trips consisted of incessant quizzing on economic principles and random stock market factoids. You’d think that having grown up in a financially literate household that I would more naturally come to grips with what appear to be very simple financial principles. Unfortunately, I cannot. Instead, I find myself having an exceedingly difficult time accepting what so many have done with apparent ease.

Let’s start with "don’t fight the Fed." Famed bond maven Bill Gross (who just became even more famous today by leaving Pimco) has uttered this phrase frequently. In fact, it yields 95,700,000 results in a Google search. Popular author, Dennis Gartman, of the financial newsletter The Gartman Letter, calls it "one thing I’ve learned in 40 years." However, not fighting the Fed involves some implicit assumptions, a few of which strike me as shaky. For starters, you must believe that the Fed can actually influence markets as it sees appropriate. One would think a simple review of financial history would illustrate that the Fed hasn’t always got markets to behave accordingly. Unless, of course, ten years of economic despair from 1929-1939, double-digit inflation during the 1970s, a tech stock bubble that saw the Nasdaq drop 80%, and a historically unprecedented crash in home prices that almost broke the world’s financial system, were all part of a master plan that I’ve yet to appreciate. Perhaps I’m just naive, but this doesn’t appear to be my idea of control.

In recent years, we’ve seen the Fed tirelessly try to invent new monetary tools to stimulate the US economy. By almost any measure, economic growth (not to be confused with asset prices) has been anemic. Thinking back a little further, what would "don’t fight the Fed" have looked like when Alan Greenspan (aka the Maestro) said there was "no evidence" home prices could collapse or that "the worst may be over" for the housing market in October of 2006? Wouldn’t a "don’t fight the fed" mentality have considered a house to be a reasonable investment at basically the worst time in history? After all, warning in 2006, as we did repeatedly, that housing prices were extremely elevated would have been in conflict with the Fed chief’s view. Similarly, when Ben Bernanke called the sub-prime crisis "contained" a more disbelieving stance would likely have saved some serious portfolio losses (and Evergreen was very much in the disbeliever camp when he made that statement).

Talking about the past Fed chiefs could be water under the bridge. New chairwoman Janet Yellen is now running the show and she has her own agenda. Which brings me to my next point: What is her agenda? This is supposed to be a straightforward answer--a dual mandate, meaning stable prices and maximum unemployment. A more technical definition is provided here from the Federal Reserve Bank of Chicago’s website:

"The Board of Governors of the Federal Reserve System and the Federal Open Market Committee shall maintain long run growth of the monetary and credit aggregates commensurate with the economy’s long run potential to increase production, so as to promote effectively the goals of maximum employment, stable prices and moderate long-term interest rates."

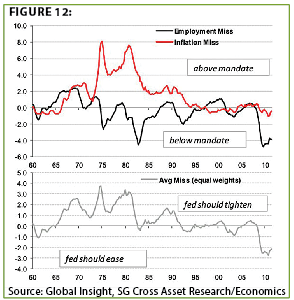

President Obama said his top criteria for naming Bernanke’s successor was someone who understood the dual mandate of stable prices and maximum employment. Yellen, too, has commented on the importance of the Fed’s dual mandate. However, a layman’s analysis of the chart below leads to one of two troubling conclusions.

The first conclusion is they are completely incapable of meeting a dual mandate with any meaningful consistency. The second, and more startling, conclusion is they might not even be trying these days. If the Fed isn’t following the dual mandate, what are they following? Originally, Yellen said unemployment under 6.5% was her prime goal. After that was met, the new barometer became some collection of economic data that I’ve yet to see articulated (how do you say "seats of the pants" in central bank-ese?) I’ve yet to find anyone who can explain to me the Fed’s objective and course for reaching it. Fed governor Stanley Fischer argued recently for a broadening of their mandate, which seems strange since they haven’t exactly executed flawlessly with "just" two.

In fairness, Yellen’s heart maybe in the right place trying to stoke the economy, while Washington D.C. is distracted as candidates reposition themselves for mid-terms. But serious reform, like we advocated in last week’s EVA, seems a long ways away. Of all people, Yellen should know by now that monetary tools are not a legitimate substitute for a broad spectrum of reforms. The longer we go without those, the deeper will be the hole in which we find ourselves. The deeper the Big Dig, the more blame there is to go around when the walls finally collapse. It’s my bet that she’s far less adept at blame avoidance than most of her neighbors in Washington, who have spent their careers elevating buck-passing to a fine art. Ms. Yellen might want to be prepared to take some advice from that philosopher king, Forrest Gump: "Run, Janet run!!"

The perils of keeping the faith. In the last Evergreen Exchange, I discussed the possible short-term ramifications of the new monetary policies being used by the European Central Bank (ECB). Today, I want to take a look at the potential long-term implications this policy could have on the global economy.

Mohammed El-Erian, one of the world’s most respected economists, and former CEO of Pimco Investments, recently spoke with Reuters on a variety of topics pertaining to the global markets. He stated in the interview that markets are currently placing an enormous amount of faith in the world’s central banks—especially their ability to divorce asset valuations from fundamentals. Market participants have seemingly forgotten that investing based on misguided faith is the same thinking that generated the two most recent bubbles in US markets. Investors in the tech bubble disregarded earnings because the growth of new technologies would eventually justify meteoric valuations. Then, in another broad decoupling from fundamentals, market participants convinced themselves that home prices would never decline. This caused credit conditions to loosen in a big way, allowing consumers to leverage up to unprecedented levels. Unfortunately, for those investing with complete disregard to fundamentals, asset prices did revert back in-line costing many dearly. Today, a fundamental reality check would mean the end of the monetary experiment employed by the world’s central banks. The multi-trillion dollar question is not if this will happen, but when.

When QE3 was announced in the summer of 2012, I was admittedly wrong in my belief that US investors would finally realize that central bank liquidity was doing little to support the US recovery. Economic data of late has improved, but it doesn’t justify the S&P’s roughly 40% return over that time period. The challenge for investors, especially those with short time horizons, is to avoid accepting the markets’ currently irrational behavior as a "new normal" environment. As we’ve seen time and time again, once a faith-based trade is exposed, fundamental realities take over and asset prices adjust quickly. Today the ECB is trying to spark its stagnant economy through new monetary tools. I’ve started to wonder: Is it possible I was right about the eventual end of the experiment, but wrong about the US market being the first to lose faith in the all-powerful Central Bank?

TLTR-Oh-no. Last week, the ECB started the first phase of the previously-announced Targeted Long-Term Refinancing Operation (TLTRO). The full program will provide loans of up to €800 billion to European banks in an effort to increase lending to small- and medium-sized companies in the European Union (EU). While it sounds great in theory, unfortunately, far fewer banks than expected showed up to take advantage of these loans. Of the €200 billion made available in the initial phase of the program, the actual number accessed was just €90.3 billion (estimates were around €180 billion). This had to be disheartening for Mario Draghi who likely thought this program could be a silver bullet for the ECB. The lackluster results must have stung even worse given that in 2012’s euro crisis, the initial long-term refinancing operation saw banks borrow close to €1 trillion from the ECB almost immediately.

But the optimists in Europe would argue against panicking. Banks will have another opportunity to borrow in December, and they could just be waiting to see October’s ECB stress test results to determine how much capital they’ll need to borrow. It is also possible banks are waiting for the end of the ECB’s asset-backed purchase program to see what collateral they have available to lend in the TLTRO. For me, this is the first sign that monetary policy won’t be enough to inflate asset prices in the EU. In the end, this would mean a big roll of the dice coming up snake eyes for the ECB.

To take a step back, our partners at Gavekal believe two negative scenarios (as well as one positive scenario they feel is unlikely) are possible for the EU. First, we could see a "Japanization" of the EU, leading to stagnate growth, major debt accumulation, and a constant battle with deflation. This is the likely outcome if the ECB continues to take a band-aid approach to monetary policy and no broad reforms are made in struggling EU countries. The second scenario, and one that would lead to a major slowdown in the global economy, would be an even more dramatic, European crisis. If the market fails to embrace ECB monetary policies, and stronger countries grow tired of supporting insolvent ones, an exit from the EU might become inevitable. In fact, that last point highlights one of the many reasons Scotland’s succession vote might have many ripple effects throughout the EU, even though it failed, as it encourages the various disolution movements.

Getting back to fundamentals. In Europe, Italian debt to GDP is at 136% and headed to 150% by 2015. Its economy is currently in its third recession since 2008. In Spain, the unemployment rate still exceeds 24% despite recent signs of life. And France continues to annually miss its overly optimistic budget targets. Since September 4, the day Mario Draghi officially announced the new policies, European stock markets are down. A reading in the red is a far cry from the normal reaction to increased central bank involvement. It’s clear the strength of European markets is rapidly deteriorating and economic fundamentals are going from bad to worse. The market may want Draghi to do more, but Germany is unlikely to agree. While Draghi and the ECB may be willing to do whatever it takes to keep the Euro together, Germany and other northern countries may not share their dedication. This could shatter the great euro monetary experiment, producing extreme turmoil in Europe. This prop of central bank involvement would be yanked out from under investors, forcing them to once again rely on fundamental valuations to determine asset prices. Of course, maybe this time market values won’t revert back to—or even below—their long-term averages. Right! And maybe Bill Gross will be given a going-away party at Pimco, too!

Important Disclosures

This report is for informational purposes only and does not constitute a solicitation or an offer to buy or sell any securities mentioned herein. This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. All of the recommendations and assumptions included in this presentation are based upon current market conditions as of the date of this presentation and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed. Information contained in this report has been obtained from sources believed to be reliable, Evergreen Capital Management LLC makes no representation as to its accuracy or completeness, except with respect to the Disclosure Section of the report. Any opinions expressed herein reflect our judgment as of the date of the materials and are subject to change without notice. The securities discussed in this report may not be suitable for all investors and are not intended as recommendations of particular securities, financial instruments or strategies to particular clients. Investors must make their own investment decisions based on their financial situations and investment objectives.