As Yogi Berra famously said, “it’s deja-vu all over again.” When I first started in the financial industry, asbestos-related civil suits had really kicked into gear. Companies were going bankrupt left and right because of asbestos exposure. Young analysts like myself were told to scour through lists of tickers, as the stock of any company with even a whiff of exposure to the toxic material would get slaughtered. It was very much a “shoot first, ask questions later” environment. Fast forward 30 years, and the same environment is prevalent again, this time with artificial intelligence replacing asbestos.

We recently touched on this new market development. Essentially, any business model linked to the organization, dissemination, or storage of “knowledge” has suddenly become extremely toxic. This is quite a reversal. At the start of this century, knowledge was by and large unaccounted for and so deeply undervalued. Then, over the following two decades, knowledge became the only asset worth focusing on. But suddenly, knowledge is perceived to be ubiquitous and essentially free. Rather than an asset, knowledge is almost a liability!

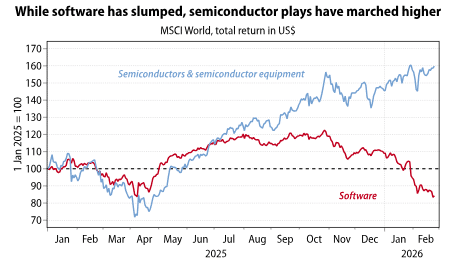

This sudden shift in perceptions explains why the stocks of knowledge companies—whether software, business processing or credit card payment systems—are suddenly finding no buyers. As I argued in early February, revolutions always end up eating their own children and it seems like the AI revolution may be no exception. All of which brings us to today’s market quandary: while software stocks can barely find a bid, semiconductor stocks continue to make new highs.

With the former (Microsoft, Oracle, IBM…) often the clients of the latter (Nvidia, AMD, SK Hynix…), this leaves investors facing a dilemma: if software stocks continue to struggle, will AI capex, on which the current valuation of semiconductor stocks depends, remain totally unconstrained?

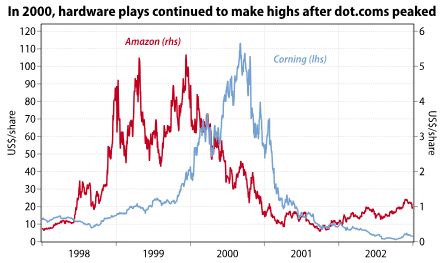

Staying on the Yogi Berra theme, today’s dichotomy is reminiscent of the market breakdown of the early 2000s. Back then, the internet was the disrupting force. However, by March 2000, dot.com companies were hitting the skids. Still, the companies building telecom networks (Corning, Cisco, JDSU, Sun Microsystems…) kept on soaring, and most made new all-time highs over the summer months. But by the time the school year restarted, it was obvious that with the dot.com companies out of cash, orders for the hardware providers were also drying up. Stocks duly tanked.

A historical precedent which leaves investors with three possible scenarios:

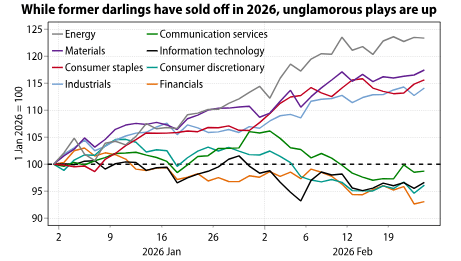

In the past few weeks, it has started to feel as if the market is beginning to shift from scenario #2 to scenario #3. Indeed, former investor darlings such as tech, communication services, financials or consumer discretionary stocks are now all down year to date. Meanwhile, industrials, staples, energy and materials have been ripping higher. It is as if the market is saying “I don’t know who will win or lose from AI, but I’m pretty confident that Exxon will continue to pump oil and sell gas, that P&G will sell shampoo, and Kimberly-Clark will sell diapers. These companies may not be exciting, but at least I am sure that they still will be here in a year’s time, and that their business will not be zero.”

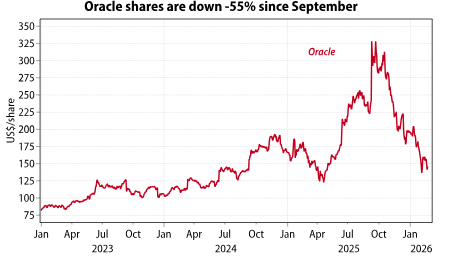

All of which brings us to a fairly obvious point: for most professional investors, the biggest fear of all is of investing in companies whose share prices end up worthless. Such an outcome is a much greater career risk than underperforming an index. So when massive companies like Oracle lose -55% of their market capitalization in five months, it sends shivers down spines. Suddenly, the quest becomes to avoid being the bag holder in the next roadkill company.

In short, the market zeitgeist is changing in front of our eyes. Portfolio managers are taking off the “offensive team” (knowledge companies) and putting on the defensive team (HALO). To reverse this will take good news on the tech front (much stronger than expected earnings from software companies? Large share buybacks?). However, the big risk is that the coming weeks will instead see some of the large hyperscale's (Microsoft? Amazon?) announce cuts in AI capex (perhaps to fund buybacks?). Such announcements would see the software sell-off spread to semiconductors. At that point, the Nasdaq and S&P 500 would most likely gap down…

DISCLOSURE: This material has been prepared or is distributed solely for informational purposes only and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any opinions, recommendations, and assumptions included in this presentation are based upon current market conditions, reflect our judgment as of the date of this presentation, and are subject to change. Past performance is no guarantee of future results. All investments involve risk including the loss of principal. All material presented is compiled from sources believed to be reliable, but accuracy cannot be guaranteed and Evergreen makes no representation as to its accuracy or completeness. Securities highlighted or discussed in this communication are mentioned for illustrative purposes only and are not a recommendation for these securities. Evergreen actively manages client portfolios and securities discussed in this communication may or may not be held in such portfolios at any given time.